1) Between 1994 and 2004, the standard deviation of the returns for the S&P 500 and

the NYSE indexes were 0.27 and 0.14, respectively, and the covariance of these index

returns was 0.03. What was the correlation coefficient between the two market

indicators?

a. 1.26

b. 0.7937

c. 0.2142

d. 0.1111

e. 0.44

2) Which of the following is not a value-weighted series?

a.NASDAQ Industrial Index

b.Dow Jones Industrial Average

c.Wilshire 5000 Equity Index

d.American Stock Exchange Series

e.NASDAQ Composite Index

3) A graph of a bond’s Price-Yield curve reveals all of the following except

a. Price moves inverse to yield

b. The bond sells at a premium when the yield is below the coupon rate

c. The bond sells at a discount when the yield is above the coupon rate

d. The Price-Yield curve in concave

e. All of the above are characteristics of the Price-Yield curve

4) Consider a risky asset that has a standard deviation of returns of 15. Calculate the

correlation between the risky asset and a risk free asset.

a. 1.0

b. 0.0

c. -1.0

d. 0.5

e. -0.5

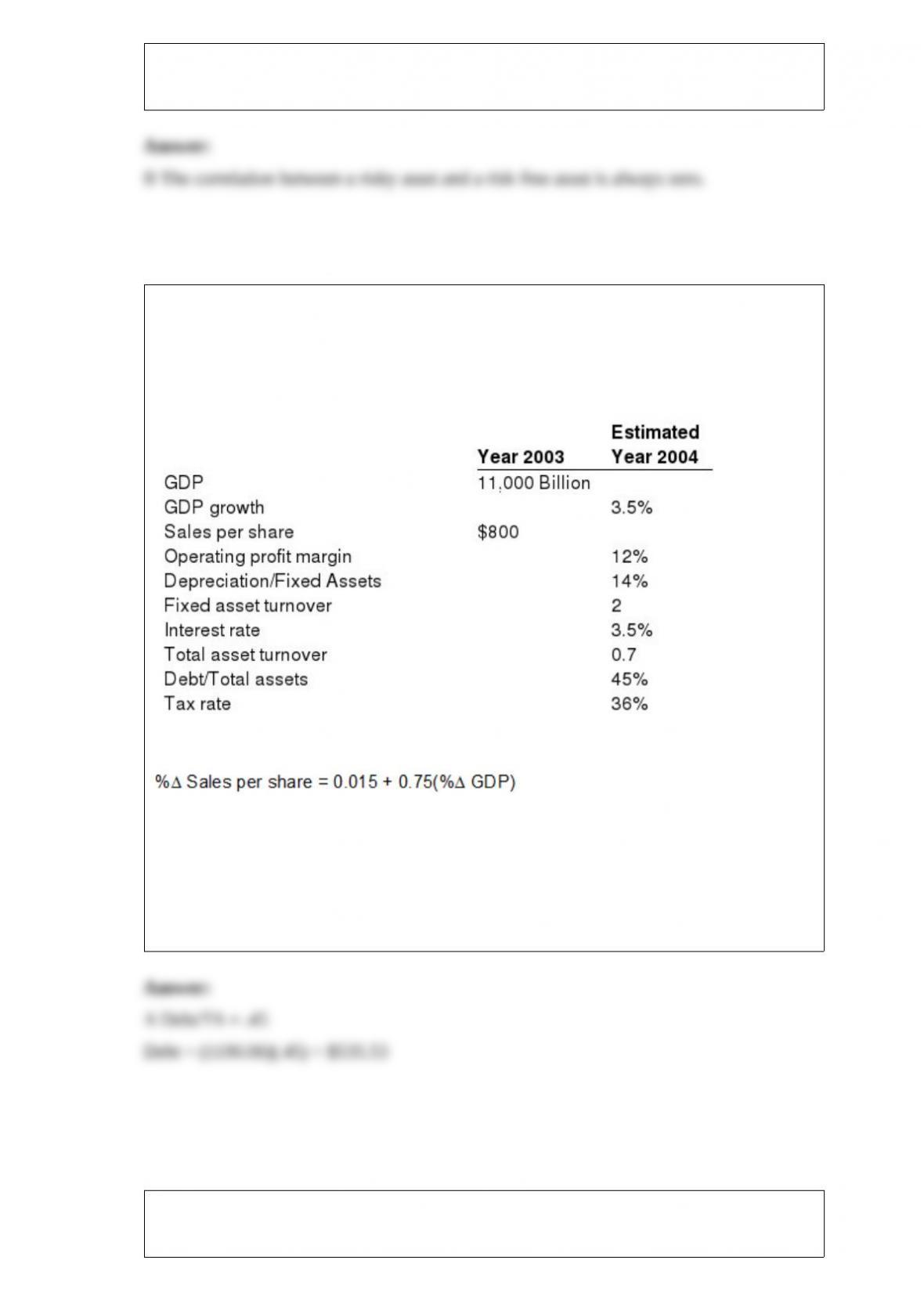

5) Exhibit 12.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information that you propose to use to obtain an estimate of

year 2004 EPS for the MacLog Company.

In addition a regression analysis indicates the following relationship between growth in

sales per share for MacLog and GDP growth is

Calculate the firm’s level of debt for the year 2004.

a. $535.53

b. $600.75

c. $637.67

d. $485.98

e. $393.72

6) The strongest explanations for the size anomaly are

a.risk measurements

b.higher transaction costs

c.P/E ratio

d.a and b.

e.b and c.

7) Given Birdchip’s beta of 1.25 and a risk free rate of 6 percent, what is the expected

rate of return assuming a 12 percent market return?

a. 1%

b. 10%

c. 11%

d. 12%

e. 31%

8) Which of the following is not a stage in the industrial life cycle?

