1) Lester Corporation had 8,200 units of work in process on November 1 . During

November, 26,800 units were started and as of November 30, 7,900 units remained in

production. How many units were completed during November?

A.16,100

B.26,500

C.27,100

D.42,800

E.None of the other answers are correct

2) During a recent accounting period, Marty’s shipping department processed 26 orders.

Each order typically takes four hours to complete. However, the average time increased

to five hours because of various departmental inefficiencies. If shipping labor is paid

$14 per hour, the company’s non-value-added cost would be:

A.$0

B.$56

C.$364

D.$1,456

E.$1,820

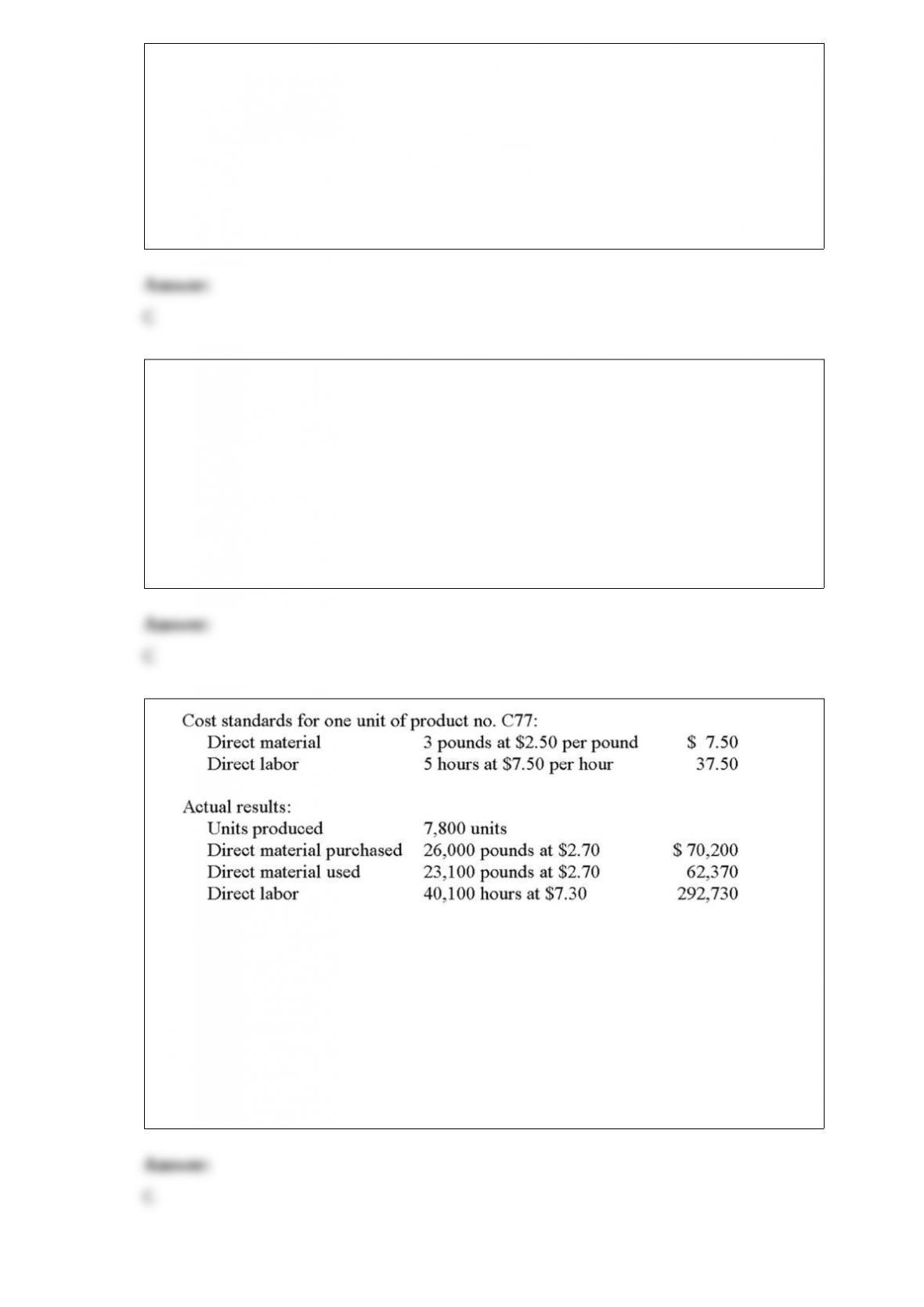

3)

Assume that the company computes variances at the earliest point in time.

The direct-labor rate variance is:

