1) For a firm using the indirect method, an increase in a deferred tax liability should be

added back to net income to arrive at cash flow from operating activities.

2) A $3,000 increase in total owners’ equity occurs if treasury stock costing $11,500 is

sold for $14,500.

3) The payment of life insurance premiums on company executives is an example of a

permanent difference.

4) There is more than one possible approach to measuring fair value.

5) International financial reporting standards allow firms to voluntarily opt, in some

cases, to measure financial assets at fair market value.

6) Under International Financial Reporting Standards, interest paid can be classified

either as an operating or financing cash flow.

7) Both common and preferred stock dividends are subtracted in arriving at net income

available to common stockholders.

8) Most executive compensation packages involve a base salary, an annual incentive,

and a long-term incentive.

9) The lessor’s lease Gross investment in leased asset balance is the same at the end of

the lease term whether the residual value is guaranteed or unguaranteed.

10) When the outcome of a transaction for services cannot be reliably measured, IFRS

rules call for entities to recognize revenue only up to the amount of recoverable costs

incurred to that point.

11) One reason that companies issue stock options is to attempt to align employees’

interests with the interests of the owners.

12) Under new FASB guidance, firms who sell products that combine hardware and

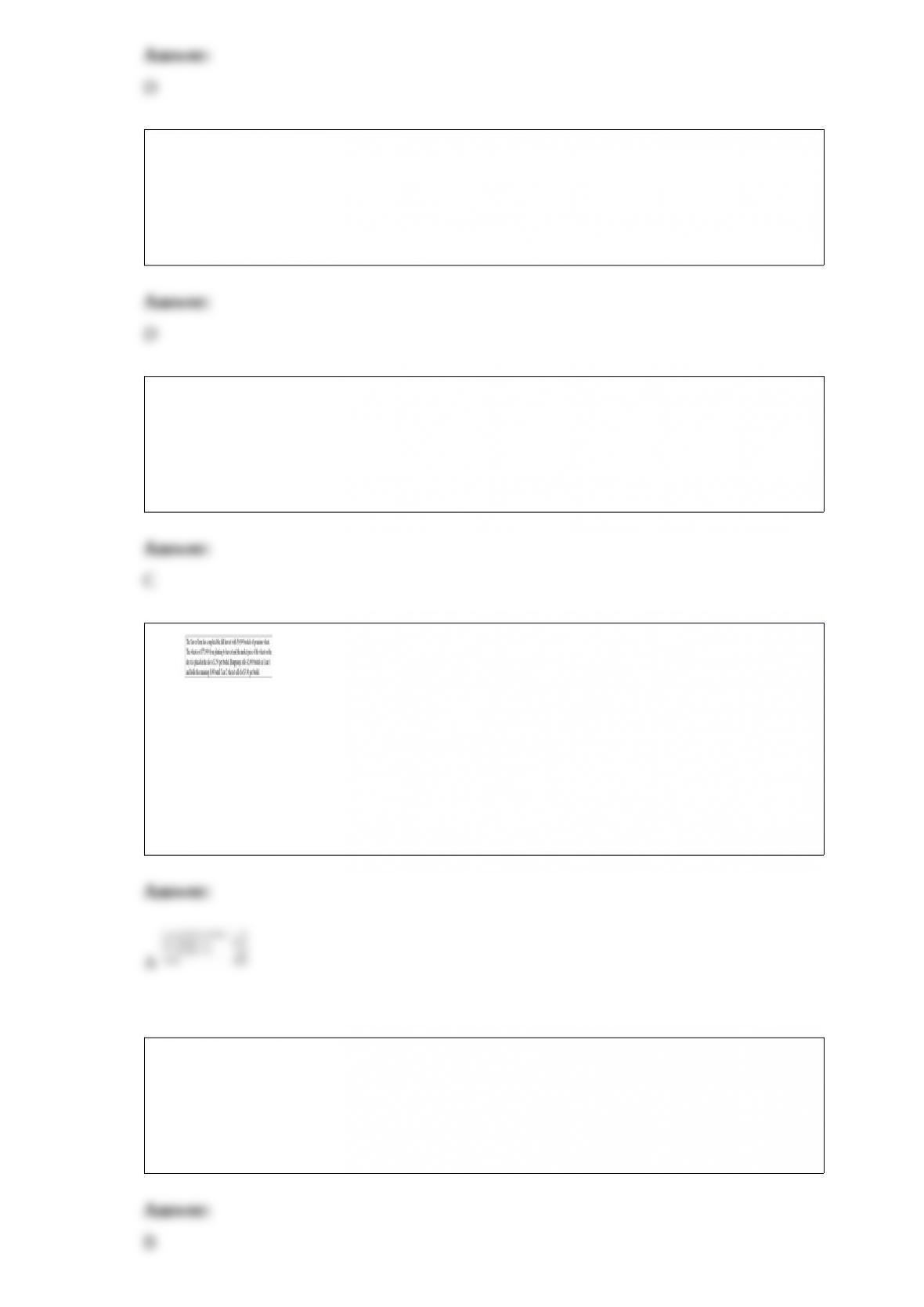

software can recognize the portion of the overall arrangement fee that is attributable to

delivered items even in the absence of specific evidence about the separate selling

prices of the components.

13) Selected data for Kris Corporation’s comparative balance sheets for Year 1 and Year

2 are as follows:

How much did Kris pay in income taxes to the government in Year 2?

A.$30,000

B.$80,000

C.$110,000

D.$150,000

14) When a company changes from straight-line depreciation to

double-declining-balance depreciation, the change is reported

A.prospectively because it is impractical to determine the effects of this change on prior

years’ income

B.as an error correction

C.as a change in an accounting estimate

D.using the retrospective approach

15) Goodwill represents

A.management’s estimate of the value of the firm’s “unidentified” intangible assets

B.the difference between the acquisition value of an acquired business and the fair

