Market share is usually easy to define. True or False

Answer:

The adjusted present value method values firm without debt and then subtracts the

value of future tax savings resulting from the tax-deductibility of interest. True or False

Answer:

Environmental laws in the European Union are generally more restrictive than in the

U.S. True or False

Answer:

Highly decentralized organizational structures generally expedite the integration effort

more so than highly centralized structures. True or False

Answer:

Market-based valuation methods are less prone to manipulation than discounted cash

flow methods because they require a more detailed statement of assumptions. True or

False

Answer:

Purchase accounting affects only the cash flow of the combined firms but not the

reported net income. True or False

Answer:

Holding companies can gain effective control of other companies by owning

significantly less than 100% of their outstanding voting stock. True or False

Answer:

Horizontal mergers are rarely rejected by antitrust regulators. True or False

Answer:

There is widespread agreement over the magnitude of the liquidity discount. True or

False

Answer:

A business plan articulates a mission or vision for the firm and a strategy for realizing

that mission. True or False

Answer:

The enterprise or free cash flow to the firm approach to valuation discounts the after-tax

free cash flow available to the firm from operations at the weighted average cost of

capital to obtain the enterprise value. True or False

Answer:

A sudden improvement in operating profits in the year in which the business is being

offered for sale may suggest that both revenue and expenses had been overstated during

the historical period.

True or False

Answer:

Asset sales by the target firm just prior to the transaction may threaten the tax-free

status of the deal. Moreover, tax-free deals are disallowed within ten-years of a spin-off.

True or False

Answer:

Managers and owners in public companies are likely to have the same emotional

attachment to their businesses as those in private firms. True or False

Answer:

Mergers and acquisitions rarely pay off for target firm shareholders, but they are usually

beneficial to acquiring firm shareholders. True or False

Answer:

Type A reorganizations are generally viewed as the least flexible of the various types of

tax-free reorganizations. True or False

Answer:

Stock purchases involve the exchange of the target’s stock for cash, debt, stock of the

acquiring company, or some combination. True or False

Answer:

If the tangible book value of a firm significantly exceeds its market value for an

extended period of time, it can become an attractive takeover target. True or False

Answer:

Form of payment refers only to the acquirer’s common stock used to make up the

purchase price paid to target shareholders. True or False

Answer:

In applying the adjusted present value method, the present value of a highly leveraged

transaction should reflect the present value of the firm without leverage plus the present

value of tax savings plus the present value of expected financial distress. True or False

Answer:

Confidentiality agreements are usually signed before any information is exchanged to

protect the buyer and the seller from loss of competitive information. True or False

Answer:

The acquisition vehiclerefers to the legal structure created to acquire the target

company. True or False

Answer:

Improper revenue recognition is the most common form of financial reporting fraud.

True or False

Answer:

Tangible book value is the value of shareholders’ equity less net fixed assets. True or

False

Answer:

Investors in segmented markets will bear a lower level of risk by holding a

disproportionately large share of their investments in their local market as opposed to

the level of risk if they invested in a globally diversified portfolio. True or False

Answer:

The availability and reliability of data for public companies tends to be much greater

than for small private firms. True or False

Answer:

Unlike a limited partnership, the LLC is taxed on all profits before they are paid out to

its members. True or False

Answer:

The current stock price of the acquiring firm may decline, reflecting a potential dilution

of its EPS or a growth in EPS of the combined firms, which is less than the growth that

investors had anticipated for the acquirer as a standalone business. True or False

Answer:

Business alliances may represent attractive alternatives to mergers and acquisitions.

True or False

Answer:

The acquired company should be fully integrated into the acquiring company if an

earn-out is used to consummate the transaction. True or False

Answer:

Operational restructuring refers to the outright or partial sale of companies or product

lines or to downsizing by closing unprofitable or non-strategic facilities. True or False

Answer:

The most important calculation to the financial sponsor in an LBO analysis is the IRR.

True or False

Answer:

In the absence of a voluntary settlement out of court, the debtor firm may seek

protection from its creditors by initiating bankruptcy. However, creditors cannot force

the debtor firm into bankruptcy. True or False

.

Answer:

Firms with significant expertise, brands, patents, copyrights, and proprietary

technologies seek to grow by exploiting these advantages in emerging markets. True or

False

Answer:

The total purchase price paid by the buyer should also reflect the assumption of

liabilities stated on the target’s balance sheet, but it should exclude all off balance sheet

liabilities. True or False

Answer:

The tax status of the transaction may influence the purchase price by

a. Raising the price demanded by the seller to offset potential tax liabilities

b. Reducing the price demanded by the seller to offset potential tax liabilities

c. Causing the buyer to lower the purchase price if the transaction is taxable to the

target firm’s shareholders

d. Forcing the seller to agree to defer a portion of the purchase price

e. Forcing the buyer to agree to defer a portion of the purchase price

Answer:

A diversified automotive parts supplier has decided to sell its valve manufacturing

business. This sale is referred to as a

a. Merger

b. Divestiture

c. Spin-off

d. Equity carveout

e. Liquidation

Answer:

Which other types of legislation can have a significant impact on a proposed

transaction?

a. State anti-takeover laws

b. State antitrust laws

c. Federal benefits laws

d. Federal and state environmental laws

e. All of the above

Answer:

Conoco Phillips Buys a Stake in Russian Oil Giant Lukoil

In late 2004, Conoco Phillips (Conoco) announced the purchase of 7.6 percent of

Lukoil’s (a largely government owned Russian oil and gas company) stock for $2.36

billion during a government auction of Lukoil’s stock. The deal gives Conoco access to

Russia’s huge, but largely undeveloped, oil and natural gas reserves. Conoco intends to

boost its investment to 10 percent by yearend and to 20 percent within two-to-three

years. To help ensure that Conoco’s interests are protected, even though it has only a

minority position, Conoco will have one seat on Lukoil’s board and Lukoil changed its

corporate charter to require unanimous board approval for the most important decisions

such as payment of dividends and major new investments. Conoco will gain one

additional seat once its ownership share climbs to 20 percent. Conoco has also agreed to

pay $370 million to Lukoil for a 30 percent stake in a joint venture to develop reserves

in northern Russia. The two firms will split operational responsibilities equally.

Conoco’s stock fell more than 1 percent immediately following the announcement.

Discussion Questions:

1) Describe the operational and managerial challenges facing the two partners.

2) Do you believe that Conoco gained an effective say in Lukoil’s operations following

its investment? Explain your answer.

3) Why do you believe Conoco’s stock fell immediately following the announcement?

Answer:

Which of the following represent common international market entry strategies?

a. Mergers and acquisitions

b. Licensing

c. Exporting

d. Greenfield or solo ventures

e. All of the above

Answer:

The Bankruptcy Abuse Prevention and Creditor Protection Act of 2005 is intended to

achieve all of the following except:

a. To reduce the maximum length of time debtors have to submit a reorganization plan

b. To give debtors more time to accept or reject leases

c. To limit key employee compensation

d. To enable the debtor to extend the lease indefinitely as long as lease payments are

made on a timely basis

e. B and D only

Answer:

Which of the following is not true about generally accepted accounting principles

(GAAP)?

a. GAAP provide specific guidelines as to how to account for specific events impacting

the financial performance of the firm.

b. The scrupulous application GAAP accounting rules does ensure consistency in

comparing one firm’s financial performance to another.

c. It is customary for definitive agreements of purchase and sale to require that a target

company represent that its financial books are kept in accordance with GAAP.

d. GAAP guarantees that a firm’s financial books are accurate.

e. Differences between how a firm records actual financial transactions and how they

should be recorded based on GAAP may indicate fraud or mismanagement.

Answer:

The market governance model is applicable when which of the following conditions are

true?

a. Capital markets are liquid

b. Equity ownership is widely dispersed

c. Ownership and control are separate

d. Board members are largely independent

e. All of the above

Answer:

.

Deb Ltd. Seeks an Exit Strategy

In late 2004, Barclay’s Private Equity acquired slightly more than one half the equity in

Deb Ltd. (Deb), valued at about $250 million. The private equity arm of Britain’s

Barclay’s bank outbid other suitors in an auction to acquire a controlling interest in the

firm. PriceWaterhouseCooper had been hired by the Williamson family, the primary

stockholder in the firm, to find a buyer.