A.$7,800F

B.$7,950F

C.$8,020F

D.$8,000U

E.none of the other answers are correct

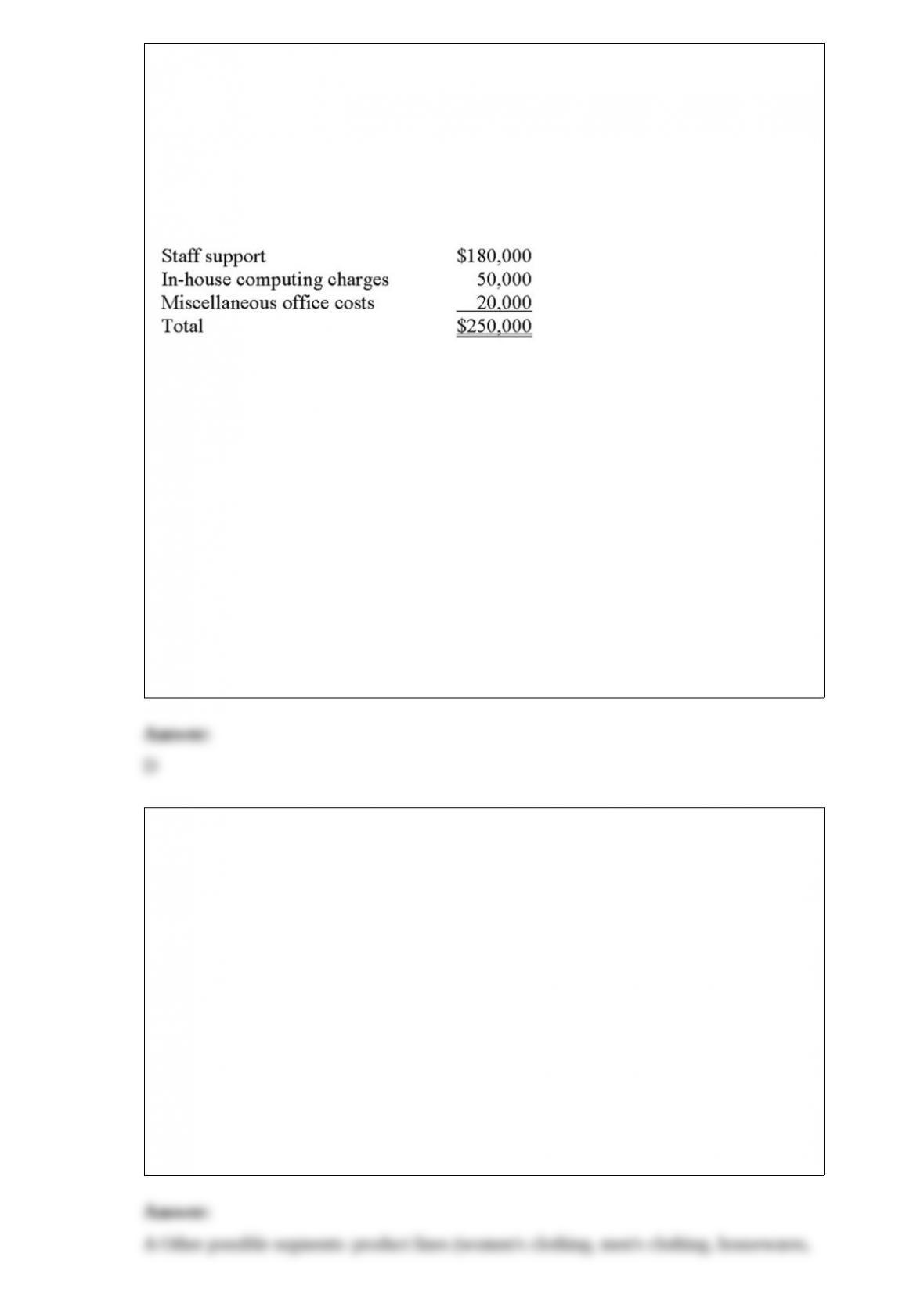

4) Kelly and Logan, an accounting firm, provides consulting and tax planning services.

For many years, the firm’s total administrative cost (currently $250,000) has been

allocated to services on the basis of billable hours to clients. A recent analysis found

that 65% of the firm’s billable hours to clients resulted from tax planning services, while

35% resulted from consulting services.

The firm, contemplating a change to activity-based costing, has identified three

components of administrative cost, as follows:

A recent analysis of staff support found a strong correlation between the number of staff

personnel and the number of clients served (consulting, 20; tax planning, 60). In

contrast, in-house computing and miscellaneous office cost varied directly with the

number of computer hours logged and number of client transactions, respectively.

Consulting consumed 30% of the firm’s computer hours and had 20% of the total client

transactions.

Assuming the use of activity-based costing, the proper percentage to use in allocating

staff support costs to tax planning services is:

A.20%

B.60%

C.65%

D.75%

E.80%

5) Segmented income statements are used to show revenues, expenses, and income for

major parts of an organization.

Required:

A. Consider a regional chain of department stores that has two or three stores in each of

several cities. One way to segment this business is geographically. Describe another

way of segmenting the firm.

B. Segmented income statements often distinguish between “fixed expenses

controllable by the segment manager” and “fixed expenses traceable to the segment, but

controllable by others.” Assume that the Cleveland district has three retail stores. Give

two examples of each type of fixed cost.

C. Common costs create difficulties when preparing segmented income statements.

Define “common costs,” give an example for the regional chain of department stores,

and explain in general terms why such costs create a problem.

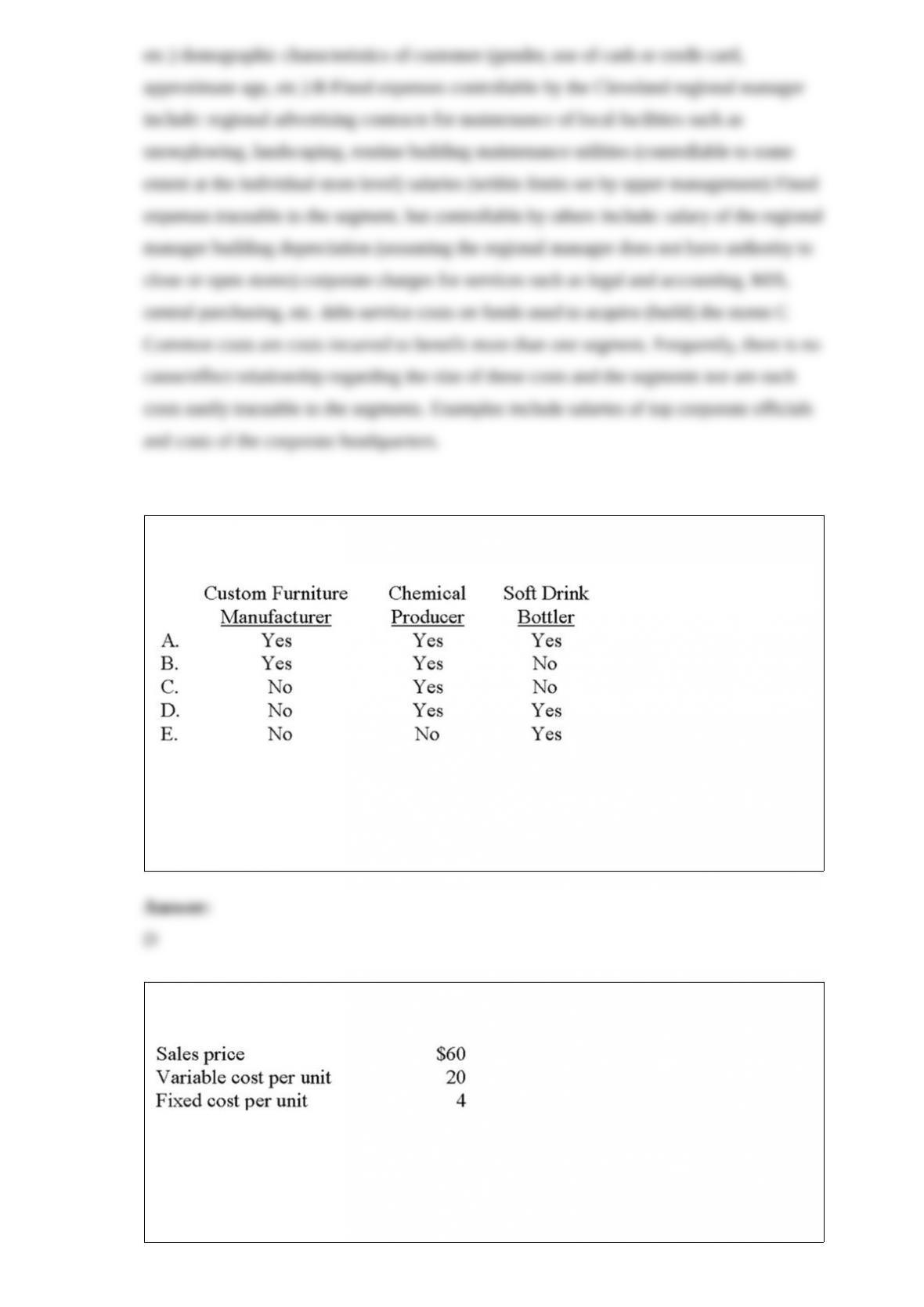

6) Which of the following companies would likely use a process-costing system?

