1) Companies can smooth reported income by strategically timing the recognition of

revenue and expenses to dampen the normal ups and downs of business activity.

2) GAAP requires that all exchange transactions be recorded at the fair value of the

exchanged assets. Thus, except in the rare case that the book value and the fair value of

exchanged assets are identical, gains (or losses) on exchanges should be expected.

3) The current asset turnover ratio helps the analyst spot efficiency gains from improved

accounts receivable and inventory management.

4) For purposes of impairment tests, the fair value of an asset is defined by the FASB as

the price that would be received to sell an asset in an orderly transaction between

market participants at the measurement date.

5) Cross-sectional analysis helps identify similarities and differences across companies

over time.

6) Cash flow from operating activities is very comparable across firms within the same

industry in the United States given that all firms must follow GAAP.

7) The current ratio will be lower over the lease term when the lessee treats the lease as

a capital lease rather than an operating lease.

8) The IASB and FASB are working together to develop a single set of high-quality,

compatible accounting standards that can be used for both domestic and cross-border

financial reporting.

9) Interest payments are included when computing the recognized gross profit on

installment sales.

10) Return on assets is defined as EBI divided by total year-end assets.

11) A contra account is an account that is subtracted from a related account.

12) Equity securities designated by the investor to be held for a short period of time are

classified as available-for-sale securities.

13) Taxable income is governed by the doctrine of constructive receipt or ability to pay.

14) To efficient market investors, financial statement data provide a basis for assessing

risk, dividend yield, or other firm attributes that are important to portfolio selection

decisions.

15) Many start-up high-growth companies use stock options as a means of attracting

talented employees while attempting to conserve cash.

16) While basic earnings per share (EPS) must be disclosed, management may opt to

place it in the notes to the financial statements.

17) Investors are uncertain about the quality of each company’s debt or equity offerings

because the ultimate return from the security depends on future events.

18) Stock options come in various forms, the choice of which is largely dependent on

the financial accounting treatment for the executive and the company.

19) Some capital providers possess enough bargaining power to allow them to compel

companies to deliver the financial information they need for analysis.

20) Similarities between U.S. GAAP and IFRS include which of the following?

A.Both U.S. GAAP and IFRS permit the same cost flow assumptions

B.Inventory is carried at the lower of cost or net realizable value under both U.S. GAAP

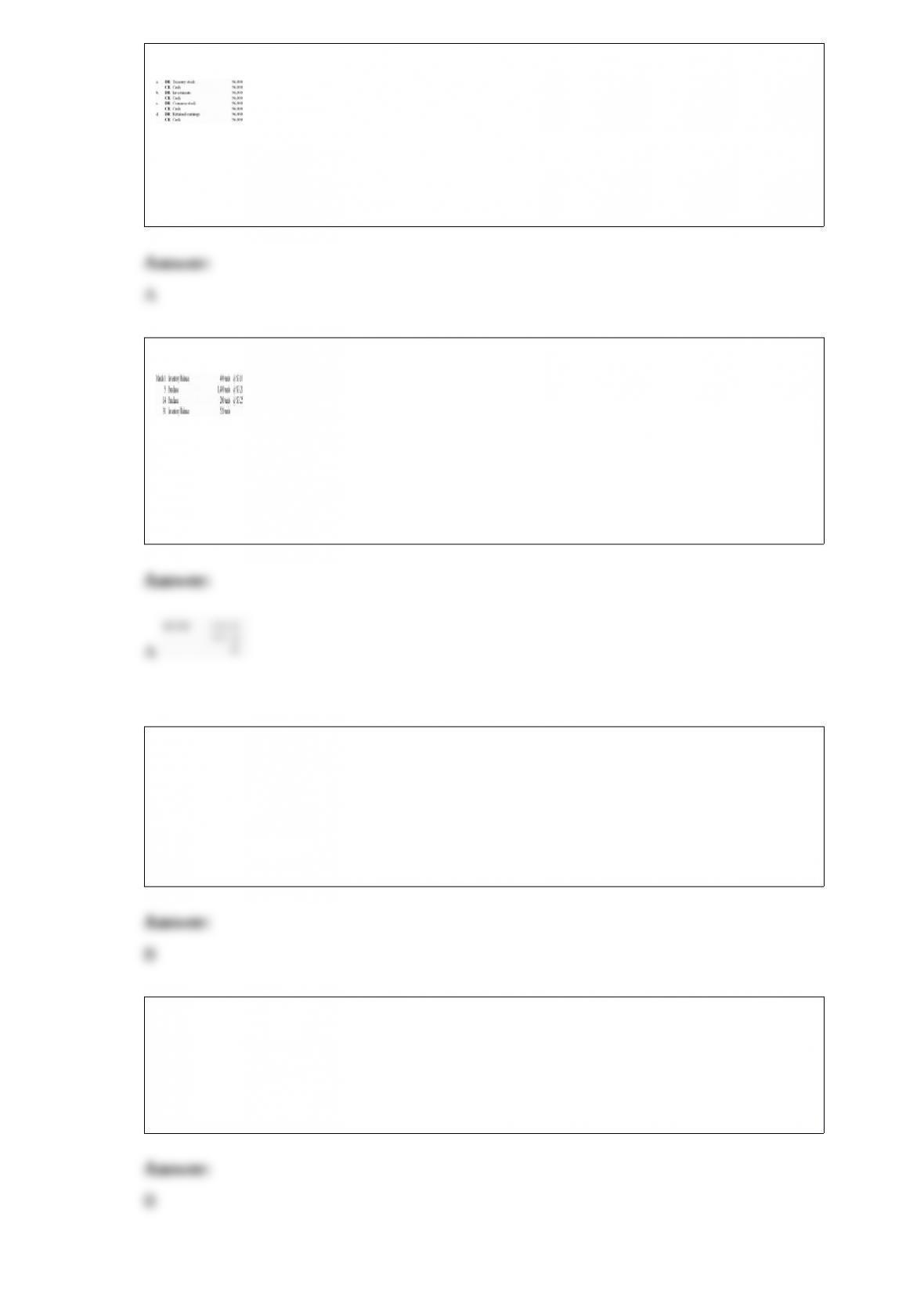

and IFRS

C.Direct costing is required under both U.S. GAAP and IFRS

D.The definition of inventory is similar in both U.S. GAAP and IFRS

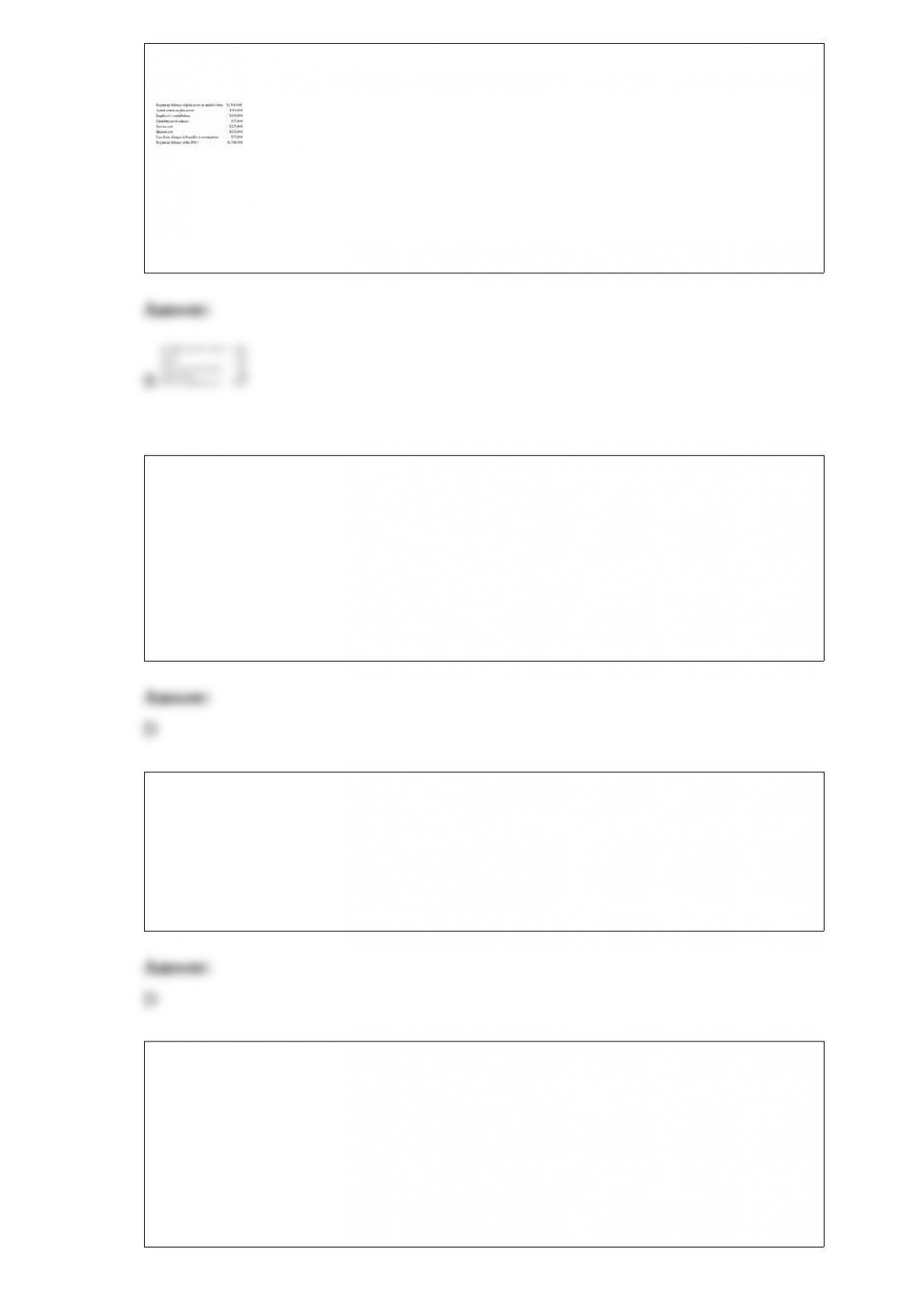

21) The trustee for the Bronson Corporation pension sent a report to the CEO with the

following information for the fiscal year:

The ending balance of the pension benefit obligation (PBO) is

A.$1,730,000

B.$1,821,000

C.$1,896,000

D.$1,971,000

22) Which of the following statements does not properly describe GAAP accounting for

derivatives?

A.Derivatives are reported within the balance sheet at fair value

B.Speculative investments in derivative contracts can increase earnings volatility

C.Changes in the fair value of a derivative must be included in net income when they

occur

D.A derivative’s unrealized holding gain or loss for a particular year is not a component

of that year’s income from operations

23) Which of the following is not a required disclosure pertaining to defined benefit

pension plans?

A.A reconciliation of the beginning and ending projected benefit obligation balances

B.The retirement benefits that are expected to be paid in the next five years

C.The amount of pension expense and its components

D.The contributions to be made into the pension fund for each of the next five years

24) A company issued 1,000 shares of $10 par value common stock due to a previously

declared stock dividend; the market value at both the date of declaration and

distribution was $12 per share. Which of the following correctly describes the reporting

of this stock issue within the financing activities section of the cash flow statement?

A.A cash outflow of $12,000

B.A cash outflow of $10,000

C.A cash outflow of $2,000

D.There is no cash flow

25) Under the accrual basis, how much revenue should Canon recognize in November?

A.$0

B.$16,000

C.$24,000

D.$40,000

26) A lender may be protected from deterioration of the borrower’s creditworthiness if

the commercial lending agreement requires the borrower to maintain a

A.current ratio above a certain level

B.return on assets above a certain level

C.specified return on equity

D.specified accounts receivable turnover

27) Analysts prefer the indirect method for the preparation of the cash flow statement

because the size and direction of the items reconciling net income to net cash flow from

operating activities provide a yardstick for measuring the

A.current ratio

B.return on assets

C.quality of earnings

D.rate of dividends

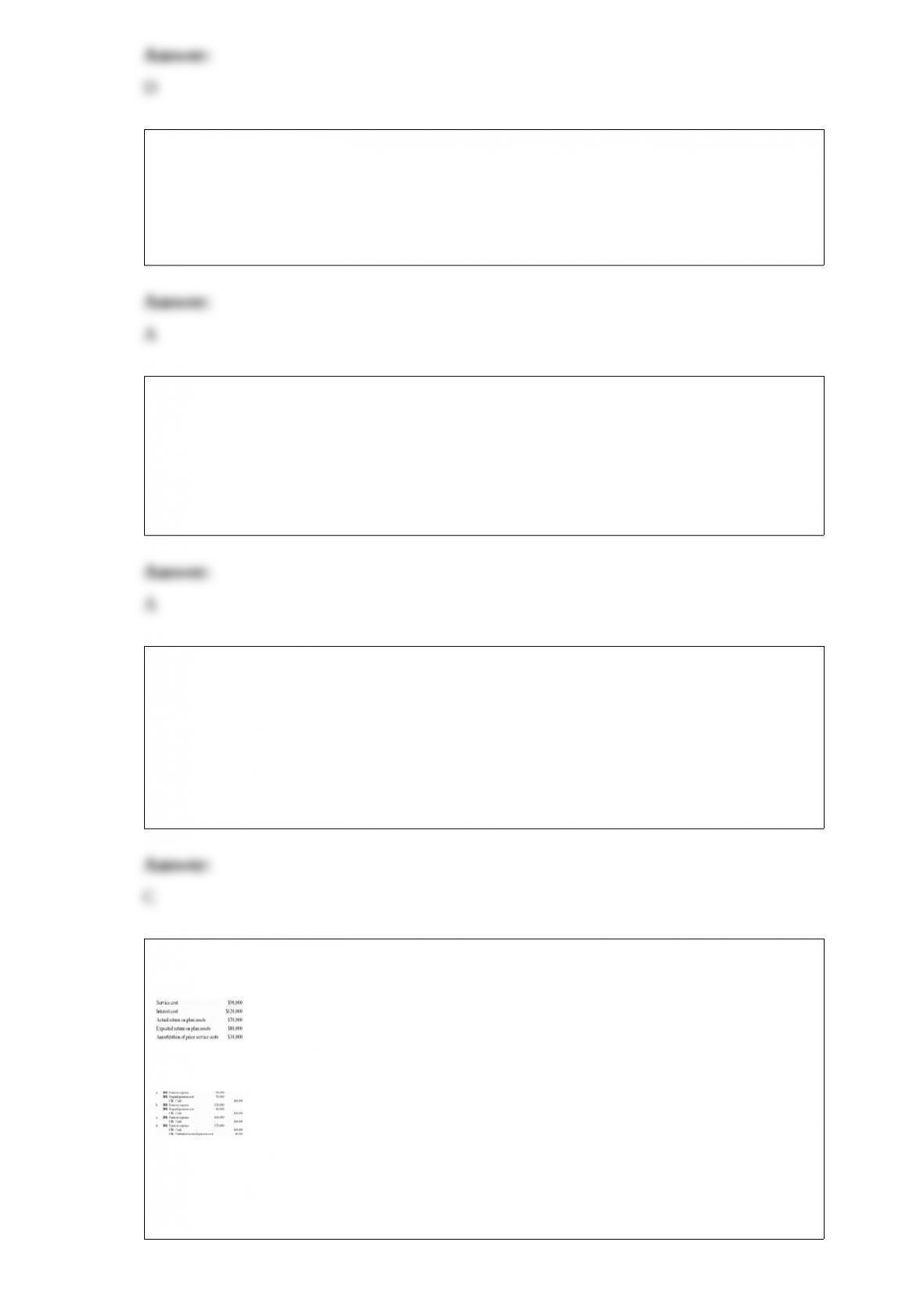

28) TKE Corporation established a defined benefit pension plan in 2009 . TKE has

provided the following information for the year ended December 31, 2011:

If the company contributes $160,000 cash to the pension plan trustee, which one of the

following journal entries properly records the payment?

A.Option a

B.Option b

C.Option c

D.Option d

29) When analysts provide basic EPS for income from continuing operations that

exclude the effects of special (i.e., nonrecurring) gains or losses and certain other

non-cash charges, such earnings are frequently referred to as

A.normal earnings

B.pro forma earnings

C.sustainable earnings

D.real earnings

30) As transitory or value-irrelevant components become a larger part of a firm’s

reported earnings, which of the following effects would you not expect to witness?

A.The quality of those reported earnings is eroded

B.The firm’s stock price rises in the year such components are reported proportionate to

their impact on income

C.Reported earnings become a less reliable indicator of the company’s long-run

sustainable cash flows

D.Earnings are a less reliable indicator of the firm’s fundamental value

31) Which of the following statements pertaining to lease accounting is not correct?

A.For a particular lease agreement, the amount of interest expense recorded by the

lessee can be different than the amount of interest revenue recorded by the lessor during

the same time period

B.The current ratio will be decreased over the lease term if a lessor treats a lease as a

capital lease rather than an operating lease

C.It is very challenging for different firms to treat virtually identical leases dissimilarly

due to the fact that the required lease capitalization criteria are difficult to circumvent

D.The required disclosures pertaining to operating leases require the lessee to disclose

what the impact on the financial statements would have been if the lease would have

been treated as a capital lease

32) The Marino Company has provided you the following information pertaining to its

defined benefit pension plan that was adopted on January 1, 2011:

The service cost was $950,000 during 2011 and $1,045,000 during 2012 .

The prior service cost amortization each year was $290,000.

The contribution to the pension plan was $1,500,000 on December 31, 2011 and

$1,800,000 on December 31, 2012 .

The actuarially determined discount rate and the expected return on plan assets was

10%.

The actual return on plan assets was 9.5%.

Retirement benefits pertaining to years of service prior to 2011 were granted to the

employees. The prior service cost is being amortized over the remaining ten-year life of

the employees.

What is the pension expense for the year ended December 31, 2011?

A.$1,240,000

B.$1,530,000

C.$950,000

D.$1,380,000

33) TAD, Inc. uses the lower of cost or market method to value inventory. If the

inventory value is replacement cost, which one of the following statements is true?

A.Historical cost is less than replacement cost

B.Replacement cost is greater than net realizable value less a normal profit margin

C.Replacement cost is greater than historical cost

D.Net realizable value is greater than historical cost

34) Sand engaged in operations at the start of 2011 and reported $550,000 in pre-tax

book income for the year. Tax depreciation for Sand exceeded book depreciation by

$50,000. The tax rate for 2011 was 30%, and Congress had enacted a tax rate of 20%

for the years after 2011 .

What is the current portion of the tax expense for Sand for 2011?

A.$100,000

B.$150,000

C.$160,000

D.$165,000

35) According to generally accepted accounting principles, revenue should be

recognized at the earliest time when

A.the “critical event” has taken place and the proceeds are collected

B.the “critical event” has taken place and the amount of revenue collected is reasonably

assured

C.collection is reasonably assured and the “critical event” can be measured

D.collection has taken place and the “critical event” can be measured

36) The Mick Company reported a LIFO cost of goods sold for the year of $100,000.

The LIFO reserve decreased by $30,000 for the year. An estimate of the cost of goods

sold under FIFO is

A.$70,000

B.$130,000

C.$160,000

D.$200,000

37) Which of the following is true regarding IFRS?

A.Equity method investments may be accounted for under the fair value option if this

option is selected at the inception of the investment

B.All impairment losses for Available-For-Sale debt securities are recognized in income

regardless of reason

C.Fair value is used for debt and equity securities held in the trading portfolio with FV

unrealized gains/losses reported in other comprehensive income

D.All of the choices are correct regarding IFRS

38) Selected data for Kris Corporation’s comparative balance sheets for Year 1 and Year

2 are as follows:

What are Kris’ cash flows from investing activities for Year 2?

A.$0

B.$100,000 inflow

C.$100,000 outflow

D.$350,000 outflow

39)

The implied total earnings multiple of Firm A is

A.1.00

B.4.10

C.5.00

D.10.00

40) Changes in a company’s capital expenditures or fixed asset sales over time must

A.be carefully analyzed for changes in the company’s strategy

B.be indicative of changes in the company’s strategy

C.indicate incompetent management

D.raise the company’s risk of default on its debt

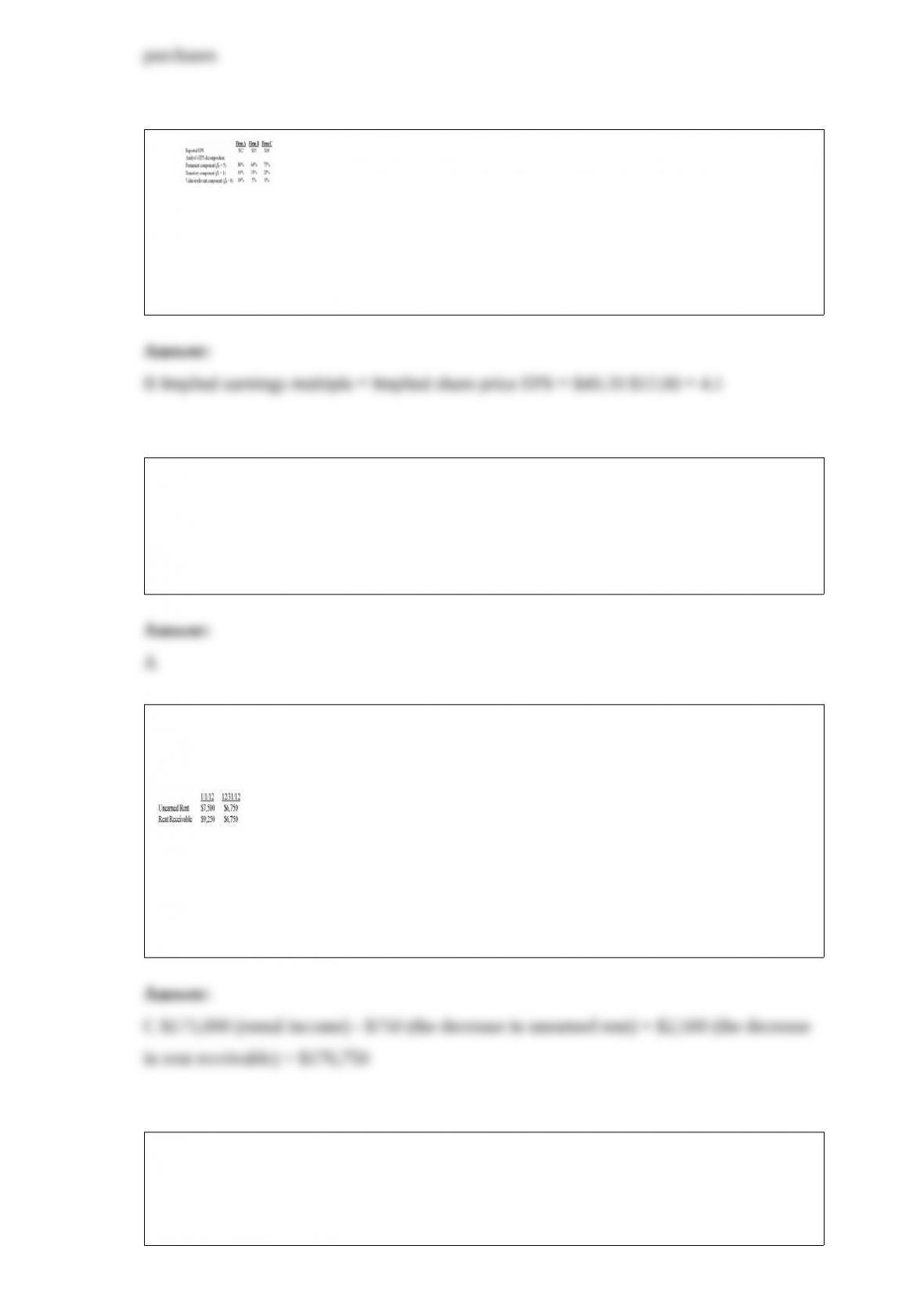

41) The Superior Real Estate Corporation reported rental income totaling $175,000 for