value of its identifiable net assets

C.the difference between the acquisition value of an acquired business and the book

value of its identifiable net assets

D.the sum of the acquisition value of an acquired business and the fair value of its

identifiable net assets

16) Brick Company started construction on a new office building on January 1, 2011,

and moved into the finished building on July 1, 2012 . Of the building’s $3,000,000

total cost, $2,000,000 was incurred in 2011 evenly throughout the year. The remaining

$1,000,000 was paid in installments of $500,000 each on February 1, 2012 and June 30,

2012 . Brick’s incremental borrowing rate was 12% throughout the construction period

and the total amount of interest incurred by Brick during 2011 and 2012 was $200,000

and $210,000 respectively.

Required:

a. What amount of capitalized interest should Brick report as part of its building

account at December 31, 2011?

b. What amount of capitalized interest should Brick report as part of its building

account at December 31, 2012?

17) The SEC has issued a proposed roadmap for the adoption of IFRS by U.S. public

companies, specifying adoption by the end of

A.2011

B.2014

C.2015

D.The roadmap does not specify a “date certain” for adoption

18) Under IFRS, research must be expensed but some development expenditures may

be capitalized. To capitalize development expenditures, firms must demonstrate several

factors that include all of the following except

A.technical feasibility

B.length of time the intangible asset is expected to provide benefits

C.ability to use or sell the asset

D.how the intangible asset will generate probable future economic benefits

19) Which of the following is a reason why lease accounting under GAAP should be

reconsidered?

A.It is too easy for firms to circumvent lease capitalization criteria

B.The SEC has stated that the FASB should reexamine lease accounting

C.Operating leases are a popular means of off-balance sheet financing

D.Each of the above are substantiated reasons

20) Financial statement forecasts (or projections) are

A.one of the required footnote disclosures found in each company’s annual report

B.filed annually with the SEC by all public companies

C.frequently used in determining management compensation

D.essential ingredients of business valuation and credit risk analysis

21) A lessee must use which one of the following discount rates to value a capital lease?

