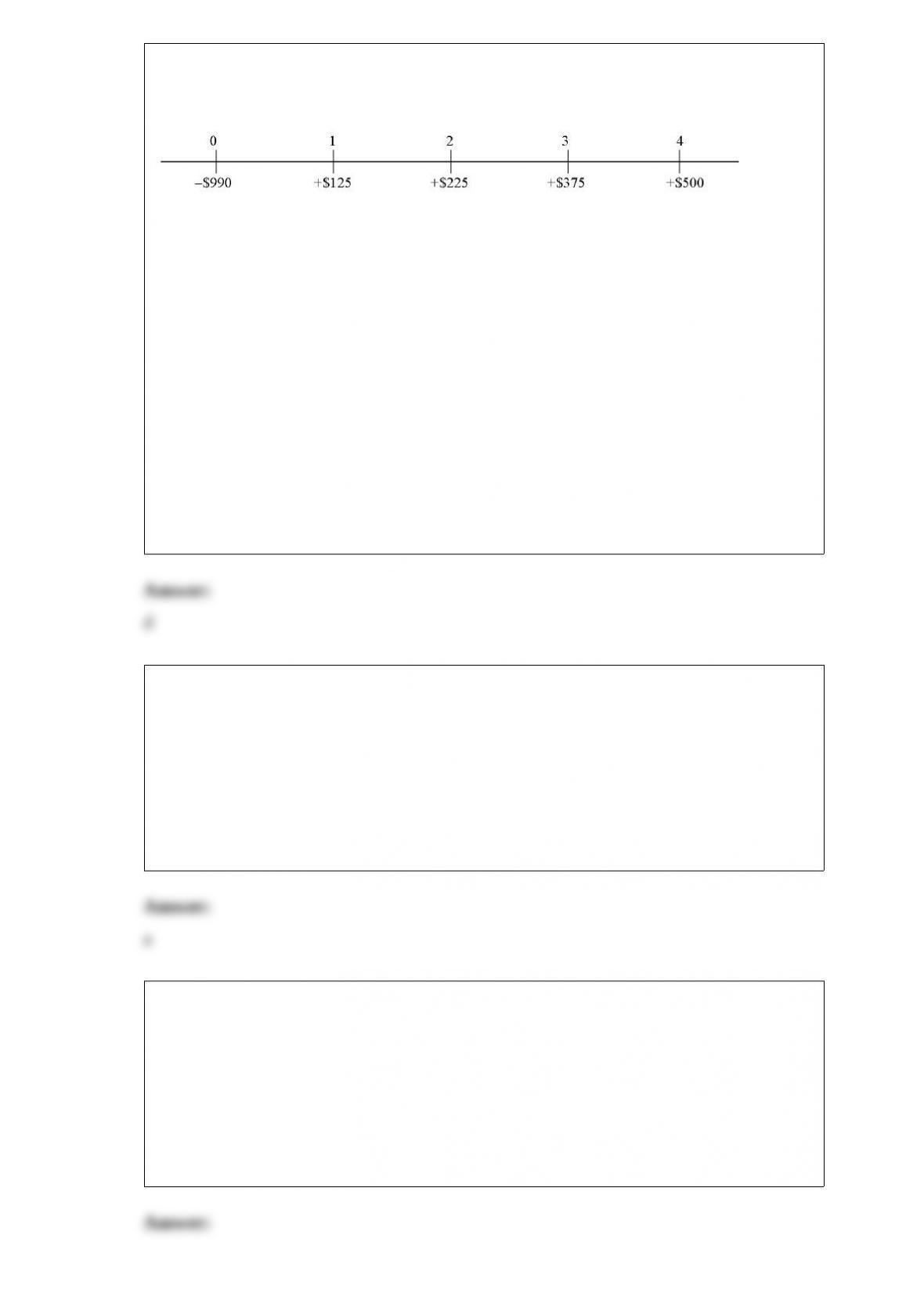

1) consider a project of the cornell haul moving company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

the firm’s tax rate is 34%; the firm’s bonds trade with a yield to maturity of 8%; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity,

the required return would be 10%

using the apv method, what is the value of this project to an all-equity firm?

