Bridge financing is usually expected to be replaced within two years after the closing

date of the LBO transaction. True or False

Answer:

Purchaser-supplier relationships are also called logistics alliances. True or False

Answer:

Form of payment may consist of something other than cash, stock, or debt such as

tangible and intangible assets.

True or False

Answer:

In partnerships, the allocation of profits and losses among partners will normally follow

directly from the allocation of shares or partnership interests. True or False

Answer:

A planning-based acquisition process consists of both a business plan and acquisition

plan, which drive all subsequent phases of the acquisition process. True or False

Answer:

A section of the U.S. tax code known as 1031 forbids investors to make a “like kind”

exchange of investment properties. True or False

Answer:

The maximum purchase price is the minimum price plus the present value of sources of

value. True or False

Answer:

Individual investors can generally diversify their own stock portfolios more efficiently

than corporate managers who diversify the companies they manage. True or False

Answer:

Antitrust regulatory agencies may make their approval of a merger contingent on the

willingness of the merger partners to divest certain businesses. True or False

Answer:

U.S. antitrust regulatory authorities generally view the creation of R&D alliances

among businesses in the same industry as anticompetitive, even if the alliance shares its

research with all alliance participants. True or False

Answer:

Management may sell assets to fund diversification opportunities? True or False

Answer:

M&As can provide quick access to a new market; and, they are subject to fewer

problems than domestic M&As. True or False

Answer:

Many corporations, particularly large, highly diversified organizations, constantly are

reviewing ways in which they can enhance shareholder value by changing the

composition of their assets, liabilities, equity, and operations. True or False

Answer:

Coca Cola is an example of a company that pursues both a differentiation and cost

leadership strategy. True or False

Answer:

In the absence of earnings, other factors that drive the creation of value for a firm may

be used for valuation purposes. True or False

Answer:

A collection of markets is said to comprise an industry. True or False

Answer:

A transaction generally will be considered non-taxable to the seller or target firm’s

shareholder if it involves the purchase of the target’s stock or assets for substantially all

cash, notes, or some other nonequity consideration. True or False

Answer:

Insider trading involves buying or selling securities based on knowledge not available

to the general public. True or False

Answer:

Preferred stock often is issued in LBO transactions, because it provides investors a

fixed income security, which has a claim that is junior to common stock in the event of

liquidation. True or False

Answer:

LBOs can be of an entire company or divisions of a company. True or False

Answer:

Financial considerations, such as an acquirer believing the target is undervalued, a

booming stock market or falling interest rates, frequently drive surges in the number of

acquisitions. True or False

Answer:

So-called contract related transition issues often involve how the new employees will

be paid and what benefits they should receive. True or False

Answer:

In constructing the enterprise value, the market value of the firm’s common equity value

is added to the market value of the firm’s long-term debt and the market value of

preferred stock. True or False

Answer:

In an equity carve-out, the cash raised by the subsidiary in this manner may be

transferred to the parent as a dividend or as an inter-company loan. True or False

Answer:

Obtaining additional investment funds from others is the primary motivation for

creating various types of alliances. True or False

Answer:

In many countries, family owned firms have been successful because of their shared

interests and because investors place a higher value on short-term performance than on

the long-term health of the business. True or False

Answer:

Earnouts are generally very poor ways to create trust and often represent major

impediments to the integration process. True or False

Answer:

Antitrust regulators take into account the likelihood that a firm would fail and exit a

market if it is not allowed to merger with another firm. True or False

Answer:

If the discount rate is assumed to be 8% and the current cash flow is $1.5 million and is

expected to remain at that level in perpetuity, the implied valuation is $18.75 million.

True or False

Answer:

Only interest payments on ESOP loans are tax deductible by the firm sponsoring the

ESOP. True or False

Answer:

The so-called PEG ratio is calculated by dividing the firm’s price-to-earning ratio by the

expected growth rate in the firm’s share price. True or False

Answer:

Unlike other legal structures, a corporate structure does not have to be dissolved

because of the death of the owners or if one of the owners wish to liquidate their

ownership position.

True or False

Answer:

Whether an analyst should use a short or long-term interest rate for the risk free rate in

calculating the CAPM depends on when

the investor receives their future cash flows. True or False

Answer:

Which of the following statements best describes the business judgment rule?

a. Board members are expected to conduct themselves in a manner that could

reasonably be seen as being in the best interests of the shareholders.

b. Board members are always expected to make good decisions.

c. The courts are expected to ‘second guess’ decisions made by corporate boards.

d. Directors and managers are always expected to make good decisions.

e. Board decisions should be subject to constant scrutiny by the courts.

Answer:

Which of the following factors influences corporate governance practices?

a. Securities legislation

b. Government regulatory agencies

c. The threat of a hostile takeover

d. Institutional activism

e. All of the above

Answer:

Case Study. Private Equity Firms Acquire Yellow Pages Business

Qwest Communications agreed to sell its yellow pages business, QwestDex, to a

consortium led by the Carlyle Group and Welsh, Carson, Anderson and Stowe for $7.1

billion. In a two stage transaction, Qwest sold the eastern half of the yellow pages

business for $2.75 billion in late This portion of the business included directories in

Colorado, Iowa, Minnesota, Nebraska, New Mexico, South Dakota, and North Dakota.

The remainder of the business, Arizona, Idaho, Montana, Oregon, Utah, Washington,

and Wyoming, was sold for $4.35 billion in late 2003. Caryle and Welsh Carson each

put in $775 million in equity (about 21 percent of the total purchase price).

Qwest was in a precarious financial position at the time of the negotiation. The telecom

was trying to avoid bankruptcy and needed the first stage financing to meet impending

debt repayments due in late 2002. Qwest is a local phone company in 14 western states

and one of the nation’s largest long-distance carriers. It had amassed $26.5 billion in

debt following a series of acquisitions during the 1990s.

The Carlyle Group has invested globally, mainly in defense and aerospace businesses,

but it has also invested in companies in real estate, health care, bottling, and

information technology. Welsh Carson focuses primarily on the communications and

health care industries. While the yellow pages business is quite different from their

normal areas of investment, both firms were attracted by its steady cash flow. Such cash

flow could be used to trim debt over time and generate a solid return. The business’

existing management team will continue to run the operation under the new ownership.

Financing for the deal will come from J.P. Morgan Chase, Bank of America, Lehman

Brothers, Wachovia Securities, and Deutsche Bank. The investment groups agreed to a

two stage transaction to facilitate borrowing the large amounts required and to reduce

the amount of equity each buyout firm had to invest. By staging the purchase, the

lenders could see how well the operations acquired during the first stage could manage

their debt load.

The new company will be the exclusive directory publisher for Qwest yellow page

needs at the local level and will provide all of Qwest’s publishing requirements under a

fifty year contract. Under the arrangement, Qwest will continue to provide certain

services to its former yellow pages unit, such as billing and information technology,

under a variety of commercial services and transitional services agreements (Qwest:

2002).

Discussion Questions:

1) Why was QwestDex considered an attractive LBO candidate? Do you think it has

significant growth potential? Explain the following statement: “A business with high

growth potential may not be a good candidate for an LBO.

2) Why did the buyout firms want a 50-year contract to be the exclusive provider of

publishing services to Qwest Communications?

3) Why would the buyout firms want Qwest to continue to provide such services as

billing and information technology support? How might such services be priced?

4) Why would it take five very large financial institutions to finance the transactions?

5) Why was the equity contribution of the buyout firms as a percentage of the total

capital requirements so much higher than amounts contributed during the 1980s?

