Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

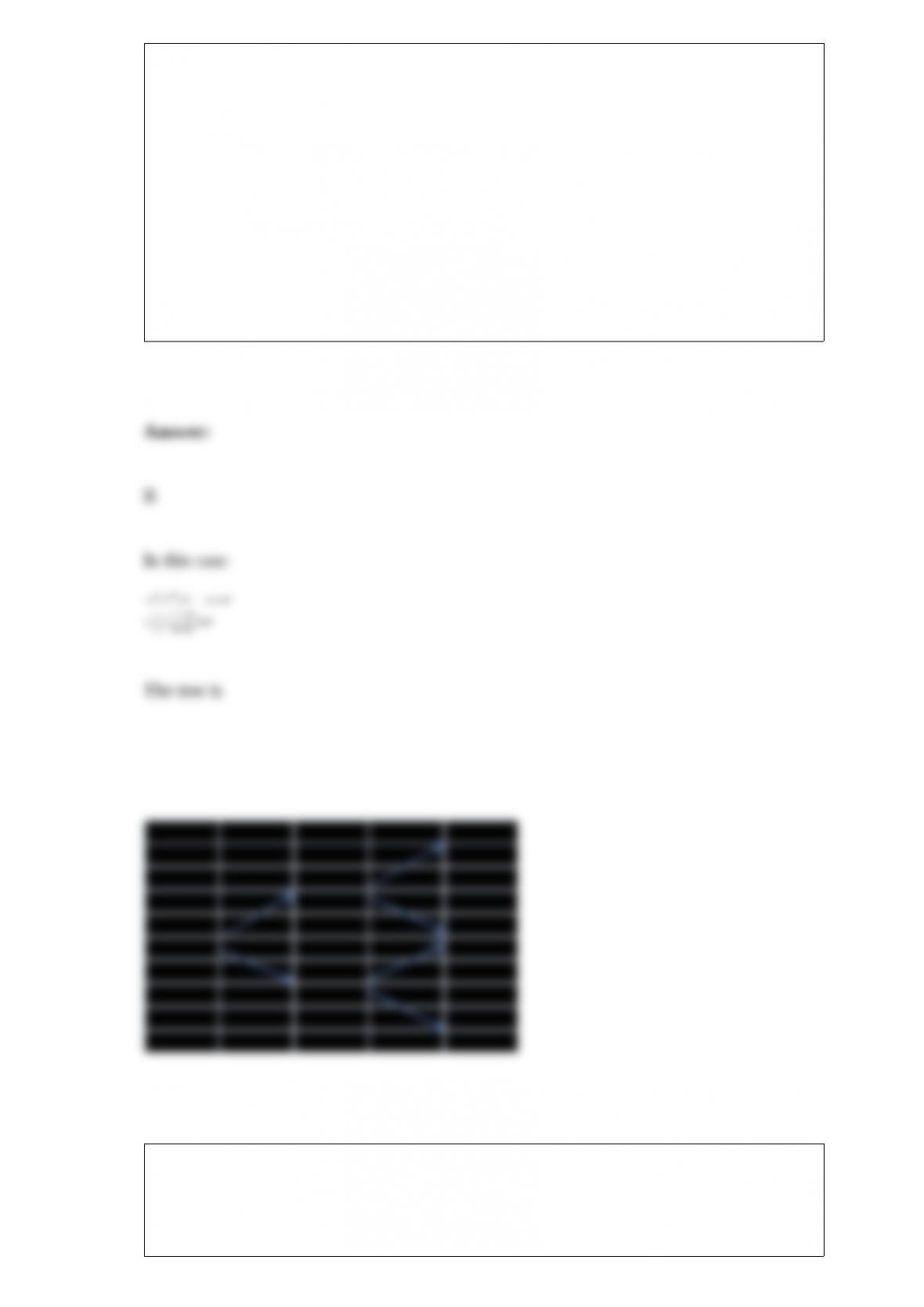

The current price of a non-dividend paying stock is $50. Use a two-step tree to value an

American put option on the stock with a strike price of $48 that expires in 12 months.

Each step is 6 months, the risk free rate is 5% per annum, and the volatility is 20%.

Which of the following is the option price?

A. $1.95

B. $2.00

C. $2.05

D. $2.10

A one-year call option on a stock with a strike price of $30 costs $3; a one-year put

option on the stock with a strike price of $30 costs $4. Suppose that a trader buys two

call options and one put option. The breakeven stock price above which the trader

makes a profit is

A. $35

B. $40

C. $30

D. $36

A trader uses 3-month Eurodollar futures to lock in a rate on $5 million for six months.

How many contracts are required?

A. 5

B. 10

C. 15

D. 20

Which of the following describes the five-year swap rate?

A. The rate on a five-year loan to a AA-rated company

B. The rate on a five-year loan to an A-rated company

C. The rate that can be earned over five years from a series of short-term loans to

AA-rated companies

D. The rate that can be earned over five years from a series of short-term loans to

A-rated companies

Which of the following describes a protective put?

A. A long put option on a stock plus a long position in the stock

B. A long put option on a stock plus a short position in the stock

C. A short put option on a stock plus a short call option on the stock

D. A short put option on a stock plus a long position in the stock

Which of the following is true of a positive semi-definite variance-covariance matrix

A. All elements of the matrix are positive

B. The determinant of the matrix is positive

C. The matrix has ones on the diagonal

D. The matrix is internally consistent

A short forward contract that was negotiated some time ago will expire in three months

and has a delivery price of $40. The current forward price for three-month forward

contract is $42. The three month risk-free interest rate (with continuous compounding)

is 8%. What is the value of the short forward contract?

A. +$2.00

B. -$2.00

C. +$1.96

D. -$1.96

A company surprises the market with an announcement that it has granted stock options

to senior executives. The options are exercised four years later. When does dilution take

place?

A. Dilution takes place when the options are exercised

B. Dilution takes place on the announcement date

C. Dilution takes place gradually over the four years

D. There is no dilution

Accountants like to value a derivatives portfolio at

A. The bid price

B. The offer price

C. The exit price

D. Original cost less depreciation

The price of a stock is $64. A trader buys 1 put option contract on the stock with a strike

price of $60 when the option price is $10. When does the trader make a profit?

A. When the stock price is below $60

B. When the stock price is below $64

C. When the stock price is below $54

D. When the stock price is below $50

Which of the following is true of LIBOR

A. The LIBOR rate is free of credit risk

B. A LIBOR rate is lower than the Treasury rate when the two have the same maturity

C. It is a rate used when borrowing and lending takes place between banks

D. It is subject to favorable tax treatment in the U.S.

Which of the following is NOT true about a range forward contract?

A. It ensures that the exchange rate for a future transaction will lie between two values

B. It can be structured so that it costs nothing to set up

C. It requires a forward contract as well as two options

D. It can be used to hedge either a future inflow or a future outflow of a foreign

currency

The current price of a non-dividend-paying stock is $30. Over the next six months it is

expected to rise to $36 or fall to $26. Assume the risk-free rate is zero. An investor sells

six-month call options with a strike price of $32. Which of the following hedges the

position?

A. Buy 0.6 shares for each call option sold

B. Buy 0.4 shares for each call option sold

C. Short 0.6 shares for each call option sold

D. Short 0.4 shares for each call option sold

Which of the following best describes a central clearing party

A. It is a trader that works for an exchange

B. It stands between two parties in the over-the-counter market

C. It is a trader that works for a bank

D. It helps facilitate futures trades

A one-year forward contract is an agreement where

A. One side has the right to buy an asset for a certain price in one year€s time.

B. One side has the obligation to buy an asset for a certain price in one year€s time.

C. One side has the obligation to buy an asset for a certain price at some time during the

next year.

D. One side has the obligation to buy an asset for the market price in one year€s time.