A.Prime rate

B.Implicit lease rate

C.Lessee’s incremental borrowing rate

D.Lower of implicit lease rate or lessee’s incremental borrowing rate

22) Time-series analysis helps identify financial trends

A.across companies at a single point in time

B.across business units at a single point in time

C.over time for a single company or business unit

D.among the companies that comprise an industry group

23)

Using the completed transaction (sales) method, how much net revenue should Sarver

recognize in Year 1?

A.$42,000

B.$50,000

C.$105,000

D.$125,000

24) Return on Assets (ROA) measures a firm’s

A.cost effectiveness of its operating activities

B.profitable use of its assets

C.profitability of sales

D.return on shareholders’ investment

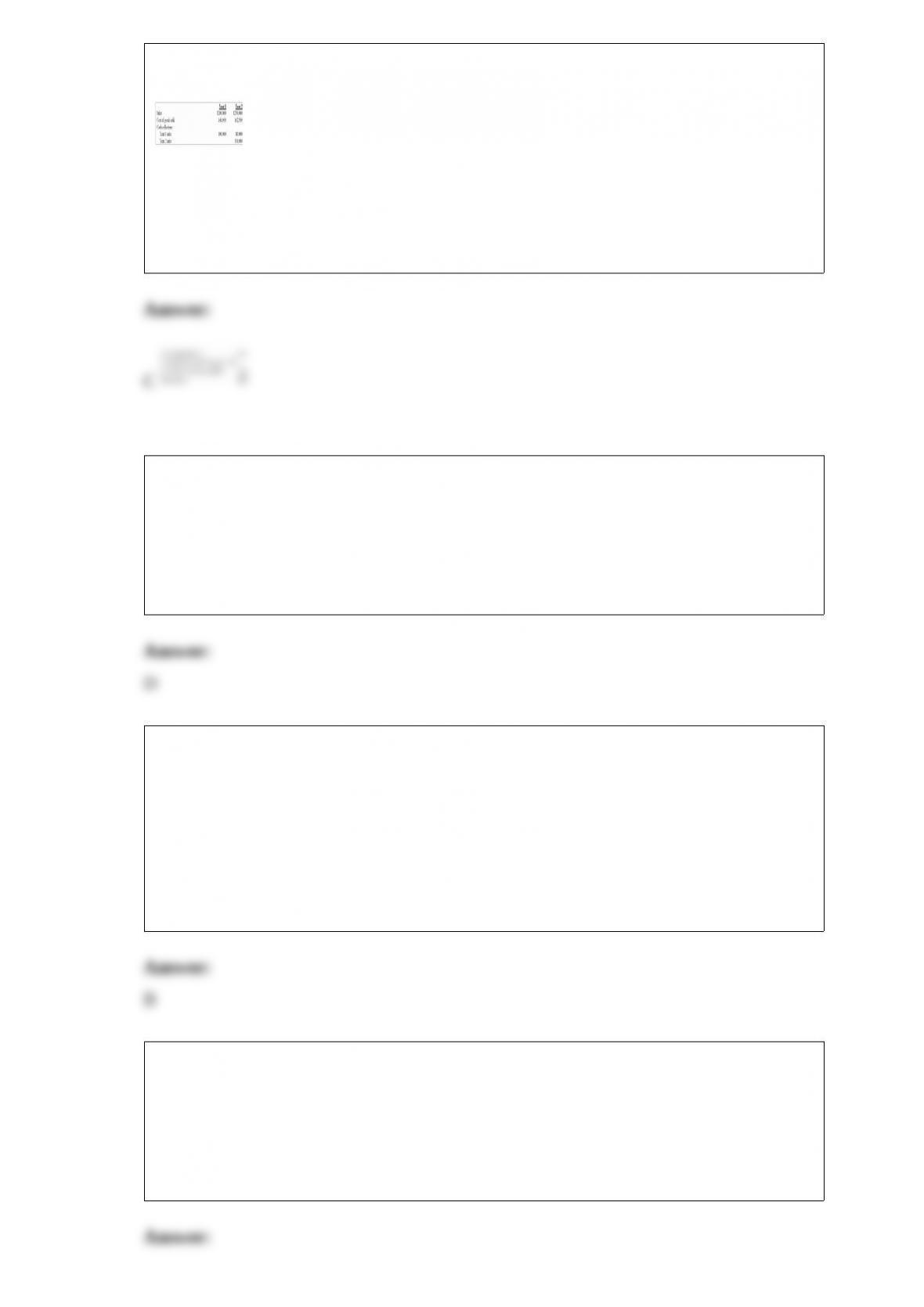

25) Ford Appliance Center records revenue on the installment sales method. The

following information is available for the first two years of business.

