The principal task of the Consumer Financial Protection Bureau (CFPB) is to:

A. design the monetary policy.

B. ensure safety and soundness of the banking system.

C. write new rules to protect customers of the financial services industry.

D. provide insurance to the investors’ funds in the banks.

E. ensure that the banks conform to the international banking regulations.

Answer:

The net interest margin of a bank is influenced by:

A. changes in the level of interest rates.

B. changes in the volume of interest-bearing assets and interest-bearing liabilities.

C. changes in interest income from loans and investments.

D. changes in interest expense on deposits and other borrowed funds.

E. All of the options are correct.

Answer:

The internal capital growth rate for a bank is a function of which of the following

factors?

A. Profit margin.

B. Asset utilization.

C. Equity multiplier.

D. Earnings retention ratio.

E. All of the options are correct.

Answer:

A bank is considering making a loan to Sean Finnigan. Sean owns his own home and

has lived there for the past four years. What aspect of evaluating a consumer loan

application is this fact most concerned with?

A. Character and purpose

B. Income level

C. Deposit balance

D. Employment and residential stability

E. Pyramiding of debt

Answer:

The Financial Services Regulatory Relief Act of 2006:

A. adds selected new service powers to depository institutions.

B. loosens regulations on depository institutions.

C. grants the Federal Reserve authority to pay interest on depository institutions’ legal

reserves.

D. All of the options are correct.

E. None of the options are correct.

Answer:

Under the feasibility standard adopted by the Comptroller of the Currency, applicants

for a national bank charter are required to submit _____________, which contains a

description of the proposed bank and its marketing, management, and financial plans.

A. memorandum of association

B. articles of association

C. a business plan

D. a merger plan

E. a contingency plan

Answer:

A bank has a profit margin of 5 percent, an asset utilization ratio of 11 percent, an

equity multiplier of 12, and a retention ratio of 60 percent. What is this bank’s ICGR?

A. 6.60 percent

B. 3.96 percent

C. 7.20 percent

D. 0.33 percent

E. None of the options is correct.

Answer:

Barbara Miller is a small dealer who specializes in healthcare stocks. She needs a loan

so that she can sustain her portfolio of stocks until customer-buy orders catch up with

what she has already purchased from the market. She only expects to need this loan for

a week. What type of loan does Barbara need?

A. Self-liquidating inventory loan

B. Working capital loan

C. Interim construction financing

D. Security dealer financing

E. Retailer and equipment financing

Answer:

By agreeing to service any assets that are packaged together in the securitization

process a bank can:

A. ensure the assets that are packaged and securitized remain in the package and are

not sold off.

B. choose the best loans to go through the securitization process.

C. earn added fee income.

D. liquidate any assets it chooses.

E. None of the options is correct.

Answer:

A bank has $100 million in assets in the 0 percent risk-weight category, $200 million in

assets in the 20 percent risk-weight category, $500 million in assets in the 50 percent

risk-weight category, and $750 million in assets in the 100 percent risk-weight category.

This bank has $57 million in core (Tier 1) capital. What is this bank’s ratio of Tier 1

capital to risk-weighted assets?

A. 3.68 percent

B. 7.60 percent

C. 18.25 percent

D. 5.48 percent

E. None of the options is correct.

Answer:

A bank that uses a short hedge is most likely:

A. trying to avoid higher borrowing costs.

B. trying to avoid declining asset values.

C. trying to avoid lower than expected yields from loans and securities.

D. trying to avoid higher borrowing costs or trying to avoid declining asset values.

E. trying to offset a negative duration gap.

Answer:

Factors that influence a bank’s choice among the various sources of reserves include

which of the following?

A. Immediacy of the need

B. Duration of the need

C. Interest rate outlook

D. Regulations

E. All of the options are correct

Answer:

Richard Thornton has applied for a home equity loan from Capital Two Bank. The bank

on its part has estimated the market value of Richard’s property at $750,000. If the

amount of existing mortgage loan on the property is $500,000 and Capital Two as a

policy lends only up to 70 percent of the borrowing base, what is the maximum amount

of loan will Richard get?

