Interest revenue from notes receivable is typically reported on a multiple step income

statement as a part of Income from Operations.

Because it is easier to use, the direct write-off method for uncollectible accounts is

typically used instead of the allowance method.

When expenses exceed revenues in a period, stockholders’ equity will increase.

FOB shipping point means that ownership of goods passes to the buyer when the goods

reach the buyer.

Generally Accepted Accounting Principles (GAAP) require profitable companies to

distribute some of their earnings to their stockholders.

Revenue is reported on the income statement only if cash was received at the point of

sale.

The Securities and Exchange Commission (SEC) is the government agency that has

primary responsibility for setting accounting standards in the U.S.

Notes receivable are typically only used when a company sells large dollar value items

(such as cars).

If a company produces the same number of units per period over an asset’s useful life,

each period’s depreciation expense using the straight-line method will be the same as

that recorded using the units-of-production method.

Journal entries show the effects of transactions on the elements of the accounting

equation, as well as the account balances.

In the United States, generally accepted accounting principles (GAAP) are established

by the PCAOB (Public Company Accounting Oversight Board).

An asset is purchased on January 1 for $40,000. It is expected to have a useful life of

five years after which it will have an expected residual value of $5,000. The company

uses the straight-line method. If it is sold for $30,000 exactly two years after it is

purchased, the company will record a:

A) gain of $6,000.

B) gain of $4,000.

C) loss of $4,000.

D) loss of $6,000.

Which of the following statements regarding goodwill is not correct?

A) Goodwill is not amortized.

B) Goodwill is tested annually for impairment.

C) Goodwill is written down if its value is found to be impaired.

D) Private companies amortize goodwill using the straight-line method over 20 years or

less.

A current asset is one that the company:

A) has owned for over one year.

B) has owned for over five years.

C) will use up or converted into cash in less than 12 months.

D) has updated to reflect its current value.

What journal entry must be prepared when the company is notified by the bank that a

customer’s check that had been deposited in the amount of $776 was returned NSF?

A) Debit Accounts Receivable and credit Cash in the amount of $776

B) Debit Cash and credit Accounts Receivable in the amount of $776

C) Debit NSF Check Expense and credit Accounts Receivable in the amount of $776

D) No journal entry is necessary.

