The first step a pension fund should take before beginning to invest is to

A. establish investment objectives.

B. develop a list of investment managers with superior records to interview.

C. establish asset allocation guidelines.

D. decide between active and passive management.

The duration of a 5-year zero-coupon bond is

A. smaller than 5.

B. larger than 5.

C. equal to 5.

D. equal to that of a 5-year 10% coupon bond.

E. None of the options are correct.

You buy one Home Depot June 60 call contract and one June 60 put contract. The call

premium is $5 and the put premium is $3.

At expiration, you break even if the stock price is equal to

A. $52.

B. $60.

C. $68.

D.either $52 or $68.

E. None of the options are correct.

The following data are available relating to the performance of Long Horn Stock Fund

and the market portfolio:

The risk-free return during the sample period was 6%.

Calculate the information ratio for Long Horn Stock Fund.

A. 1.33

B. 4.00

C. 8.67

D. 31.43

E. 37.14

If interest rate parity does not hold,

A. covered interest arbitrage opportunities will exist.

B. covered interest arbitrage opportunities will not exist.

C. arbitragers will be able to make risk-free profits.

D. covered interest arbitrage opportunities will exist, and arbitragers will be able to

make risk-free profits.

E. covered interest arbitrage opportunities will not exist, and arbitragers will be able to

make risk-free profits. If interest rate parity holds, covered interest arbitrage

opportunities will not exist.

Which one of the following stock index futures has a multiplier of $100 times the index

value?

A. CAC 40

B. S&P 500 Index

C. Nikkei

D. DAX-30

E. NASDAQ 100

Suppose that the risk-free rates in the United States and in Canada are 3% and 5%,

respectively. The spot exchange rate between the dollar and the Canadian dollar (C$) is

$0.80/C$. What should the futures price of the C$ for a one-year contract be to prevent

arbitrage opportunities, ignoring transactions costs.

A. $1.00/C$

B. $1.70/C$

C. $0.88/C$

D. $0.78/C$

E. $1.22/C$

Prior to expiration,

A. the intrinsic value of a call option is greater than its actual value.

B. the intrinsic value of a call option is always positive.

C. the actual value of a call option is greater than the intrinsic value.

D. the intrinsic value of a call option is always greater than its time value.

Altman’s Z scores are assigned based on a firm’s financial characteristics and are used