A.Choice A

B.Choice B

C.Choice C

D.Choice D

E.Choice E

7) At a volume level of 500,000 units, Sullivan reported the following information:

The company’s contribution-margin ratio is closest to:

A.0.33

B.0.40

C.0.60

D.0.67

E.None of the other answers is correct

8) Which of the following project evaluation methods focuses on accounting income

rather than cash flows?

A.Net present value

B.Accounting rate of return

C.Internal rate of return

D.Payback period

E.None of the other answers are correct

9) The high-low method and least-squares regression are used by accountants to:

A.evaluate divisional managers for purposes of raises and promotions

B.choose among alternative courses of action

C.maximize output

D.estimate costs

E.control operations

10) Which of the following statements about manufacturing cost flows is false?

A.Direct materials, direct labor, and manufacturing overhead are entered in the

Work-in-Process Inventory account

B.The Finished-Goods Inventory account will contain entries that reflect the cost of

goods sold during the period

C.The cost of units sold during the period will typically appear on the income statement

D.When a company sells goods that cost $54,000 for $60,000, the firm will enter

$6,000 in an account entitled Profit on Sale

E.Units are normally transferred from Work-in-Process Inventory to Finished-Goods

Inventory

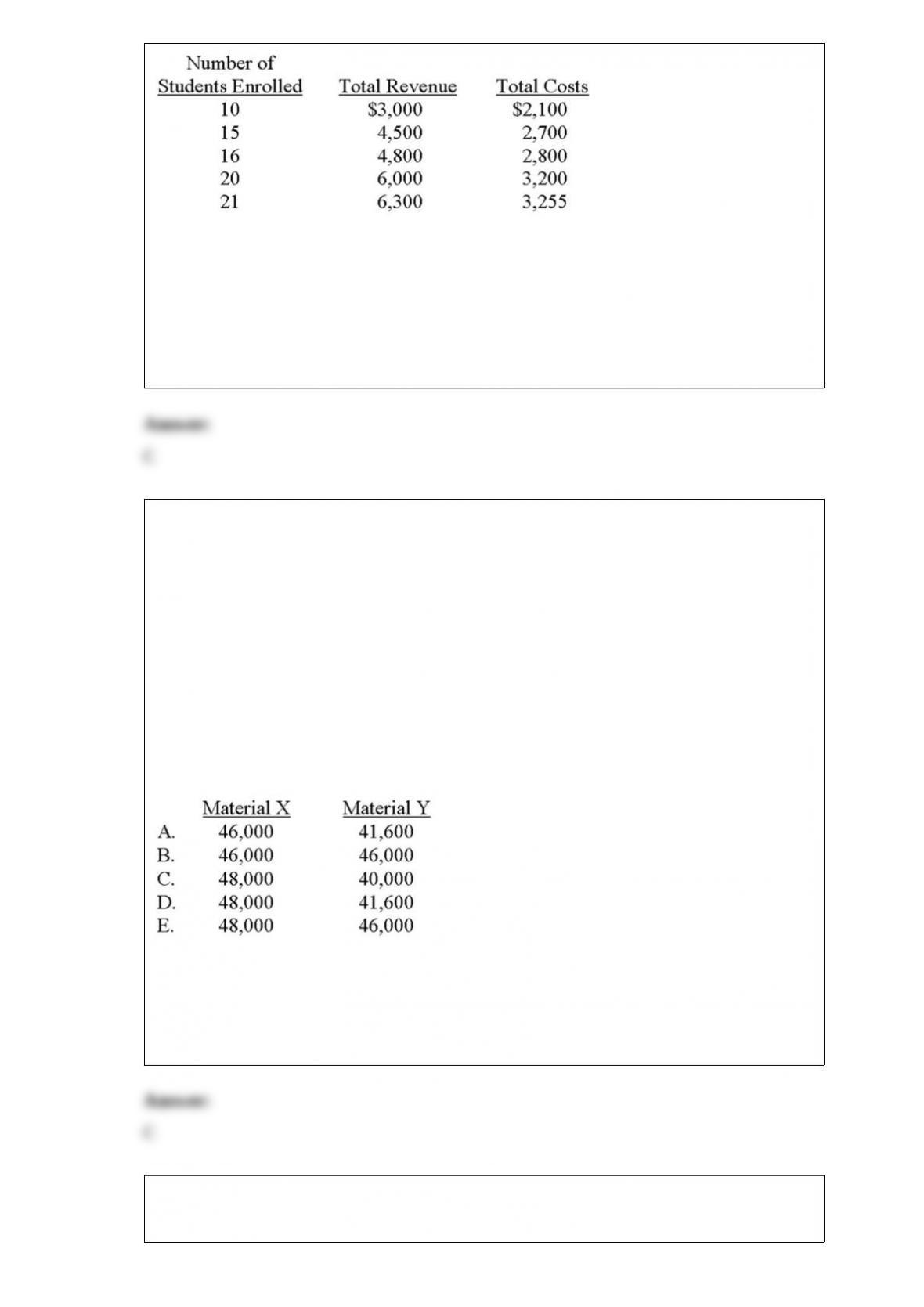

11) Wee Care is a nursery school for pre-kindergarten children. The school has

determined that the following biweekly revenues and costs occur at different levels of

enrollment:

The average cost per student when 16 students enroll in the school is:

A.$100

B.$125

C.$175

D.$300

E.$400

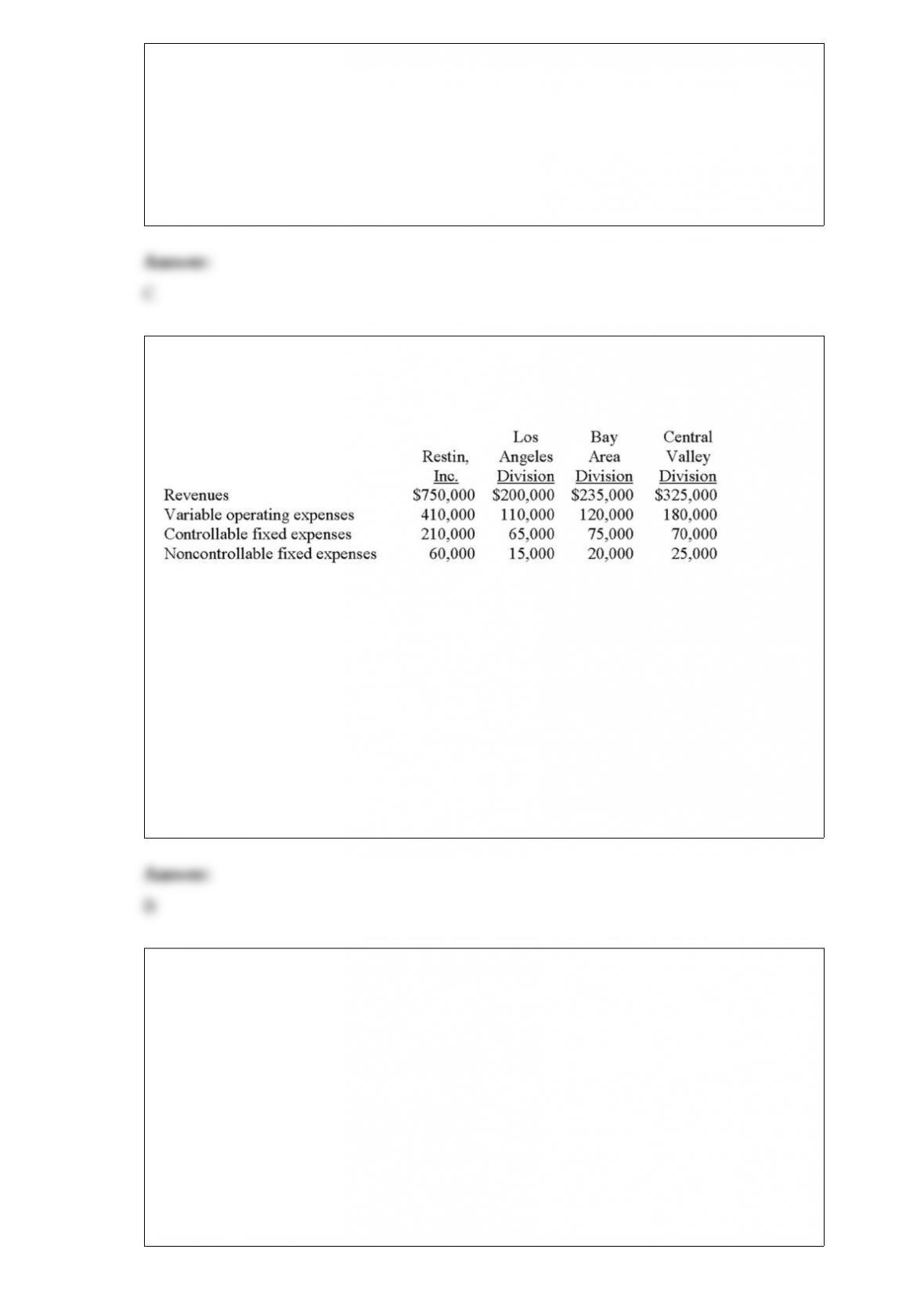

12) Willingham uses a process-costing system for its single product, which is

manufactured from Material X and Material Y. X and Y are introduced to the product as

follows:

Material X: Added at the beginning of manufacturing

Material Y: Added at the 75% stage of completion

The company started and completed 40,000 units during the period, and had an ending

work-in-process inventory amounting to 8,000 units, 20% complete. Which of the

following choices correctly expresses the total equivalent units of production for

Material X and Material Y?

A.Choice A

B.Choice B

C.Choice C

D.Choice D

E.Choice E

13) Yang Corporation recently computed total product costs of $567,000 and total

period costs of $420,000, excluding $35,000 of sales commissions that were overlooked

by the company’s administrative assistant. On the basis of this information, Yang’s

income statement should reveal operating expenses of:

A.$35,000

B.$420,000

C.$455,000

D.$567,000

E.$602,000

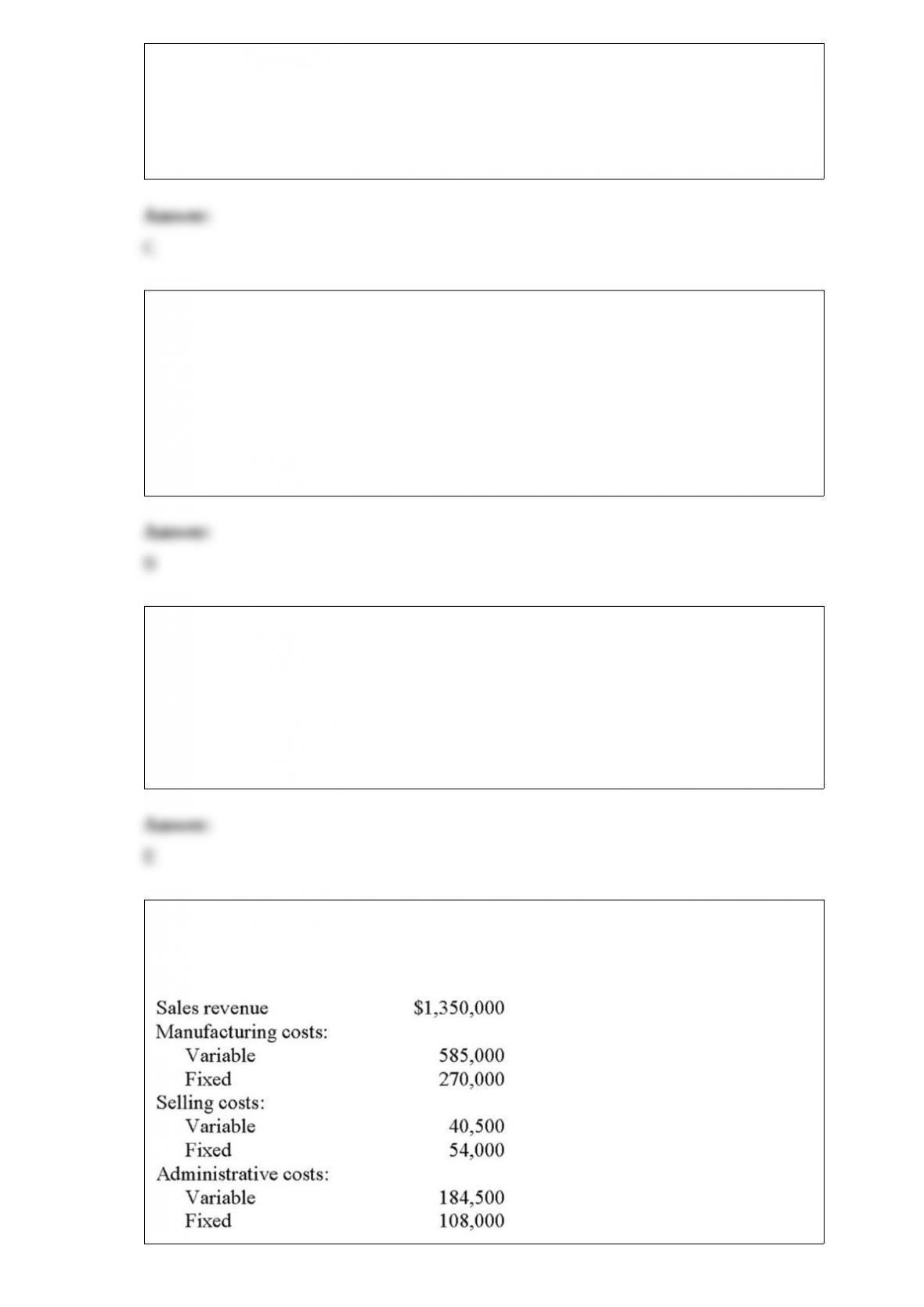

14) The following information was taken from the segmented income statement of

Restin, Inc., and the company’s three divisions:

In addition, the company incurred common fixed costs of $18,000.