How much realized gross profit on installment sales will Ford recognize in Year 2?

A.$24,000

B.$45,500

C.$69,500

D.$130,000

26) GAAP requires firms to report comprehensive income

A.at the end of the income statement

B.as a separate statement of comprehensive income

C.in the statement of changes in stockholders’ equity

D.in a statement that is displayed with the same prominence as other financial

statements

27) When a firm does not adopt the fair value option, it

A.need not disclose the fair value of its long-term notes receivable

B.still must disclose the fair value of its long-term notes receivable unless the reported

value approximates fair value

C.still must disclose the fair value of its long-term notes receivable if the reported value

exceeds fair value

D.may disclose the fair value of its long-term notes receivable if the reported value

exceeds fair value, but such disclosure is not required

28) The apportionment of the cost of a copyright to future periods under the matching

principle is

A.depletion

B.amortization

C.depreciation

D.allocation

29) Monetary assets are comprised of

A.cash and cash equivalents

B.cash, cash equivalents, and accounts receivable

C.cash, cash equivalents, accounts receivable, and notes receivable

D.cash, accounts receivable, notes receivable, and inventory

30) Long-term incentive components of executive compensation plans should include

stock options

A.to enhance the short-term focus of executives

B.to mitigate the short-term focus of executives

C.to mitigate the long-term focus of executives

D.to encourage better performance by low-level staff

31) When the market rate of interest is below the nominal rate, a bond sells at

A.par

B.a premium

C.a discount

D.stated value

32) Almond Industries owns an investment that experienced a decline during 2012 that

has been judged to be “other than temporary”. The investment is held in Almond’s

trading portfolio. It was purchased in March 2011 at a cost of $460,000. At the end of

2011, the fair value of the investment was $520,000. At the end of 2012, the fair value

of the investment is $410,000. What amount of loss will Almond Industries report on its

income statement for the year ending December 31, 2012 related to this investment?

A.An unrealized loss $110,000

B.An unrealized loss of $50,000

C.An unrealized loss of $60,000

D.A realized loss of $50,000

33) Which one of the following would be reported in the cash flow from operating

activities section of the cash flow statement under the direct method?

A.Increase in taxes payable

B.Interest and dividends received

C.Issuance of common stock

D.Cash payments made on short-term notes

34) Reported earnings numbers often contain three distinctly different components,

each subject to a different earnings capitalization rate. Which of the following is not one

of these components?

A.A permanent earnings component

B.A transitory earnings component

C.A restructured earnings component

D.A value-irrelevant earnings component

35) Which one of the following explanations for the growth of accounts receivable

outstripping the growth of sales presents a red flag?

A.The firm adopts new credit terms that lengthen the payment terms to the industry

average

B.The firm adopts an aggressive revenue recognition policy

C.The firm develops an attractive credit policy for first time buyers

D.The firm changes its timing of revenue recognition to a more conservative approach

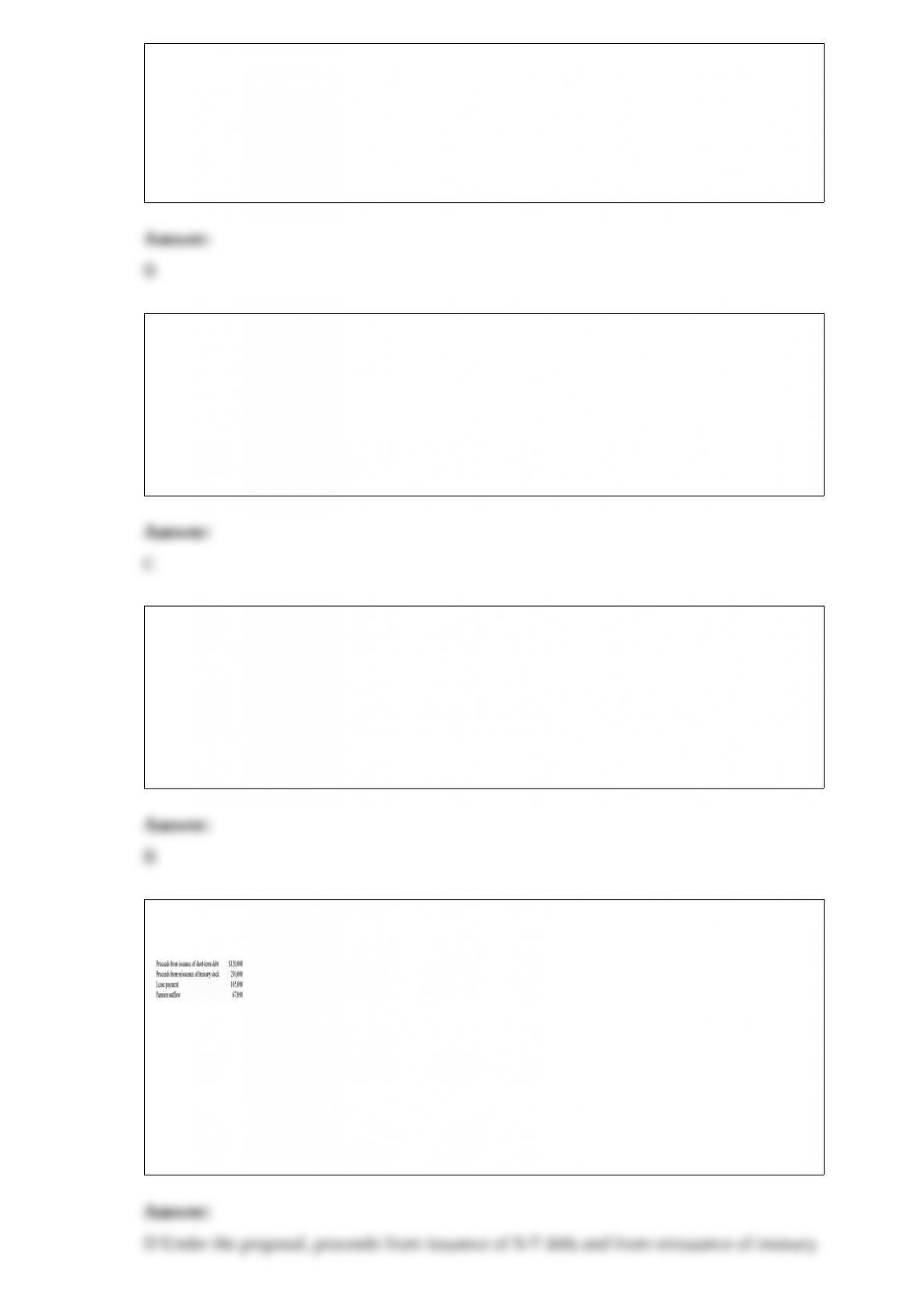

36) During 2012, Autumn Company had the following information related to cash

flows:

If Autumn Company’s statement of cash flows is prepared using the proposal on the

statement of cash flows put forth by the IASB and the FASB, what amount would be

reported as net cash from financing activities?

A.$172,000 cash outflow

B.$178,000 cash inflow

C.$58,000 cash inflow

D.$350,000 cash inflow

37) A major difference between accounting for postretirement benefit plans and pension

plans is that

A.postretirement benefit plans are not required to be funded

B.postretirement benefit plans do not create a liability to be shown on the plan sponsor’s

balance sheet

C.postretirement benefit plans do not deduct the return on plan assets when funded

D.there is no accumulated postretirement benefit obligation

38) The Bears Corporation has provided you the following information:

The accounts receivable balance increased $50,000.