to predict

A. required coupon rates for new bond issues.

B. bankruptcy risk.

C. the likelihood of a firm becoming a takeover target.

D. the probability of a bond issue being called.

E. None of the options are correct.

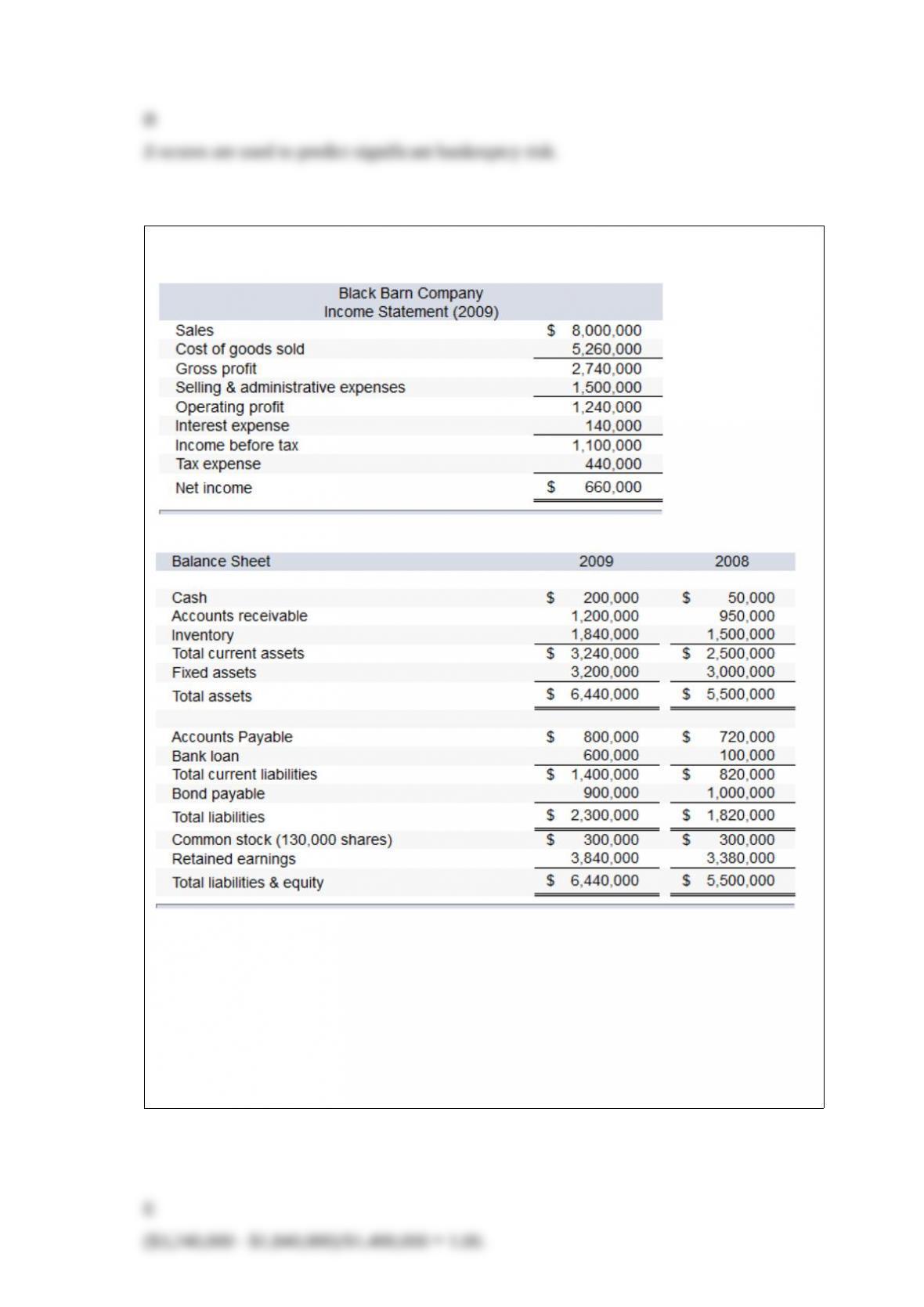

The financial statements of Black Barn Company are given below.

Note: The common shares are trading in the stock market for $40 each.

Refer to the financial statements of Black Barn Company. The firm’s quick ratio for

2009 is

A. 1.69.

B. 1.52.

C. 1.23.

D. 1.07.

E. 1.00.

Shares of several foreign firms are traded in the U.S. markets in the form of

A. ADRs.

B. ECUs.

C. single-country funds.

D. All of the options are correct.

E. None of the options are correct.

A European call option can be exercised

A. any time in the future.

B.only on the expiration date.

C. if the price of the underlying asset declines below the exercise price.

D. immediately after dividends are paid.

Which of the following statements is true about models that attempt to measure the

empirical performance of the CAPM?

A. The conventional CAPM works better than the conditional CAPM with human

capital.

B. The conventional CAPM works about the same as the conditional CAPM with

human capital.

C. The conditional CAPM with human capital yields a better fit for empirical returns

than the conventional CAPM.

D. Adding firm size to the model specification dramatically improves the fit.

E. Adding firm size to the model specification worsens the fit.

Brokers’calls

A. are funds used by individuals who wish to buy stocks on margin.

B. are funds borrowed by the broker from the bank, with the agreement to repay the

bank immediately if requested to do so.

C. carry a rate that is usually about one percentage point lower than the rate on U.S.

T-bills.

D are funds used by individuals who wish to buy stocks on margin and are funds

borrowed by the broker from . the bank, with the agreement to repay the bank

immediately if requested to do so.

E. are funds used by individuals who wish to buy stocks on margin and

carry a rate that is usually about one percentage point lower than the rate on U.S.

T-bills.

