A mutual fund had average daily assets of $3.0 billion in 2016. The fund sold $600

million worth of stock and purchased $700 million worth of stock during the year. The

fund’s turnover ratio is

A. 27.5%.

B. 12%.

C. 15%.

D. 25%.

E. 20%.

The intrinsic value of an at-the-money call option is equal to

A. the call premium.

B. zero.

C. the stock price plus the exercise price.

D. the striking price.

E. None of the options are correct.

Which one of the following statements regarding delivery is true?

A. Most futures contracts result in actual delivery.

B. Only 1% to 3% of futures contracts result in actual delivery.

C. Only 15% of futures contracts result in actual delivery.

D. Approximately 50% of futures contracts result in actual delivery.

E. Futures contracts never result in actual delivery.

The tracking error of an optimized portfolio can be expressed in terms of the

____________ of the portfolio, and

thus reveals ____________.

A. return; portfolio performance

B. total risk; portfolio performance

C. beta; portfolio performance

D.beta; benchmark risk

E. relative return; benchmark risk

Which of the following investments allows the investor to choose how to allocate

assets?

A. Variable Life insurance policies

B. Keogh plans

C. Personal funds

D. Taxqualified defined contribution plans

E. All of the options are correct.

If a 6% coupon bond is trading for $950.00, it has a current yield of

A. 6.5%.

B. 6.3%.

C. 6.1%.

D. 6.0%.

E. 6.6%.

In 2016, ____________ were the most significant liability of U.S. households in terms

of total value.

A. credit cards

B. mortgages

C. bank loans

D. student loans

E. other forms of debt

The beta of a stock has been estimated as 1.4 using regression analysis on a sample of

historical returns. A commonly-used adjustment technique would provide an adjusted

beta of

A. 1.27.

B. 1.32.

C. 1.13.

D. 1.0.

A firm has a lower quick (or acid test) ratio than the industry average, which implies

A. the firm has a lower P/E ratio than other firms in the industry.

B. the firm is less likely to avoid insolvency in the short run than other firms in the

industry.

C. the firm may be more profitable than other firms in the industry.

D. the firm has a lower P/E ratio than other firms in the industry, and the firm is less

likely to avoid insolvency in the short run than other firms in the industry.

E. the firm is less likely to avoid insolvency in the short run than other firms in the

industry, and the firm may be more profitable than other firms in the industry.

Suppose the following equation best describes the evolution of β over time:

βt = 0.25 + 0.75βt– 1.

If a stock had a β of 0.6 last year, you would forecast the β to be _______ in the coming

year.

A. 0.45

B. 0.60

C. 0.70

D. 0.75

Consider an investment opportunity set formed with two securities that are perfectly

negatively correlated. The

global-minimum variance portfolio has a standard deviation that is always

A. greater than zero.

B. equal to zero.

C. equal to the sum of the securities’ standard deviations.

D. equal to 1.

The term “arbitrage” refers to

A. buying low and selling high.

B. short selling high and buying low.

C. earning risk-free economic profits.

D. negotiating for favorable brokerage fees.

E. hedging your portfolio through the use of options.

What is the yield to maturity of a 3-year bond?

A. 4.6%

B. 4.9%

C. 5.2%

D. 5.5%

E. 5.8%

If a 9% coupon bond that pays interest every 182 days paid interest 112 days ago, the

accrued interest would be

A. $27.69.

B. $27.35.

C. $26.77.

D. $27.98.

E. $28.15.

A trader who has a __________ position in gold futures wants the price of gold to

__________ in the future.

A. long; decrease

B. short; decrease

C. short; stay the same

D. short; increase

E. long; stay the same

New issues of securities are sold in the ________ market(s).

A. primary

B. secondary

C. over-the-counter

D. primary and secondary

Other things equal, the price of a stock call option is negatively correlated with which

of the following factors?

A. The stock price

B. The time to expiration

C. The stock volatility

D. The exercise price

E. The stock price, time to expiration, and stock volatility

The elasticity of an option is

A. the volatility level for the stock that the option price implies.

B. the continued updating of the hedge ratio as time passes.

C. the percentage change in the stock call-option price divided by the percentage

change in the stock price.