Assume that the Los Angeles division increases its promotion expense, a controllable

fixed cost, by $10,000. As a result, revenues increased by $50,000. If variable expenses

are tied directly to revenues, the new Los Angeles segment contribution margin is:

A.$12,500

B.$22,500

C.$32,500

D.$50,000

E.$60,000

15) Isthmus Corporation uses the physical-units method to allocate costs among its

three joint products: X, Y, and Z. The following data are available for the period just

ended:

Joint processing cost: $800,000

Total production: 150,000 pounds

Share of joint cost allocated to X: $160,000

Share of joint cost allocated to Y: $400,000

Which of the following statements is true?

A.The company would have relied on the sales value of each product when allocating

joint costs to X, Y, and Z

B.Ithaca produced 30,000 pounds of Z during the period

C.Ithaca produced 45,000 pounds of Z during the period

D.Ithaca produced 105,000 pounds of Z during the period

E.Based on the data presented, it is not possible to determine Ithaca’s production of Z

during the period

16) A flexible budget for 15,000 hours revealed variable manufacturing overhead of

$90,000 and fixed manufacturing overhead of $120,000. The budget for 25,000 hours

would reveal total overhead costs of:

A.$210,000

B.$270,000

C.$290,000

D.$350,000

E.None of the other answers are correct

17) Economic value added:

A.is a dollar amount rather than a percentage

B.uses a firm’s weighted-average cost of capital

C.uses total assets in its computation and ignores current liabilities

D.cannot be negative

E.is both a dollar amount rather than a percentage and uses a firm’s weighted-average

cost of capital

18) Edmonco Company produced and sold 45,000 units of a single product last year,

with the following results:

Edmonco’s operating leverage factor was:

A.4

B.5

C.6

D.7

E.8

19) Wel-care Corporation operates a small medical lab in Nebraska that conducts minor

medical procedures (including blood tests and x-rays) for a number of doctors. The lab

consumes various medical supplies and is staffed by two technicians, both of whom are

paid a monthly salary. In addition, there is an on-site office manager who is also paid by

the month.

Required:

A. If the lab’s patient count increases by 15%, will the lab’s total operating costs

increase by 15%? Explain.

B. Wel-care is considering opening an additional lab in a new suburban medical

building. What will likely happen to the lab’s level of fixed cost incurrence? Why?

C. What analysis methods would be available to the office manager and/or Wel-care

management if a close look at the lab’s cost behavior is desired?