A. $100,000

B. $250,000

C. $175,000

D. $750,000

E. $500,000

Answer:

The realized return to a bank from a combined cash and futures market trading

operation is composed of which of the following elements?

A. Returns earned in the cash market

B. Profit or loss from futures trading

C. Difference between the opening and closing basis between cash and futures markets

D. All of the options are correct

E. Profit or loss from futures trading and the difference between the opening and

closing basis between cash and futures markets

Answer:

A put option on Eurodollar deposit futures is most likely to be used by a bank to:

A. reduce its interest sensitive liabilities.

B. protect variable-rate loans and securities.

C. offset a positive interest-sensitive gap.

D. offset a negative interest-sensitive gap.

E. None of the options are correct.

Answer:

Money market suppliers of funds typically have a(n) ______________ response to

changes in the market interest rates.

A. elastic

B. inelastic

C. slow

D. marginal

E. opposite

Answer:

One of the benefits of applying for a federal (national) bank charter over a state charter

is that: A. it brings added prestige.

B. it results in the automatic receipt of federal deposit insurance.

C. there is better technical support in times of trouble.

D. it brings added prestige and better technical support in times of trouble.

E. All of the options are correct

Answer:

A financial institution plans to issue a group of bonds backed by a pool of automobile

loans. However, they fear that the default rate on the automobile loans will rise well

above 4 percent of the portfoliothe projected default rate. The financial institution wants

to lower the interest payments if the loan default rate rises too high. Which type of

credit derivative contract would you most recommend for this situation?

A. Credit-linked note

B. Credit option

C. Credit risk option

D. Total-return swap

E. Credit swap

Answer:

A bank is considering making a loan to Alice Granger. The bank is looking at her credit

report from Equifax and also examining the reason Alice has put on the loan application

for needing the loan. According to the text, what aspect of evaluating a consumer loan

application is the bank looking at?

A. Character and purpose

B. Income level

C. Deposit balance

D. Employment and residential stability

E. Pyramiding of debt

Answer:

The Fred National Bank is planning to add a branch office on the west side of town.

The bank has done a survey and has discovered that the mean household income in the

area is $76,000 per year. Which factor would this address when considering whether to

add a new branch?

A. Number of retail shops

B. Average income level of households

C. Ratio of population to branches

D. Number of service facilities operated by financial service competitors

E. Population density

Answer:

Time deposits with minimum denominations of $100,000 are generally referred to as:

A. mini CDs.

B. jumbo CDs.

C. large CDs.

D. giant CDs.

E. super CDs.

Answer:

According to the text, Basel II agreement had resulted in less total capital and:

A. less concentration on operating risk.

B. a weaker mix of capital.

C. more retention ratio.

D. less concentration on assets.

E. a weaker leverage ratio.

Answer:

Disclosure laws require that a borrower be quoted the “true cost” of a loan, as reflected

in the:

A. internal rate of return (IRR).

B. annual percentage rate (APR).

C. net present value (NPV).

D. flat rate of interest.

E. interest rate on reducing balance.

Answer:

Which of the following is an important asset-based balance sheet composition ratio?

A. Notes payable/Total liabilities and net worth

B. Gross profit/Sales

C. Net operating profit/Total assets

D. Inventories/Total assets

E. Net income after taxes/Total assets

Answer:

A bank has capital to risk-weighted assets of 1.8%. What type of bank is this?

A. Well capitalized

B. Adequately capitalized

C. Undercapitalized

D. Significantly undercapitalized

E. Critically undercapitalized

Answer:

The most profitable credit card customers for a bank are those that:

A. use their credit card frequently.

B. pay off any charges incurred within a few days.

C. charge at least $10,000 per year.

D. use their credit card as a source of installment loans.

E. None of the options is correct

Answer:

An advantage of interest rate swap is that:

A. it can help protect from interest rate fluctuations.

B. it can help achieve lower borrowing costs.

C. it can help closely match the maturities of assets and liabilities.

D. it can help transform actual cash flows to more closely match desired cash flow

patterns.