a.-$46,502,288.10

b.$12,494,643.75

c.$36,580,767.55

d.-$67,163,445.12

e.$59,459,301.03

2) the majority of foreign vertical integration is

a.backward

b.forward

c.sideways

d.none of the above

3) the british version of the eximbank

a.helps u.s. exporters develop and expand their overseas sales

b.is called inland revenue

c.is called the exports credits guarantee department

d.is called eximbank u.k

4) while debt can reduce agency costs between shareholders and management,

a.excessive debt may also induce the risk-averse managers to forgo profitable but risky

investment projects, causing an underinvestment problem

b.with debt financing companies can misuse debt to finance corporate empire building

c.both a and b

d.none of the above

5) which is growing at a faster rate, foreign direct investment by mncs or international

trade?

a.fdi by mncs

b.international trade

c.since they are linked, they grow at the same rate.

d.none of the above

6) if a dollar earned by a foreign affiliate is taxed under the same rules as a dollar

earned by a domestic affiliate of the mnc, then we have achieved

a.capital-export neutrality

b.capital-import neutrality

c.national neutrality

d.tax equity

7) financial accounting standards board (fasb) statements 8 and 52 relate to the

translation methods. the following outlines the objectives and descriptions of the two

statements.

(i) – measure in dollars an enterprise’s assets, liabilities, revenues, or expenses that are

denominated in a foreign currency according to generally accepted accounting

principles

(ii) – is essentially the temporal method of translation (with some subtle differences)

(iii) – provide information that is generally compatible with the expected economic

effects of a rate change on an enterprise’s cash flows and equity

(iv) – reflect in consolidated statements the financial results and relationships of the

individual consolidated entities as measured in their functional currencies in conformity

with u.s. generally accepted accounting principles

the “functional currency” is defined in fasb 52 as

a.the currency of the primary economic environment in which the entity operates

b.the currency in which the mnc prepares its consolidated financial statements

c.a currency that is not the parent firm’s home country currency

d.both b and c

8) generally speaking, when both a firm’s costs and its price is sensitive to exchange

rate changes

a.the firm is not subject to high degrees of operating exposure

b.the firm is subject to high degrees of operating exposure

c.the firm should hedge

d.none of the above

9) a translation exposure report shows, for each account that is included in the

consolidated balance sheet,

a.the amount of foreign exchange exposure that exists for each foreign subsidiary in

which the mnc has a material interest

b.the amount of foreign exchange exposure that exists on a net basis for the firm

c.the amount of foreign exchange exposure that exists for each foreign currency in

which the mnc has exposure

d.none of the above

10) goldman sachs estimates that as much as __% of the pretax profits that porsche

reported for a recent fiscal year came from skillfully executing currency options.

a.5

b.10

c.15

d.75

11) a foreign branch is

a.an extension of the parent and is not an independently incorporated firm separate from

the parent

b.an affiliate organization of the mnc that is independently incorporated in the foreign

country, and one in which the u.s. mnc owns at least 10 percent of the voting equity

stock

c.either a minority foreign subsidiary (an uncontrolled foreign corporation) or a

controlled foreign corporation

d.both b and c

12) english common law countries tend to provide a stronger protection of shareholder

rights than french civil law countries because

a.the former countries tend to be more democratic than the latter

b.the former countries tend to protect property rights better than the latter

c.the former countries tend to have more separation of power than the latter

d.all of the above

13) for european currency options written on euro with a strike price in dollars, what of

the effect of an increase in r$?