Net sales was $500,000.

The gross profit was 40% of net sales.

The inventory account increased $45,000.

The accounts payable balance decreased $17,000.

$7,500 of accounts receivable were written off.

The bad debt expense was $10,000.

Required:

1> Determine the cash collected from customers.

2> Determine the cash paid to suppliers.

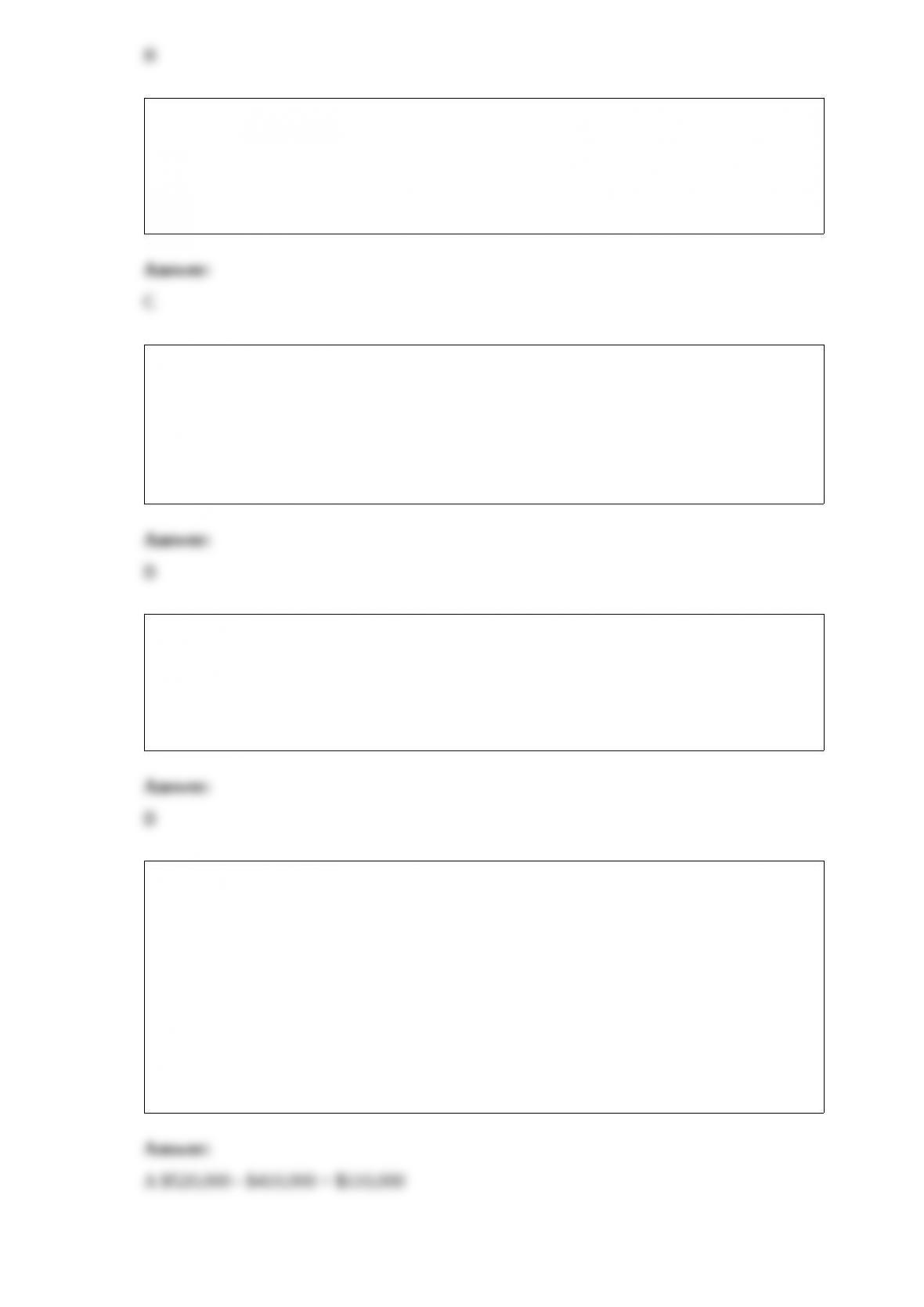

39) On January 1, 2011, Hitchcock Corporation entered into a 5-year interest rate swap