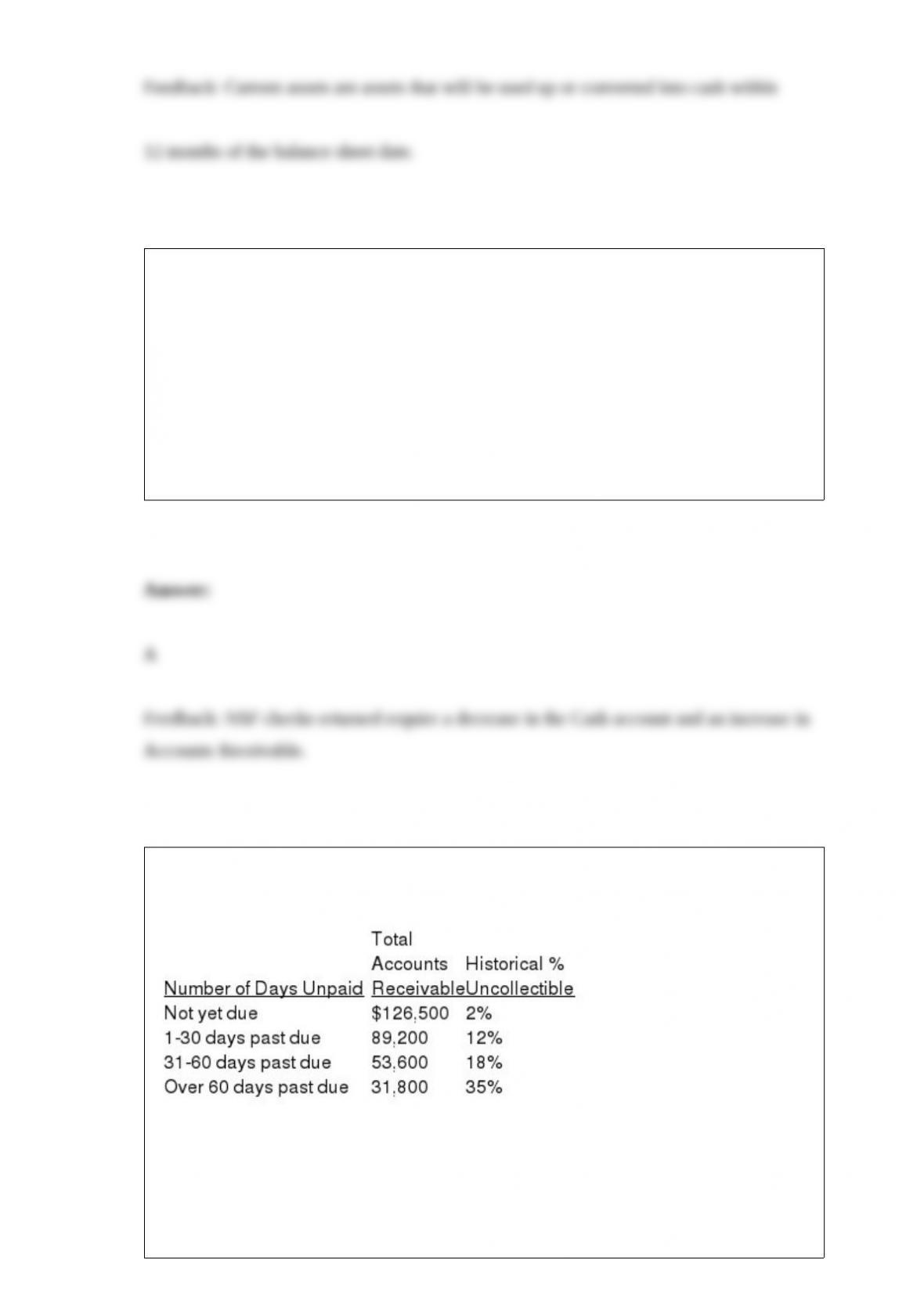

The following summarizes the aging of accounts receivable for Johnston Supplies, Inc.

as of July 31, 2016:

Required:

Part a. The unadjusted balance of the Allowance for Doubtful Accounts of Johnston

Supplies, Inc. is a credit balance in the amount of $28,947 on July 31, 2016. Prepare the

required adjusting entry to record Bad Debt Expense for the year.

Part b. Johnston Supplies, Inc. writes off $3,081 of uncollectible accounts during on

August 15, 2016. Prepare the required adjusting entry to record the write-off.

Part c. Use a T-account to determine the account balance in the Allowance for Doubtful

Accounts on August 15, 2016.

Match the term and its definition. There are more definitions than terms.

Terms

____ 1) Net Realizable Value

____ 2) Percentage of Credit Sales Method

____ 3) Allowance for Doubtful Accounts

____ 4) Principal

____ 5) Write-Off

____ 6) Aging of Accounts Receivable

____ 7) Credit Terms

____ 8) Factoring

Definitions

A. How much money you can expect to earn over a period of time selling your goods.

B. The length of the credit period and any discounts offered for prompt payment.

C. A method of estimating uncollectible debts by forecasting the probability of not

collecting late accounts.

D. Selling accounts receivable to another company for immediate cash.

E. The account in which the estimated amount of accounts receivable expected to be

uncollectible is recorded.

F. Also known as net accounts receivable.

G. A method of estimating uncollectible debts by looking at the historical average of

credit sales not collected.

H. The amount of money lent.

I. Credit that a company receives when one good is exchanged for another.

J. The interest earned by money over a period of time.

K. When a company increases the amount of accounts receivable by adding the interest

earned as accounts age without being collected.

L. The process of removing specific customers’ accounts deemed uncollectible.

The gross profit equation is:

A) (Sales Revenue + Sales Returns & Allowances) – Cost of Goods Sold

B) (Sales + Sales Discounts) – Cost of Goods Sold

C) (Sales Revenue – Sales Returns & Allowances – Sales Discounts) – Cost of Goods

Sold

D) (Sales Revenue – Sales Returns & Allowances – Sales Discounts) + Cost of Goods

Sold

If inventory is updated periodically, which of the equations is correct?