D. the sensitivity of the delta to the stock price.

Which of the following statements regarding delivery is false?

I) Most futures contracts result in actual delivery.

II) Only 1% to 3% of futures contracts result in actual delivery.

III) Only 15% of futures contracts result in actual delivery.

A. I only

B. II only

C. III only

D. I and II

E. I and III

Consider the single-factor APT. Stocks A and B have expected returns of 12% and 14%,

respectively. The risk-free rate of return is 5%. Stock B has a beta of 1.2. If arbitrage

opportunities are ruled out, stock A has a beta of

A. 0.67.

B. 0.93.

C. 1.30.

D. 1.69.

The exact indifference curves of different investors

A. cannot be known with perfect certainty.

B. can be calculated precisely with the use of advanced calculus.

C. are known with perfect certainty and allow the advisor to create more suitable

portfolios for the client.

D. although not known with perfect certainty, do allow the advisor to create more

suitable portfolios for the

client.

A bond has a par value of $1,000, a time to maturity of 20 years, a coupon rate of 10%

with interest paid annually, a current price of $850, and a yield to maturity of 12%.

Intuitively and without using calculations, if interest payments are reinvested at 10%,

the realized compound yield on this bond must be

A. 10.00%.

B. 10.9%.

C. 12.0%.

D. 12.4%.

E. None of the options are correct.

If investors do not know their investment horizons for certain,

A. the CAPM is no longer valid.

B. the CAPM underlying assumptions are not violated.

C. the implications of the CAPM are not violated as long as investors’ liquidity needs

are not priced.

D. the implications of the CAPM are no longer useful.

You purchased shares of a mutual fund at a price of $17 per share at the beginning of

the year and paid a front-end load of 5.0%. If the securities in which the fund invested

increased in value by 12% during the year, and the fund’s expense ratio was 1.0%, your