agreement. The agreement called for the company to make payments based on an 8%

fixed notional amount of $500,000 and to receive interest based on a floating interest

rate. The contract called for cash settlement of the net interest amount at the end of each

year. The floating rate was to be reset at each cash settlement date. Thus, the floating

rate for determining each end of year payment is the rate as of the end of the prior year.

Market (LIBOR) interest rates were 8% at January 1, 2011, 6.5% at December 31,

2011, and 9% at December 31, 2012 . The fair value of the swap is as follows:

Requirements:

1> Complete the following table to show the amounts appearing in Hitchcock’s

financial statements related to the swap for the years ended December 31, 2011 and

December 31, 2012 . There may be zeros in several of the cells. Indicate debits and

credits by putting parentheses around credits. Show your work within the table.

2> Complete the following table to show the amounts appearing in Hitchcock’s

statement of comprehensive income related to the swap and the hedged item for the

years ended December 31, 2011 and December 31, 2012, assuming that the interest rate

swap is being used as a perfectly effective cash flow hedge for a $500,000 variable rate

note payable issued by Hitchcock. There may be zeros in multiple cells. Indicate debits

and credits by placing parentheses around the credits. Show your work within the table.

3> Complete the following table to show the amounts appearing in Hitchcock’s

statement of comprehensive income related to the swap and the hedged item for the

years ended December 31, 2011 and December 31, 2012, assuming that the interest rate

swap is being used as a perfectly effective fair value hedge for a $500,000 investment in

a fixed rate note. The note is classified as an available-for-sale security. There may be

zeros in multiple cells. Indicate debits and credits by placing parentheses around the

credits. Show your work within the table.

40) Mackerel Company purchased equipment on January 2, 2010 for $100,000. The

equipment had an estimated eight-year service life and $5,000 salvage value.

Mackerel’s policy for “eight-year assets” is to use double-declining balance depreciation

for the first five years of the asset’s life and then switch to the straight-line depreciation

method.

Required:

In its December 31, 2012 balance sheet, what amount should Mackerel report as net

book value for this equipment?

41) Nadir Company purchased a milling machine on January 3, 2003 for $55,000. The

machine was being depreciated on the straight-line method over an estimated useful life

of 10 years, with $5,000 salvage value. At the beginning of 2011, the company paid

$15,000 to overhaul the machine. As a result of this expenditure, the company

estimated that the remaining useful life of the machine was now 8 years with no salvage

value.

Required:

What should be the depreciation expense recorded for this machine in 2011 and what is

the asset’s December 31, 2011 book value?

42) Briefly define “abnormal earnings” and describe the key features of the abnormal

earnings approach to valuation.

43) In its accrual-basis income statement for the year ended December 31, 2011, Ralph

Company reported revenue of $2,565,000. Additional information was as follows:

Required:

Under the cash basis of income determination, how much should Ralph report as

revenue for 2011?

44) The Collins Company paid $1,050,000 to purchase 70% of Revsine Company’s

outstanding common stock on July 1, 2012 . Revsine’s balance sheet on the acquisition

date reported net assets totaling $1,200,000. Revsine’s land had a fair value which was

$175,000 greater than book value, while the inventory’s fair value exceeded its book

value by $67,500. Immediately after the acquisition of the Revsine stock, Collins

reported net assets of $5,785,000.

Required:

1> Determine the consolidated net assets total as of July 1, 2012 using the acquisition

method of accounting.

2> Determine the amount of noncontrolling interest to be reported on the July 1, 2012

balance sheet. How is the noncontrolling interest reported within the consolidated

balance sheet? Assume that the acquisition method of accounting is applicable.