E. All of the options are correct

Answer:

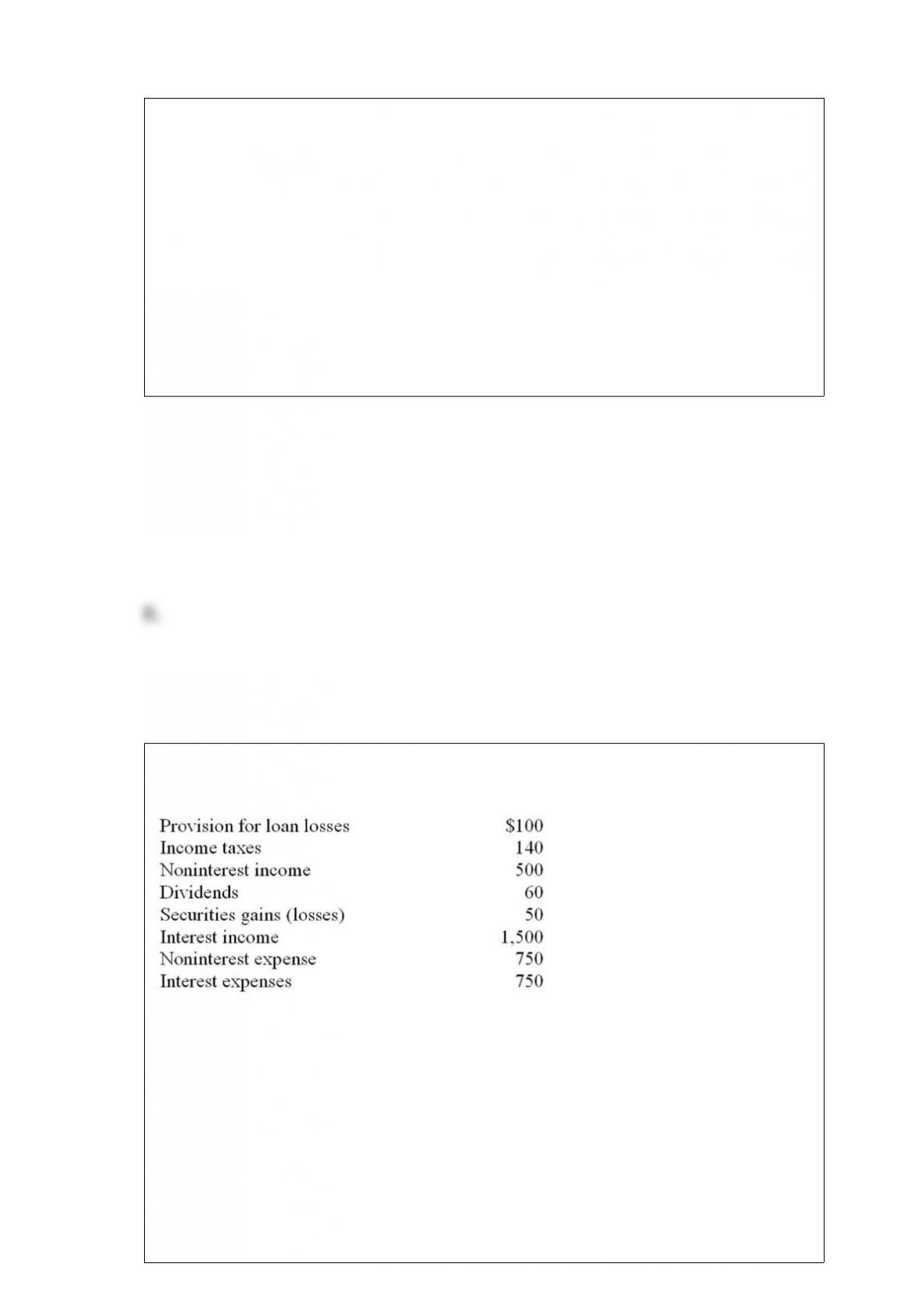

You know the following information about the Taylor National Bank:

Given this information, what is the value of this firm’s net operating income or net

income before extraordinary income?

