1) After conducting a rate-sensitive analysis, a bank finds itself with the following

amounts of rate-sensitive assets and liabilities (RSAs and RSL) and fixed-rate assets

and liabilities (FRAs and FRLs); the rate of return and cost rates on the accounts are

also given:

If the bank wishes to set up a swap to totally hedge the interest rate risk, the bank

should

A.pay a variable rate of interest and receive a fixed rate of interest.

B.pay a fixed rate of interest and receive a variable rate of interest.

C.pay a variable rate of interest and receive a variable rate of interest.

D.pay a fixed rate of interest and receive a fixed rate of interest.

2) A bank has DA = 2.4 years and DL= 0.9 years. The bank has total equity of $82

million and total assets of $850 million. Interest rates are at 6 percent. To get DE to

equal zero to protect the equity value in the event of an interest rate change, the bank

could

A.reduce DA to 1.21 years.

B.increase DL to 2.44 years.

C.increase DL to 3.10 years.

D.reduce DA to zero.

E.increase DL to 2.76 years.

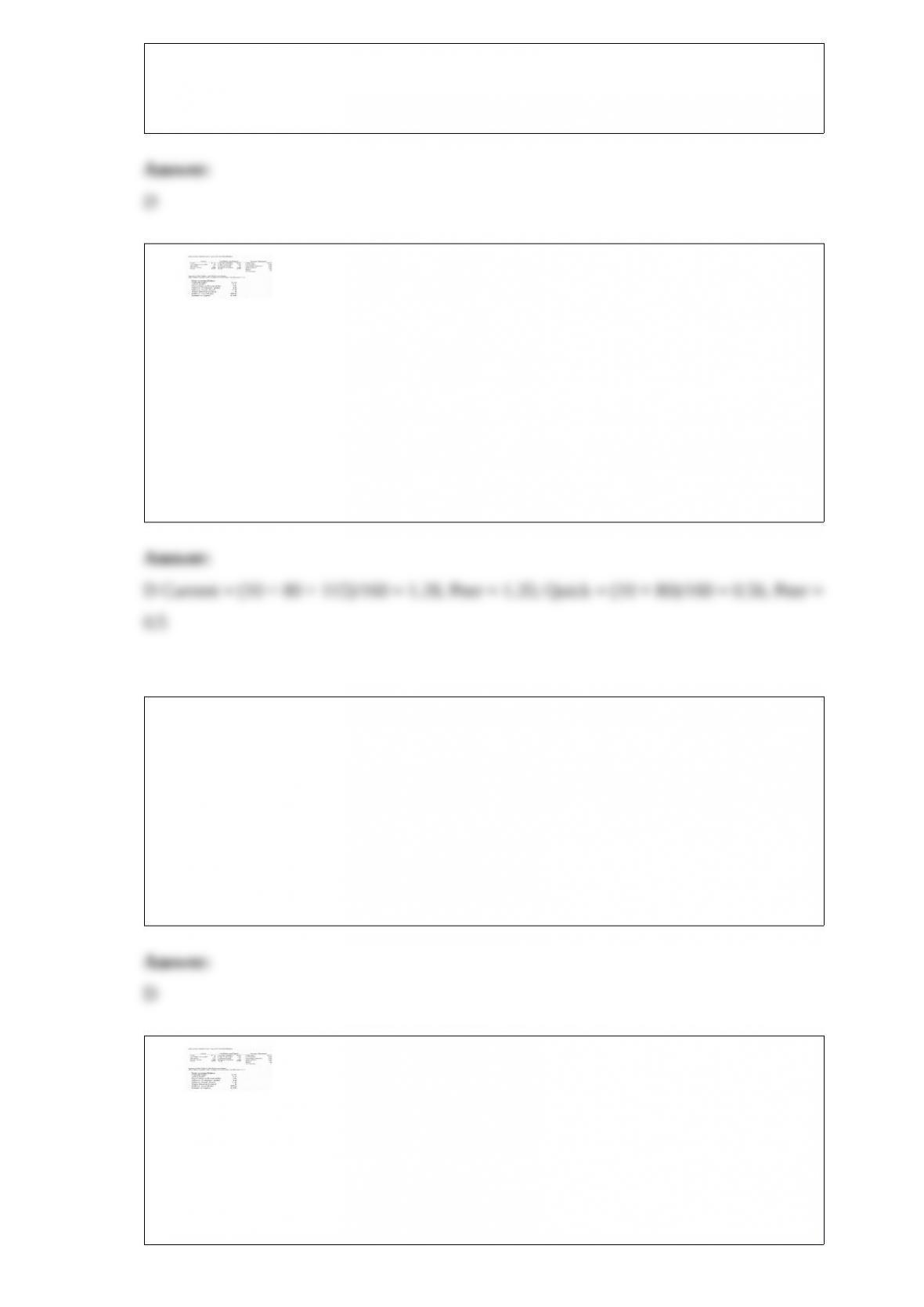

3) Big Valley is collecting their receivables about __________________ than the

typical firm.

A.22 percent more quickly

B.12 percent more quickly

C.17 percent more slowly

D.12 percent more slowly

4) Which of the following statements are true about a traditional IRA?

I. Subject to an income limit, in 2011 a single person could contribute up to $5,000 per

year of pretax income to an IRA.

II. All withdrawals are tax-free.

III. Earnings on the IRA account are not taxed until withdrawn.

IV. You must begin withdrawals at age 59 ½.

V. Withdrawal(s) can be a lump sum or installments.

A.I, II, IV

B.I, II, IV, and V

C.I, III, and V

D.II, IV, and V

E.III, IV, and V

5) The primary federal banks€ regulators have established guidelines for derivatives

usage at banks that includes the following:

I. Banks must establish internal guidelines regarding hedging activity.

II. Banks must establish trading limits.

III. Banks are prohibited from using derivatives to speculate.

IV. Banks must disclose large derivatives positions that may materially affect

stakeholders in their financial statements.

A.I and II only

B.I, III, and IV only

C.I, II, and IV only

D.II, III, and IV only

E.I, II, III, and IV

6)

Big Valley’s return on equity indicates that the firm generates a _____ return to their

shareholders than their peers.

A.3.02 percent higher

B.15.25 percent higher

C.5.75 percent lower

D.1.05 percent lower

E.2.04 percent higher

7) Areas of commercial bank regulation dealing with preventing banks from

discriminating unfairly in lending are termed ______________________ regulations.