A) Cost of goods sold = Beginning inventory + Purchases – Ending inventory

B) Cost of goods sold = Beginning inventory + Purchases + Ending inventory

C) Beginning inventory + Purchases = Ending inventory

D) Ending inventory = Beginning inventory + Purchases + Cost of goods sold.

At the beginning of the year, your company borrows $20,000 by signing a four-year

promissory note that states an annual interest rate of 8% plus principal repayments of

$5,000 each year. Interest is paid at the end of the second and fourth quarters, whereas

principal payments are due at the end of each year. How does this new promissory note

affect the current and non-current liability amounts reported on the classified balance

sheet prepared at the end of the first quarter?

A) Increase current liabilities by $400; increase non-current liabilities by $20,000

B) Increase current liabilities by $1,600; increase non-current liabilities by $20,000

C) Increase current liabilities by $5,400; increase non-current liabilities by $20,000

D) Increase current liabilities by $5,400; increase non-current liabilities by $15,000

Thompson Company had beginning inventory of $6,000, cost of goods sold of $14,000,

and ending inventory of $8,000. Purchases were:

A) $12,000.

B) $10,000.

C) $9,000.

D) $16,000.

If the total amount that should have been debited to Insurance Expense is mistakenly

debited instead to Prepaid Insurance, what will be the effect on the financial statements

for the year?

A) Revenues will be overstated.

B) Assets will be overstated.

C) Stockholders’ equity will be understated.

D) Expenses will be overstated.