return if you sold the fund at the end of the year would be

A. 4.75%.

B. 5.45%.

C. 5.65%.

D. 4.39%.

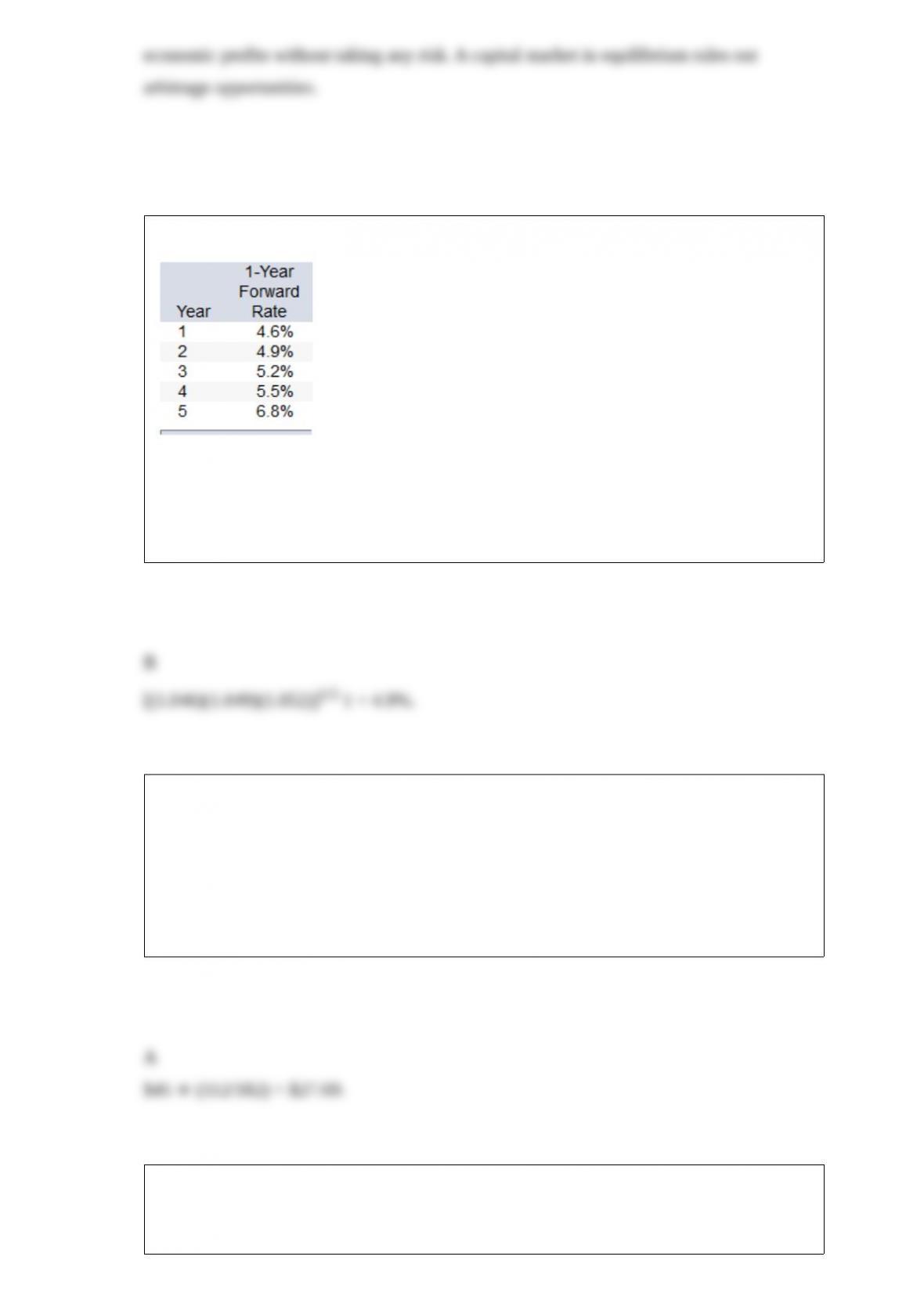

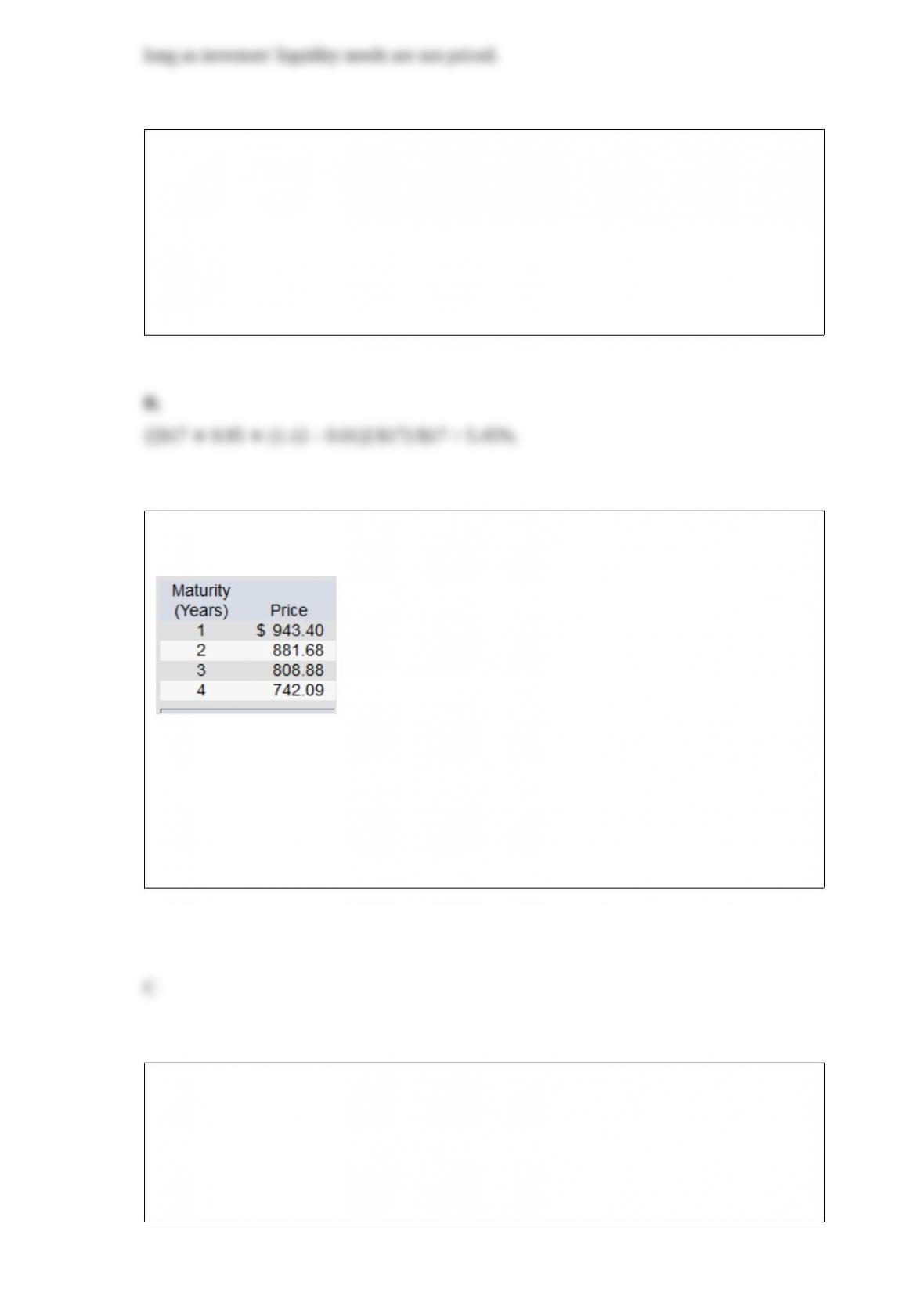

The following is a list of prices for zero-coupon bonds with different maturities and par

values of $1,000.

According to the expectations theory, what is the expected forward rate in the third

year?

A. 7.00%

B. 7.33%

C. 9.00%

D. 11.19%

E. None of the options are correct.

The holding-period return (HPR) for a stock is equal to

A. the real yield minus the inflation rate.

B. the nominal yield minus the real yield.

C. the capital gains yield minus the tax rate.

D. the capital gains yield minus the dividend yield.

E. the dividend yield plus the capital gains yield.

Although derivatives can be used as speculative instruments, businesses most often use

them to

A. attract customers.

B. appease stockholders.

C. offset debt.

D. hedge risks.

E. enhance their balance sheets.

Financial futures contracts are actively traded on the following indices except

A. the S&P 500 Index.

B. the New York Stock Exchange Index.

C. the Nikkei Index.

D. the Dow Jones Industrial Index.

E. All are actively traded.

Investors can use publicly available financial data to determine which of the following?

I) The shape of the yield curve

II) Expected future short-term rates (if liquidity premiums are ignored)