The sale solved a dilemma for Nick Williamson, the firm’s CEO and son of the founder,

who had invented the firm’s flagship product, Swarfega. The company had been

founded some 60 years earlier based on a single product, a car cleaning agent. Since

then, the Swarfega brand name had grown into a widely known brand associated with a

broad array of cleaning products.

In 1990, the elder Williamson wanted to retire and his son Nick, along with business

partner Roy Tillead, bought the business from his father. Since then, the business has

continued to grow, and product development has accelerated. The company developed

special Swarfega-dispensing cartridges that have applications in hospitals, clinics, and

other medical faculties.

After 13 years of sustained growth, Williamson realized that some difficult decisions

had to be made. He knew he did not have a natural successor to take over the company.

He no longer believed the firm could be managed successfully by the same

management team. It was now time to think seriously about succession planning. So in

early 2004, he began to seek a buyer for the business. He preferably wanted somebody

who could bring in new talents, ideas, and up-to-date management techniques to

continue the firm’s growth.

The terms of the agreement called for Williamson to work with a new senior

management team until Barclays decided to take the firm public. This was expected

some time during the five-to-seven year period following the sale. At that point,

Williamson would sell the remainder of his family’s stock in the business (Goodman,

2005).

Discussion Questions

1) Succession planning issues are often a reason for family-owned businesses to sell.

Why do you believe it may have been easier for Nick than his father to sell the business

to a non-family member?

2) What other alternatives could Nick have pursued? Discuss the advantages and

disadvantages of each.

3)What do you believe might be some of the unique challenges in valuing a

family-owned business? Be specific.

Answer:

Pixar and Disney Part Company

The announcement on February 5, 2004, of the end of the wildly successful partnership

between Walt Disney Company (“Disney”) and Pixar Animation Studios (“Pixar”)

rocked the investment and entertainment world. While the partnership continued until

the end of 2005, the split-up underscores the nature of the rifts that can develop in

business alliances of all types. The dissolution of the partnership ends a relationship in

existence since 1995 in which Disney produced and distributed the highly popular films

created by Pixar. Under the terms of the original partnership agreement, the two firms

cofinanced each film and split the profits evenly. Moreover, Disney received 12.5

percent of film revenues for distributing the films. Negotiations to renew the

partnership after 2005 foundered on Pixar’s desire to get a greater share of the

partnership’s profits. Disney CEO Michael Eisner refused to accept a significant

reduction in distribution fees and film royalties; while Steve Jobs, Pixar’s CEO,

criticized Disney’s creative capabilities and noted that marketing alone does not make a

poor film successful.

After 10 months of talks between Disney and Pixar, Disney rejected a deal that would

have required it to earn substantially less from future Pixar releases. Disney also would

have had to relinquish potentially lucrative copyrights to existing films such as Toy

Story and Finding Nemo. Disney shares immediately fell by almost 2 percent on the

news of the announcement, while Pixar’s shares skyrocketed almost 4 percent by the

end of the day. Pixar contributed more than 50 percent of Disney Studio’s operating

profits, and Disney Studios accounted for about one fourth of Disney’s total operating

profits. While Disney now faces Pixar as a competitor, it retains the rights to make

video and theatrical sequels and TV shows to the movies covered by the current

partnership agreement. However, while Disney does retain the right to make sequels to

Pixar films, it does not own the underlying technology and must recreate the millions of

lines of computer code for each character.

The key challenge for Disney will be to fill the creative vacuum left by the loss of Pixar

writers and animators. Disney is particularly vulnerable in that it has severely cut back

its own feature animation department and stumbled in recent years with a variety of box

office duds (e.g., Treasure Planet). Reflecting concern that Disney would not be able to

compete with Pixar, bond-rating service, Fitch Ratings suggested a possible downgrade

of Disney debt. Pixar announced that it was seeking another production studio.

Immediately following this announcement, Sony and others approached Pixar with

proposals to collaborate in making animated films.

Epilogue

In early 2006, Pixar agreed to be acquired by Disney.

Discussion Questions:

1) In your opinion, what were the motivations for forming the Disney-Pixar partnership

in 1995? Which partner do you believe had the greatest leverage in these negotiations?

Explain your answer.

2) What happened since 1995 that might have contributed to the break-up? (Hint:

Consider partner objectives, perceived relative contribution and in-house capabilities.)

3) How does the dissolution of the partnership leave Disney vulnerable? What could

Disney have done to protect itself from these vulnerabilities in the original

negotiations? (Hint: Consider scope of the agreement, management and control, dispute

resolution mechanisms, valuation of tangible and intangible assets, ownership of

partnership assets following dissolution, performance criteria)

4) What does the reaction of the stock market and credit rating agencies tell you about

how investors value the contribution of the two partners to the partnership? Do you

think investors may have over-reacted?

Answer:

Autos R Us and Pre-owned Inc represent used car dealers that compete in the same city.

These competitors each invest $15 million to form a new, jointly owned company, Real

Value Inc, that will sell cars in a nearby city. The new firm is best described by which of

the following terms:

a. Merger

b. Acquisition

c. Leveraged buyout

d. Joint venture

e. Consolidation

Answer:

Fair market value is

a. The cash or cash equivalent value that a willing buyer would pay or seller would

accept for a business

b. The cash or cash equivalent value that a willing buyer would pay or seller would

accept for a business, assuming each had access to all necessary information

c. The cash or cash equivalent value that a willing buyer would pay or seller would

accept for a business, assuming each had access to all necessary information and that

neither party is under duress.

d. The discounted value of free cash flow to the firm

e. The discounted value of free cash flow to equity investors.

Answer:

Which of the following are generally considered restructuring activities?

a. A merger

b. An acquisition

c. A divestiture

d. A consolidation

e. All of the above

Answer:

Studies show that which of the following combinations of corporate defenses can be

most effective in discouraging

hostile takeovers?

a. Poison pills and staggered boards

b. Poison pills and golden parachutes

c. Golden parachutes and staggered boards

d. Standstill agreements and White Knights

e. Poison Pills and tender offers

Answer:

Which of the following is generally not true about communication during the

integration period?

a. Communication should be as frequent as possible

b. Employees should be sheltered from bad news

c. The CEO of the combined firms should lead the effort to communicate to employees

at all levels

d. Regularly scheduled employee meetings are often the best way to communicate

progress to plan

e. The reasons for changing work practices and compensation must be thoroughly

explained to employees

Answer:

Premiums paid to LBO firm shareholders average

a. 20%

b. 70%

c. 5%

d. Less than typical mergers

e. More than typical mergers

Answer:

Which of the following is not true of licensing?

a. Licensing allows a firm to purchase the right to manufacture and sell another firm’s

products within a specific country or set of countries.

b. The licensor is normally paid a royalty on each unit sold.

c. Licensors have considerable control the manufacturing and marketing of their

products marketed in foreign countries.

d. The licensee takes the risks and makes the investments in facilities for

manufacturing, marketing and distribution of goods and services.

e. Licensing is an increasingly popular entry mode for smaller firms with insufficient

capital and limited brand recognition.

Answer:

Which of the following is the most common reason that M&As often fail to meet

expectations?

a. Overpayment

b. Form of payment

c. Large size of target firm

d. Inadequate post-merger due diligence

e. Poor post-merger communication

Answer:

Which of the following is a common problem associated with tracking stocks?

a. Tracking stocks often de-motivate managers of the business for which the stock is

created

b. Such stocks are too complicated for investors to understand

c. Tracking stocks may create internal operating conflicts among the parent’s business

units

d. Such stocks often create huge tax liabilities for the parent

e. None of the above

Answer:

Which of the following is not a characteristic of a spin-off?

a. The parent creates a new legal subsidiary for the business to be spun-off

b. The shares of the new subsidiary are sold to the public

c. The ownership of shares in the new legal subsidiary is the same as the stockholders’

proportional ownership of shares in the parent firm

d. The new business once spun-off has its own management and board

e. Spin-offs are generally not taxable to the parent’s shareholders if properly structured

Answer:

Which one of the following factors is not considered calculating a firm’s PEG ratio?

a. Projected growth rate of the value indicator (e.g., earnings)

b. Ratio of market price to value indicator (e.g., P/E)

c. Share exchange ratio

d. Historical growth rate of the value indicator

e. None of the above

Answer:

Which of the following statements about the comparable companies’ valuation method

is not true?

a. Requires the use of firms that are ‘substantially” similar to the target firm

b. Uses market based rather than cash flow based valuations

c. Often used as the basis of investment banker fairness opinions

d. Generally provides the most accurate valuation method

e. Provides an estimate of the target firm at a moment in time.

Answer:

Which of the following is not typically true of post-closing evaluation of an

acquisition?

a. It is important not to change the performance benchmarks against which the

acquisition is measured

b. It is critical to ask the tough questions

c. It is an opportunity to learn from mistakes

d. It is commonly done

e. It is frequently avoided by acquiring firms because of the potential for

embarrassment.

Answer:

Factors that are most likely to contribute to the magnitude of premiums paid to LBO

target firm shareholders are

a. Tax benefits

b. Improved operating efficiency

c. Improved decision making

d. A, B, and C

e. A and C only

Answer:

Inside M&A. Financial Services Firms Streamline their Operations

During 2005 and 2006, a wave of big financial services firms announced their

intentions to spin-off operations that did not seem to fit strategically with their core

business. In addition to realigning their strategies, the parent firms noted the favorable

tax consequences of a spin-off, the potential improvement in the parent’s financial

returns, the elimination of conflicts with customers, and the removal of what, for some,

had become a management distraction.

American Express announced plans in early 2005 to jettison its financial advisory

business through a tax-free spin-off to its shareholders. The firm also noted that it

would incur significant restructuring-related expenses just before the spin-off. Such

one-time write-offs by the parent are sometimes necessary to “clean up” the balance

sheet of the unit to be spun off and unburden the newly formed company’s earnings

performance. American Express anticipated substantial improvement in future financial

returns on assets as it will be eliminating more than $410 billion in assets from its

balance sheet that had been generating relatively meager earnings.

Investment bank Morgan Stanley announced in mid-2005 its intent to spin-off its

Discover Credit Card operation. While Discover Card generated about one fifth of the

firm’s pretax profits, Morgan Stanley had been unable to realize significant synergies

with its other operations. The move represented an attempt by senior Morgan Stanley

management to mute shareholder criticism of the company’s lackluster stock

performance due to what many viewed had been the firm’s excessive diversification.

Similarly, J.P. Morgan Chase announced plans in 2006 to spin off its $13 billion private

equity fund, J.P. Morgan Partners. The bank would invest up to $1 billion in a new fund

J.P. Morgan Partners plans to open as a successor to the current Global Fund. Because

the bank’s ownership position would be less than 25 percent, it would be classified as a

passive partner. The expectation is that, by jettisoning this operation, the bank would be

able to reduce earnings volatility and decrease competition between the bank and large

customers when making investments.

Discussion Questions:

1) Speculate as to why a firm may choose to spin-off rather than divest a business?

2) In what ways might the spin-offs harm parent firm shareholders?

Answer:

Stakeholders include which of the following groups?

a. Shareholders

b. Customers

c. Lenders

d. Suppliers

e. All of the above

Answer:

To decide if a business is worth more to the shareholder if sold, the parent firm

generally considers all of the following factors except for

a. The after-tax cash flows of the business to be sold

b. The after-tax sale value of the business to be sold

c. The parent’s cost of capital

d. A and B

e. A, B, and C

Answer:

The following takeover defenses are generally put in place by a firm before a takeover

attempt is

initiated.

a. Standstill agreements

b. Poison pills

c. Recapitalization

d. Corporate restructuring

e. Greenmail

Answer:

Which of the following tends to be true of LBOs

a. LBOs rely heavily on management incentives to improve operating performance

b. The premium paid to target firm shareholders often exceeds 40%

c. Tax benefits are predictable and are built into the purchase price premium

d. The cost of equity is likely to change as the LBO repays debt

e. All of the above

Answer:

Alcatel Merges with Lucent, Highlighting Cross-Cultural Issues

Alcatel SA and Lucent Technologies signed a merger pact on April 3, 2006, to form a

Paris-based telecommunications equipment giant. The combined firms would be led by

Lucent’s chief executive officer Patricia Russo. Her charge would be to meld two

cultures during a period of dynamic industry change. Lucent and Alcatel were

considered natural merger partners because they had overlapping product lines and

different strengths. More than two-thirds of Alcatel’s business came from Europe, Latin

America, the Middle East, and Africa. The French firm was particularly strong in

equipment that enabled regular telephone lines to carry high-speed Internet and digital

television traffic. Nearly two-thirds of Lucent’s business was in the United States. The

new company was expected to eliminate 10 percent of its workforce of 88,000 and save

$1.7 billion annually within three years by eliminating overlapping functions.

While billed as a merger of equals, Alcatel of France, the larger of the two, would take

the lead in shaping the future of the new firm, whose shares would be listed in Paris, not

in the United States. The board would have six members from the current Alcatel board

and six from the current Lucent board, as well as two independent directors that must

be European nationals. Alcatel CEO Serge Tehuruk would serve as the chairman of the

board. Much of Ms. Russo’s senior management team, including the chief operating

officer, chief financial officer, the head of the key emerging markets unit, and the

director of human resources, would come from Alcatel. To allay U.S. national security

concerns, the new company would form an independent U.S. subsidiary to administer

American government contracts. This subsidiary would be managed separately by a

board composed of three U.S. citizens acceptable to the U.S. government.

International combinations involving U.S. companies have had a spotty history in the

telecommunications industry. For example, British Telecommunications PLC and

AT&T Corp. saw their joint venture, Concert, formed in the late 1990s, collapse after

only a few years. Even outside the telecom industry, transatlantic mergers have been

fraught with problems. For example, Daimler Benz’s 1998 deal with Chrysler, which

was also billed as a merger of equals, was heavily weighted toward the German

company from the outset.

In integrating Lucent and Alcatel, Russo faced a number of practical obstacles,

including who would work out of Alcatel’s Paris headquarters. Russo, who became

Lucent’s chief executive in 2000 and does not speak French, had to navigate the

challenges of doing business in France. The French government has a big influence on

French companies and remains a large shareholder in the telecom and defense sectors.

Russo’s first big fight would be dealing with the job cuts that were anticipated in the

merger plan. French unions tend to be strong, and employees enjoy more legal

protections than elsewhere. Hundreds of thousands took to the streets in mid-2006 to

protest a new law that would make it easier for firms to hire and fire younger workers.

Russo has extensive experience with big layoffs. At Lucent, she helped orchestrate

spin-offs, layoffs, and buyouts involving nearly four-fifths of the firm’s workforce.

Making choices about cuts in a combined company would likely be even more difficult,

with Russo facing a level of resistance in France unheard of in the United States, where

it is generally accepted that most workers are subject to layoffs and dismissals. Alcatel

has been able to make many of its job cuts in recent years outside France, thereby

avoiding the greater difficulty of shedding French workers. Lucent workers feared that

they would be dismissed first simply because it is easier than dismissing their French

counterparts.

After the 2006 merger, the company posted six quarterly losses and took more than $4.5

billion in write-offs, while its stock plummeted more than 60 percent. An economic

slowdown and tight credit limited spending by phone companies. Moreover, the market

was getting more competitive, with China’s Huawei aggressively pricing its products.

However, other telecommunications equipment manufacturers facing the same

conditions have not fared nearly as badly as Alcatel-Lucent. Melding two

fundamentally different cultures (Alcatel’s entrepreneurial and Lucent’s centrally

controlled cultures) has proven daunting. Customers who were uncertain about the new

firm’s products migrated to competitors, forcing Alcatel-Lucent to slash prices even

more. Despite the aggressive job cuts, a substantial portion of the projected $3.1 billion

in savings from the layoffs were lost to discounts the company made to customers in an

effort to rebuild market share.

Frustrated by the lack of progress in turning around the business, the Alcatel-Lucent

board announced in July 2008 that Patricia Russo, the American chief executive, and

Serge Tchuruk, the French chairman, would leave the company by the end of the year.