Answer:

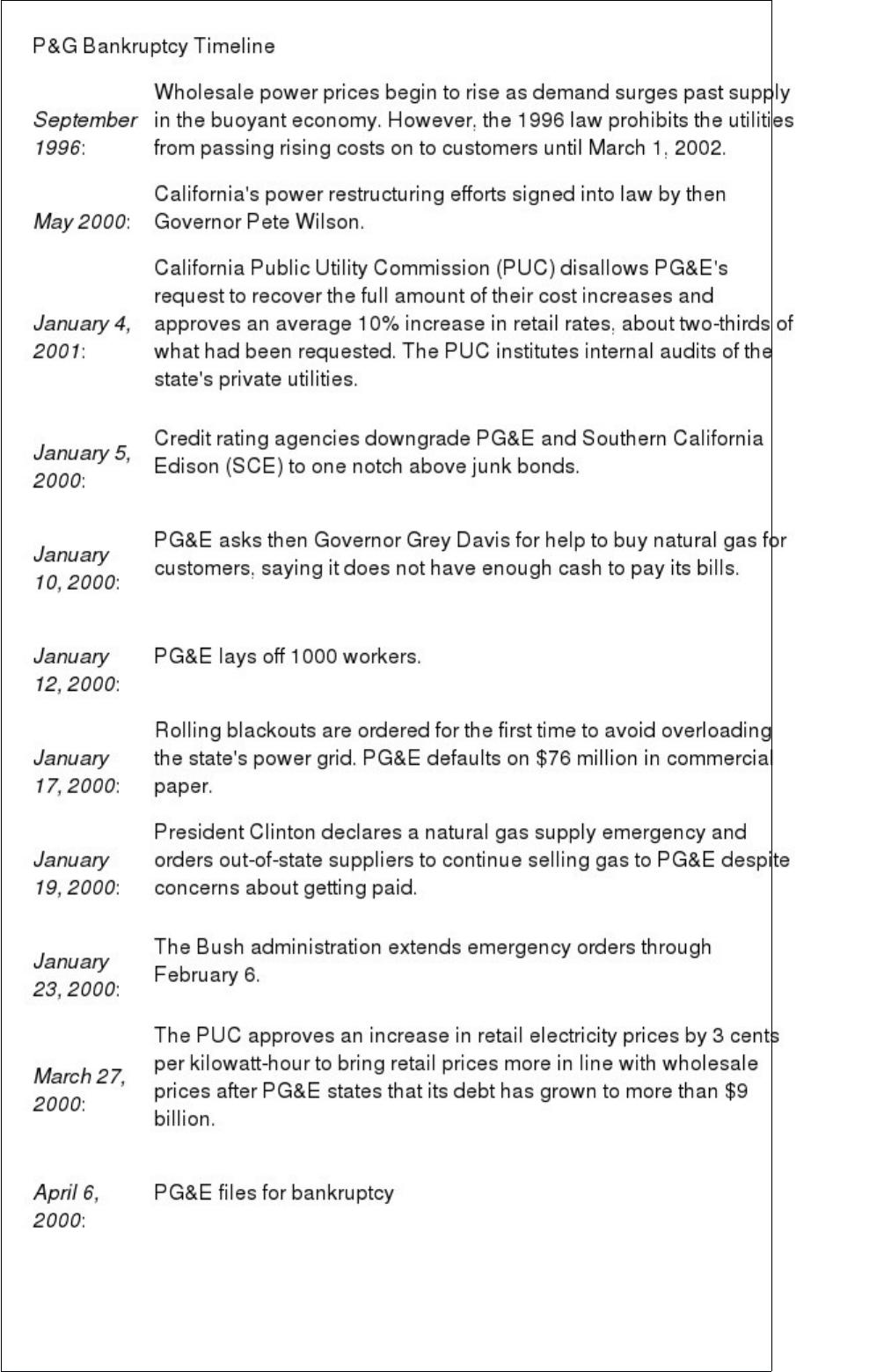

PG&E SEEKS BANKRUPTCY PROTECTION

Pacific, Gas, and Electric (PG&E), the San Francisco-based utility, filed for bankruptcy

on April 7, 2001, citing nearly $9 billion in debt and un-reimbursed energy costs. The

utility, one of three privately owned utilities in California, serves northern and central

California. The intention of the Chapter 11 reorganization was to make the utility

solvent again by protecting the firm from lawsuits or any other action by those who are

owed money by the utility. The bankruptcy will also allow the utility to deal with all of

the firm’s debts in a single forum rather than with individual debtors in what had

become a highly politicized venue. The following time line outlines the firm’s road to

bankruptcy.

Utility industry analysts saw PG&E’s move as largely an effort to escape the political

paralysis that had befallen the state’s regulatory apparatus. The bankruptcy filing came

one day after Governor Davis dropped his opposition to raising retail rates. However,

the Governor’s reversal came after five month’s of negotiations with the state’s privately

owned utilities on a rescue plan.

PG&E’s common shares fell 37 percent on the day the firm filed for reorganization.

Fearing a similar fate for San Diego Gas and Electric, the shares of Sempra Energy,

SDG&E’s parent corporation, also dropped by 35 percent

In an attempt to insulate California ratepayers from escalating wholesale electricity

prices, the state entered into a series of 5-to-10 year contracts with electricity power

generators that account for more than two-thirds of the state’s projected power needs.

The last contracts were signed by the state in June 2001. By September, a slowing

economy pushed the wholesale price of electricity well below the level the state was

required to pay in the “take or pay” contracts the state had just signed. Estimates

suggest that California taxpayers will have to pay between $40 and $45 billion in power

costs over the next decade depending on what happens to future energy costs. PG&E

has continued to supply its customers without disruption or blackout while being under

the protection of the bankruptcy court.

Southern California Edison, nearing bankruptcy for reasons similar to those that drove

PG&E to seek protection from its creditors, reached agreement with the Public Utility

Commission to pay off $3.3 billion in debt owed to power generators from customer

revenues. Previously, the PUC had forbid the utility to use monies generated from two

previous rate increases for this purpose. The U.S. District Court judge approved the

plan on October 5, 2001. While some creditors complained that the settlement was not

reassuring because it did not include a timetable for repayment of outstanding debt,

others viewed the agreement as a voluntary reorganization plan without going through

the expensive process of filing for bankruptcy with the federal court.

Discussion Questions:

1) In your judgment, did regulators attenuate or exacerbate the situation? Explain your

answer.

2) PG&E pursued bankruptcy protection, while Southern California Edison did not.

What could PG&E have been done differently to avoid bankruptcy?

Answer:

Which of the following are used by antitrust regulators to determine whether a proposed

transaction will be anti-competitive?

a. Market share

b. Barriers to entry

c. Number of substitute products

d. A and B only

e. A, B, and C

Answer:

Vertical mergers are likely to be challenged by antitrust regulators for all of the

following reasons except for

a. An acquisition by a supplier of a customer prevents the supplier’s competitors from

having access to the customer.

b. The relevant market has few customers and is highly concentrated

c. The relevant market has many suppliers.

d. The acquisition by a customer of a supplier could become a concern if it prevents the

customer’s competitors from having access to the supplier.

e. The suppliers’ products are critical to a competitor’s operations

Answer:

Which of the following is not true of taxable asset purchases?

a. Net operating losses carry over to the acquiring firm

b. The acquiring firm may step up its basis in the acquired assets.

c. The target firm is subject to recapture of tax credits and excess depreciation

d. Target firm shareholders’ are subject to a potential immediate tax liability

e. Target firm net operating losses and tax credits cannot be transferred to the acquiring

firm

Answer:

Moody’s credit rating agency defines instances of default as which of the following:

a. Missed or delayed payment of interest or principal

b. Bankruptcy

c. Receivership

d. Any exchange (equity for debt) diminishing the value of what is owed to bondholders

e. All of the above

Answer:

Which of the following are examples of business alliances?

a. Mergers

b. Acquisitions

c. Joint ventures

d. Equity partnerships

e. C and D

Answer:

Total consideration is a legal term referring to the composition of the purchase price

paid by the buyer for the target firm. It may consist of which of the following:

a. Cash

b. Cash and stock

c. Cash, stock, and debt

d. A, B, and C

e. A and B only

Answer:

Which of the following is generally not considered a source of value to the acquiring

firm?

a. Duplicate facilities

b. Patents

c. Land on the balance sheet at below market value

d. Warranty claims

e. Copyrights

Answer:

Which of the following is not true about integrating business alliances?

a. Teamwork is the underpinning that makes alliances work.

b. Control is best exerted through coordination

c. Decisions are made at the top of the organization

d. Decisions are based on the premise that all participants to the alliance have had an

opportunity to express their opinions.

e. The failure of one party to meet commitments will erode trust

Answer:

Pacific Surfware acquired Surferdude and as part of the transaction both of the firms

ceased to exist in their

form prior to the transaction and combined to create an entirely new entity, Wildly

Exotic Surfware. Which one of the following terms best describes this transaction?

a. Divestiture

b. Tender offer

c. Joint venture

d. Spinoff

e. Consolidation

Answer:

Which of the following are often participants in the acquisition process?

a. Investment bankers

b. Lawyers

c. Accountants

d. Proxy solicitors

e. All of the above

Answer:

Which of the following are common takeover tactics?

a. Bear hugs

b. Open market purchases

c. Tender offers

d. Litigation

e. All of the above

Answer:

Debt restructuring of a bankrupt firm is usually accomplished in which of the following

ways:

a. An extension

b. A composition

c. A debt for equity swap

d. Some combination of a, b, or c

e. All of the above

Answer:

Joe’s barber shop buys Jose’s Hair Salon. Which of the following terms best describes

this deal?

a. Joint venture

b. Strategic alliance

c. Horizontal

d. Vertical

e. Conglomerate

Answer:

Xon Enterprises is attempting to take over Rayon Group. Rayon’s shareholders have the

right to buy additional

shares at below market price if Xon (considered by Rayon’s board to be a hostile

bidder) buys more than 15 percent of Rayon’s outstanding shares. What term applies to

this antitakeover measure?

a. Share repellent plan

b. Golden parachute plan

c. Pac Man defense

d. Poison pill

e. Greenmail provision

Answer:

Antitrust regulatory authorities tend to look most favorably on which type of alliances?

a. Equity partnerships

b. Marketing alliances among competitors

c. Global alliances

d. Project oriented ventures involving collaborative research

e. None of the above

Answer:

Which of the following are the basic principles on which the market model is based?

a. Management incentives should be aligned with those of shareholders and other major

stakeholders

b. Transparency of financial statements

c. Equity ownership should be widely dispersed

d. A & B only

e. A, B, and C only

Answer:

Which of the following is not a characteristic of a joint venture corporation?

a. Profits and losses can be divided between the partners disproportionately to their

ownership shares.

b. New investors can become part of the JV corporation without having to dissolve the

original JV corporate structure.

c. The JV corporation can be used to acquire other firms.

d. Investors’ liability is limited to the extent of their investment.

e. The JV corporation may be subject to double taxation.

Answer:

The riskiness of highly leveraged transactions declines overtime due to which of the

following factors?

a. Debt reduction assuming nothing else changes

b. Increasing discount rates

c. A rising unlevered beta

d. An unchanging cost of equity

e. An unchanging weighted average cost of capital

Answer:

For a firm having common and preferred equity as well as debt, common equity value

can be estimated in which of the following ways?

a. By subtracting the book value of debt and preferred equity from the enterprise value

of the firm

b. By subtracting the market value of debt from the enterprise value of the firm

c. By subtracting the market value of debt and the market value of preferred equity

from the enterprise value of the firm

d. By adding the market value of debt and preferred equity to the enterprise value of the

firm

e. By adding the market value of debt and book value of preferred equity to the

enterprise value of the firm

Answer:

The purpose of a “fairness” opinion from an investment bank is

a. To evaluate for the target’s board of directors the appropriateness of a takeover offer

b. To satisfy Securities and Exchange Commission filing requirements

c. To support the buyer’s negotiation effort

d. To assist acquiring management in the evaluation of takeover targets

e. A and B

Answer:

An LBO can be valued from the perspective of which of the following?

a. Equity investors

b. Lenders

c. All those supplying funds to finance the transaction

d. A and B only

e. A, B, and C

Answer:

Which of the following is true of the enterprise valuation model?

a. Discounts free cash flow to the firm by the cost of equity

b. Discounts free cash flow to the firm by the weighted average cost of capital

c. Discounts free cash flow to equity by the cost of equity

d. Discounts free cash flow to equity by the weighted average cost of capital

e. None of the above

Answer:

Which of the following is not true of liquidity or marketability risk or discount?

a. It is measurable.

b. It is believed to have declined in recent years

c. The magnitude of the discount or risk is inversely related to the size of the investor’s

equity ownership in the business.

d. The magnitude of the discount or risk is directly related to the size of the investor’s

equity ownership in the business.

e. It is important to adjust the discount rate for liquidity risk.

Answer:

Which of the following represent common components of the global capital asset

pricing model when applied to valuing firms in emerging countries?

a. Risk free rate of return

b. Specific country’s risk premium

c. Firm size risk premium

d. Emerging country firm’s global beta

e. All of the above

Answer:

Inbev Acquires an American Icon

For many Americans, Budweiser is synonymous with American beer and American

beer is synonymous with Anheuser-Busch (AB). Ownership of the American icon

changed hands on July 14, 2008, when beer giant Anheuser Busch agreed to be

acquired by Belgian brewer InBev for $52 billion in an all-cash deal. The combined

firms would have annual revenue of about $36 billion and control about 25 percent of

the global beer market and 40 percent of the U.S. market. The purchase is the most

recent in a wave of consolidation in the global beer industry. The consolidation

reflected an attempt to offset rising commodity costs by achieving greater scale and

purchasing power. While likely to generate cost savings of about $1.5 billion annually

by 2011, InBev stated publicly that the transaction is more about the two firms being

complementary rather than overlapping.

The announcement marked a reversal from AB’s position the previous week when it

said publicly that the InBev offer undervalued the firm and subsequently sued InBev for

“misleading statements” it had allegedly made about the strength of its financing. To

court public support, AB publicized its history as a major benefactor in its hometown

area (St. Louis, Missouri). The firm also argued that its own long-term business plan

would create more shareholder value than the proposed deal. AB also investigated the

possibility of acquiring the half of Grupo Modelo, the Mexican brewer of Corona beer,

which it did not already own to make the transaction too expensive for InBev.

While it publicly professed to want a friendly transaction, InBev wasted no time in

turning up the heat. The firm launched a campaign to remove Anheuser’s board and

replace it with its own slate of candidates, including a Busch family member. However,

AB was under substantial pressure from major investors, including Warren Buffet, to

agree to the deal since the firm’s stock had been lackluster during the preceding several

years. In an effort to gain additional shareholder support, InBev raised its initial $65 bid

to $70. To eliminate concerns over its ability to finance the deal, InBev agreed to fully

document its credit sources rather than rely on the more traditional but less certain

credit commitment letters. In an effort to placate AB’s board, management, and the

myriad politicians who railed against the proposed transaction, InBev agreed to name

the new firm Anheuser-Busch InBev and keep Budweiser as the new firm’s flagship

brand and St. Louis as its North American headquarters. In addition, AB would be given

two seats on the board, including August A. Busch IV, AB’s CEO and patriarch of the

firm’s founding family. InBev also announced that AB’s 12 U.S. breweries would

remain open.

Discussion Questions:

1) Why would rising commodity prices spark industry consolidation?

2) Why would the annual cost savings not be realized until the end of the third year?

3) What is a friendly takeover? Speculate as to why it may have turned hostile?

4) InBev launched a proxy contest to take control of the Anheuser-Busch Board and

includes a Busch family member on its slate of candidates. The firm also raised its bid

from $65 to $40 and agreed to fully document its loan commitments. Explain how each

of these actions helped complete the transaction?

5) InBev agreed to name the new company Anheuser-Busch InBev, keep Budwieser

brand, maintain headquarters in St. Lous, and not to close any of the firm’s 12 breweries

in North America. How might these decisions impact InBev’s ability to realize projected

cost savings?

Answer:

Which one of the following is not a characteristic of a corporate legal structure?

a. Unlimited liability

b. Double taxation

c. Continuity of ownership

d. Managerial autonomy

e. Ease of raising money

Answer:

A steel maker acquired a coal mining company. Which of the following terms best

describes this deal?

a. Vertical

b. Conglomerate

c. Horizontal

d. Obtuse

e. Tender offer

Answer:

Adobe’s Acquisition of Omniture: Field of Dreams Marketing?

On September 14, 2009, Adobe announced its acquisition of Omniture for $1.8 billion

in cash or $21.50 per share. Adobe CEO Shantanu Narayen announced that the firm

was pushing into new business at a time when customers were scaling back on

purchases of the company’s design software. Omniture would give Adobe a steady

source of revenue and may mean investors would focus less on Adobe’s ability to

migrate its customers to product upgrades such as Adobe Creative Suite.

Adobe’s business strategy is to develop a new line of software that was compatible with

Microsoft applications. As the world’s largest developer of design software, Adobe

licenses such software as Flash, Acrobat, Photoshop, and Creative Suite to website

developers. Revenues grow as a result of increased market penetration and inducing

current customers to upgrade to newer versions of the design software.

In recent years, a business model has emerged in which customers can “rent” software

applications for a specific time period by directly accessing the vendors’ servers online

or downloading the software to the customer’s site. Moreover, software users have

shown a tendency to buy from vendors with multiple product offerings to achieve better

product compatibility.

Omniture makes software designed to track the performance of websites and online

advertising campaigns. Specifically, its Web analytic software allows its customers to

measure the effectiveness of Adobe’s content creation software. Advertising agencies

and media companies use Omniture’s software to analyze how consumers use websites.