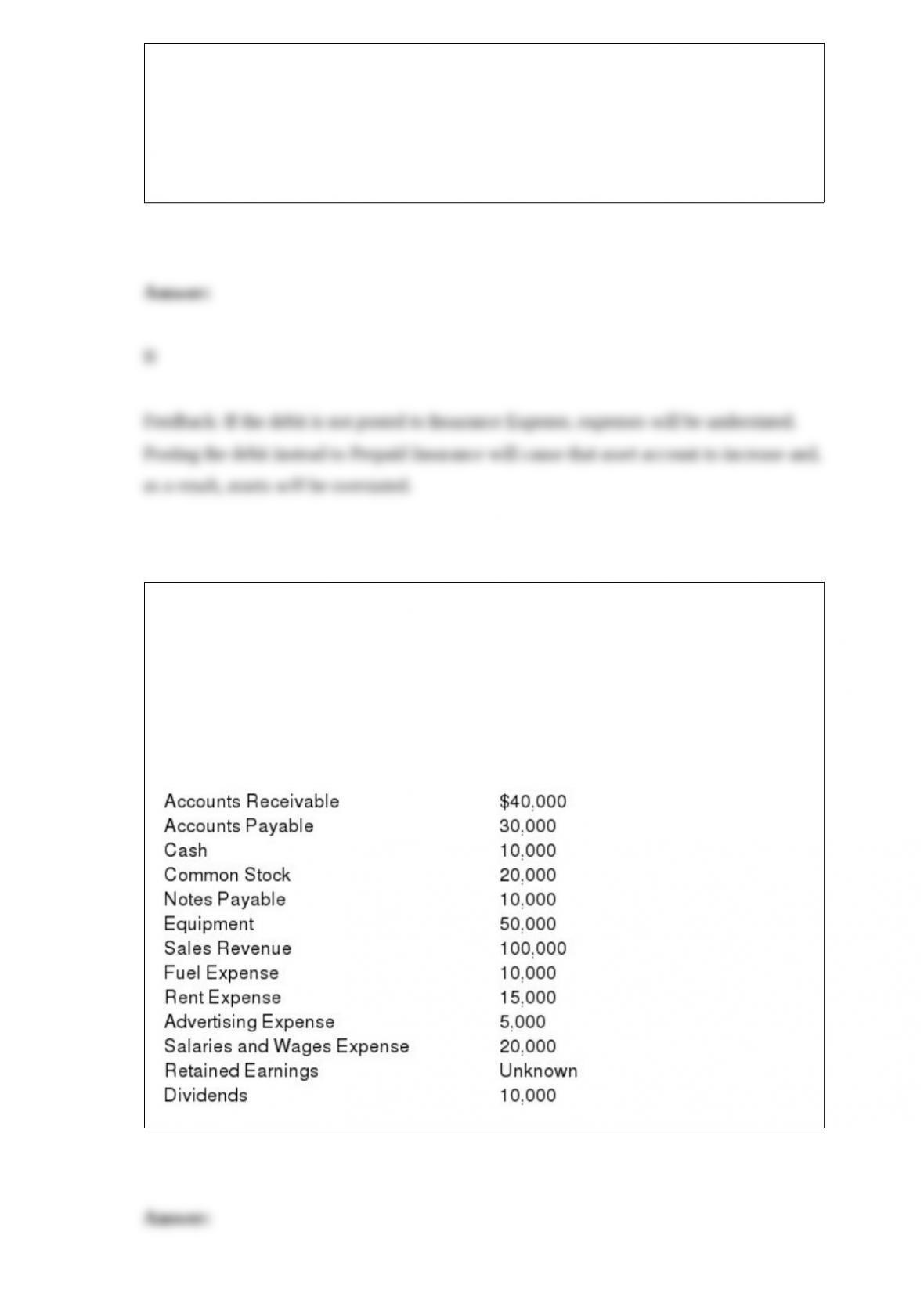

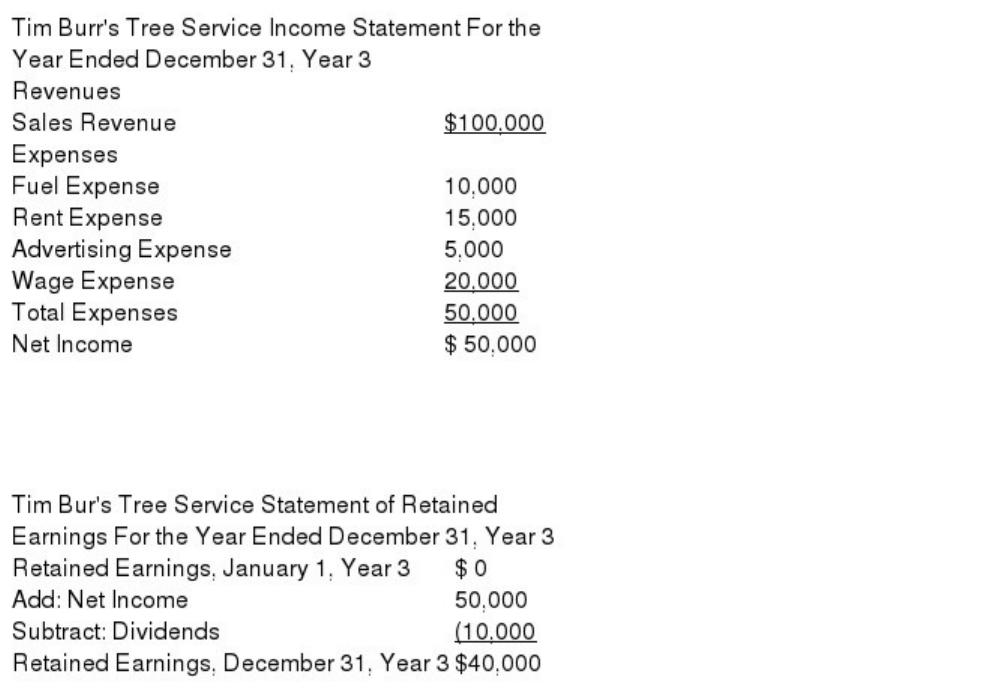

Following is a list of financial statement items and amounts for Tim Burr’s Tree Service

as of 12/31/X3, the end of its first year in operation.

Required:

Use this information to prepare the Income Statement, Statement of Retained Earnings,

and Balance Sheet.