Of the following types of ETFs, an investor who wishes to invest in a diversified

portfolio that tracks the Russell 2000 should choose

A. SPY.

B. DIA.

C. QQQQ.

D. IWM.

E. VTI.

The yield to maturity of a 20-year zero-coupon bond that is selling for $372.50 with a

value at maturity of $1,000 is

A. 5.1%.

B. 8.8%.

C. 10.8%.

D. 13.4%.

E. None of the options are correct.

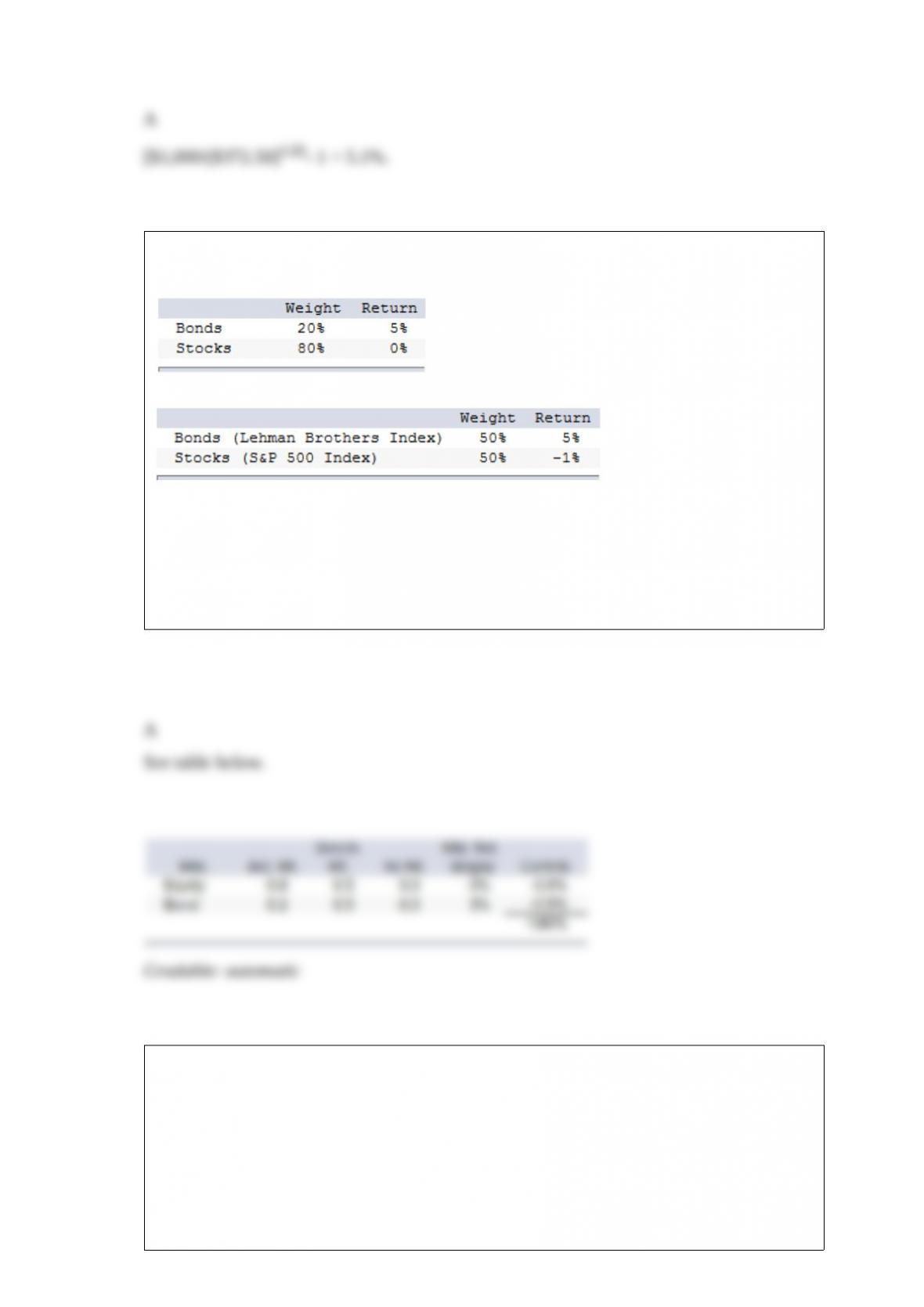

In a particular year, Razorback Mutual Fund earned a return of 1% by making the

following investments in asset classes:

The return on a bogey portfolio was 2%, calculated from the following information.