a.decrease the value of calls and puts ceteris paribus

b.increase the value of calls and puts ceteris paribus

c.decrease the value of calls, increase the value of puts ceteris paribus

d.increase the value of calls, decrease the value of puts ceteris paribus

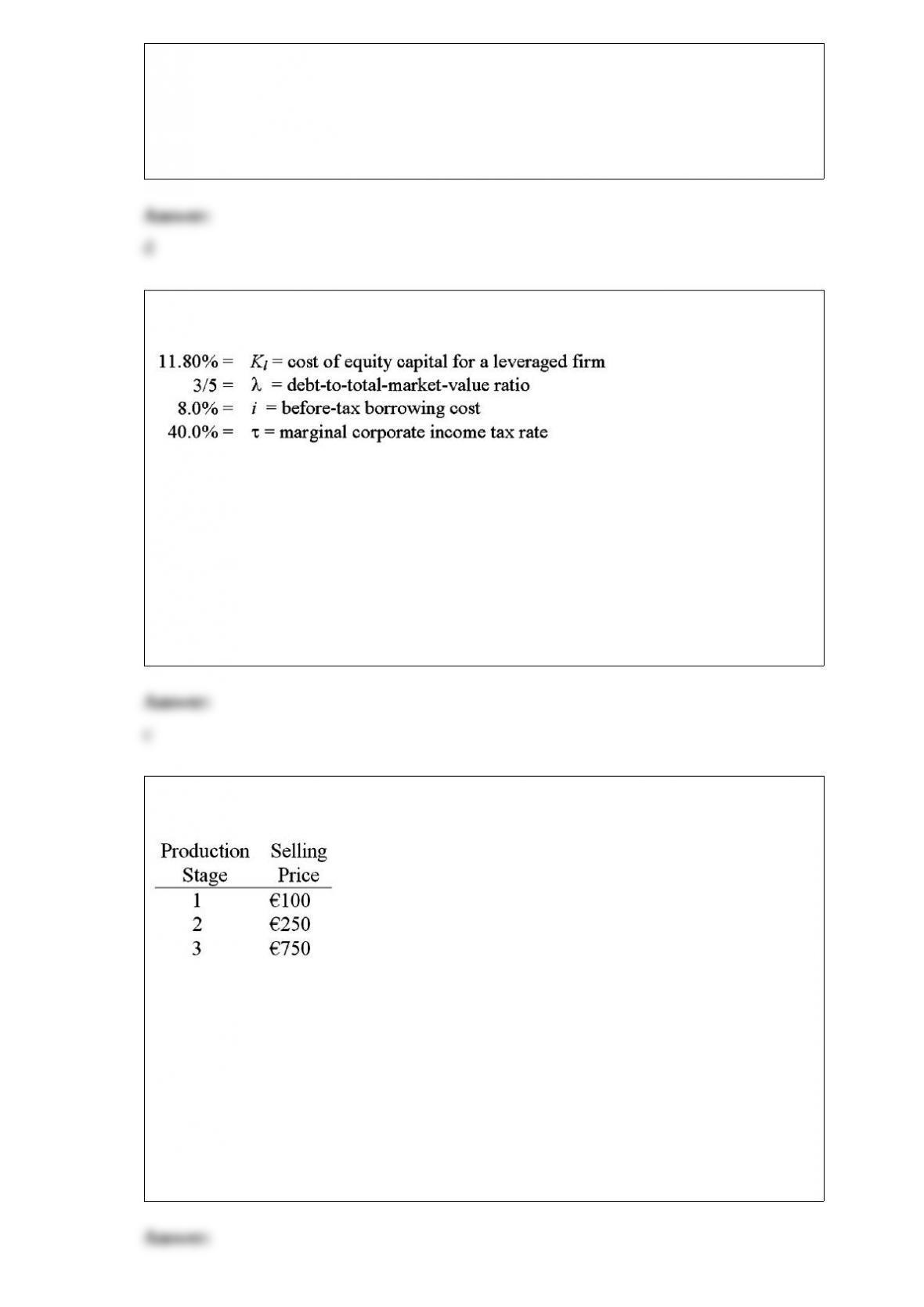

14) solve for the weighted average cost of capital:

a.8.67%

b.8.00%

c.7.60%

d.7.33%

e.7.14%

15) assume that a product has the following three stages of production:

if the value-added tax (vat) rate is 25%, what would be the vat over all stages of

production?

a.187.50

b.120

c.150

d.225

16) why is it rational to make shareholders “weak” by giving control to the managers of

the firm?

a.this may be rational when shareholders may be neither qualified nor interested in

making business decisions

b.this may be rational since many shareholders find it easier to sell their shares in an

underperforming firm than to monitor the management

c.this may be rational to the extent that managers are answerable to the board of

directors

d.all of the above are explanations for the separation of ownership and control

17) in the context of the capital budgeting analysis of an mnc that has strong foreign

competitors, “lost sales” refers to

a.the cannibalization of existing projects by new projects

b.the entire sales revenue of a new foreign manufacturing facility representing the

incremental sales revenue of the new project

c.both a and b

d.none of the above