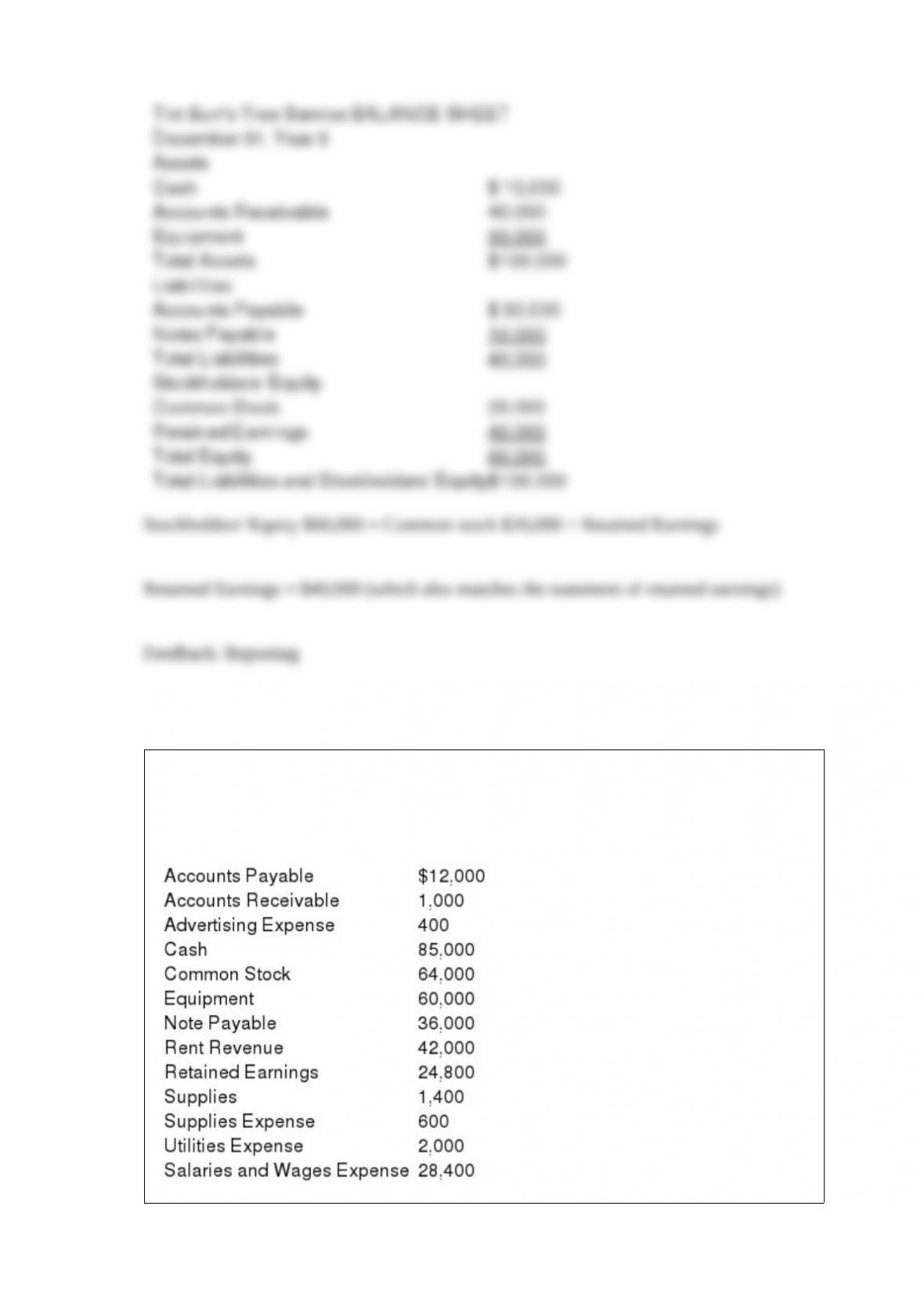

At September 30, Balance Corporation reported the following unadjusted amounts for

its accounts, each of which is considered to be a normal account balance. Prepare an

unadjusted trial balance.

Bluebell Company sells blue jeans. Last year, bell-bottom jeans were fashionable; this

year, boot cut jeans are in style. The company has 375 units of bell-bottom jeans with a

cost of $17 per unit and a market value of $15 per unit. The inventory also includes

1,000 units of boot cut jeans with a cost of $16 per unit and a market value of $19 per

unit.

Required:

Part a – Explain whether this situation requires an adjustment to the accounting records.

Part b – Prepare the journal entry, if any, that is required to adjust the Inventory account.

On April 1, a company established a petty cash fund of $1,000.

Required:

Prepare the journal entry, if any, required on April 1.