The contribution of asset allocation across markets to the Razorback Fund’s total excess

return was

A. –1.80%.

B. –1.00%.

C. 0.80%.

D. 1.00%.

You invest 55% of your money in security A with a beta of 1.4 and the rest of your

money in security B with a

beta of 0.9. The beta of the resulting portfolio is

A. 1.466.

B. 1.157.

C. 0.968.

D. 1.082.

E. 1.175.

A coupon bond that pays interest annually is selling at a par value of $1,000, matures in

five years, and has a coupon rate of 9%. The yield to maturity on this bond is

A. 8.0%.

B. 8.3%.

C. 9.0%.

D. 10.0%.

E. None of the options are correct.

Consider the single factor APT. Portfolios A and B have expected returns of 14% and

18%, respectively. The risk-free rate of return is 7%. Portfolio A has a beta of 0.7. If

arbitrage opportunities are ruled out, portfolio B must have a beta of

A. 0.45.

B. 1.00.

C. 1.10.

D. 1.22.

E. None of the options are corrct.

Consider the regression equation:

rirf = g0 + g1bi + eit

where:

rirf = the average difference between the monthly return on stock i and the monthly risk

free rate

bi = the beta of stock i

This regression equation is used to estimate

A. the benchmark error.

B. the security market line.

C. the capital market line.

D. the benchmark error and the security market line.

E. the benchmark error, the security market line, and the capital market line.

A seven-year par value bond has a coupon rate of 9% (paid annually) and a modified

duration of

A. 7 years.

B. 5.49 years.

C. 5.03 years.

D. 4.87 years.

If you determine that the S&P 500 Index futures is overpriced relative to the spot S&P

500 Index, you could make an arbitrage profit by

A. buying all the stocks in the S&P 500 and selling put options on the S&P 500 Index.

B. selling short all the stocks in the S&P 500 and buying S&P Index futures.

C. selling all the stocks in the S&P 500 and buying call options on the S&P 500 Index.

D. selling S&P 500 Index futures and buying all the stocks in the S&P 500.

E. None of the options are correct.

To create a common size balance sheet, ____________ all items on the balance sheet by

____________.

A. multiply; owners’equity

B. multiply; total assets

C. divide; owners’equity

D. divide; total assets

E. multiply; debt

Lower dividend-payout policies have a __________ impact on the value of the call and

a __________ impact on the value of the put compared to higher dividend-payout

policies.

A. negative; negative

B. positive; positive

C. positive; negative

D. negative; positive

E. zero; zero

Jaffe (1974) found that stock prices _________ after insiders intensively bought shares.

A. decreased

B. did not change

C. increased

D. became extremely volatile

E. became much less volatile

You invest 50% of your money in security A with a beta of 1.6 and the rest of your

money in security B with a

beta of 0.7. The beta of the resulting portfolio is

A. 1.40.

B. 1.15.

C. 0.36.

D. 1.08.

E. 0.80.

________ bias means that investors are too slow in updating their beliefs in response to

evidence.

A. Framing

B. Regret avoidance

C. Overconfidence

D. Conservatism

E. None of the options are correct.

The ____ is an example of a U.S. index of large firms.

A. Wilshire 5000

B. DJIA

C. DAX

D. Russell 2000

E. All of the options.

As a financial analyst, you are tasked with evaluating a capital-budgeting project. You

were instructed to

use the IRR method, and you need to determine an appropriate hurdle rate. The risk-free

rate is 5%, and

the expected market rate of return is 10%. Your company has a beta of 0.67, and the

project that you are

evaluating is considered to have risk equal to the average project that the company has

accepted in the past.

According to CAPM, the appropriate hurdle rate would be

A. 10%.

B. 5%.

C. 8.35%.

D. 28.35%.

E. 0.67%.

Which of the following bonds has the longest duration?

A. An 8-year maturity, 0% coupon bond

B. An 8-year maturity, 5% coupon bond

C. A 10-year maturity, 5% coupon bond

D. A 10-year maturity, 0% coupon bond

E. Cannot tell from the information given

Which one of the following variables influences the value of call options?

I) Level of interest rates

II) Time to expiration of the option

III) Dividend yield of underlying stock

IV) Stock price volatility

A. I and IV only

B. II and III only

C. I, II, and IV only

D. I, II, III, and IV

E. I, II, and III only

Corporations can exclude ____________% of the dividends received from preferred

stock from taxes.

A. 50

B. 70

C. 20

D. 15

E. 62