rev: 10_17_2013_QC_37326

A.safety and soundness

B.consumer protection

C.investor protection

D.credit allocation

E.monetary policy

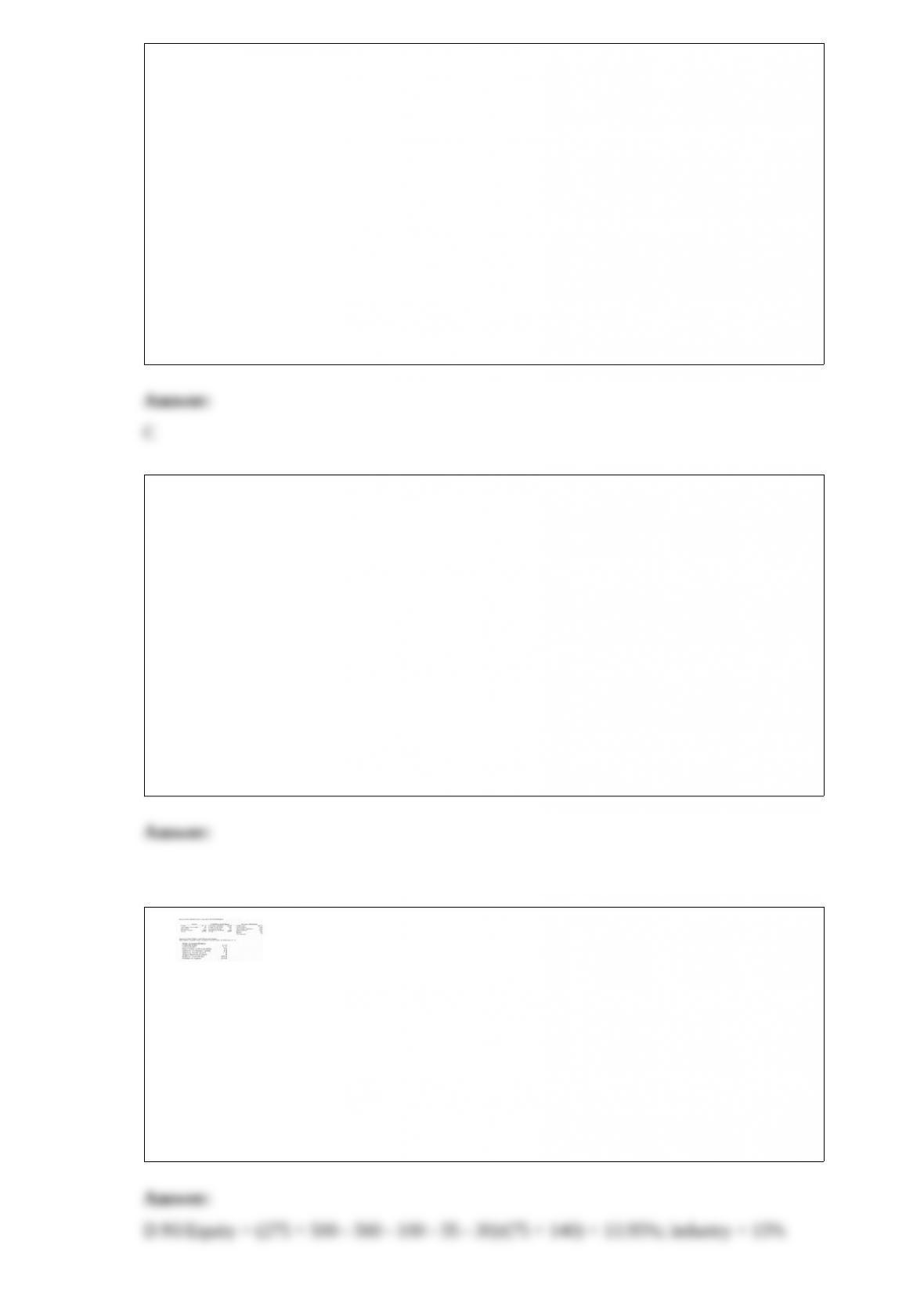

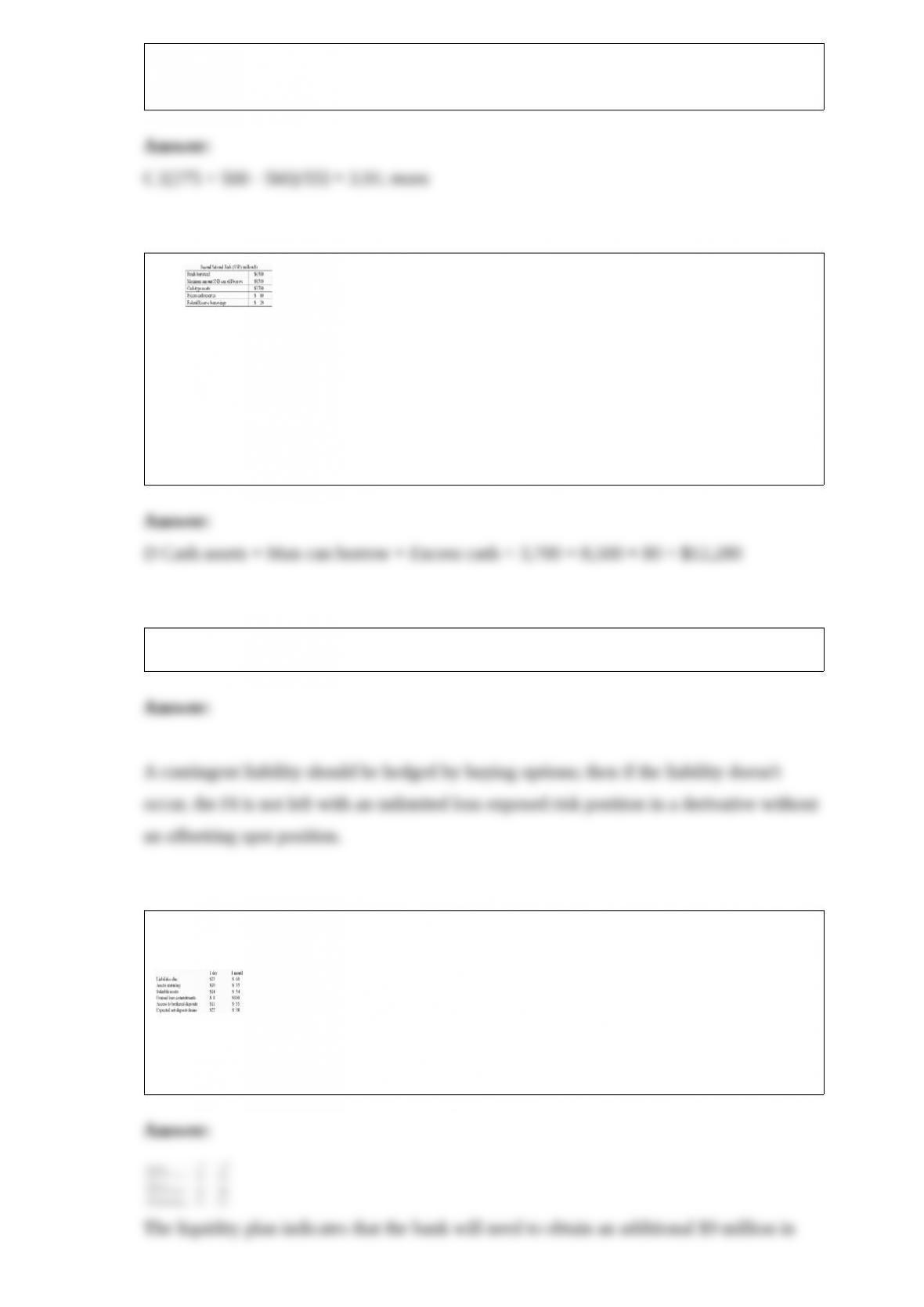

8)

What are Second National Bank’s total uses of liquidity?

A.$6,520

B.$13,500

C.$14,200

D.$12,280

E.$5,760

9) You own a mortgage-backed security and you will receive fixed semiannual interest

payments and no principal payments as long as prepayments remain within a given

range. If prepayments move outside the range, you will receive prepayments. You must

be holding a ______________________.

A.class C or lower sequential pay CMO

B.PAC CMO

C.PO security

D.pass-through security

E.CDO

10)