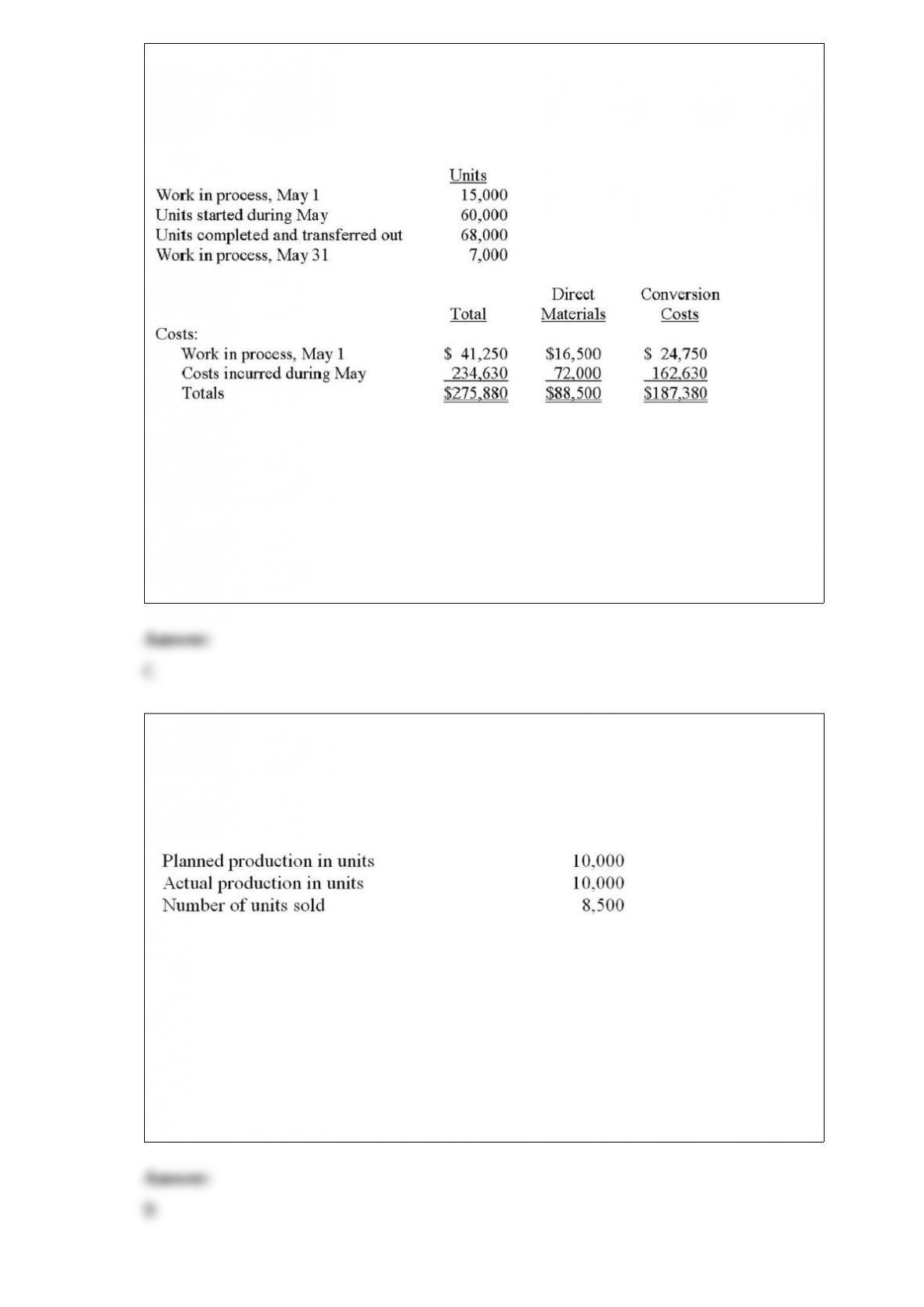

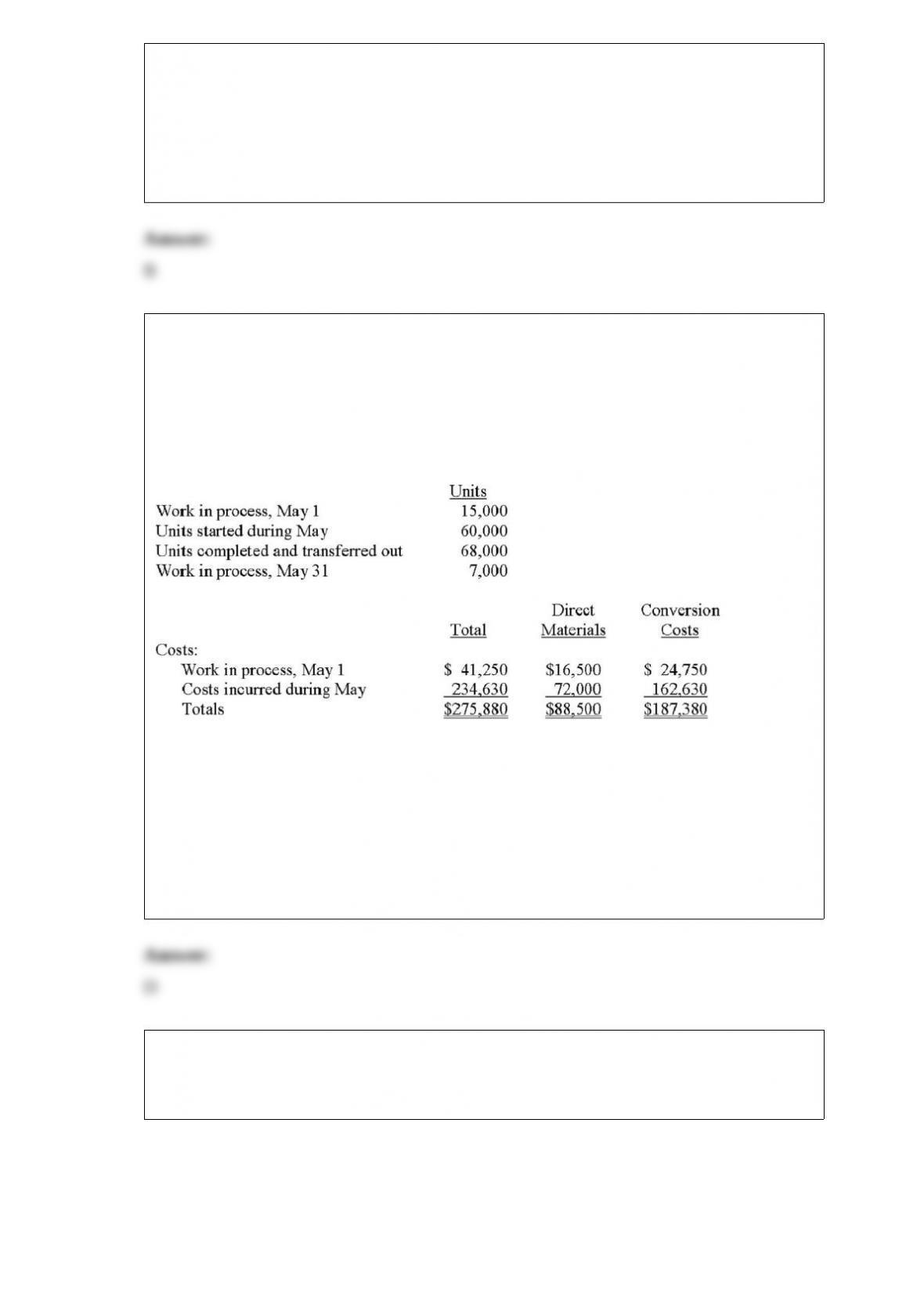

20) Southern Lake Chemical manufactures a product called Zubek. Direct materials are

added at the beginning of the process, and conversion activity occurs uniformly

throughout production. The beginning work-in-process inventory is 60% complete with

respect to conversion; the ending work-in-process inventory is 20% complete. The

following data pertain to May:

Using the weighted-average method of process costing, the equivalent units of

conversion activity total:

A.60,400

B.68,000

C.69,400

D.74,000

E.None of the answers is correct

21) Franz began business at the start of this year and had the following costs: variable

manufacturing cost per unit, $9; fixed manufacturing costs, $60,000; variable selling

and administrative costs per unit, $2; and fixed selling and administrative costs,

$220,000. The company sells its units for $45 each. Additional data follow.

There were no variances.

The income (loss) under variable costing is:

A.$(7,500)

B.$9,000

C.$15,000

D.$18,000

E.None of the other answers are correct

22) The income calculation for a division manager’s ROI should be based on:

A.divisional contribution margin

B.profit margin controllable by the division manager

C.profit margin traceable to the division

D.divisional income before interest and taxes

E.divisional net income

23) Southern Lake Chemical manufactures a product called Zubek. Direct materials are

added at the beginning of the process, and conversion activity occurs uniformly

throughout production. The beginning work-in-process inventory is 60% complete with

respect to conversion; the ending work-in-process inventory is 20% complete. The

following data pertain to May:

Using the weighted-average method of process costing, the cost of goods completed

and transferred during May is:

A.$249,560

B.$250,240

C.$258,400

D.$263,840

E.None of the answers is correct

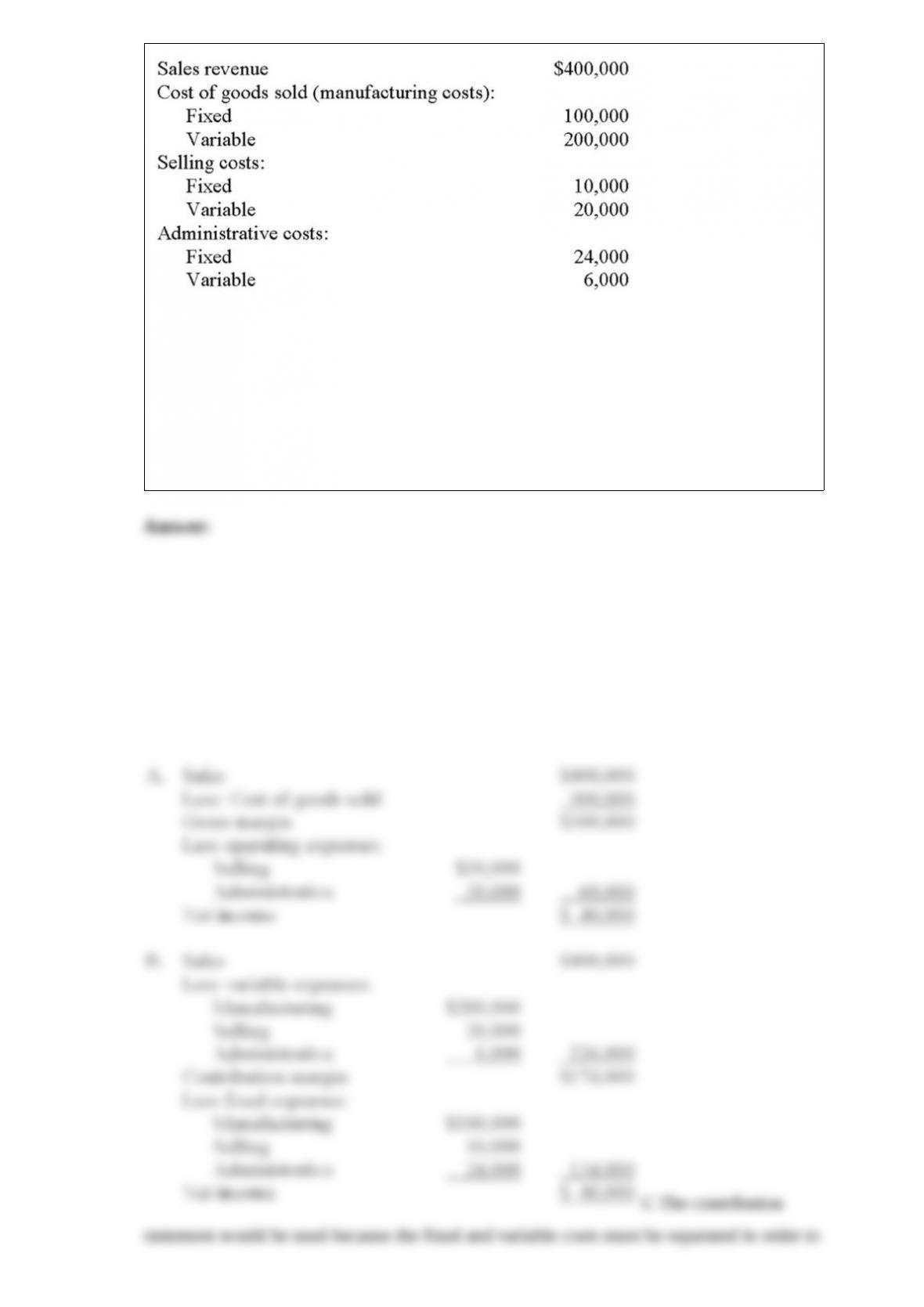

24) Brice Publications, Inc. produces and sells business books. The results of the

company’s operations for the year ended December 31, 20×1, are given below.

Required:

A. Prepare a traditional income statement for the company.

B. Prepare a contribution income statement for the company.

C. Which income statement (traditional or contribution) would an operating manager

most likely use to study changes in operating income that are caused by changes in

sales? Why?

25) Consider the following statements about budget administration:

I. The budgeting process is a very formal process in all organizations regardless of an

organization’s size.

II. The budget manual is prepared to communicate budget procedures and deadlines to

employees throughout an organization.

III. Effective internal control procedures require that the budget director be an

individual other than the controller.

Which of the above statements is (are) true?

A.I only

B.II only

C.III only

D.I and II

E.I and III

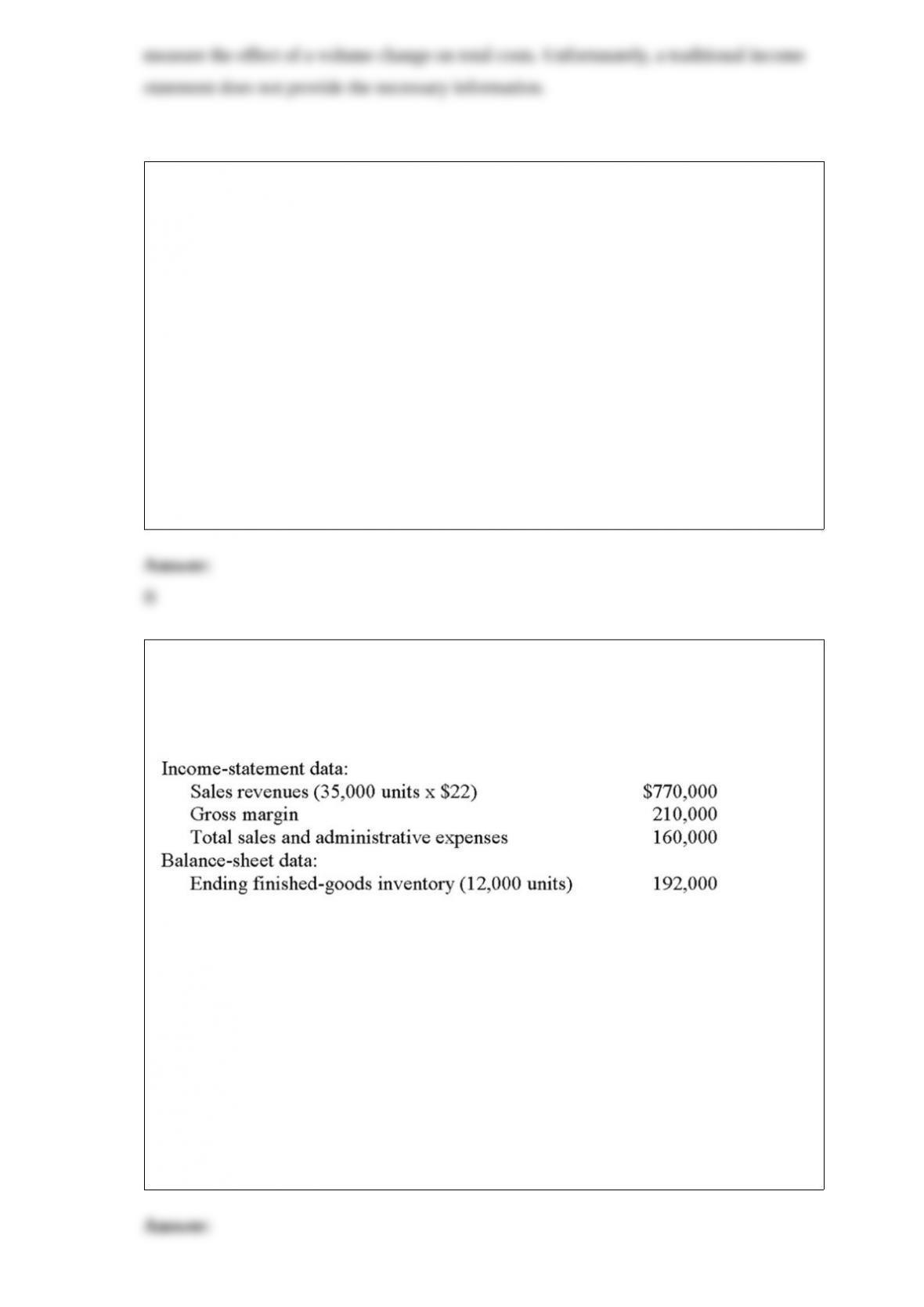

26) Kim, Inc. began business at the start of the current year and maintains its

accounting records on an absorption-cost basis. The following selected information

appeared on the company’s income statement and end-of-year balance sheet:

Kim achieved its planned production level for the year. The company’s fixed

manufacturing overhead totaled $141,000, and the firm paid a 10% commission based

on gross sales dollars to its sales force.