a. Early pioneering development

b. Rapid accelerating growth

c. Acquisition and consolidation

d. Mature growth

e. Stabilization and market maturity

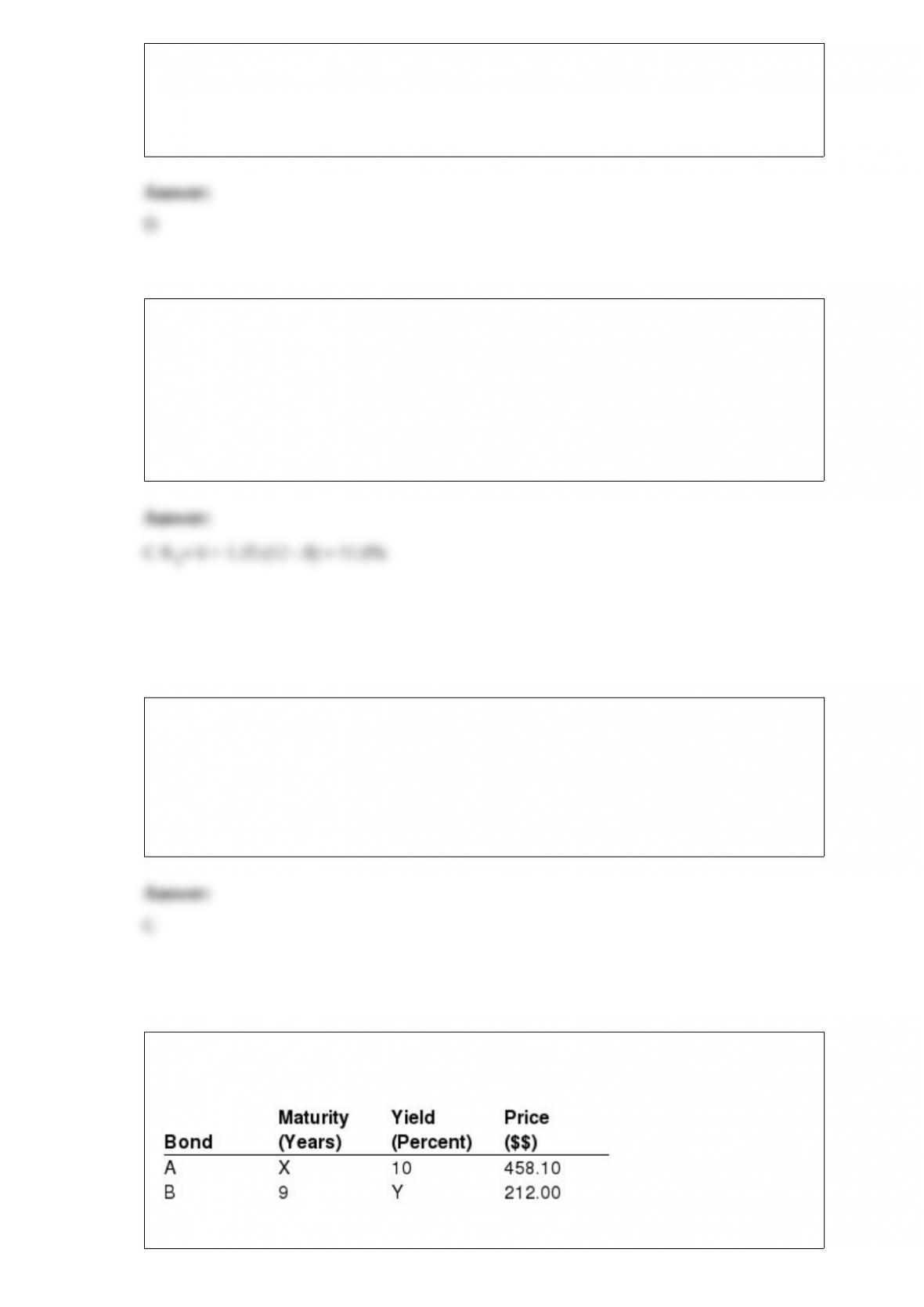

9) For bonds A and B below find the values of X and Y assuming each is a zero coupon

bond with a $1,000 face value (semiannual compounding).

a. 8 years and 4 percent

b. 10 years and 8 percent

c. 12 years and 10 percent

d. 14 years and 12 percent

e. 8 years and 18 percent

10) Which of the following is an approach to asset management?

a. Management and advisory firms

b. Investment companies

c. Strategic management

d. Choices a and b only

e. All of the above

11) A major question in modern finance regarding closed-end investment companies is

a. Why do these funds sell at discounts?

b. Why do the discounts differ between funds?

c. What are the returns available to investors from funds that sell at a large discount?

d. Choices a and b only

e. All of the above

12) Which of the following economic series are included in the NBER leading indicator

group?

a. Average weekly hour of production workers.

b. Average weekly initial claims for unemployment insurance.

c. Index of bond prices.

d. a and b.

e. b and c.

13) Expected earnings per share estimates requires all of the following except

a. A sales per share estimate.

b. A GDP estimate.

c. An aggregate operating profit margin estimate

d. An estimate of the real risk-free rate.

e. A tax rate estimate.

14) A major source of risk faced by GNMA issues is

a. Default risk.

b. Prepayment risk.

c. Counterparty risk.

d. a and b.

e. a, b and c.

15) Exhibit 13.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The Home Appliance Industry had free cash flow to equity (FCFE) of $87 for the most

recent year ending reported yesterday. The industry anticipates a growth rate of 8% for

the next three years due to favorable economic conditions. However, the growth rate is

expected to decline to 4% after three years and remain at that level indefinitely. The

required rate of return is 12% for this industry.