It competes with Google and other smaller participants. Omniture charges customers

fees based on monthly website traffic, so sales are somewhat less sensitive than

Adobe’s. When the economy slows, Adobe has to rely on squeezing more revenue from

existing customers. Omniture benefits from the takeover by gaining access to Adobe

customers in different geographic areas and more capital for future product

development. With annual revenues of more than $3 billion, Adobe is almost ten times

the size of Omniture.

Immediately following the announcement, Adobe’s stock fell 5.6 percent to $33.62,

after having gained about 67 percent since the beginning of In contrast, Omniture

shares jumped 25 percent to $21.63, slightly above the offer price of $21.50 per share.

While Omniture’s share price move reflected the significant premium of the offer price

over the firm’s preannouncement share price, the extent to which investors punished

Adobe reflected widespread unease with the transaction.

Investors seem to be questioning the price paid for Omniture, whether the acquisition

would actually accelerate and sustain revenue growth, the impact on the future

cyclicality of the combined businesses, the ability to effectively integrate the two firms,

and the potential profitability of future revenue growth. Each of these factors is

considered next.

Adobe paid 18 times projected 2010 earnings before interest, taxes, depreciation, and

amortization, a proxy for operating cash flow. Considering that other Web acquisitions

were taking place at much lower multiples, investors reasoned that Adobe had little

margin for error. If all went according to plan, the firm would earn an appropriate return

on its investment. However, the likelihood of any plan being executed flawlessly is

problematic.

Adobe anticipates that the acquisition will expand its addressable market and growth

potential. Adobe anticipates significant cross-selling opportunities in which Omniture

products can be sold to Adobe customers. With its much larger customer base, this

could represent a substantial new outlet for Omniture products. The presumption is that

by combining the two firms, Adobe will be able to deliver more value to its customers.

Adobe plans to merge its programs that create content for websites with Omniture’s

technology. For designers, developers, and online marketers, Adobe believes that

integrated development software will streamline the creation and delivery of relevant

content and applications.

The size of the market for such software is difficult to gauge. Not all of Adobe’s

customers will require the additional functionality that would be offered. Google

Analytic Services, offered free of charge, has put significant pressure on Omniture’s

earnings. However, firms with large advertising budgets are less likely to rely on the

viability of free analytic services.

Adobe also is attempting to diversify into less cyclical businesses. However, both

Adobe and Omniture are impacted by fluctuations in the volume of retail spending.

Less retail spending implies fewer new websites and upgrades to existing websites,

which directly impacts Adobe’s design software business, and less advertising and retail

activity on electronic commerce sites negatively impacts Omniture’s revenues.

Omniture receives fees based on the volume of activity on a customer’s site.

Integrating the Omniture measurement capabilities into Adobe software design products

and cross-selling Omniture products into the Adobe customer base require excellent

coordination and cooperation between Adobe and Omniture managers and employees.

Achieving such cooperation often is a major undertaking, especially when the Omniture

shareholders, many of whom were employees, were paid in cash. The use of Adobe

stock would have given them additional impetus to achieve these synergies in order to

boost the value of their shares.

Achieving cooperation may be slowed by the lack of organizational integration of

Omniture into Adobe. Omniture will become a new business unit within Adobe, with

Omniture’s CEO, Josh James, joining Adobe as a senior vice president of the new

business unit. He will report to Narayen. This arrangement may have been made to

preserve Omniture’s corporate culture.

Adobe is betting that the potential increase in revenues will grow profits of the

combined firms despite Omniture’s lower margins. Whether the acquisition will

contribute to overall profit growth depends on which products contribute to future

revenue growth. The lower margins associated with Omniture’s products would slow

overall profit growth if the future growth in revenue came largely from Omniture’s Web

analytic products.

Discussion Questions:

1) Who are Adobe’s and Omniture’s customers and what are their needs?

2) What factors external to Adobe and Omniture seem to be driving the transaction? Be

specific.

3) What factors internal to Adobe and Omniture seem to be driving the transaction? Be

specific.

4) How would the combined firms be able to better satisfy these needs than the

competition?

5) Do you believe the transaction can be justified based on your understanding of the

strengths and weaknesses of the two firms and perceived opportunities and threats to

the two firms in the marketplace? Be specific.

Answer:

Financing LBOs–The SunGard Transaction

With their cash hoards accumulating at an unprecedented rate, there was little that

buyout firms could do but to invest in larger firms. Consequently, the average size of

LBO transactions grew significantly during 2005. In a move reminiscent of the

blockbuster buyouts of the late 1980s, seven private investment firms acquired 100

percent of the outstanding stock of SunGard Data Systems Inc. (SunGard) in late

SunGard is a financial software firm known for providing application and transaction

software services and creating backup data systems in the event of disaster. The

company’s software manages 70 percent of the transactions made on the Nasdaq stock

exchange, but its biggest business is creating backup data systems in case a client’s

main systems are disabled by a natural disaster, blackout, or terrorist attack. Its large

client base for disaster recovery and back-up systems provides a substantial and

predictable cash flow.

SunGard’s new owners include Silver lake Partners, Bain Capital LLC, The Blackstone

Group L.P., Goldman Sachs Capital Partners, Kohlberg Kravis Roberts & Co.,

Providence Equity Partners Inc. and Texas Pacific Group. Buyout firms in 2005 tended

to band together to spread the risk of a deal this size and to reduce the likelihood of a

bidding war. Indeed, with SunGard, there was only one bidder, the investor group

consisting of these seven firms.

The software side of SunGard is believed to have significant growth potential, while the

disaster-recovery side provides a large stable cash flow. Unlike many LBOs, the deal

was announced as being all about growth of the financial services software side of the

business. The deal is structured as a merger, since SunGard would be merged into a

shell corporation created by the investor group for acquiring SunGard. Going private,

allows SunGard to invest heavily in software without being punished by investors, since

such investments are expensed and reduce reported earnings per share. Going private

also allows the firm to eliminate the burdensome reporting requirements of being a

public company.

The buyout represented potentially a significant source of fee income for the investor

group. In addition to the 2 percent management fees buyout firms collect from investors

in the funds they manage, they receive substantial fee income from each investment

they make on behalf of their funds. For example, the buyout firms receive a 1 percent

deal completion fee, which is more than $100 million in the SunGard transaction.

Buyout firms also receive fees paid for by the target firm that is “going private” for

arranging financing. Moreover, there are also fees for conducting due diligence and for

monitoring the ongoing performance of the firm taken private. Finally, when the buyout

firms exit their investments in the target firm via a sale to a strategic buyer or a

secondary IPO, they receive 20 percent (i.e., so-called carry fee) of any profits.

Under the terms of the agreement, SunGard shareholders received $36 per share, a 14

percent premium over the SunGard closing price as of the announcement date of March

28, 2005, and 40 percent more than when the news first leaked about the deal a week

earlier. From the SunGard shareholders’ perspective, the deal is valued at $11.4 billion

dollars consisting of $10.9 billion for outstanding shares and “in-the-money” options

(i.e., options whose exercise price is less than the firm’s market price per share) plus

$500 million in debt on the balance sheet.

The seven equity investors provided $3.5 billion in capital with the remainder of the

purchase price financed by commitments from a lending consortium consisting of

Citigroup, J.P. Morgan Chase & Co., and Deutsche Bank. The purpose of the loans is to

finance the merger, repay or refinance SunGard’s existing debt, provide ongoing

working capital, and pay fees and expenses incurred in connection with the merger. The

total funds necessary to complete the merger and related fees and expenses is

approximately $11.3 billion, consisting of approximately $10.9 billion to pay SunGard’s

stockholders and about $400.7 million to pay fees and expenses related to the merger

and the financing arrangements. Note that the fees that are to be financed comprise

almost 4 percent of the purchase price. Ongoing working capital needs and capital

expenditures required obtaining commitments from lenders well in excess of $11.3

billion.

The merger financing consists of several tiers of debt and “credit facilities.” Credit

facilities are arrangements for extending credit. The senior secured debt and senior

subordinated debt are intended to provide “permanent” or long-term financing. Senior

debt covenants included restrictions on new borrowing, investments, sales of assets,

mergers and consolidations, prepayments of subordinated indebtedness, capital

expenditures, liens and dividends and other distributions, as well as a minimum interest

coverage ratio and a maximum total leverage ratio.