A. $150

B. $210

C. $400

D. ($250)

E. $750

Answer:

Havoc State Bank has a loan that it fears will not be repaid because the company is

going into bankruptcy. What type of risk would this be an example of?

A. Default risk

B. Inflation risk

C. Liquidity risk

D. Call risk

E. Basis risk

Answer:

During the financial crisis of 2007-2009, the collapse of Lehman Brothers and the

bailout of Bear Stearns reaffirmed the importance of the fundamental principle of: A.

superior management.

B. globalization.

C. government bailout.

D. regulatory arbitrage.

E. public trust and confidence in the system.

Answer:

The first major bank within the U.S. to establish a separate department for granting

loans to consumers was:

A. First National City Bank of New York.

B. BankAmerica.

C. Bank One.

D. State Street Bank.

E. Bank of New York.

Answer:

A bank which offers its full range of services from only one office is known as a:

A. unit bank.

B. branch bank.

C. correspondent bank.

D. bank holding company.

E. None of the options are correct.

Answer:

Depository institutions hold deposits with the Federal reserve:

A. to satisfy legal reserve requirements.

B. to clear checks.

C. to pay for purchases of government securities.

D. for inter-bank lending through Fed’s wire system.

E. All of the options are correct.

Answer:

The ___________________________ Act prohibits lenders from asking certain

questions to a customer, such as a customer’s age or race.

Answer:

_____________________________ are the ultimate standards of performance in a

market-oriented economy. These measure the net income that remains for owners after

all expenses (except stockholder dividends) have been charged against revenues.

Answer:

When a bank has a positive duration gap a parallel increase in the interest rates on the

assets and liabilities of the bank will lead to a(n) __________________ in the bank’s

net worth.

Answer:

Depositors must send their customers the amount of interest earnings received, along

with the _________________ earned. It is the interest rate the customer has actually

earned on the account.

Answer:

Under the ___________________________ Act, no individual can be denied credit

because of race, sex, religious affiliation, age or receipt of public assistance.

Answer:

Lenders can set aside a group of loans on their balance sheet, issue bonds, and pledge

the loans as collateral against the bonds in a type of securitization known as

___________. These usually stay on the bank’s balance sheet as liabilities.

Answer:

The securities most often used in a repurchase agreement are

____________________.

Answer:

______________________ examines how effectively assets are being utilized to

generate sales and how efficiently sales are converted into cash.

Answer:

A(n) _________________________ allows homeowners to borrow against the residual

value of their residence.

Answer:

An interest-rate _______ would protect the swap party receiving a fixed-rate payment

and making a floating-rate payment in a swap.

Answer:

The _____________________ Act requires each merging bank to seek approval from

its principal federal regulating agency before a merger can take place.

Answer:

A(n) __________________________ gap means that for a parallel increase in all

interest rates, the market value of net worth will tend to increase.

Answer:

Weak loans considered to be substandard or doubtful are also known as __________

credits.

Answer:

____________ is a type of short-term loan, where the business lenders support

installment purchases of automobiles, home appliances, furniture, business equipment,

and other durable goods by financing the receivables that dealers take on when they

write installment contracts to cover customer purchases.

Answer:

In an interest rate swap, the ________________________ or principal amount is not

exchanged.

Answer:

__________________________ is the risk due to changes in market interest rates

which can adversely affect the bank’s net interest margin, assets, liabilities, and equity.

Answer:

As data processing of financial information becomes more important, managers of

financial firms can realize cost savings from _______________________, transferring

tasks from inside the firm to other firms specializing in information technology.

Answer: