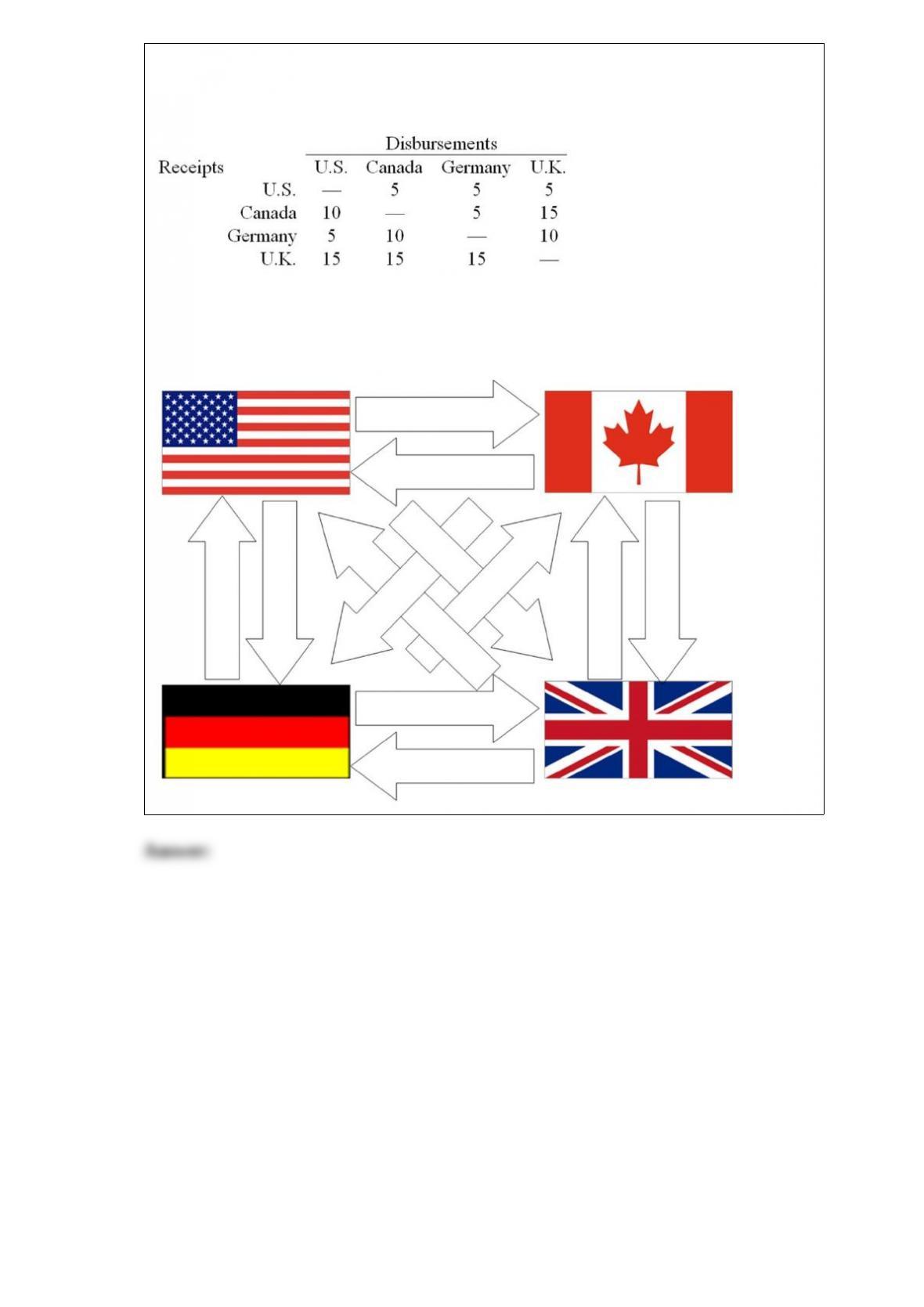

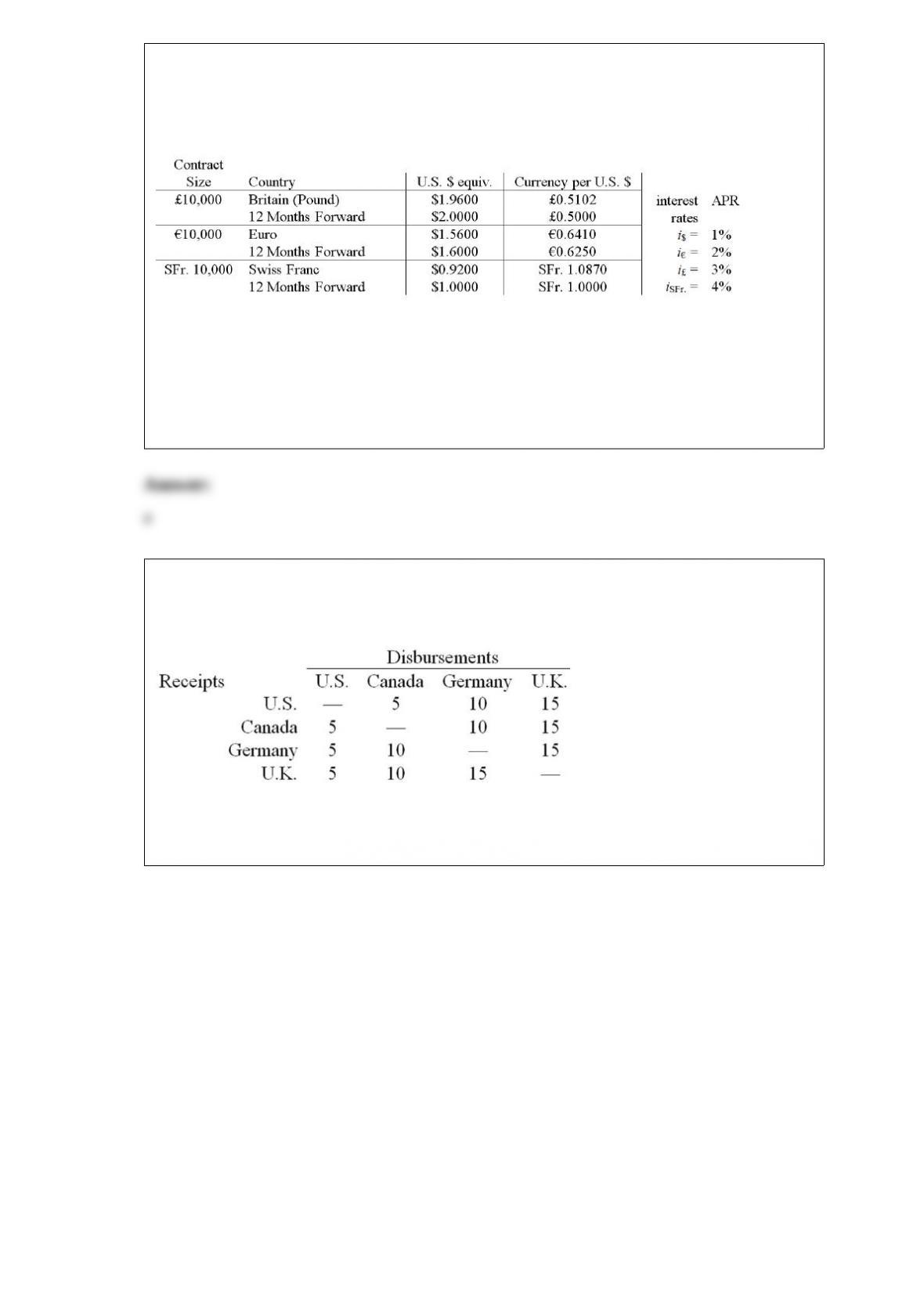

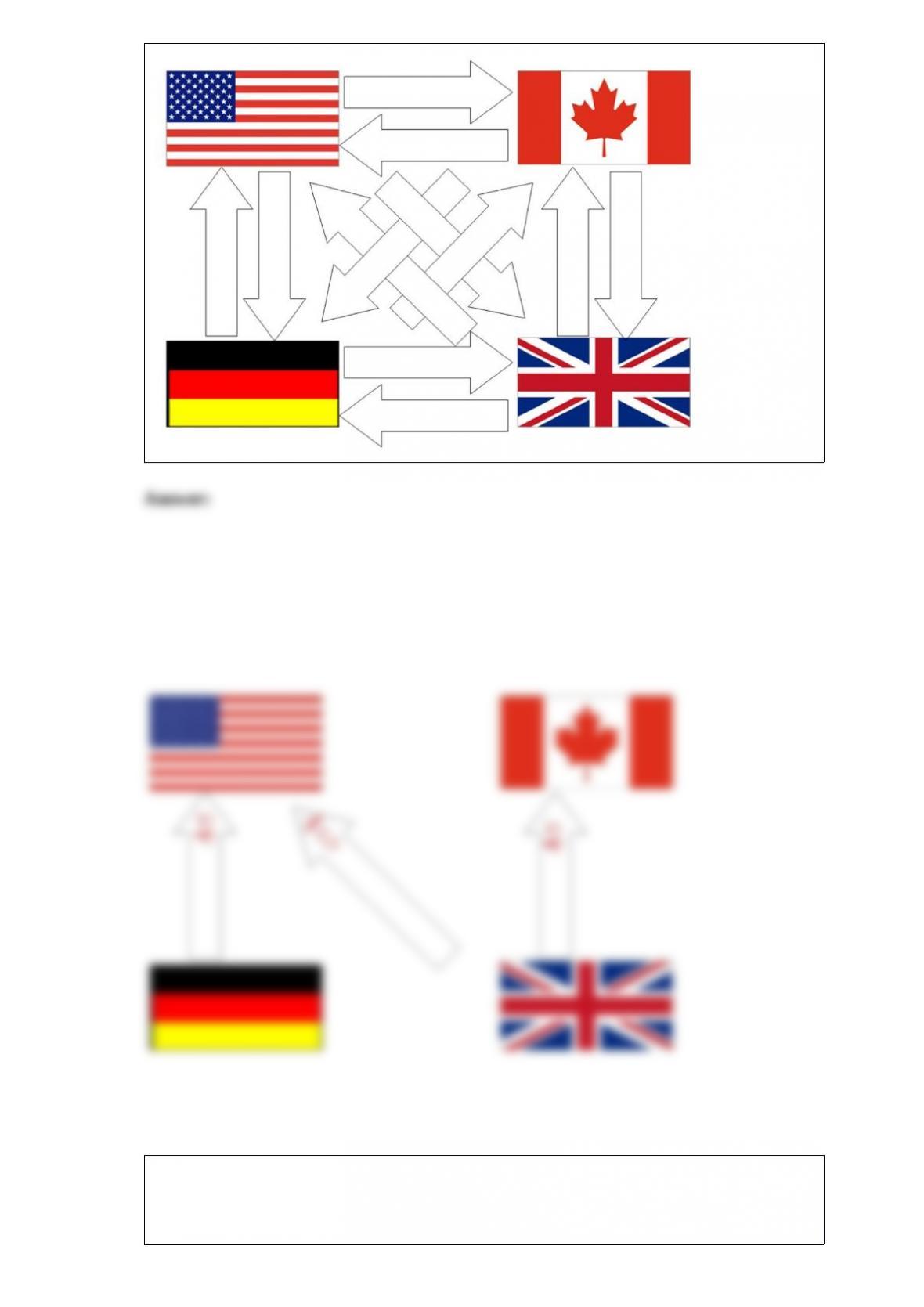

1) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

using your results to the last question, use bilateral netting to simplify.

2) if you could accurately and consistently forecast exchange rates

a.this would be a very handy thing as girls prefer guys with skills

b.you could impress your dates

c.you could make a great deal of money

d.all of the above

3) the first adrs began trading ________ as a means of eliminating some of the risks,

delays, inconveniences, and expenses of trading the actual shares.

a.in 1997

b.in 1987

c.in 1977

d.in 1927

4) under the theory of comparative advantage, liberalization of international trade will

a.enhance the welfare of the world’s citizens

b.create unemployment and displacement of workers permanently

c.result in higher prices in the long run as monopolist are able to charge higher prices

after eliminating their competitors

d.all of the above

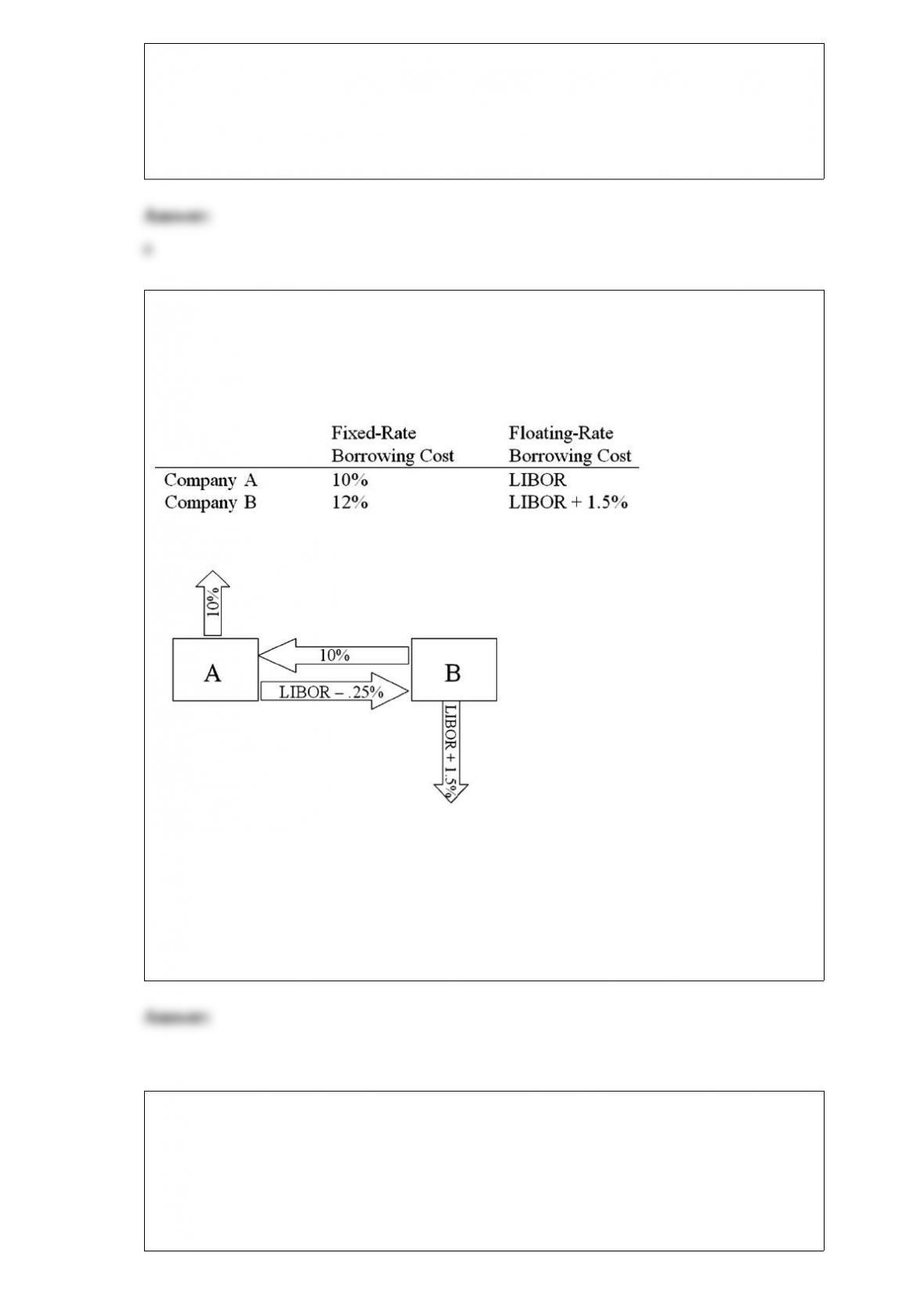

5) compute the payments due in the second year on a three-year amortizing swap from

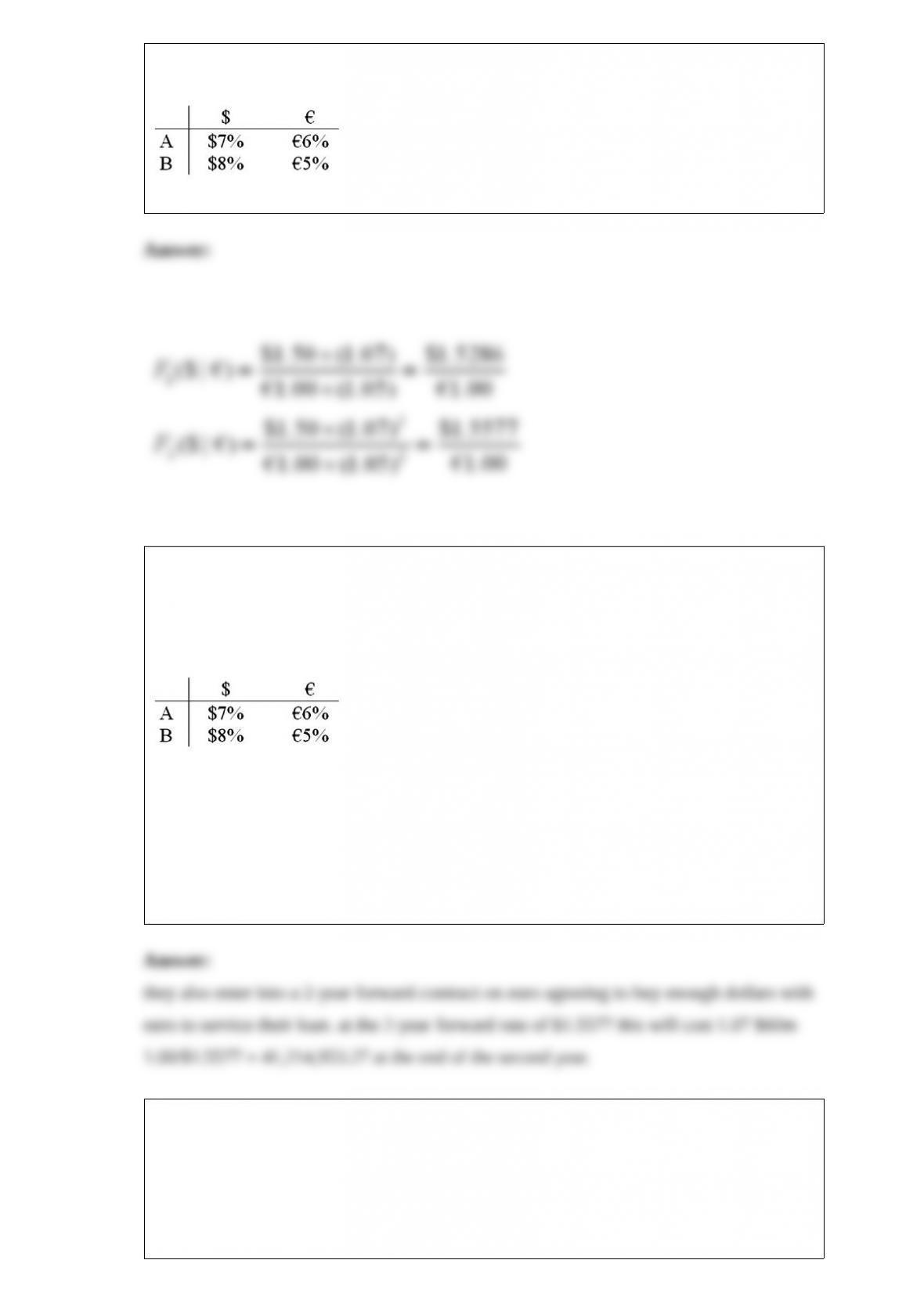

company b to company a. company a and company b both want to borrow £1,000,000

for three years. a wants to borrow floating and b wants to borrow fixed. a and b agree to

split the qsd.

a.b pays £402,114.80 to a

b.b pays £100,000 to a

c.b pays £69,788.52 to a

d.none of the above

6) with a mnc

a.the decision to set a transfer price is further complicated by import duty

considerations

b.the decision to set a transfer price can be further complicated by exchange rate

restrictions imposed by governments

c.the decision to set a transfer price is further complicated by tax considerations, if there

is a difference in tax rates between the host country and the home country

d.all of the above

7) a japanese importer has a 1,000,000 payable due in one year.

the one-year risk free rates are i$ = 4.03%; i = 6.05%; and i¥ = 1%. detail a strategy

using forward contracts that will hedge his exchange rate risk. have an estimate of how

many contracts of what type.

a.go short in 12 yen forward contracts. go long in 16 euro contracts

b.go long in 12 yen forward contracts. go short in 16 euro contracts

c.go short in 16 yen forward contracts. go long in 12 euro contracts

d.none of the above

8) also, mncs often find it profitable to locate manufacturing/processing facilities near

a.the home office to exploit their assets in place

b.the natural resources in order to save transportation costs

c.their competitor’s manufacturing plant to even out the playing field with regard to

shipping costs

d.none of the above

9) assume that xyz corporation is a leveraged company with the following information:

kl = cost of equity capital for xyz = 13%

i = before-tax borrowing cost = 8%

t = marginal corporate income tax rate = 30%

calculate the debt-to-total-market-value ratio that would result in xyz having a weighted

average cost of capital of 9.3%.

a.35%

b.40%

c.45%

d.50%

10) investors will generally accept a lower yield on ________ than on __________ of

comparable terms, making them a less costly source of funds for the issuer to service.

a.bearer bonds; registered bonds

b.registered bonds; bearer bonds

c.eurobonds; domestic bonds

d.domestic bonds; eurobonds

11) suppose that the current exchange rate is 0.80 = $1.00. the direct quote, from the

u.s. perspective is

a.1.00 = $1.25

b.0.80 = $1.00

c.£1.00 = $1.80

d.none of the above

12) as of today, the spot exchange rate is 1.00 = $1.50 and the rates of inflation

expected to prevail for the next year in the u.s. is 2% and 3% in the euro zone. what is

the one-year forward rate that should prevail?

a.1.00 = $1.5147

b.1.00 = $1.4854

c.1.00 = $0.6602

d.$1.00 = 0.6602

13) a translation exposure report shows, for each account that is included in the

consolidated balance sheet,

a.the amount of foreign exchange exposure that exists for each foreign subsidiary in

which the mnc has a material interest

b.the amount of foreign exchange exposure that exists on a net basis for the firm

c.the amount of foreign exchange exposure that exists for each foreign currency in

which the mnc has exposure

d.none of the above

14) “dragon” bonds are

a.dollar-denominated foreign bonds originally sold to u.s. investors

b.dollar-denominated bonds originally sold in asia with non-japanese issuers

c.pound sterling-denominated foreign bonds originally sold in the u.k

d.none of the above

15) the term interest rate swap

a.refers to a ‘single-currency interest rate swap” shortened to “interest rate swap”

b.involves “counterparties” who make a contractual agreement to exchange cash flows

at periodic intervals

c.can be “fixed-for-floating rate” or “fixed-for-fixed rate”

d.all of the above

16) the “world beta” measures the

a.unsystematic risk

b.sensitivity of returns on a security to world market movements

c.risk-adjusted performance

d.risk of default and bankruptcy

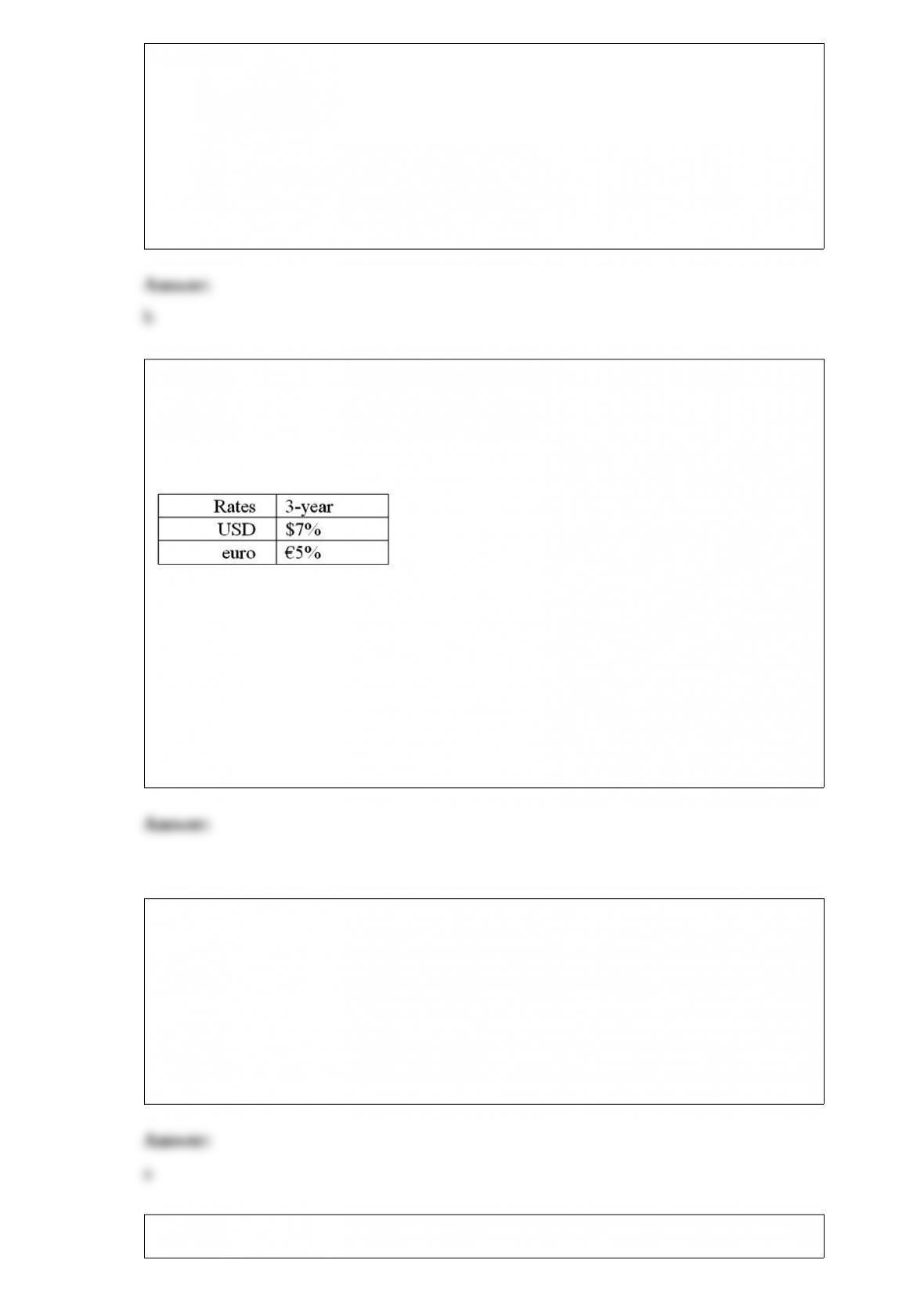

17) suppose that you are a swap bank and you notice that interest rates on coupon bonds

are as shown. develop the 3-year bid price of a euro swap quoted against flat usd libor.

the current spot exchange rate is $1.50 per 1.00. the size of the swap is 40 million

versus $60 million.

in other words, what you be willing to pay in euro against receiving usd libor?

a.7%

b.6%

c.5%

d.none of the above

18) a transfer price

a.is the price that one division of a firm charges to another division of a firm

b.is an accounting issue, not a finance issue

c.does not involve actual cash flows, therefore does not impact the share price

d.none of the above

19) your firm is a swiss importer of bicycles. you have placed an order with an italian

firm for 1,000,000 worth of bicycles. payment (in euro) is due in 12 months. use a

money market hedge to redenominate this one-year receivable into a swiss

franc-denominated receivable with a one-year maturity.

the following were computed without rounding. select the answer closest to yours.

a.sfr. 1,728,900.26

b.sfr. 1,600,000

c.sfr. 1,544,705.88

d.sfr. 800,000

20) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

using your results to the last question, use bilateral netting.

21) consider the situation of firm a and firm b. the current exchange rate is $1.50/. firm

a is a u.s. mnc and wants to borrow 40 million for 2 years. firm b is a french mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown;

both firms have aaa credit ratings.

what are the irp 1-year and 2-year forward exchange rates?

22) consider the situation of firm a and firm b. the current exchange rate is $1.50/. firm

a is a u.s. mnc and wants to borrow 40 million for 2 years. firm b is a french mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown;

both firms have aaa credit ratings.

explain how firm a could use the forward exchange markets to redenominate a 2-year

$60m 7% usd loan into a 2-year euro denominated loan.

firm a could borrow $60m today and exchange for 40m at today’s spot rate.

then they could enter a 1-year forward contract on euro agreeing to buy enough dollars

with euro to service their loan. at the 1-year forward rate of $1.5268 this will cost .07

$60m 1.00/$1.5268 = 2,747,663.55 in one year.

23) the time from acceptance to maturity on a $500,000 banker’s acceptance is 270

days.

the importing bank’s acceptance commission is 0.75 percent and that the market rate for

270-day b/as is 4 percent.

calculate the amount the banker will receive if the exporter discounts the b/a with the

importer’s bank.

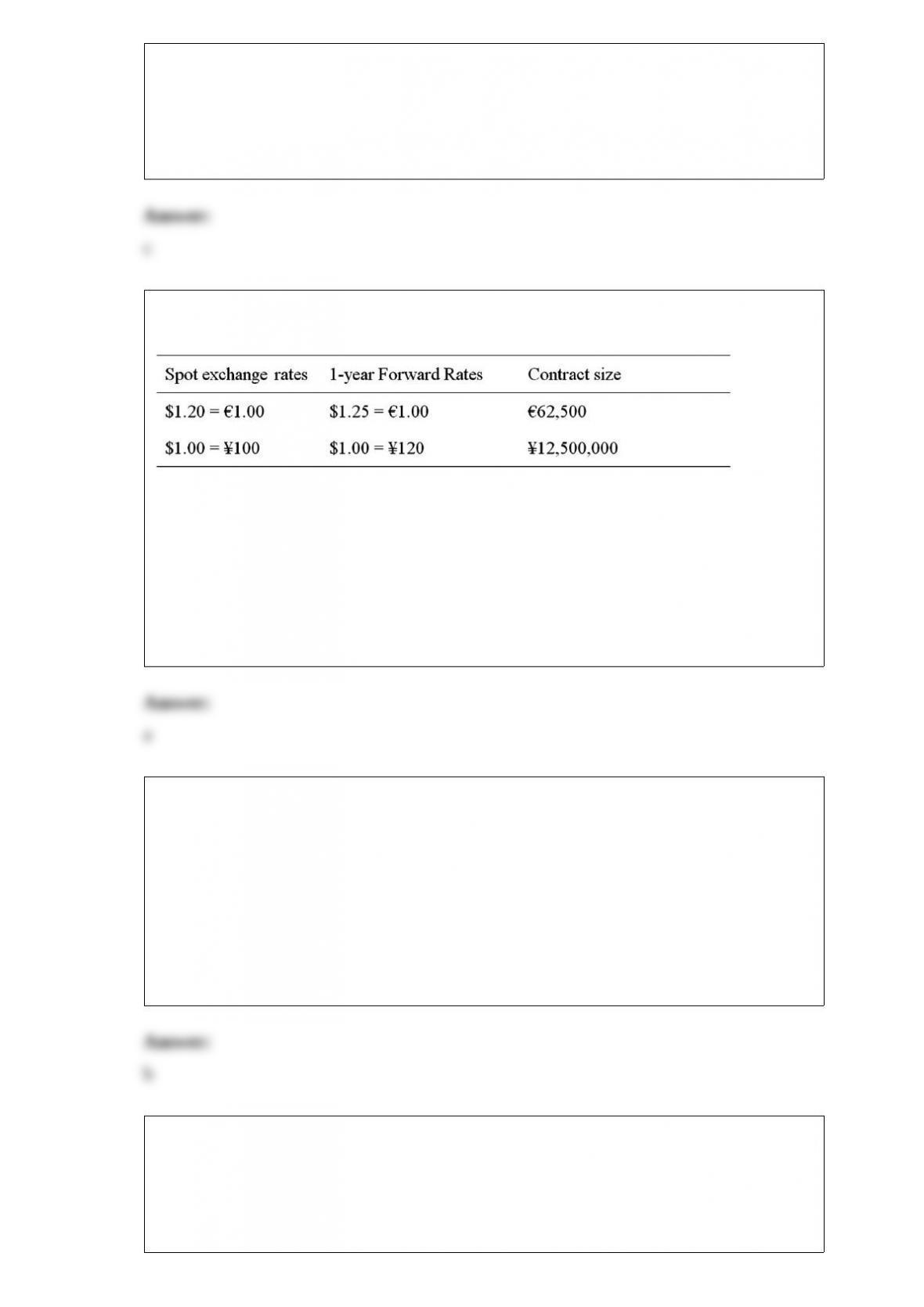

24) verify that the dollar value of your put option equals the dollar value of your call.

your answer is worth zero points if it does not include currency symbols ($,)!

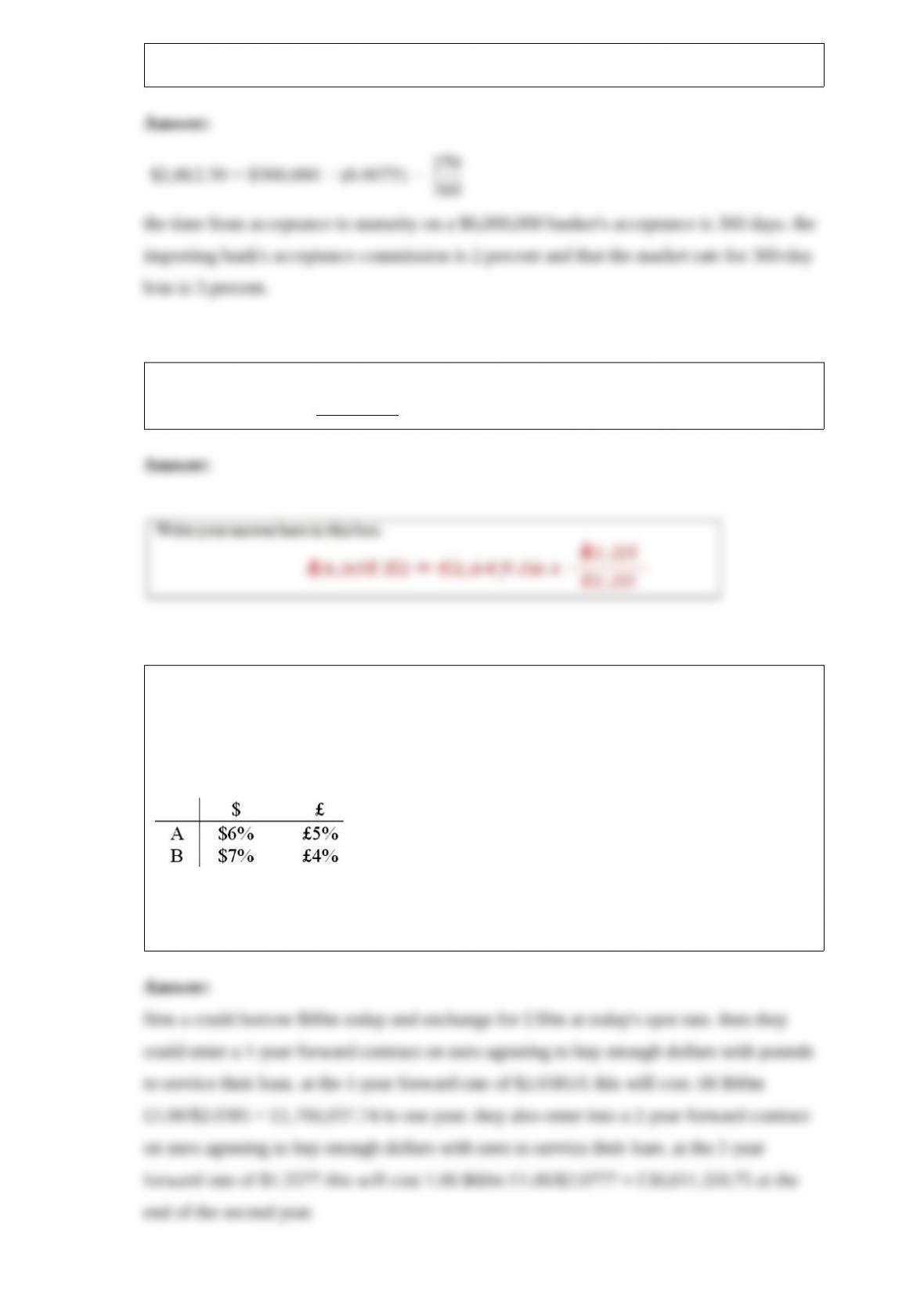

25) consider the situation of firm a and firm b. the current exchange rate is $2.00/£ firm

a is a u.s. mnc and wants to borrow £30 million for 2 years. firm b is a british mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown,

both firms have aaa credit ratings.

explain how firm a could use the forward exchange markets to redenominate a 2-year

$60m 6% usd loan into a 2-year pound denominated loan.

26) the time from acceptance to maturity on a $2,000,000 banker’s acceptance is 90

days.

the importing bank’s acceptance commission is 1.25 percent and that the market rate for

90-day b/as is 6 percent.

determine the amount the exporter will receive if he holds the b/a until maturity.