the year ending December 31, 2012 . The following information was obtained from

Superior Corporation’s balance sheets:

How much cash did Superior collect from its tenants during 2012?

A.$175,750

B.$178,250

C.$176,750

D.$171,750

42) The Vernon Corporation was formed on January 2, 2011 . The company sold 20,000

shares of $8.00 par value stock for $20.00 per share. On July 1, 2011, Vernon bought

back 4,000 shares of stock for $24.00 per share. The treasury stock was resold on

September 1, 2011 for $32.00 per share.

Which one of the following is the correct entry to record the purchase of treasury stock?

A.Option a

B.Option b

C.Option c

D.Option d

43) The following information pertains to the Fan Company’s inventory item B1008:

In a periodic inventory system, the ending LIFO inventory is

A.$1,624

B.$1,655

C.$1,678

D.$1,733

44) The allocation of the tax cost (benefit) across various components of book income

within a given period is called

A.interperiod tax allocation

B.intraperiod tax allocation

C.current income tax allocation

D.constructive receipt allocation

45) Bond investments made to generate trading gains are classified as

A.available-for-sale securities

B.trading securities

C.held to maturity securities

D.minority securities

46) In the case of goods sold on layaway,

A.the seller should not recognize revenue until the products are delivered to the

customer

B.the cash received to date should be recognized as an asset until merchandise is

delivered to the customer

C.revenue should be recognized under the installment sales method

D.the seller should recognize revenue before products are delivered to the customer

47) What will be the expected abnormal earnings of a firm which has earnings of

$40,000 with a required equity cost of capital of 10%, when the book value at the

beginning of period is $800,000?

A.$(40,000)

B.$(80,000)

C.$40,000

D.$80,000

48) Davis Company began manufacturing operations on January 2, 2011 . During 2011

Davis earned a pre-tax book income of $85,000 and had taxable income of $75,000.

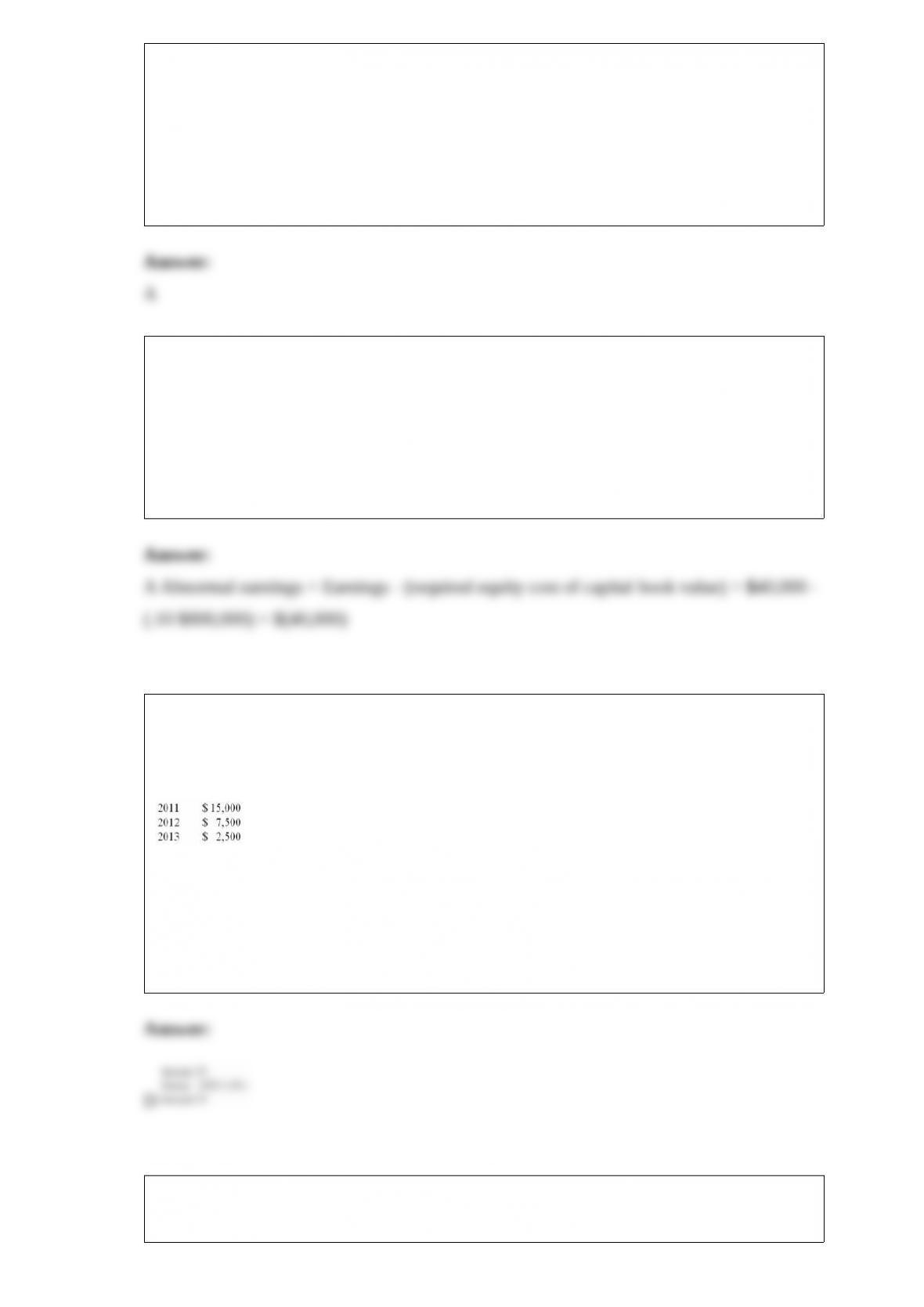

Davis had a temporary difference relating to a prepaid asset that will be expensed as

follows for book purposes:

The enacted tax rates are 30% for 2011 and 2012; and 40% for subsequent years.

Income tax expense for 2011 is

A.$30,000

B.$25,750

C.$22,500

D.$19,250

49) The failure of a company to pay other debts, such as payables or other loans, when

due is called

A.routine default

B.non-default

C.cross default

D.compliance default

50) Ambiguity can arise as to whether receivables have been sold or instead are being

used as collateral for a loan whenever certain obligations, duties, or rights regarding the

transferred receivables are retained by the transferor. In distinguishing between sales

and collateralized borrowings using receivables, the critical issue

A.is whether the terms regarding the transfer were initiated by the transferor or

transferee

B.is whether the transferor surrenders control over the receivables

C.comes down to how clearly the rights, etc. being retained are specified in the transfer

agreement

D.is whether any gain or loss related to the transfer is recognized in earnings

51) When receivables are bundled together and transferred to another organization that

issues securities collateralized by the transferred receivables, the arrangement is

A.collateralization

B.discounting

C.factoring

D.securitization

52) What is meant by sustainable earnings?

53) Swan Company has provided you with the following data pertaining to their

pension plan for the year ended December 31, 2011:

The 2011 service cost was $175,500.

The projected benefit obligation as of January 1, 2011 was $1,950,000.

Plan assets as of January 1, 2011 totaled $2,020,000.

The actual return on plan assets during 2011 was 10%.

Amortization of prior service costs during 2011 was $9,750.

The expected return on plan assets was 8%.

The pension plan funding during 2011 totaled $170,000.

The settlement/discount rate was 8%.

Prepare the journal entry to record pension expense for the year ended December 31,

2011 .