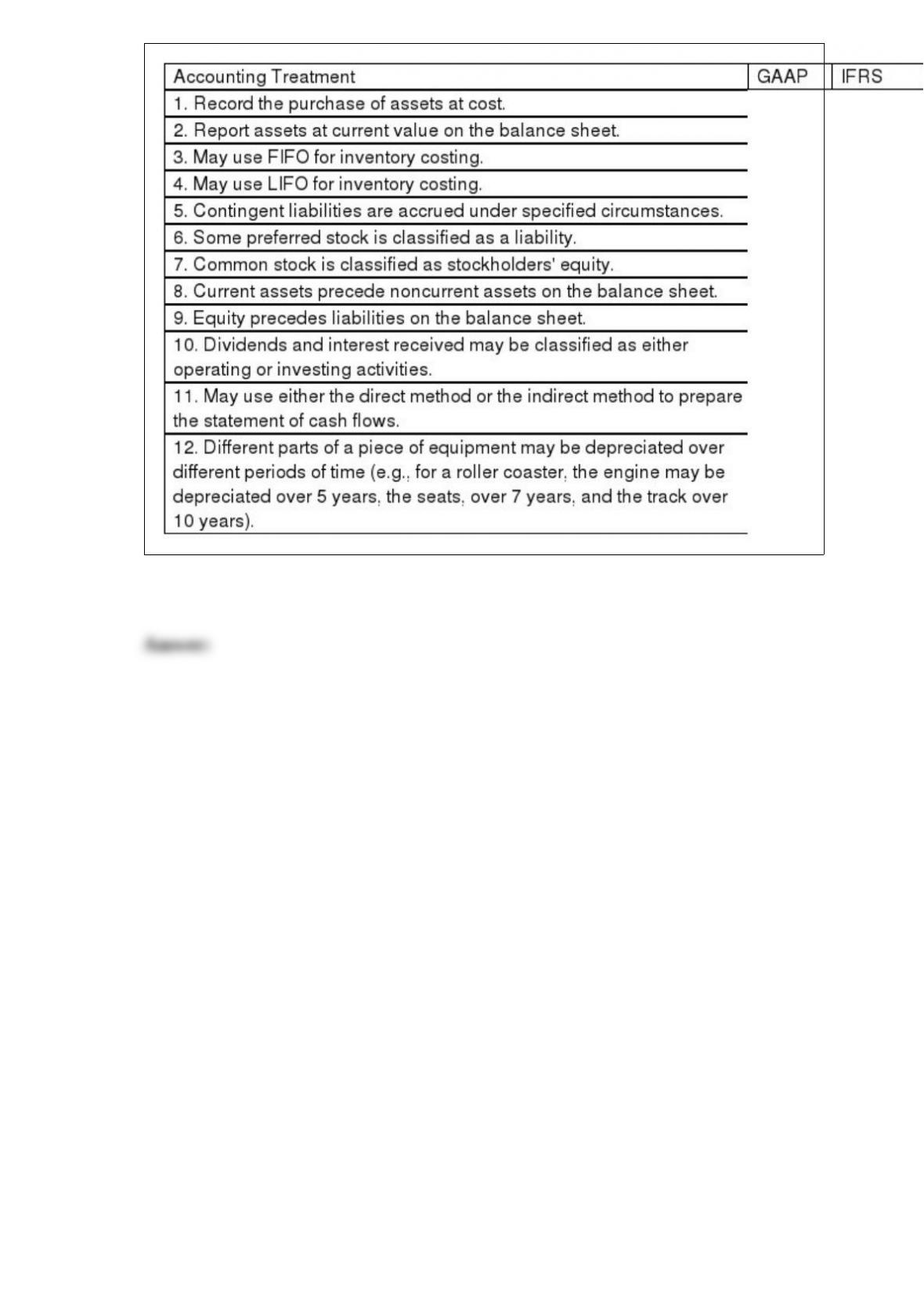

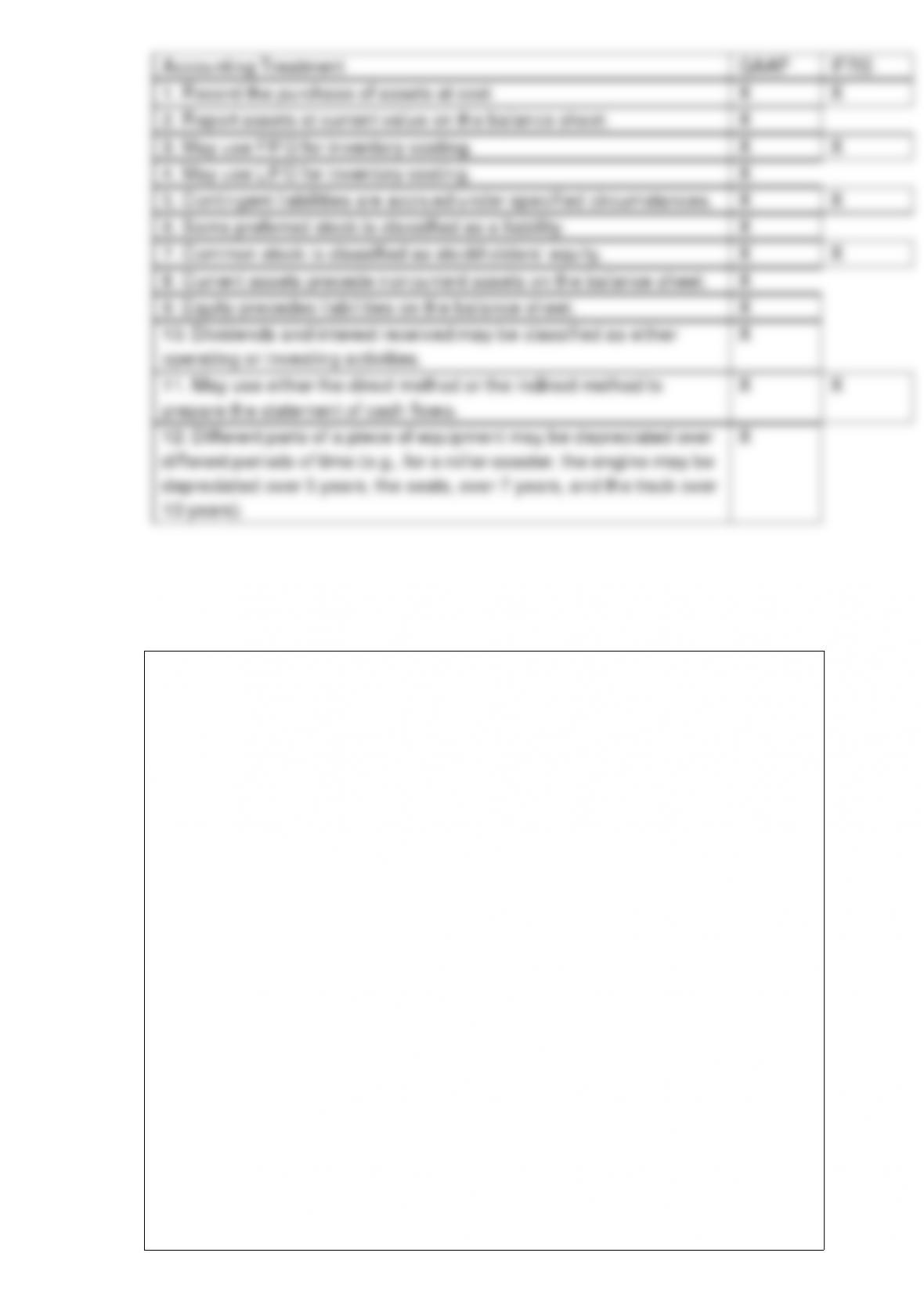

For each of the accounting treatments below, indicate whether it is followed in GAAP,

or IFRS, or both, by placing an “X” in the appropriate column(s).

Choose the letter of the appropriate category to match each asset described.

Asset

1) ______ Warehouse

2) ______ Licensing rights

3) ______ Supplies

4) ______ Patents

5) ______ Production equipment

6) ______ Goodwill

7) ______ Land

8) ______ Office computer

Category

T – Tangible long-lived asset

I – Intangible long-lived asset

N – Not a long-lived asset