If the offering of notes is not completed on or prior to the closing, the banks providing

the financing have committed to provide up to $3 billion in loans under a senior

subordinated bridge credit facility. The bridge loans are intended as a form of temporary

financing to satisfy immediate cash requirements until permanent financing can be

arranged. A special purpose SunGard subsidiary will purchase receivables from

SunGard, with the purchases financed through the sale of the receivables to the lending

consortium. The lenders subsequently finance the purchase of the receivables by issuing

commercial paper, which is repaid as the receivables are collected. The special purpose

subsidiary is not shown on the SunGard balance sheet. Based on the value of

receivables at closing, the subsidiary could provide up to $500 million. The obligation

of the lending consortium to buy the receivables will expire on the sixth anniversary of

the closing of the merger.

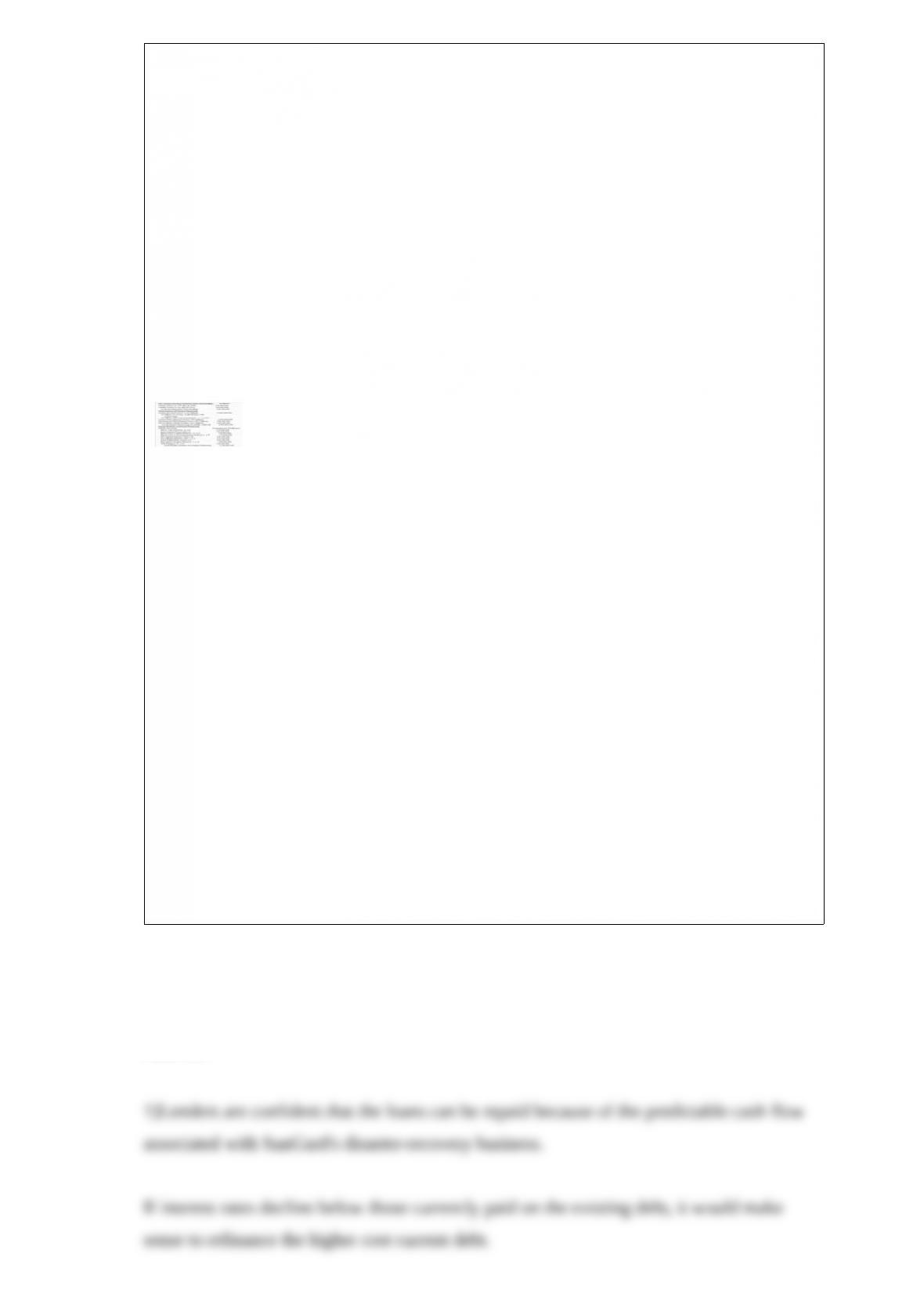

The following table provides SunGard’s post-merger proforma capital structure. Note

that the proforma capital structure is portrayed as if SunGard uses 100 percent of bank

lending commitments. Also, note that individual LBO investors may invest monies

from more than one fund they manage. This may be due to the perceived attractiveness

of the opportunity or the limited availability of money in any single fund. Of the $9

billion in debt financing, bank loans constitute 56 percent and subordinated or

mezzanine debt comprises represents 44 percent.

SunGard Proforma Capital Structure

1The roman numeral II refers to the fund providing the equity capital managed by

the partnership.

Case Study Discussion Questions:

1) SunGard is a software company with relatively few tangible assets. Yet, the ratio of

debt to equity of almost 5 to 1. Why do you think lenders would be willing to engage in

such a highly leveraged transaction for a firm of this type?

2) Under what circumstances would SunGard refinance the existing $500 million in

outstanding senior debt after the merger? Be specific.

3) In what ways is this transaction similar to and different from those that were

common in the 1980s? Be specific.

4) Why are payment-in-kind securities (e.g., debt or preferred stock) particularly well

suited for financing LBOs? Under what circumstances might they be most attractive to

lenders or investors?

5) Explain how the way in which the LBO is financed affects the way it is operated and

the timing of when equity investors choose to exit the business. Be specific.

Answer:

Promises to PeopleSoft’s Customers Complicate Oracle’s Integration Efforts

When Oracle first announced its bid for PeopleSoft in mid-2003, the firm indicated that

it planned to stop selling PeopleSoft’s existing software programs and halt any additions

to its product lines. This would result in the termination of much of PeopleSoft’s

engineering, sales, and support staff. Oracle indicated that it was more interested in

PeopleSoft’s customer list than its technology. PeopleSoft earned sizeable profit

margins on its software maintenance contracts, under which customers pay for product

updates, fixing software errors, and other forms of product support. Maintenance fees

represented an annuity stream that could improve profitability even when new product

sales are listless. However, PeopleSoft’s customers worried that they would have to go

through the costly and time-consuming process of switching software. To win customer

support for the merger and to avoid triggering $2 billion in guarantees PeopleSoft had

offered its customers in the event Oracle failed to support its products, Oracle had to

change dramatically its position over the next 18 months.

One day after reaching agreement with the PeopleSoft board, Oracle announced it

would release a new version of PeopleSoft’s products and would develop another

version of J.D. Edwards’s software, which PeopleSoft had acquired in 2003. Oracle

committed itself to support the acquired products even longer than PeopleSoft’s

guarantees would have required. Consequently, Oracle had to maintain programs that

run with database software sold by rivals such as IBM. Oracle also had to retain the

bulk of PeopleSoft’s engineering staff and sales and customer support teams.

Among the biggest beneficiaries of the protracted takeover battle was German software

giant SAP. SAP was successful in winning customers uncomfortable about dealing with

either Oracle or PeopleSoft. SAP claimed that its worldwide market share had grown

from 51 percent in mid-2003 to 56 percent by late 2004. SAP took advantage of the

highly public hostile takeover by using sales representatives, email, and an international

print advertising campaign to target PeopleSoft customers. The firm touted its

reputation for maintaining the highest quality of support and service for its products.

Discussion Questions

1) How did the commitments Oracle made to PeopleSoft’s customers have affected its

ability to realize anticipated synergies? Be specific.

2) Explain why Oracle’s willingness to pay such a high premium for PeopleSoft and its

willingness to change its position on supporting PeopleSoft products and retaining the

firm’s employees may have had a negative impact on Oracle shareholders. Be specific.

Answer:

McKesson HBOC Restates Revenue

McKesson Corporation, the nation’s largest drug wholesaler, acquired medical software

provider HBO & Co. in a $14.1 billion stock deal in early 1999. The transaction was

touted as having created the country’s largest comprehensive health care services

company. McKesson had annual sales of $18.1 billion in fiscal year 1998, and HBO &

Co. had fiscal 1998 revenue of $1.2 billion. HBO & Co. makes information systems

that include clinical, financial, billing, physician practice, and medical records software.

Charles W. McCall, the chair, president, and chief executive of HBO & Co., was named

the new chair of McKesson HBOC.