Calculate the intrinsic value of the Home Appliance Industry at the end of the 8%

growth period three years from now.

a. $109.59

b. $113.98

c. $949.83

d. $1,369.94

e. $1,424.73

16) In an investment policy statement the objectives of an investor are expressed in

terms of

a.risk and return

b.risk

c.return

d.time horizon

e.liquidity needs

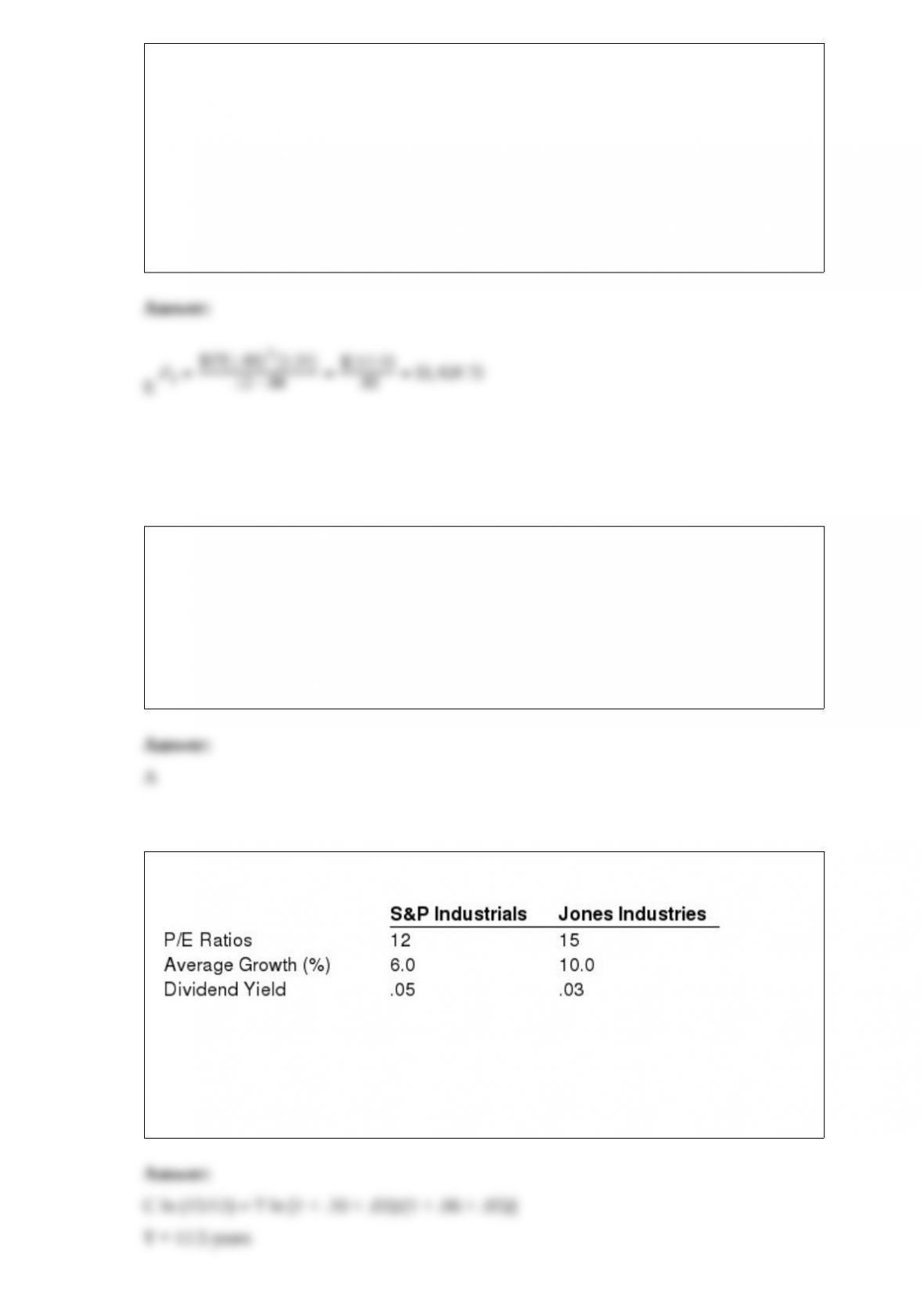

17) What is the implied growth duration of Jones Industries given the following:

a. 7.2 years

b. 10.9 years

c. 12.5 years

d. 13.9 years

e. 15.2 years

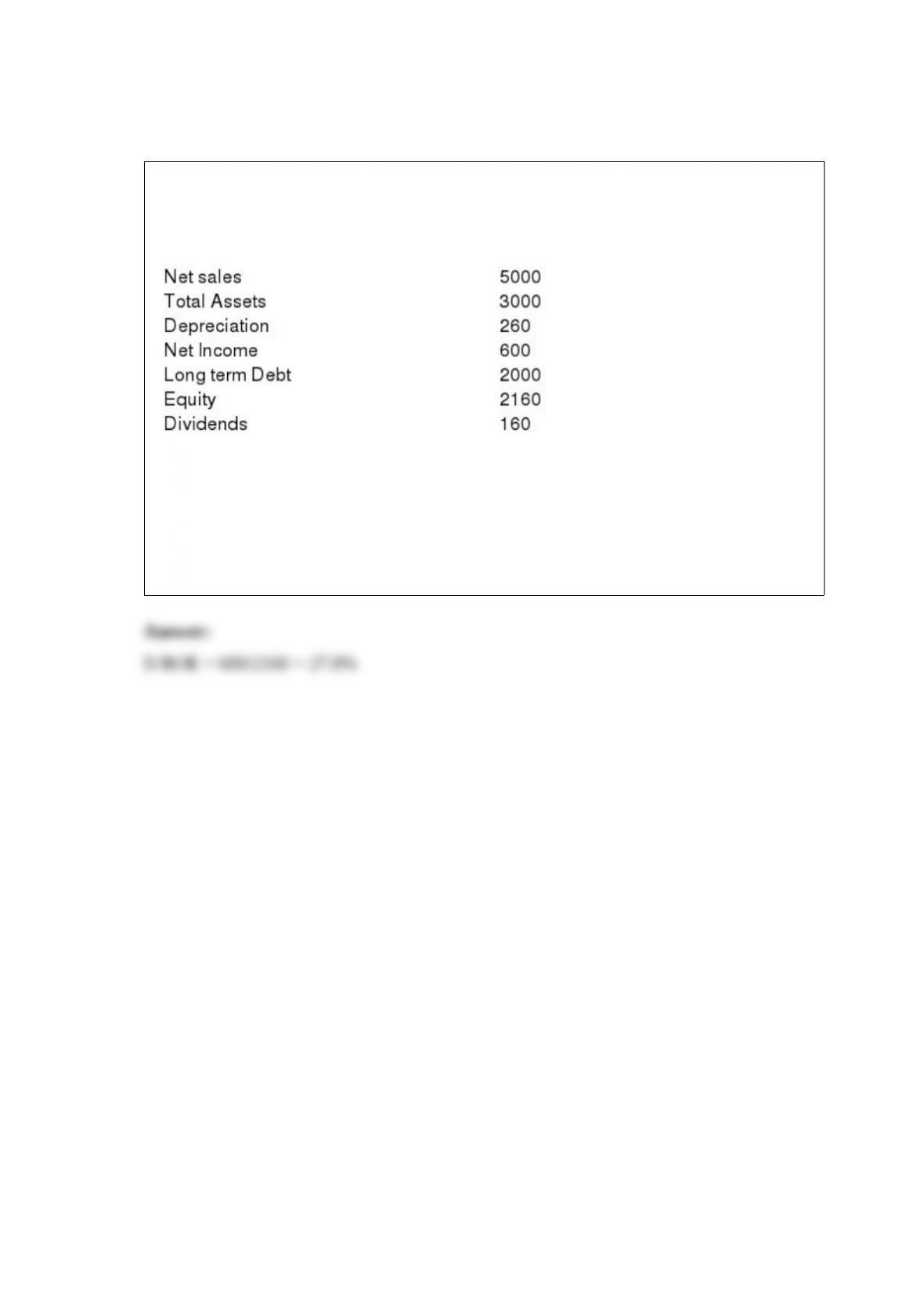

18) Exhibit 10.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

You are provided with the following information about MaxCorp.

Calculate the return on equity (ROE).

a. 20.4%

b. 17.8%

c. 22.4%

d. 27.8%

e. 30.4%