The board also announced that, as part of the shake-up, the size of the board would be

reduced, with Henry Schacht, a former chief executive at Lucent, stepping down.

Perhaps hamstrung by its dual personality, the French-American company seemed

poised to take on a new personality of its own by jettisoning previous leadership.

Discussion Questions:

1) Explain the logic behind combining the two companies. Be specific.

2) What are the major challenges the management of the combined companies are

likely to face? How would you recommend resolving these issues?

3) Most corporate mergers are beset by differences in corporate cultures. How do

cross-border transactions compound these differences?

4) Why do you think mergers, both domestic and cross-border, are often communicated

by the acquirer and target firms’ management as mergers of equals?

5) In what way would you characterize this transaction as a merger of equals? In what

ways should it not be considered a merger of equals?

Answer:

Post merger earnings per share are affected by all of the following factors, except for

a. Acquiring firm’s outstanding shares

b. Price offered for the target company

c. Number of target firm’s outstanding shares

d. Current price of the acquiring company’s stock

e. Current price of the target firm’s stock

Answer:

Earn-outs tend to shift risk from the seller to the buyer in that a higher price is paid only

when the seller has met or exceeded certain performance criteria. True or False

Answer:

Which of the following best defines market segmentation

a. The identification of customers with common characteristics and needs

b. The identification of customers with heterogeneous characteristics and needs

c. The grouping of customers with different characteristics

d. The process of reducing large markets into smaller markets without regard to

customer characteristics

e. The process of identifying the various markets that comprise an industry without

regard to customer characteristics

Answer:

Each of the following is true about the acquisition search process except for

a. A candidate search should start with identifying the primary selection criteria.

b. The number of selection criteria should be as lengthy as possible.

c. At a minimum, the primary criteria should include the industry and desired size of

transaction.

d. The size of the transaction may be defined in terms of the maximum purchase price

the acquirer is willing to pay.

e. A search strategy entails the use of electronic databases, trade publications, and

querying the acquirer’s law, banking, and accounting firms for qualified candidates.

Answer:

Excess capacity in many industries often drives M&A activity as firms strive to achieve

which of the following?

a. Greater economies of scale

b. Greater economies of scope

c. Greater pricing power with customers

d. Greater pricing power with suppliers

e. All of the above

Answer:

“Grave Dancer” Takes Tribune Corporation Private in an Ill-Fated Transaction

At the closing in late December 2007, well-known real estate investor Sam Zell

described the takeover of the Tribune Company as “the transaction from hell.” His

comments were prescient in that what had appeared to be a cleverly crafted, albeit

highly leveraged, deal from a tax standpoint was unable to withstand the credit malaise

of The end came swiftly when the 161-year-old Tribune filed for bankruptcy on

December 8, 2008.

On April 2, 2007, the Tribune Corporation announced that the firm’s publicly traded

shares would be acquired in a multistage transaction valued at $8.2 billion. Tribune

owned at that time 9 newspapers, 23 television stations, a 25% stake in Comcast’s

SportsNet Chicago, and the Chicago Cubs baseball team. Publishing accounts for 75%

of the firm’s total $5.5 billion annual revenue, with the remainder coming from

broadcasting and entertainment. Advertising and circulation revenue had fallen by 9%

at the firm’s three largest newspapers (Los Angeles Times, Chicago Tribune, and

Newsday in New York) between 2004 and 2006. Despite aggressive efforts to cut costs,

Tribune’s stock had fallen more than 30% since 2005.

The transaction was implemented in a two-stage transaction, in which Sam Zell

acquired a controlling 51% interest in the first stage followed by a backend merger in

the second stage in which the remaining outstanding Tribune shares were acquired. In

the first stage, Tribune initiated a cash tender offer for 126 million shares (51% of total

shares) for $34 per share, totaling $4.2 billion. The tender was financed using $250

million of the $315 million provided by Sam Zell in the form of subordinated debt, plus

additional borrowing to cover the balance. Stage 2 was triggered when the deal received

regulatory approval. During this stage, an employee stock ownership plan (ESOP)

bought the rest of the shares at $34 a share (totaling about $4 billion), with Zell

providing the remaining $65 million of his pledge. Most of the ESOP’s 121 million

shares purchased were financed by debt guaranteed by the firm on behalf of the ESOP.

At that point, the ESOP held all of the remaining stock outstanding valued at about $4

billion. In exchange for his commitment of funds, Mr. Zell received a 15-year warrant

to acquire 40% of the common stock (newly issued) at a price set at $500 million.

Following closing in December 2007, all company contributions to employee pension

plans were funneled into the ESOP in the form of Tribune stock. Over time, the ESOP

would hold all the stock. Furthermore, Tribune was converted from a C corporation to a

Subchapter S corporation, allowing the firm to avoid corporate income taxes. However,

it would have to pay taxes on gains resulting from the sale of assets held less than ten

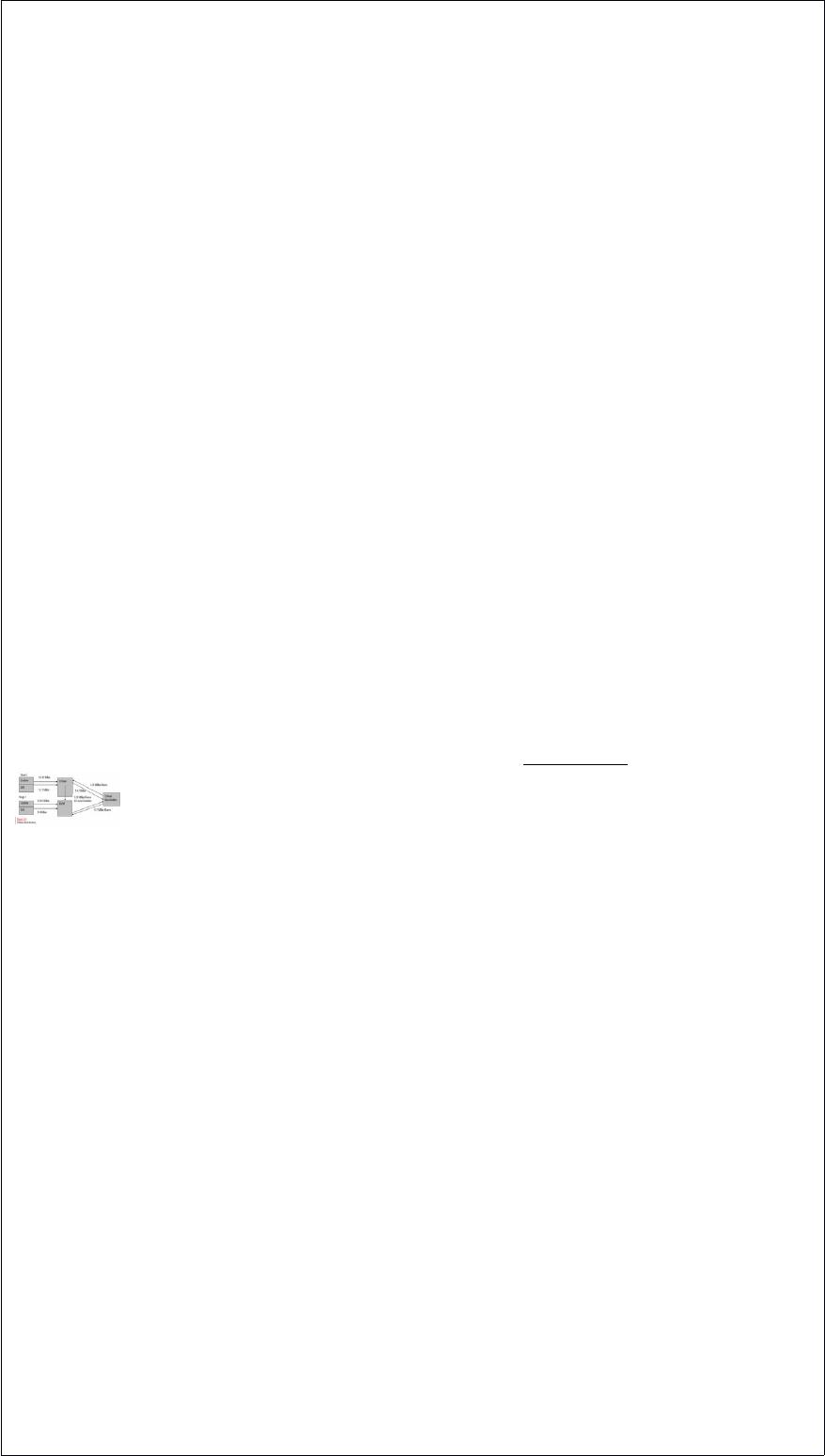

years after the conversion from a C to an S corporation (Figure 13.4).

Tribune deal structure.

The purchase of Tribune’s stock was financed almost entirely with debt, with Zell’s

equity contribution amounting to less than 4% of the purchase price. The transaction

resulted in Tribune being burdened with $13 billion in debt (including the approximate

$5 billion currently owed by Tribune). At this level, the firm’s debt was ten times

EBITDA, more than two and a half times that of the average media company. Annual

interest and principal repayments reached $800 million (almost three times their

preacquisition level), about 62% of the firm’s previous EBITDA cash flow of $1.3

billion. While the ESOP owned the company, it was not be liable for the debt

guaranteed by Tribune.

The conversion of Tribune into a Subchapter S corporation eliminated the firm’s current

annual tax liability of $348 million. Such entities pay no corporate income tax but must

pay all profit directly to shareholders, who then pay taxes on these distributions. Since

the ESOP was the sole shareholder, Tribune was expected to be largely tax exempt,

since ESOPs are not taxed.

In an effort to reduce the firm’s debt burden, the Tribune Company announced in early

2008 the formation of a partnership in which Cablevision Systems Corporation would

own 97% of Newsday for $650 million, with Tribune owning the remaining 3%.

However, Tribune was unable to sell the Chicago Cubs (which had been expected to

fetch as much as $1 billion) and the minority interest in SportsNet Chicago to help

reduce the debt amid the 2008 credit crisis. The worsening of the recession, accelerated

by the decline in newspaper and TV advertising revenue, as well as newspaper

circulation, thereby eroded the firm’s ability to meet its debt obligations.

By filing for Chapter 11 bankruptcy protection, the Tribune Company sought a reprieve

from its creditors while it attempted to restructure its business. Although the extent of

the losses to employees, creditors, and other stakeholders is difficult to determine, some

things are clear. Any pension funds set aside prior to the closing remain with the

employees, but it is likely that equity contributions made to the ESOP on behalf of the

employees since the closing would be lost. The employees would become general

creditors of Tribune. As a holder of subordinated debt, Mr. Zell had priority over the

employees if the firm was liquidated and the proceeds distributed to the creditors.

Those benefitting from the deal included Tribune’s public shareholders, including the

Chandler family, which owed 12% of Tribune as a result of its prior sale of the Times

Mirror to Tribune, and Dennis FitzSimons, the firm’s former CEO, who received $17.7

million in severance and $23.8 million for his holdings of Tribune shares. Citigroup and

Merrill Lynch received $35.8 million and $37 million, respectively, in advisory fees.

Morgan Stanley received $7.5 million for writing a fairness opinion letter. Finally,

Valuation Research Corporation received $1 million for providing a solvency opinion

indicating that Tribune could satisfy its loan covenants.

What appeared to be one of the most complex deals of 2007, designed to reap huge tax

advantages, soon became a victim of the downward-spiraling economy, the credit

crunch, and its own leverage. A lawsuit filed in late 2008 on behalf of Tribune

employees contended that the transaction was flawed from the outset and intended to

benefit Sam Zell and his advisors and Tribune’s board. Even if the employees win, they

will simply have to stand in line with other Tribune creditors awaiting the resolution of

the bankruptcy court proceedings.

Discussion Questions:

1) What is the acquisition vehicle, post-closing organization, form of payment, form of

acquisition, and tax strategy described in this case study?

2) Describe the firm’s strategy to finance the transaction?

3) Is this transaction best characterized as a merger, acquisition, leveraged buyout, or

spin-off? Explain your answer.

4) Is this transaction taxable or non-taxable to Tribune’s public shareholders? To its

post-transaction shareholders? Explain your answer.

5) Comment on the fairness of this transaction to the various stakeholders involved.

How would you apportion the responsibility for the eventual bankruptcy of Tribune

among Sam Zell and his advisors, the Tribune board, and the largely unforeseen

collapse of the credit markets in late 2008? Be specific.

Answer:

Financing Challenges in the Home Depot Supply Transaction

Buyout firms Bain Capital, Carlyle Group, and Clayton, Dubilier & Rice (CD&R) bid

$10.3 billion in June 2007 to buy Home Depot Inc.’s HD Supply business. HD Supply

represented a collection of small suppliers of construction products. Home Depot had

announced earlier in the year that it planned to use the proceeds of the sale to pay for a

portion of a $22.5 billion stock buyback.

Three banks, Lehman Brothers, JPMorgan Chase, and Merril Lynch agreed to provide

the firms with a $4 billion loan. The repayment of the loans was predicated on the

ability of the buyout firms to improve significantly HD Supply’s current cash flow.

Such loans are normally made with the presumption that they can be sold to investors,

with the banks collecting fees from both the borrower and investor groups. However, by

July, concern about the credit quality of subprime mortgages spread to the broader debt

market and raised questions about the potential for default of loans made to finance

highly leveraged transactions. The concern was particularly great for so-called

“covenant-lite” loans for which the repayment terms were very lenient.

Fearing they would not be able to resell such loans to investors, the three banks

involved in financing the HD Supply transaction wanted more financial protection.

Additional protection, they reasoned, would make such loans more marketable to

investors. They used the upheaval in the credit markets as a pretext for reopening

negotiations on their previous financing commitments. Home Depot was willing to

lower the selling price thereby reducing the amount of financing required by the buyout

firms and was willing to guarantee payment in the event of default by the buyout firms.

While Bain, Carlyle, and CD&R were willing to increase their cash investment and pay

higher fees to the banks, they were unwilling to alter the original terms of the loans.

Eventually the banks agreed to provide financing consisting of a $1 billion

“covenant-lite” loan and a $1.3 billion “payment-in-kind” loan. Home Depot agreed to

assume the loan payments on the $1 billion loan if the investor firms were to default

and to lower the selling price to $8.5 billion for 87.5 percent of HD Supply, with Home

Depot retaining the remaining 12.5 percent.

By the end of August, Home Depot had succeeded in raising the cash needed to help

pay for its share repurchase, and the banks had reduced their original commitment of $4

billion in loans to $2.3 billion. While they had agreed to put more money into the

transaction, the buyout firms had been successful in limiting the number of new

restrictive covenants.

Case Study Discussion Questions:

1) Based on the information given it the case, determine the amount of the price

reduction Home Depot accepted for HD Supply and the amount of cash the three

buyout firms put into the transaction?

2) Why did banks lower their lending standards in financing LBOs in 2006 and early

2007? How did the lax

standards contribute to their inability to sell the loans to investors? How did the

inability to sell the loans once made curtail their future lending?

Answer:

Kraft Foods Undertakes Split-Off of Post Cereals in Merger-Related Transaction

In August 2008, Kraft Foods announced an exchange offer related to the split-off of its

Post Cereals unit and the closing of the merger of its Post Cereals business into a

wholly-owned subsidiary of Ralcorp Holdings. Kraft is a major manufacturer and

distributor of foods and beverages; Post is a leading manufacturer of breakfast cereals;

and Ralcorp manufactures and distributes brand-name products in grocery and mass

merchandise food outlets. The objective of the transaction was to allow Kraft

shareholders participating in the exchange offer for Kraft Sub stock to become

shareholders in Ralcorp and Kraft to receive almost $1 billion in cash or cash

equivalents on a tax-free basis.

Prior to the transaction, Kraft borrowed $300 million from outside lenders and

established Kraft Sub, a shell corporation wholly owned by Kraft. Kraft subsequently

transferred the Post assets and associated liabilities, along with the liability Kraft

incurred in raising $300 million, to Kraft Sub in exchange for all of Kraft Sub’s stock

and $660 million in debt securities issued by Kraft Sub to be paid to Kraft at the end of

ten years. In effect, Post was conveyed to Kraft Sub in exchange for assuming Kraft’s

$300 million liability, 100% of Kraft Sub’s stock, and Kraft Sub debt securities with a

principal amount of $660 million. The consideration that Kraft received, consisting of

the debt assumption by Kraft Sub, the debt securities from Kraft Sub, and the Kraft Sub

stock, is considered tax free to Kraft, since it is viewed simply as an internal

reorganization rather than a sale.1 Kraft later converted to cash the securities received

from Kraft Sub by selling them to a consortium of banks.

In the related split-off transaction, Kraft shareholders had the option to exchange their

shares of Kraft common stock for shares of Kraft Sub, which owned the assets and

liabilities of Post. If Kraft was unable to exchange all of the Kraft Sub common shares,

Kraft would distribute the remaining shares as a dividend (i.e., spin-off) on a pro rata

basis to Kraft shareholders.

With the completion of the merger of Kraft Sub with Ralcorp Sub (a Ralcorp

wholly-owned subsidiary), the common shares of Kraft Sub were exchanged for shares

of Ralcorp stock on a one for one basis. Consequently, Kraft shareholders tendering

their Kraft shares in the exchange offer owned 0.6606 of a share of Ralcorp stock for

each Kraft share exchanged as part of the split-off.

Concurrent with the exchange offer, Kraft closed the merger of Post with Ralcorp. Kraft

shareholders received Ralcorp stock valued at $1.6 billion, resulting in their owning

54% of the merged firm. By satisfying the Morris Trust tax code regulations,2 the

transaction was tax free to Kraft shareholders. Ralcorp Sub was later merged into

Ralcorp. As such, Ralcorp assumed the liabilities of Ralcorp Sub, including the $660

million owed to Kraft.

The purchase price for Post equaled $2.56 billion. This price consisted of $1.6 billion in

Ralcorp stock received by Kraft shareholders and $960 million in cash equivalents

received by Kraft. The $960 million included the assumption of the $300 million

liability by Kraft Sub and the $660 million in debt securities received from Kraft Sub.3

The steps involved in the transaction are described in Exhibit 1.

Discussion Questions and Answers:

1) What does the decision to split up the firm say about Kraft’s decision to buy Cadbury

in 2010?

2) Why did Kraft chose not to divest its grocery business, using the proceeds to either

reinvest in its faster growing snack business, to buy back its stock, or a combination of

the two?

3) How might a spin-off create shareholder value for Kraft Foods shareholders?

4) Kraft CEO Irene Rosenfeld argued that an important justification for the Cadbury

acquisition in 2010 was to create two portfolios of businesses: some very strong cash

generating businesses and some very strong growth businesses in order to increase

shareholder value. How might this strategy have boosted the firm’s value?

5) While Kraft’s share value did increase following the Cadbury deal, it lagged the

performance of key competitors. Why do you believe this was the case? Explain your

answer.

6) There is often a natural tension between so-called activist investors interested in

short-term profits and a firm’s management interested in pursuing a longer-term vision.

When is this tension helpful to shareholders and when does it destroy shareholder

value?

Answer:

The Bear Stearns SagaWhen Failure Is Not an Option

Prodded by the Fed and the U.S. Treasury Department, J.P. Morgan Chase (JPM), the

nation’s third largest bank, announced, on March 17, 2008, that it had reached an

agreement to buy 100 percent of Bear Stearns’s outstanding equity for $2 per share. As

one of the nation’s larger investment banks, Bear Stearns had a reputation for being

aggressive in the financial derivatives markets. Hammered out in two days, the

agreement called for the Fed to guarantee up to $30 billion of Bear Stearns’s “less

liquid” assets. In an effort to avoid what was characterized as a ‘systemic meltdown,”

regulatory approval was obtained at a breakneck pace. The Office of the Comptroller of

Currency and Fed approvals were in place at the time of the announcement. The SEC

elected not to review the deal. Federal and state antitrust regulatory approvals were

obtained in record time.

With investors fleeing mortgage-backed securities, the Fed was hoping to prevent any

further deterioration in the value of such investments. The fear was that the financial

crisis that beset Bear Stearns could spread to other companies and ultimately test the

Fed’s resources after it had said publicly that it would lend up to $200 billion to banks

in exchange for their holdings of mortgages.

Interestingly, Bear Stearns was not that big among investment banks when measured by

asset size. However, it was theoretically liable for as much as $10 trillion due to its

holdings of such financial derivatives as credit default swaps, in which it agreed to pay

lenders in the event of a borrower defaulting. If credit defaults became widespread,

Bear Stearns would not have been able to honor its contractual commitments, and the

ability of other investment banks in similar positions would have been questioned and

the panic could have spread.

With Bear Stearns’s shareholders threatening not to approve what they viewed as a “fire

sale,” JPM provided an alternative bid, within several days of the initial bid, in which it

offered $2.4 billion for about 40 percent of the stock, or about $10 per share. In

exchange for the higher offer, Bear Stearns agreed to sell 95 million newly issued

shares to JPM, giving JPM a 39.5 percent stake and an almost certain majority in any

shareholder vote, effectively discouraging any alternative bids. Under the new offer,

JPM assumed responsibility for the first $1 billion in asset losses, before the Fed’s

guarantee of up to $30 billion takes effect..

Discussion Questions

1) Why do you believe government regulators encouraged a private firm (J.P. Morgan

Chase) to acquire Bear Stearns rather than have the government take control? Do you

believe this was the appropriate course of action? Explain your answer.

2) By facilitating the merger, the Fed sent a message to Wall Street that certain financial

institutions are “too big to fail.” What effect do you think the merger will have on the

future investment activities of investment banks? Be specific.

Answer:

Cox Enterprises Offers to Take Cox Communications Private

In an effort to take the firm private, Cox Enterprises announced on August 3, 2004 a

proposal to buy the remaining 38% of Cox Communications’ shares that they did not

currently own for $32 per share. The deal is valued at $7.9 billion and represented a

16% premium to Cox Communication’s share price at that time. Cox Communications

would become a subsidiary of Cox Enterprises and would continue to operate as an

autonomous business. In response to the proposal, the Cox Communications Board of

Directors formed a special committee of independent directors to consider the proposal.

Citigroup Global Markets and Lehman Brothers Inc. have committed $10 billion to the

deal. Cox Enterprises would use $7.9 billion for the tender offer, with the remaining

$2.1 billion used for refinancing existing debt and to satisfy working capital

requirements.

Cable service firms have faced intensified competitive pressures from satellite service

providers DirecTV Group and EchoStar communications. Moreover, telephone

companies continue to attack cable’s high-speed Internet service by cutting prices on

high-speed Internet service over phone lines. Cable firms have responded by offering a

broader range of advanced services like video-on-demand and phone service. Since

2000, the cable industry has invested more than $80 billion to upgrade their systems to

provide such services, causing profitability to deteriorate and frustrating investors. In

response, cable company stock prices have fallen. Cox Enterprises stated that the

increasingly competitive cable industry environment makes investment in the cable

industry best done through a private company structure.

Discussion Questions::

1) Why did the board feel that it was appropriate to set up special committee of

independent board directors?

2) Why does Cox Enterprises believe that the investment needed for growing its cable

business is best done through a private company structure?

Answer:

GHS Helps Itself by Avoiding an IPO

In 1999, GHS, Inc., a little known supplier of medical devices, engineered a reverse

merger to avoid the time-consuming, disclosure-intensive, and costly process of an

initial public offering to launch its new internet-based self-help website. GHS spun off

its medical operations as a separate company to its shareholders. The remaining shell is

being used to launch a ”self-help” Website, with self-help guru Anthony Robbins as its

CEO. The shell corporation will be financed by $3 million it had on hand as GHS and

will receive another $15 million from a private placement. With the inclusion of

Anthony Robbins as the first among many brand names in the self-help industry that it

hopes to feature on its site, its stock soared from $.75 per share to more than $12

between May and August 1999. Robbins, who did not invest anything in the venture,

has stock in the new company valued at $276 million. His contribution to the company

is the exclusive online rights to his name, which it will use to develop Internet self-help

seminars, chat rooms, and e-commerce sites.