As one of the decade’s hottest stocks, it had soared 38-fold since early 1992.

McKesson’s first attempt to acquire HBO in mid-1998 collapsed following a news leak.

However, McKesson’s persistence culminated in a completed transaction in January

1999. In its haste, McKesson closed the deal even before an in-depth audit of HBO’s

books had been completed. In fact, the audit did not begin until after the close of the

1999 fiscal year. McKesson was so confident that its auditing firm, Deloitte & Touche,

would not find anything that it released unaudited results that included the impact of

HBO shortly after the close of the 1999 fiscal year on March 31, 1999. Within days,

indications that contracts had been backdated began to surface.

By May, McKesson hired forensic accountants skilled at reconstructing computer

records. By early June, the accountants were able to reconstruct deleted computer files,

which revealed a list of improperly recorded contracts. This evidence underscored

HBO’s efforts to deliberately accelerate revenues by backdating contracts that were not

final. Moreover, HBO shipped software to customers that they had not ordered, while

knowing that it would be returned. In doing so, they were able to boost reported

earnings, the company’s share price, and ultimately the purchase price paid by

McKesson.

In mid-July, McKesson announced that it would have to reduce revenue by $327

million and net income by $191.5 million for the past 3 fiscal years to correct for

accounting irregularities. The company’s stock had fallen by 48% since late April when

it first announced that it would have to restate earnings. McKesson’s senior

management had to contend with rebuilding McKesson’s reputation, resolving more

than 50 lawsuits, and attempting to recover $9.5 billion in market value lost since the

need to restate earnings was first announced. When asked how such a thing could

happen, McKesson spokespeople said they were intentionally kept from the due

diligence process before the transaction closed. Despite not having adequate access to

HBO’s records, McKesson decided to close the transaction anyway.

Discussion Questions:

1) Why do you think McKesson may have been in such a hurry to acquire HBO without

completing an appropriate due diligence?

2) Assume an audit had been conducted and HBO’s financial statements had been

declared to be in accordance with GAAP. Would McKesson have been justified in

believing that HBO’s revenue and profit figures were 100% accurate?

3) McKesson, a drug wholesaler, acquired HBO, a software firm. How do you think the

fact that the two firms were in different businesses may have contributed to what

happened?

4) Describe the measurable and non-measurable damages to McKesson’s shareholders

resulting from HBO’s fraudulent accounting activities.

Answer:

eBay Struggles to Reinvigorate Growth

Founded in September 1995, eBay views itself as the world’s online market place for

the sale of goods and services to a diverse community of individuals and small

businesses. Currently, eBay has sites in 24 different countries, and it offers a wide

variety of tools, features, and services enabling members to buy and sell on its sites.

The firm’s primary business is Markeplaces consisting of eBay, Shopping.com, and

classified websites. In 2006, this business accounted for 90 percent of eBay’s sales and

profits. Historically, acquisitions made by eBay have always been related to

e-commerce. For example, concern about slowing growth in its core U.S. market

caused eBay to acquire online payments provider, PayPal, in 2002. The firm achieved

significant synergy between eBay and PayPal by facilitating payments between buyers

and sellers.

In late 2005, eBay announced that it had acquired Skype International SA, a firm whose

software enabled PC users to make calls over the internet, for $2.6 billion. Skype had

revenue of $60 million in 2005, a tiny fraction of eBay’s $4.4 billion in 2005 sales, and

it was unprofitable. Skype’s existing businesses include services that give people the

ability to call landline phones for about 3 cents a minute, voicemail, and providing a

traditional phone number for Skype accounts. Skype is facing new competition from

Google, Yahoo!, and many startups.

eBay expects Skype to facilitate trade on their sites by increasing the ability of buyers

and sellers to negotiate. In addition to paying eBay listing and completed-auction fees,

sellers also could pay eBay a fee for getting an internet call, or lead, via Skype. eBay

will also use Skype to facilitate entering new markets, such as new cars, travel, real

estate, and personal and business services. Skype software gives eBay an advantage in

China, Eastern Europe and Brazil, where online trust is not well-established and where

haggling may be more a part of the culture.

The acquisition of a telephony company represented a marked departure for eBay,

which had previously acquired companies directly related to e-commerce. eBay is

venturing into new territory without any overt request from or support of its buyers and

sellers. Historically, buyers and sellers guided eBay into new markets through their

activities, such as embracing PayPal years before eBay acquired it, or by requesting

new features. In the past when eBAy has gone off on its own, such as collaborating with

Christy’s for live auctions, it has been unsuccessful. Only time will tell how well this

acquisition will work.

Discussion Questions:

1) Do you believe this acquisition if related or unrelated to eBay’s business? What are

the implications of your answer..

2) What are some of the key assumptions implicit in eBay’s decision to make this

acquisition?

Answer:

Cingular Acquires AT&T Wireless in a Record-Setting Cash Transaction

Cingular outbid Vodafone to acquire AT&T Wireless, the nation’s third largest cellular

telephone company, for $41 billion in cash plus $6 billion in assumed debt in February

2004. This represented the largest all-cash transaction in history. The combined

companies, which surpass Verizon Wireless as the largest U.S. provider, have a network

that covers the top 100 U.S. markets and span 49 of the 50 U.S. states. While Cingular’s

management seemed elated with their victory, investors soon began questioning the

wisdom of the acquisition.

By entering the bidding at the last moment, Vodafone, an investor in Verizon Wireless,

forced Cingular’s parents, SBC Communications and BellSouth, to pay a 37 percent

premium over their initial bid. By possibly paying too much, Cingular put itself at a

major disadvantage in the U.S. cellular phone market. The merger did not close until

October 26, 2004, due to the need to get regulatory and shareholder approvals. This

gave Verizon, the industry leader in terms of operating margins, time to woo away

customers from AT&T Wireless, which was already hemorrhaging a loss of subscribers

because of poor customer service. By paying $11 billion more than its initial bid,

Cingular would have to execute the integration, expected to take at least 18 months,

flawlessly to make the merger pay for its shareholders.

With AT&T Wireless, Cingular would have a combined subscriber base of 46 million,

as compared to Verizon Wireless’s 37.5 million subscribers. Together, Cingular and

Verizon control almost one half of the nation’s 170 million wireless customers. The

transaction gives SBC and BellSouth the opportunity to have a greater stake in the

rapidly expanding wireless industry. Cingular was assuming it would be able to achieve

substantial operating synergies and a reduction in capital outlays by melding AT&T

Wireless’s network into its own. Cingular expected to trim combined capital costs by

$600 to $900 million in 2005 and $800 million to $1.2 billion annually thereafter.

However, Cingular might feel pressure from Verizon Wireless, which was investing

heavily in new mobile wireless services. If Cingular were forced to offer such services

quickly, it might not be able to realize the reduction in projected capital outlays.

Operational savings might be even more difficult to realize. Cingular expected to save

$100 to $400 million in 2005, $500 to $800 million in 2006, and $1.2 billion in each

successive year. However, in view of AT&T Wireless’s continued loss of customers,

Cingular might have to increase spending to improve customer service. To gain

regulatory approval, Cingular agreed to sell assets in 13 markets in 11 states. The firm

would have six months to sell the assets before a trustee appointed by the FCC would

become responsible for disposing of the assets.

SBC and BellSouth, Cingular’s parents, would have limited flexibility in financing new

spending if it were required by Cingular. SBC and BellSouth each borrowed $10 billion

to finance the transaction. With the added debt, S&P put SBC, BellSouth, and Cingular

on credit watch, which often is a prelude in a downgrade of a firm’s credit rating.

Discussion Questions:

1) What is the total purchase price of the merger?

2) What are some of the reasons Cingular used cash rather than stock or some

combination to acquire AT&T Wireless? Explain your answer.

3) How might the amount and composition of the purchase price affect Cingular’s,

SBC’s, and BellSouth’s cost of capital?

4) With substantially higher operating margins than Cingular, what strategies would you

expect Verizon Wireless to pursue? Explain your answer.

Answer:

Calpine Emerges from the Protection of Bankruptcy Court

Following approval of its sixth Plan of Reorganization by the U.S. Bankruptcy Court

for the Southern District of New York, Calpine Corporation was able to emerge from

Chapter 11 bankruptcy on January 31, 2008. Burdened by excessive debt and court

battles with creditors on how to use its cash, the electric utility had sought Chapter 11

protection by petitioning the bankruptcy court in December 2005. After settlements

with certain stakeholders, all classes of creditors voted to approve the Plan of

Reorganization, which provided for the discharge of claims through the issuance of

reorganized Calpine Corporation common stock, cash, or a combination of cash and

stock to its creditors.