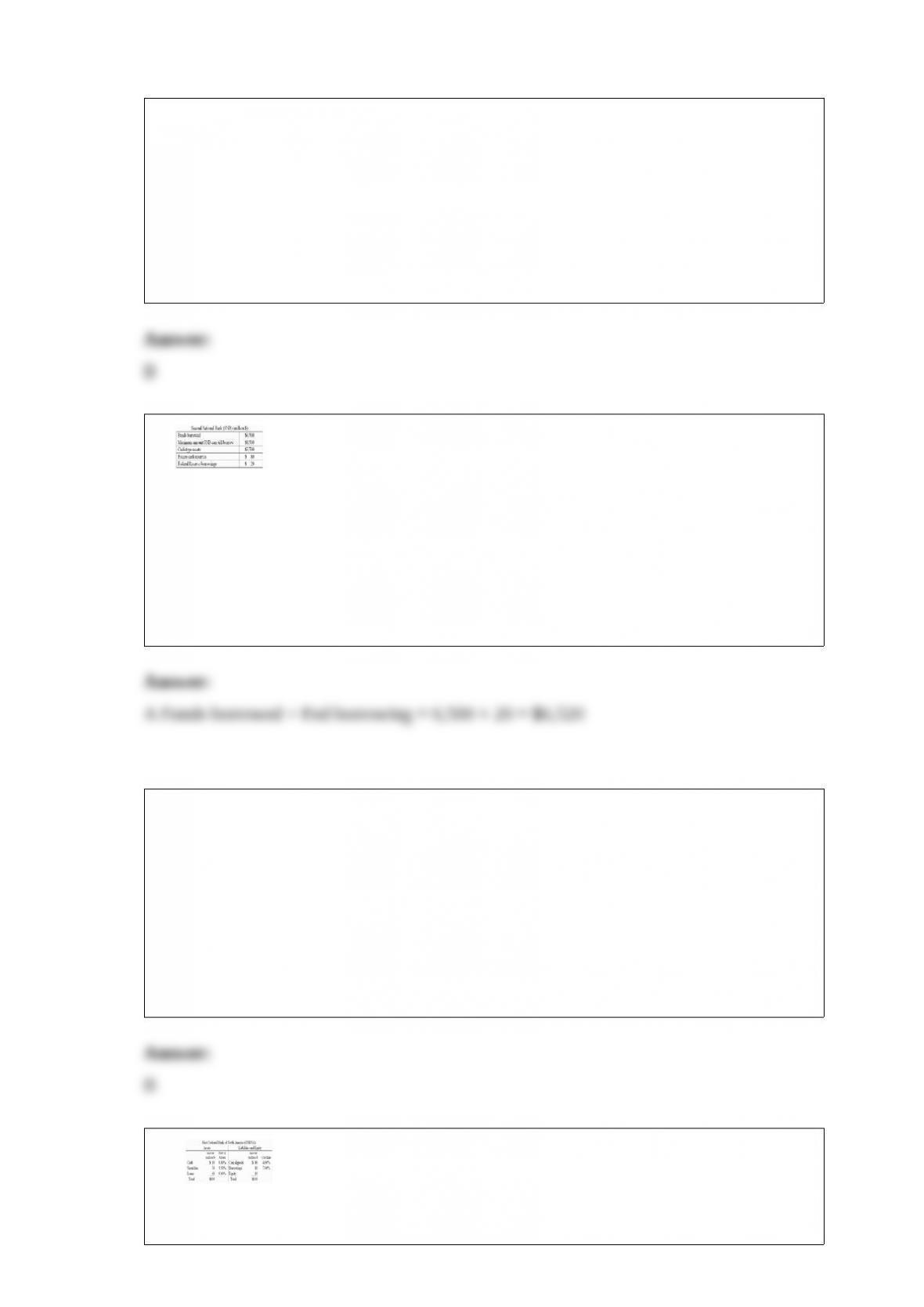

If FNBNA is expecting a $20 million net deposit drain and the bank wishes to fund the

drain by borrowing more money, how much will pretax net income change if the

borrowing cost is the same as on its existing borrowed funds?

A.$600,000

B.-$312,000

C.-$2,000,000

D.-$600,000

E.$312,000

11)

