1) one-, two-, and three-year maturity, default-free, zero-coupon bonds have yields to

maturity of 7%, 8%, and 9%, respectively. what is the implied 1-year forward rate 1

year from today?

a.2.07%

b.8.03%

c.9.01%

d.11.12%

2) it appears from empirical work that exchange rate risk ____________.

a.has been declining for individual investments in recent years

b.is mostly diversifiable

c.is mostly systematic risk

d.is unimportant for an investment in a single foreign country

3) operating roa can be found as the product of ______.

a.return on sales ato

b.tax burden interest burden

c.interest burden leverage ratio

d.roe dividend payout ratio

4) the writer of a put option _______________.

a.agrees to sell shares at a set price if the option holder desires

b.agrees to buy shares at a set price if the option holder desires

c.has the right to buy shares at a set price

d.has the right to sell shares at a set price

5) a __________ is a private investment pool open only to wealthy or institutional

investors that is exempt from sec regulation and can therefore pursue more speculative

policies than mutual funds.

a.commingled pool

b.unit trust

c.hedge fund

d.money market fund

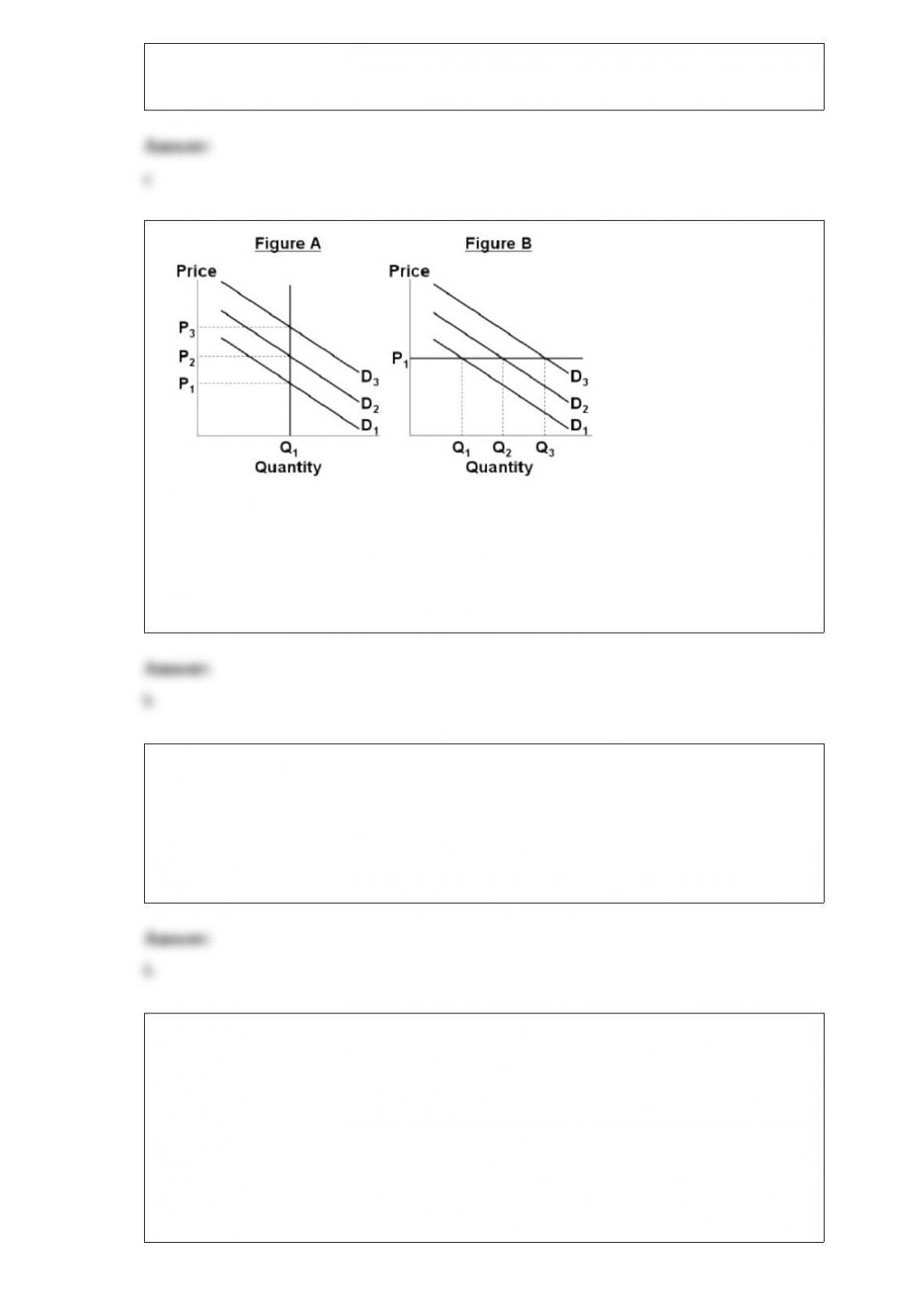

6)

refer to the above figures. which figure(s) represent a situation where negative demand

shocks can result in a recession?

a.a only.

b.b only.

c.both a and b.

d.neither a nor b.

7) after much investigation, an investor finds that intel stock is currently underpriced.

this is an example of ______.

a.asset allocation

b.security analysis

c.top-down portfolio management

d.passive management

8) a pension fund will owe $15 million to retirees in 20 years. an actuary assumes a 6%

rate of return on the funds invested in the pension plan, but the fund actually earns 8%.

the pension plan receives annual contributions from the company sponsor. if the 8%

rate of return is expected to continue, by how much can the company reduce its pension

payments per year?

a.$65,437

b.$79,985

c.$89,462

d.$95,320

9) you short-sell 200 shares of rock creek fly fishing co., now selling for $50 per share.

if you want to limit your loss to $2,500, you should place a stop-buy order at ____.

a.$37.50

b.$62.50

c.$56.25

d.$59.75

10) contributions to a traditional retirement plan are __________, and contributions to a

roth retirement plan are ____________.

a.not tax deductible; not tax deducible

b.tax deductible; tax deductible

c.tax deductible; not tax deductible

d.not tax deductible; tax deductible