Shortly after exiting bankruptcy, Calpine cancelled all of its then outstanding common

stock and authorized the issuance of 485 million shares of reorganized Calpine

Corporation common stock for distribution to holders of unsecured claims. In addition,

the firm issued warrants (i.e., securities) to purchase 48.5 million shares of reorganized

Calpine Corporation common stock to the holders of the cancelled (i.e., previously

outstanding) common stock. The warrants were issued on a pro rata basis reflecting the

number of shares of “old common stock” held at the time of cancellation. These

warrants carried an exercise price of $23.88 per share and expired on August 25, 2008.

Relisted on the New York Stock Exchange, the reorganized Calpine Corporation

common stock began trading under the symbol CPN on February 7, 2008, at about $18

per share.

The firm had improved its capital structure while in bankruptcy. On entering

bankruptcy, Calpine carried $17.4 billion of debt with an average interest rate of 10.3

percent. By retiring unsecured debt with reorganized Calpine Corporation common

stock and selling certain assets, Calpine was able to repay or refinance certain project

debt, thereby reducing the prebankruptcy petition debt by approximately $7 billion. On

exiting bankruptcy, Calpine negotiated approximately $7.3 billion of secured “exit

facilities” (i.e., credit lines) from Goldman Sachs, Credit Suisse, Deutsche Bank, and

Morgan Stanley. About $6.4 billion of these funds were used to satisfy cash payment

obligations under the Plan of Reorganization. These obligations included the repayment

of a portion of unsecured creditor claims and administrative claims, such as legal and

consulting fees, as well as expenses incurred in connection with the “exit facilities” and

immediate working capital requirements. On emerging from Chapter 11, the firm

carried $10.4 billion of debt with an average interest rate of 8.1 percent.

The Enron ShuffleA Scandal to Remember

What started in the mid-1980s as essentially a staid “old-economy” business became the

poster child in the late 1990s for companies wanting to remake themselves into

“new-economy” powerhouses. Unfortunately, what may have started with the best of

intentions emerged as one of the biggest business scandals in U.S. history. Enron was

created in 1985 as a result of a merger between Houston Natural Gas and Internorth

Natural Gas. In 1989, Enron started trading natural gas commodities and eventually

became the world’s largest buyer and seller of natural gas. In the early 1990s, Enron

became the nation’s premier electricity marketer and pioneered the development of

trading in such commodities as weather derivatives, bandwidth, pulp, paper, and

plastics. Enron invested billions in its broadband unit and water and wastewater system

management unit and in hard assets overseas. In 2000, Enron reported $101 billion in

revenue and a market capitalization of $63 billion.

The Virtual Company

Enron was essentially a company whose trading and risk management business strategy

was built on assets largely owned by others. The complex financial maneuvering and

off-balance-sheet partnerships that former CEO Jeffrey K. Skilling and chief financial

officer Andrew S. Fastow implemented were intended to remove everything from

telecommunications fiber to water companies from the firm’s balance sheet and into

partnerships. What distinguished Enron’s partnerships from those commonly used to

share risks were their lack of independence from Enron and the use of Enron’s stock as

collateral to leverage the partnerships. If Enron’s stock fell in value, the firm was

obligated to issue more shares to the partnership to restore the value of the collateral

underlying the debt or immediately repay the debt. Lenders in effect had direct recourse

to Enron stock if at any time the partnerships could not repay their loans in full. Rather

than limiting risk, Enron was assuming total risk by guaranteeing the loans with its

stock.

Enron also engaged in transactions that inflated its earnings, such as selling time on its

broadband system to a partnership at inflated prices at a time when the demand for

broadband was plummeting. Enron then recorded a substantial profit on such

transactions. The partnerships agreed to such transactions because Enron management

seems to have exerted disproportionate influence in some instances over partnership

decisions, although its ownership interests were very small, often less than 3 percent.

Curiously, Enron’s outside auditor, Arthur Andersen, had a dual role in these

partnerships, collecting fees for helping to set them up and auditing them.

Time to Pay the Piper

At the time the firm filed for bankruptcy on December 2, 2001, it had $13.1 billion in

debt on the books of the parent company and another $18.1 billion on the balance

sheets of affiliated companies and partnerships. In addition to the partnerships created

by Enron, a number of bad investments both in the United States and abroad

contributed to the firm’s malaise. Meanwhile, Enron’s core energy distribution business

was deteriorating. Enron was attempting to gain share in a maturing market by paring

selling prices. Margins also suffered from poor cost containment.

Dynegy Corp. agreed to buy Enron for $10 billion on November 2, 2001. On November

8, Enron announced that its net income would have to be restated back to 1997,

resulting in a $586 million reduction in reported profits. On November 15, chairman

Kenneth Lay admitted that the firm had made billions of dollars in bad investments.

Four days later, Enron said it would have to repay a $690 million note by

mid-December and it might have to take an additional $700 million pretax charge. At

the end of the month, Dynegy withdrew its offer and Enron’s credit rating was reduced

to junk bond status. Enron was responsible for another $3.9 billion owed by its

partnerships. Enron had less than $2 billion in cash on hand.

The end came quickly as investors and customers completely lost faith in the energy

behemoth as a result of its secrecy and complex financial maneuvers, forcing the firm

into bankruptcy in early December. Enron’s stock, which had reached a high of $90 per

share on August 17, 2001, was trading at less than $1 by December 5, 2001.

In addition to its angry creditors, Enron faced class-action lawsuits by shareholders and

employees, whose pensions were invested heavily in Enron stock. Enron also faced

intense scrutiny from congressional committees and the U.S. Department of Justice. By

the end of 2001, shareholders had lost more than $63 billion from its previous 52-week

high, bondholders lost $2.6 billion in the face value of their debt, and banks appeared to

be at risk on at least $15 billion of credit they had extended to Enron. In addition,

potential losses on uncollateralized derivative contracts totaled $4 billion. Such

contracts involved Enron commitments to buy various types of commodities at some

point in the future.

Questions remain as to why Wall Street analysts, Arthur Andersen, federal or state

regulatory authorities, the credit rating agencies, and the firm’s board of directors did

not sound the alarm sooner. It is surprising that the audit committee of the Enron board

seems to have somehow been unaware of the firm’s highly questionable financial

maneuvers. Inquiries following the bankruptcy declaration seem to suggest that the

audit committee followed all the rules stipulated by federal regulators and stock

exchanges regarding director pay, independence, disclosure, and financial expertise.

Enron seems to have collapsed in part because such rules did not do what they were

supposed to do. For example, paying directors with stock may have aligned their

interests with shareholders, but it also is possible to have been a disincentive to question

aggressively senior management about their financial dealings.

The Lessons of Enron

Enron may be the best recent example of a complete breakdown in corporate

governance, a system intended to protect shareholders. Inside Enron, the board of

directors, management, and the audit function failed to do the job. Similarly, the firm’s

outside auditors, regulators, credit rating agencies, and Wall Street analysts also failed

to alert investors. What seems to be apparent is that if the auditors fail to identify

incompetence or fraud, the system of safeguards is likely to break down. The cost of

failure to those charged with protecting the shareholders, including outside auditors,

analysts, credit-rating agencies, and regulators, was simply not high enough to ensure

adequate scrutiny.

What may have transpired is that company managers simply undertook aggressive

interpretations of accounting principles then challenged auditors to demonstrate that

such practices were not in accordance with GAAP accounting rules (Weil, 2002). This

type of practice has been going on since the early 1980s and may account for the

proliferation of specific accounting rules applicable only to certain transactions to

insulate both the firm engaging in the transaction and the auditor reviewing the

transaction from subsequent litigation. In one sense, the Enron debacle represents a

failure of the free market system and its current shareholder protection mechanisms, in

that it took so long for the dramatic Enron shell game to be revealed to the public.

However, this incident highlights the remarkable resilience of the free market system.

The free market system worked quite effectively in its rapid imposition of discipline in

bringing down the Enron house of cards, without any noticeable disruption in energy

distribution nationwide.

Epilogue

Due to the complexity of dealing with so many types of creditors, Enron filed its plan

with the federal bankruptcy court to reorganize one and a half years after seeking

bankruptcy protection on December 2, The resulting reorganization has been one of the

most costly and complex on record, with total legal and consulting fees exceeding $500

million by the end of 2003. More than 350 classes of creditors, including banks,

bondholders, and other energy companies that traded with Enron said they were owed

about $67 billion.