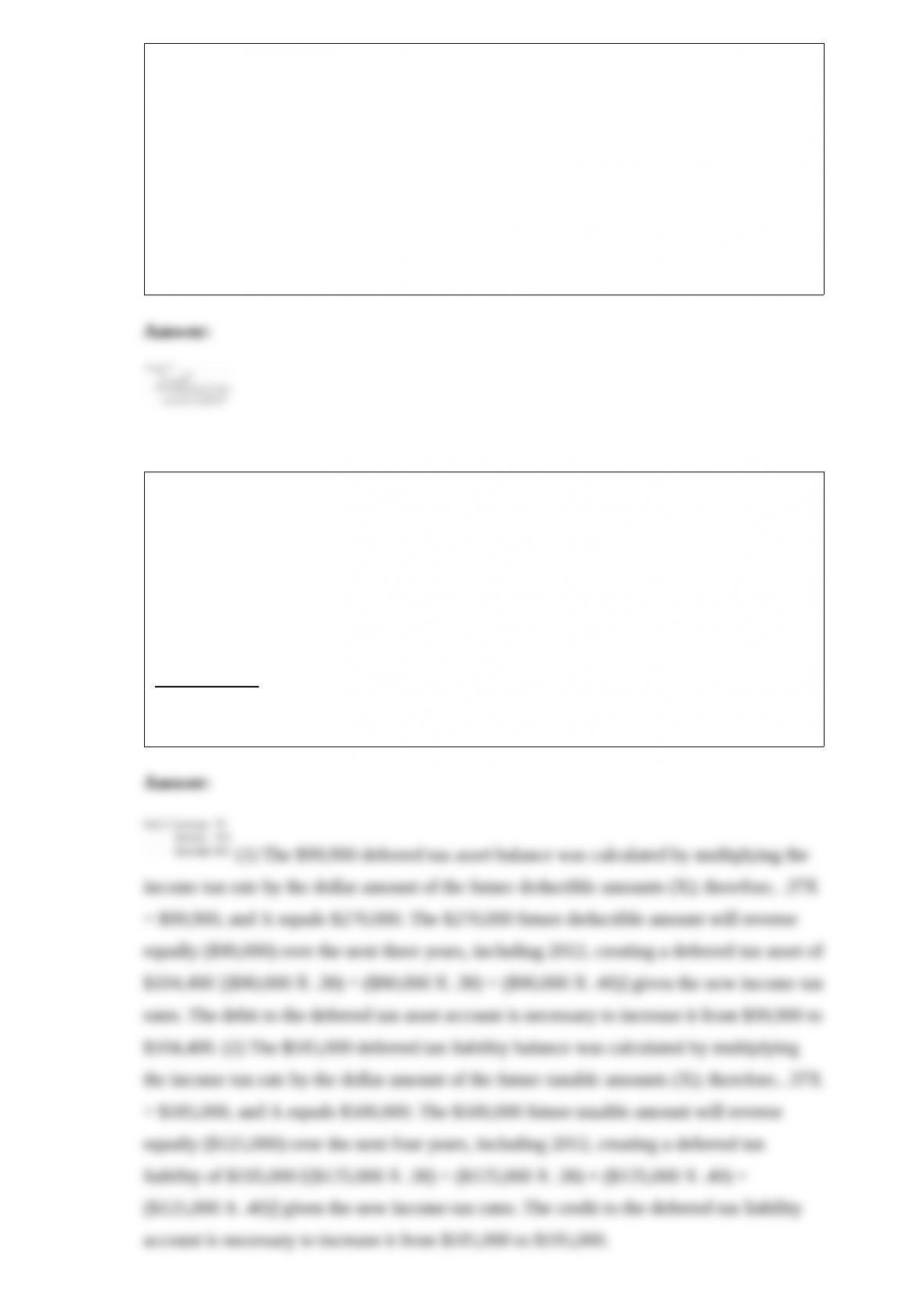

54) On January 1, 2012, Sun Company’s balance sheet reported a deferred tax liability

of $185,000 and a deferred tax asset of $99,900. The future taxable amounts that

existed as of January 1, 2012 will reverse equally over the next four years beginning in

2012, while the future deductible amounts that existed as of January 1, 2012 will

reverse equally over the next three years beginning in 2012 . The enacted income tax

rate for all tax years as of January 1, 2012 was 37%. On February 1, 2012, the tax laws

were amended resulting in income tax rates of 38% for 2012 and 2013; the income tax

rate will be 40% for tax years 2014 and later.

Requirement:

Prepare the journal entry on February 1, 2012 to record the impact of the amended

income tax rates.

55) The following inventory valuation errors have been discovered for Jellison

Corporation:

The 2009 year-end inventory was overstated by $19,000.

The 2010 year-end inventory was overstated by $46,000.

The 2011 year-end inventory was understated by $22,000.

Jellison’s reported income before income taxes in these years was as follows:

Determine what income before taxes for 2009, 2010, 2011 should have been after

correcting for the errors.

56) Denver Co. acquired a large rotary forge to be used in its manufacturing process

from a competitor that was going out of business. The following costs were incurred by

Denver in connection with the acquisition:

Required:

How much should Denver Co. capitalize to the machinery account?

57) The Sports Corporation previously issued convertible bonds with a maturity value

of $5,000,000; the book value of the bonds as of October 1, 2012 was $5,250,000. Each

$1,000 bond is convertible into 100 shares of $5 par value common stock. On October

1, 2012, bonds with a maturity value of $2,000,000 were converted into common stock;

the common stock’s market value on the conversion date was $12.75 per share. Prepare

the journal entry to record the bond conversion given the above facts only.

58) Stock markets are common in many countries and economies. Explain the need for

and use of a stock market in an economy.

59) A component of an entity may be a reportable segment or operating segment, a

reporting unit, a subsidiary, or an asset group. An asset group represents the highest

level for which identifiable cash flows are largely independent of the cash flows of

other components of the entity.

FALSE

As asset group represents the

60) Jones Corporation wrote off $150,000 of obsolete inventory at December 31, 2011 .

Required:

Describe the effect of this write-off on the company’s 2011 current and quick ratios.