III) The direction the Dow indexes are heading

IV) The actions to be taken by the Federal Reserve

A. I and II

B. I and III

C. I, II, and III

D. I, III, and IV

E. I, II, III, and IV

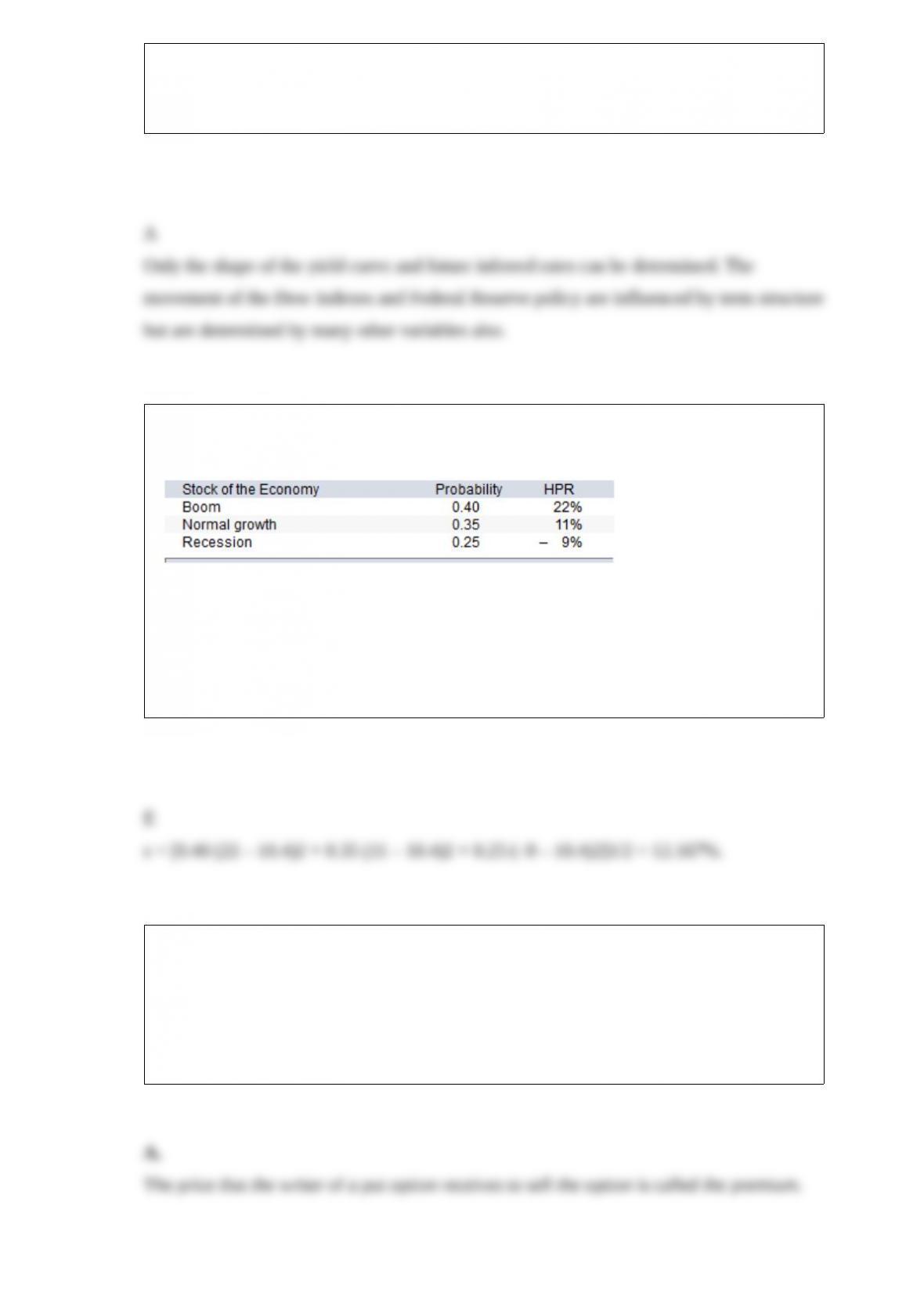

You have been given this probability distribution for the holding-period return for a

stock:

What is the expected standard deviation for the stock?

A. 2.07%

B. 9.96%

C. 7.04%

D. 1.44%

E. None of the options are correct.

The price that the writer of a put option receives to sell the option is called the

A. premium.

B.exercise price.

C. execution price.

D. acquisition price.

E. strike price.

As diversification increases, the firm-specific risk of a portfolio approaches

A. 0.

B. 1.

C. infinity.

D. (n – 1) × n.

If the annual real rate of interest is 3.5%, and the expected inflation rate is 2.5%, the

nominal rate of interest

would be approximately

A. 3.5%.

B. 2.5%.

C. 1%.

D. 6.8%.

E. None of the options are correct.

The two components of interest-rate risk are

A. price risk and default risk.

B. reinvestment risk and systematic risk.

C. call risk and price risk.

D. price risk and reinvestment risk.

E. None of the options are correct.

You sold short 200 shares of common stock at $60 per share. The initial margin is 60%.

Your initial investment was

A. $4,800.

B. $12,000.

C. $5,600.

D. $7,200.