Under the reorganization plan, unsecured creditors received an estimated 14 cents for

each dollar of claims against Enron Corp., while those with claims against Enron North

America received an estimated 18.3 cents on the dollar. The money came in cash

payments and stock in two holding companies, CrossCountry containing the firm’s

North American pipeline assets and Prisma Energy International containing the firm’s

South American operations.

After losing its auditing license in 2004, Arthur Andersen, formerly among the largest

auditing firms in the world, ceased operation. In 2006, Andrew Fastow, former Enron

chief financial officer, and Lea Fastow plead guilty to several charges of conspiracy to

commit fraud. Andrew Fastow received a sentence of 10 years in prison without the

possibility of parole. His wife received a much shorter sentence. Also in 2006, Enron

chairman Kenneth Lay died while awaiting sentencing, and Enron president Jeffery

Skilling received a sentence of 24 years in prison.

Citigroup agreed in early 2008 to pay $1.66 billion to Enron creditors who lost money

following the collapse of the firm. Citigroup was the last remaining defendant in what

was known as the Mega Claims lawsuit, a bankruptcy lawsuit filed in 2003 against 11

banks and brokerages. The suit alleged that, with the help of banks, Enron kept

creditors in the dark about the firm’s financial problems through misleading accounting

practices. Because of the Mega Claims suit, creditors recovered a total of $5 billion or

about 37.4 cents on each dollar owed to them. This lawsuit followed the settlement of a

$40 billion class action lawsuit by shareholders, which Citicorp settled in June 2005 for

$2 billion.

Case Study Discussion Questions:

1) In your judgment, what were the major factors contributing to the demise of Enron?

Of these factors, which were the most important?

2) In what way was the Enron debacle a break down in corporate governance

(oversight)? Explain your answer.

3) How were the Enron partnerships used to hide debt and inflate the firm’s earnings?

Should partnership structures be limited in the future? If so, how?

4) What should (or can) be done to reduce the likelihood of this type of situation arising

in the future? Be specific.

Answer:

Justice Department Blocks Microsoft’s Acquisition of Intuit

In 1994, Bill Gates saw dominance of the personal financial software market as a means

of becoming a central player in the global financial system. Critics argued that, by

dominating the point of access (the individual personal computer) to online banking,

Microsoft believed that it may be possible to receive a small share of the value of each

of the billions of future personal banking transactions once online banking became the

norm. With a similar goal in mind, Intuit was trying to have its widely used financial

software package, Quicken, incorporated into the financial standards of the global

banking system. In 1994, Intuit had acquired the National Payment Clearinghouse Inc.,

an electronic bill payments system integrator, to help the company develop a

sophisticated payments system. By 1995, Intuit had sold more than 7 million copies of

Quicken and had about 300,000 bank customers using Quicken to pay bills

electronically. In contrast, efforts by Microsoft to penetrate the personal financial

software market with its own product, Money, were lagging badly. Intuit’s product,

Quicken, had a commanding market share of 70% compared to Microsoft’s 30%.

In 1994 Microsoft made a $1.5 billion offer for Intuit. Eventually, it would increase its

offer to $2 billion. To appease its critics, it offered to sell its Money product to Novell

Corporation. Almost immediately, the Justice Department challenged the merger, citing

its concern about the anticompetitive effects on the personal financial software market.

Specifically, the Justice Department argued that, if consummated, the proposed

transaction would add to the dominance of the number-one product Quicken, weaken

the number two-product (Money), and substantially increase concentration and reduce

competition in the personal finance/checkbook software market. Moreover, the DoJ

argued that there would be few new entrants because competition with the new Quicken

would be even more difficult and expensive.

Microsoft and its supporters argued that government interference would cripple

Microsoft’s ability to innovate and limit its role in promoting standards that advance the

whole software industry. Only a MicrosoftIntuit merger could create the critical mass

needed to advance home banking. Despite these arguments, the regulators would not

relent on their position. On May 20, 1995, Microsoft announced that it was

discontinuing efforts to acquire Intuit to avoid expensive court battle with the Justice

Department.

Discussion Questions:

1) Explain how Microsoft’s acquisition of Intuit might limit the entry of new

competitors into the

financial software market.

2) How might the proliferation of Internet usage in the twenty-first century change your

answer

to question 1?

3) Do you believe that the FTC might approve of Microsoft acquiring Intuit today?

Why or why

not?

Answer:

Baxter to Spin Off Heart Care Unit

Baxter International Inc. announced in late 1999 its intention to spin off its

underperforming cardiovascular business, creating a new company that will specialize

in treatments for heart disease. The new company will have 6000 employees worldwide

and annual revenue in excess of $1 billion. The unit sells biological heart valves

harvested from pigs and cows, catheters and other products used to monitor hearts

during surgery, and heart-assist devices for patients awaiting surgery. Baxter conceded

that they have been ”optimizing” the cardiovascular business by not making the

necessary investments to grow the business. In contrast, the unit’s primary competitors,

Guidant, Medtronic, and Boston Scientific, are spending more on research and

investing more on start-up companies that are developing new technologies than is

Baxter.

With the spin-off, the new company will have the financial resources that formerly had

been siphoned off by the parent, to create an environment that will more directly

encourage the speed and innovation necessary to compete effectively in this industry.

The unit’s stock will be used to provide additional incentive for key employees and to

serve as a means of making future acquisitions of companies necessary to extend the

unit’s product offering.

Discussion Questions

1) In your judgment, what did Baxter’s management mean when they admitted that they

had not been “optimizing” the cardiovascular business in recent years? Explain both the

strategic and financial implications of this strategy.

2) Discuss some of the reasons why you believe the unit may prosper more as an

independent operation than as part of Baxter?

Answer:

Johnson & Johnson Sues Amgen

In 1999, Johnson & Johnson (J&J) sued Amgen over their 14-year alliance to sell a

blood-enhancing treatment called erythropoietin. The disagreement began when

unforeseen competitive changes in the marketplace and mistrust between the partners

began to strain the relationship. The relationship had begun in the mid-1980s with J&J

helping to commercialize Amgen’s blood-enhancing treatment, but the partners ended

up squabbling over sales rights and a spin-off drug.

J&J booked most of the sales of its version of the $3.7 billion medicine by selling it for

chemotherapy and other broader uses, whereas Amgen was left with the relatively

smaller dialysis market. Moreover, the companies could not agree on future products

for the JV. Amgen won the right in arbitration to sell a chemically similar medicine that

can be taken weekly rather than daily. Arbitrators ruled that the new formulation was

different enough to fall outside the licensing pact between Amgen and J&J.

Case Study Discussion Questions

1) What could these companies have done before forming the alliance to have mitigated

the problems that arose after the alliance was formed? Why do you believe they may

have avoided addressing these issues at the outset?

2) What types of mechanisms could be used other than litigation to resolve such

differences once they arise?

Answer:

Consolidation in the Global Pharmaceutical Industry:

The Glaxo Wellcome and SmithKline Beecham Example

By the mid-1980s, demands from both business and government were forcing

pharmaceutical companies to change the way they did business. Increased government

intervention, lower selling prices, increased competition from generic drugs, and

growing pressure for discounting from managed care organizations such as health

maintenance and preferred provider organizations began to squeeze drug company

profit margins. The number of contact points between the sales force and the customer

shrank dramatically as more drugs were being purchased through managed care

organizations and pharmacy benefit managers. Drugs commonly were sold in large

volumes and often at heavily discounted levels.

The demand for generic drugs also was declining. The use of formularies, drug lists

from which managed care doctors are required to prescribe, gave doctors less choice

and made them less responsive to direct calls from the sales force. The situation was

compounded further by the ongoing consolidation in the hospital industry. Hospitals

began centralizing purchasing and using stricter formularies, allowing physicians

virtually no leeway to prescribe unlisted drugs. The growing use of formularies resulted

in buyers needing fewer drugs and sharply reduced the need for similar drugs.

The industry’s first major wave of consolidations took place in the late 1980s, with such

mergers as SmithKline and Beecham and Bristol Myers and Squibb. This wave of

consolidation was driven by increased scale and scope economies largely realized

through the combination of sales and marketing staffs. Horizontal consolidation

represented a considerable value creation opportunity for those companies able to

realize cost synergies. In analyzing the total costs of pharmaceutical companies,

William Pursche (1996) argued that the potential savings from mergers could range

from 1525% of total R&D spending, 520% of total manufacturing costs, 1550% of

marketing and sales expenses, and 2050% of overhead costs.

Continued consolidation seemed likely, enabling further cuts in sales and marketing