Required:

A. How many units did Kim plan to produce during the year?

B. How much fixed manufacturing overhead did the company apply to each unit

produced?

C. Compute Kim’s cost of goods sold.

D. How much variable cost did the company attach to each unit manufactured?

27) Lasley Corporation is considering the acquisition of a new machine that is expected

to produce annual savings in cash operating costs of $30,000 before income taxes. The

machine costs $100,000, has a useful life of five years, and no salvage value. Lasley

uses straight-line depreciation on all assets, is subject to a 30% income tax rate, and has

an after-tax hurdle rate of 8%.

Required:

A. Compute the machine’s accounting rate of return on the initial investment.

B. Compute the machine’s net present value.

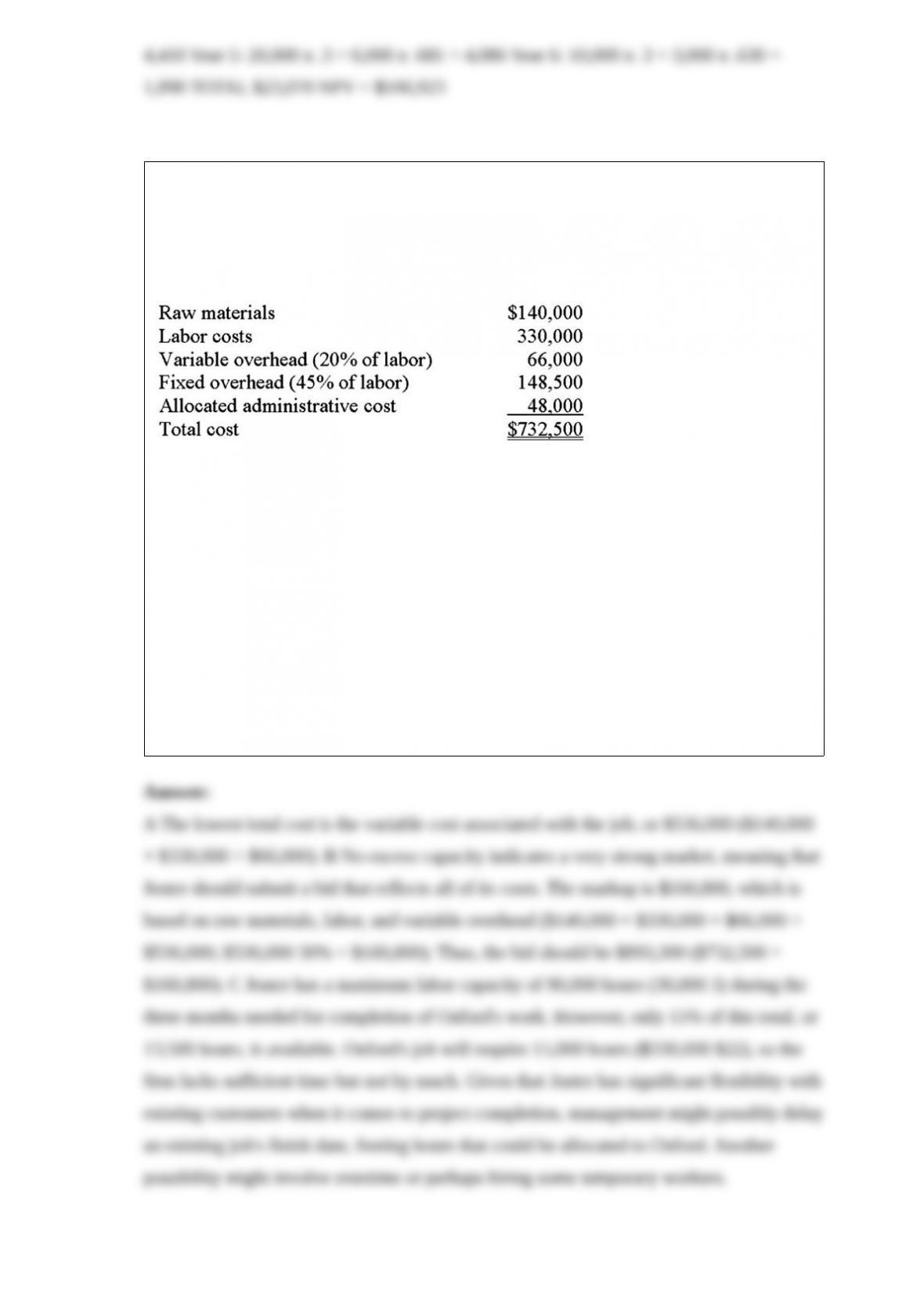

28) Joster Corporation, which has a maximum labor capacity of 30,000 hours per

month, has considerable flexibility with its customers when it comes to project

completion dates. Management is considering the submission of a bid for a job to be

performed for the city of Oxford. Costs for the job are as follows:

Joster’s labor force is paid an average of $22 per hour and if the company wins the bid,

it will have three months to complete the work. Management adds a 30% profit margin

to all jobs, computed on the basis of total variable cost.

Required:

A. Compute the lowest total cost that the company would use when figuring its bid,

assuming that Jester has excess capacity.

B. Compute Joster’s bid if the company has no excess capacity.

C. Assume that Joster is currently working at 85% of capacity. Does the firm have

sufficient time to complete the job? If not, what could the company do if it desires to do

business with Oxford?

29) Swansong plans to sell 10,000 units of a particular product during July, and expects

sales to increase at the rate of 10% per month during the remainder of the year. The

June 30 and September 30 ending inventories are anticipated to be 1,100 units and 950

units, respectively. On the basis of this information, how many units should Swansong

purchase for the quarter ended September 30?

A.31,850

B.32,150

C.32,950

D.33,250

E.None of the other answers are correct

30) Barnett, Inc., which uses a process-costing system, transfers completed production

from Department no. 1 to Department no. 2 for further work. Which of the following

best describes the account that would be credited to record this transfer?

A.Cost of Goods Transferred

B.Finished-Goods Inventory: Department no. 1

C.Finished-Goods Inventory: Department no. 2

D.Work-in-Process Inventory: Department no. 1

E.Work-in-Process Inventory: Department no. 2