Discussion Questions:

1) What are the advantages of employing a reverse merger strategy in this instance?

2) Why was the shell corporation financed through a private placement?

Answer:

The Man Behind the Legend at Berkshire Hathaway

Although not exactly a household name, Berkshire Hathaway (“Berkshire”) has long

been a high flier on Wall Street. The firm’s share price has outperformed the total return

on the Standard and Poor’s 500 stock index in 32 of the 36 years that Warren Buffet has

managed the firm. Berkshire Hathaway’s share price rose from $12 per share to $71,000

at the end of 2000, an annual rate of growth of 27%. With revenue in excess of $30

billion, Berkshire is among the top 50 of the Fortune 500 companies.

What makes the company unusual is that it is one of the few highly diversified

companies to outperform consistently the S&P 500 over many years. As a

conglomerate, Berkshire acquires or makes investments in a broad cross-section of

companies. It owns operations in such diverse areas as insurance, furniture, flight

services, vacuum cleaners, retailing, carpet manufacturing, paint, insulation and roofing

products, newspapers, candy, shoes, steel warehousing, uniforms, and an electric utility.

The firm also has “passive” investments in such major companies as Coca-Cola,

American Express, Gillette, and the Washington Post.

Warren Buffet’s investing philosophy is relatively simple. It consists of buying

businesses that generate an attractive sustainable growth in earnings and leaving them

alone. He is a long-term investor. Synergy among his holdings never seems to play an

important role. He has shown a propensity to invest in relatively mundane businesses

that have a preeminent position in their markets; he has assiduously avoided businesses

he felt that he did not understand such as those in high technology industries. He also

has shown a tendency to acquire businesses that were “out of favor” on Wall Street.

He has built a cash-generating machine, principally through his insurance operations

that produce “float” (i.e., premium revenues that insurers invest in advance of paying

claims). In 2000, Berkshire acquired eight firms. Usually flush with cash, Buffet has

developed a reputation for being nimble. This most recently was demonstrated in his

acquisition of Johns Manville in late 2000. Manville generated $2 billion in revenue

from insulation and roofing products and more than $200 million in after-tax profits.

Manville’s controlling stockholder was a trust that had been set up to assume the firm’s

asbestos liabilities when Manville had emerged from bankruptcy in the late 1980s. After

a buyout group that had offered to buy the company for $2.8 billion backed out of the

transaction on December 8, 2000, Berkshire contacted the trust and acquired Manville

for $2.2 billion in cash. By December 20, Manville and Berkshire reached an

agreement.

Discussion Questions:

1) To what do you attribute Warren Buffet’s long-term success?

2) In what ways might Warren Buffet use “financial synergy” to grow Berkshire

Hathaway? Explain your answer.

Answer:

Justice Department Requires VeriFone Systems to Sell Assets

before Approving Hypercom Acquisition

Key Points:

Asset sales commonly are used by regulators to thwart the potential build-up of

market power resulting from a merger or acquisition.

In such situations, defining the appropriate market served by the merged firms is

crucial to identifying current and potential competitors.

______________________________________________________________________

________

In late 2011, VeriFone Systems (VeriFone) reached a settlement with the U.S. Justice

Department to acquire competitor Hypercom Corp on the condition it sold Hypercom’s

U.S. point-of-sale terminal business. Business use point-of-sale terminals are used by

retailers to accept electronic payments such as credit and debit cards.

The Justice Department had sued to block the $485 million deal on concerns that the

combination would limit competition in the market for retail checkout terminals. The

asset sale is intended to create a significant independent competitor in the U.S. The

agreement stipulates that private equity firm Gores Group LLC will buy the terminals

business.

San Jose, California-based VeriFone is the second largest maker of electronic payment

equipment in the U.S. and Hypercom, based in Scottsdale, Arizona, is number three.

Together, the firms control more than 60 percent of the U.S. market for terminals used

by retailers. Ingenico SA, based in France, is the largest maker of card-payment

terminals. The Justice Department had blocked a previous attempt to sell Hypercom’s

U.S. point-of-sale business to rival Ingenico, saying that it would have increased

concentration and undermined competition.

VeriFone will retain Hypercom’s point-of-sale equipment business outside the U.S. The

acquisition will enable VeriFone to expand in the emerging market for payments made

via mobile phones by giving it a larger international presence in retail stores and the

opportunity to install more terminals capable of accepting mobile phone payments

abroad.

Discussion Questions

1) Do you believe requiring consent decrees that oblige the acquiring firm to dispose of

certain target

company assets is an abuse of government power? Why or why not?

2) What alternative actions could the government take to limit market power resulting

from a business

combination?

Answer:

Justice Department Approves Maytag/Whirlpool Combination

Despite Resulting Increase in Concentration

When announced in late 2005, many analysts believed that the $1.7 billion transaction

would face heated anti-trust regulatory opposition. The proposed bid was approved

despite the combined firms’ dominant market share of the U.S. major appliance market.

The combined companies would control an estimated 72 percent of the washer market,

81 percent of the gas dryer market, 74 percent of electric dryers, and 31 percent of

refrigerators. Analysts believed that the combined firms would be required to divest

certain Maytag product lines to receive approval. Recognizing the potential difficulty in

getting regulatory approval, the Whirlpool/Maytag contract allowed Whirlpool (the

acquirer) to withdraw from the contract by paying a “reverse breakup” fee of $120

million to Maytag (the target). Breakup fees are normally paid by targets to acquirers if

they choose to withdraw from the contract.

U.S. regulators tended to view the market as global in nature. When the appliance

market is defined in a global sense, the combined firms’ share drops to about one fourth

of the previously mentioned levels. The number and diversity of foreign manufacturers

offered a wide array of alternatives for consumers. Moreover, there are few barriers to

entry for these manufacturers wishing to do business in the United States. Many of

Whirlpool’s independent retail outlets wrote letters supporting the proposal to acquire

Maytag as a means of sustaining financially weakened companies. Regulators also

viewed the preservation of jobs as an important consideration in its favorable ruling.

Discussion Questions:

1) What is anti-trust policy and why is it important?

2) What factors other than market share should be considered in determining whether a

potential merger might result in an increased pricing power?

Answer:

Overcoming Culture Clash:

Allianz AG Buys Pimco Advisors LP

On November 7, 1999, Allianz AG, the leading German insurance conglomerate,

acquired Pimco Advisors LP for $3.3 billion. The Pimco acquisition boosts assets under

management at Allianz from $400 billion to $650 billion, making it the sixth largest

money manager in the world.

The cultural divide separating the two firms represented a potentially daunting

challenge. Allianz’s management was well aware that firms distracted by culture clashes

and the morale problems and mistrust they breed are less likely to realize the synergies

and savings that caused them to acquire the company in the first place. Allianz was

acutely aware of the potential problems as a result of difficulties they had experienced

following the acquisition of Firemen’s Fund, a large U.S.-based propertycasualty

company.

A major motivation for the acquisition was to obtain the well-known skills of the elite

Pimco money managers to broaden Allianz’s financial services product offering.

Although retention bonuses can buy loyalty in the short run, employees of the acquired

firm generally need much more than money in the long term. Pimco’s money managers

stated publicly that they wanted Allianz to let them operate independently, the way

Pimco existed under their former parent, Pacific Mutual Life Insurance Company.

Allianz had decided not only to run Pimco as an independent subsidiary but also to

move $100 billion of Allianz’s assets to Pimco. Bill Gross, Pimco’s legendary bond

trader, and other top Pimco money managers, now collect about one-fourth of their

compensation in the form of Allianz stock. Moreover, most of the top managers have

been asked to sign long-term employment contracts and have received retention

bonuses.

Joachim Faber, chief of money management at Allianz, played an essential role in

smoothing over cultural differences. Led by Faber, top Allianz executives had been

visiting Pimco for months and having quiet dinners with top Pimco fixed income

investment officials and their families. The intent of these intimate meetings was to

reassure these officials that their operation would remain independent under Allianz’s

ownership.

Discussion Questions:

1) How did Allianz attempt to retain key employees? In the short run? In the long run?

2) How did the potential for culture clash affect the way Alliance acquired Pimco?

3) What else could Allianz have done to minimize potential culture clash? Be specific.

Answer:

Sony Buys MGM

Sony’s long-term vision has been to create synergy between its consumer electronics

products and music, movies, and games. Sony, which bought Columbia Pictures in

1989 for $3.4 billion, had wanted to control Metro-Goldwyn-Mayer’s film library for

years, but it did not want to pay the estimated $5 billion it would take to acquire it. On

September 14, 2004, a consortium, consisting of Sony Corp of America, Providence

Equity Partners, Texas Pacific Group, and DLJ Merchant Banking Partners, agreed to

acquire MGM for $4.8 billion, consisting of $2.85 billion in cash and the assumption of

$2 billion in debt. The cash portion of the purchase price consisted of about $1.8 billion

in debt and $1 billion in equity capital. Of the equity capital, Providence contributed

$450 million, Sony and Texas Pacific Group $300 million, and DLJ Merchant Banking

$250 million.

The combination of Sony and MGM will create the world’s largest film library of about

7,600 titles, with MGM contributing about 54 percent of the combined libraries. Sony

will control MGM and Comcast will distribute the films over cable TV. Sony will shut

down MGM’s film making operations and move all operations to Sony. Kirk Kerkorian,

who holds a 74 percent stake in MGM, will make $2 billion because of the transaction.

The private equity partners could cash out within three-to-five years, with the

consortium undertaking an initial public offering or sale to a strategic investor. Major

risks include the ability of the consortium partners to maintain harmonious relations and

the problematic growth potential of the DVD market.

Sony and MGM negotiations had proven to be highly contentious for almost five

months when media giant Time Warner Inc. emerged to attempt to satisfy Kerkorian’s

$5 billion asking price. The offer was made in stock on the assumption that Kerkorian

would want a tax-free transaction. MGM’s negotiations with Time Warner stalled

around the actual value of Time Warner stock, with Kerkorian leery about Time

Warner’s future growth potential. Time Warner changed its bid in late August to an all

cash offer, albeit somewhat lower than the Sony consortium bid, but it was more

certain. Sony still did not have all of its financing in place. Time Warner had a

“handshake agreement” with MGM by Labor Day for $11 per share, about $.25 less

than Sony’s.

The Sony consortium huddled throughout the Labor Day weekend to put in place the

financing for a bid of $12 per share. What often takes months to work out in most

leveraged buyouts was hammered out in three days of marathon sessions at law firm

Davis Polk & Wardwell. In addition to getting final agreement on financing

arrangements including loan guarantees from J.P. Morgan Chase & Company, Sony was

able to reach agreement with Comcast to feature MGM movies in new cable and

video-on-demand TV channels. This distribution mechanism meant additional revenue

for Sony, making it possible to increase the bid to $12 per share. Sony also offered to

make a $150 non-refundable cash payment to MGM. As a testament to the adage that

timing is everything, the revised Sony bid was faxed to MGM just before the beginning

of a board meeting to approve the Time Warner offer.

Discussion Questions:

1) Do you believe that MGM is an attractive LBO candidate? Why? Why not?

2) In what way do you believe that Sony’s objectives might differ from those of the

private equity investors making up the remainder of the consortium? How might such

differences affect the management of MGM? Identify possible short-term and long-term

effects.

3) How did Time Warner’s entry into the bidding affect pace of the negotiations and the

relative bargaining power of MGM, Time Warner, and the Sony consortium?

4) What do you believe were the major factors persuading the MGM board to accept the

Revised Sony bid? In your judgment, do these factors make sense? Explain your

answer.

Answer:

Oracle Continues Its Efforts to Consolidate the Software Industry

Oracle CEO Larry Ellison continued his effort to implement his software industry

strategy when he announced the acquisition of Siebel Systems Inc. for $5.85 billion in

stock and cash on September 13, 2005. The global software industry includes hundreds

of firms. During the first nine months of 2005, Oracle had closed seven acquisitions,

including its recently completed $10.6 billion hostile takeover of PeopleSoft. In each

case, Oracle realized substantial cost savings by terminating duplicate employees and

related overhead expenses. The Siebel acquisition accelerates the drive by Oracle to

overtake SAP as the world’s largest maker of business applications software, which

automates a wide range of administrative tasks. The consolidation strategy seeks to add

the existing business of a competitor, while broadening the customer base for Oracle’s

existing product offering.

Siebel, founded by Ellison’s one-time protégé turned bitter rival, Tom Siebel, gained

prominence in Silicon Valley in the late 1990s as a leader in customer relationship

management (CRM) software. CRM software helps firms track sales, customer service,

and marketing functions. Siebel’s dominance of this market has since eroded amidst

complaints that the software was complicated and expensive to install. Moreover, Siebel

ignored customer requests to deliver the software via the Internet. Also, aggressive

rivals, like SAP and online upstart Salesforce.com have cut into Siebel’s business in

recent years with simpler offerings. Siebel’s annual revenue had plunged from about

$2.1 billion in 2001 to $1.3 billion in 2004.

In the past, Mr. Ellison attempted to hasten Siebel’s demise, declaring in 2003 that

Siebel would vanish and putting pressure on the smaller company by revealing he had

held takeover talks with the firm’s CEO, Thomas Siebel. Ellison’s public announcement

of these talks heightened the personal enmity between the two CEOs, making Siebel an

unwilling seller.

Oracle’s intensifying focus on business applications software largely reflects the

slowing growth of its database product line, which accounts for more than three fourths

of the company’s sales.

Siebel’s technology and deep customer relationships give Oracle a competitive software

bundle that includes a database, middleware (i.e., software that helps a variety of

applications work together as if they were a single system), and high-quality customer

relationship management software. The acquisition also deprives Oracle competitors,

such as IBM, of customers for their services business.

Customers, who once bought the so-called best-of-breed products, now seek a single

supplier to provide programs that work well together. Oracle pledged to deliver an

integrated suite of applications by 2007. What brought Oracle and Siebel together in the

past was a shift in market dynamics. The customer and the partner community is

communicating quite clearly that they are looking for an integrated set of products.

Germany’s SAP, Oracle’s major competitor in the business applications software

market, played down the impact of the merger, saying they had no reason to react and

described any deals SAP is likely to make as “targeted, fill-in acquisitions.” For IBM,

the Siebel deal raised concerns about the computer giant’s partners falling under the

control of a competitor. IBM and Oracle compete fiercely in the database software

market. Siebel has worked closely with IBM, as did PeopleSoft and J.D. Edwards,

which had been purchased by PeopleSoft shortly before its acquisition by Oracle.

Retek, another major partner of IBM, had also been recently acquired by Oracle. IBM

had declared its strategy to be a key partner to thousands of software vendors and that it

would continue to provide customers with IBM hardware, middleware, and other

applications.

Discussion Questions:

1) How would you characterize the Oracle business strategy (i.e., cost leadership,

differentiation, niche, or some combination of all three)? Explain your answer.

2) What other benefits for Oracle, and for the remaining competitors such as SAP, do

you see from further industry consolidation? Be specific.

3) Conduct an external and internal analysis of Oracle. Briefly describe those factors

that influenced the development of Oracle’s business strategy. Be specific.

4) In what way do you think the Oracle strategy was targeting key competitors? Be

specific.

Answer:

Kinder Morgan Buyout Raises Ethical Questions

In the largest management buyout in U.S. history at that time, Kinder Morgan Inc.’s

management proposed to take the oil and gas pipeline firm private in 2006 in a

transaction that valued the firm’s outstanding equity at $13.5 billion. Under the

proposal, chief executive Richard Kinder and other senior executives would contribute

shares valued at $2.8 billion to the newly private company. An additional $4.5 billion

would come from private equity investors, including Goldman Sachs Capital partners,

American International Group Inc., and the Carlyle Group. Including assumed debt, the

transaction was valued at about $22 billion. The transaction also was notable for the

governance and ethical issues it raised. Reflecting the struggles within the corporation,

the deal did not close until mid-2007.

The top management of Kinder Morgan Inc. waited more than two months before

informing the firm’s board of its desire to take the company private. It is customary for