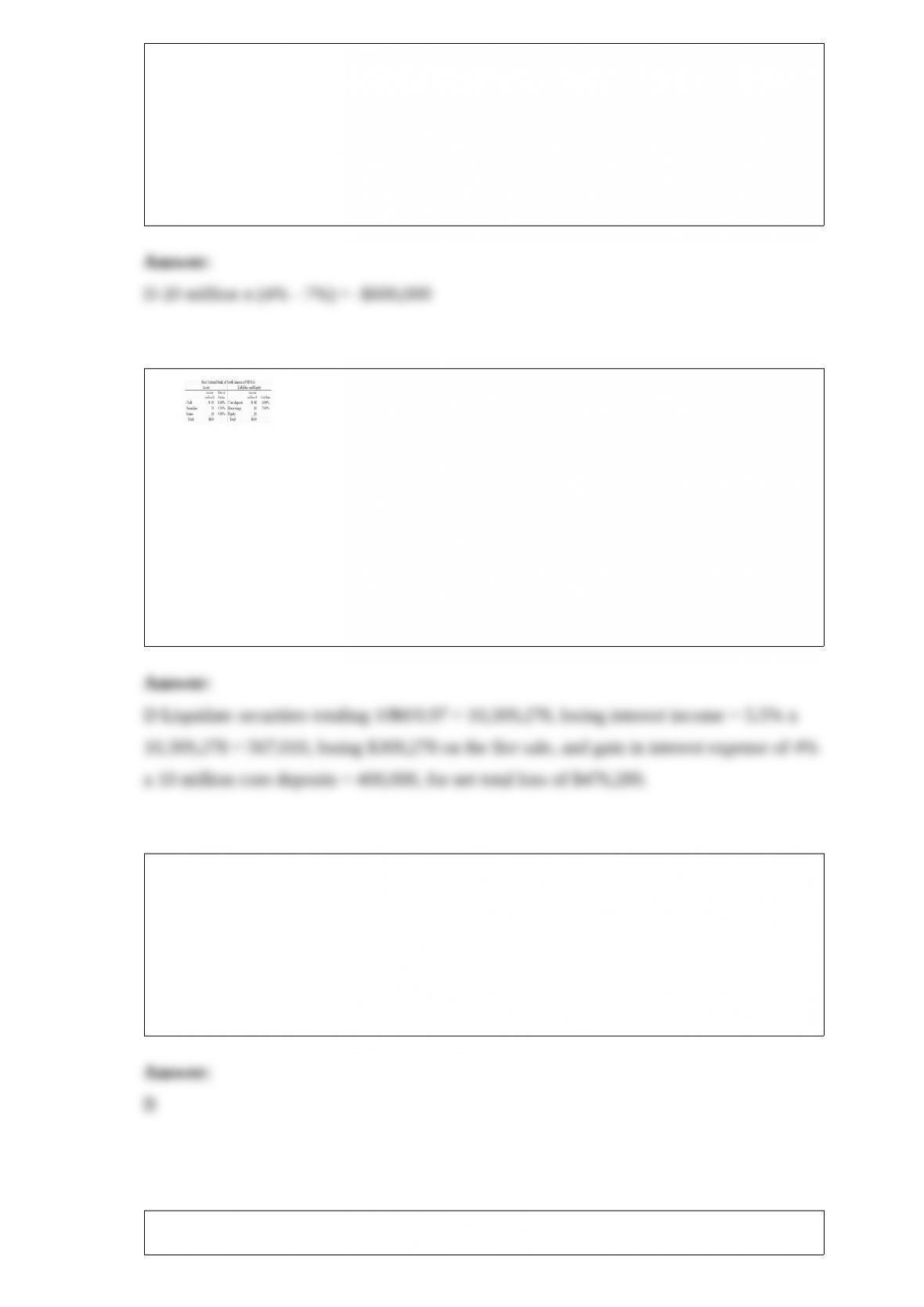

If FNBNA is expecting a $10 million net deposit drain and the securities liquidity index

is 0.97, by how much will pretax net income change if the drain is funded entirely

through securities sales?

A.-$306,122

B.-$150,000

C.-$375,339

D.-$476,289

E.-$474,490

12) The amount that a policyholder receives when he or she cashes in an insurance

policy is called the

A.cash value.

B.surrender value.

C.face value.

D.policy value.

E.fair market value.

13) A bank has on-balance-sheet assets with a book value of $940 million and a market

value of $985 million and on-balance-sheet liabilities with a book value of $900 million

and a market value of $930 million. The bank also has off-balance-sheet assets

currently valued at $150 million and off-balance-sheet liabilities worth $160 million.

Stockholders€ net worth should be valued at _________________ million.

A.$30

B.$40

C.$45

D.$50

E.$55

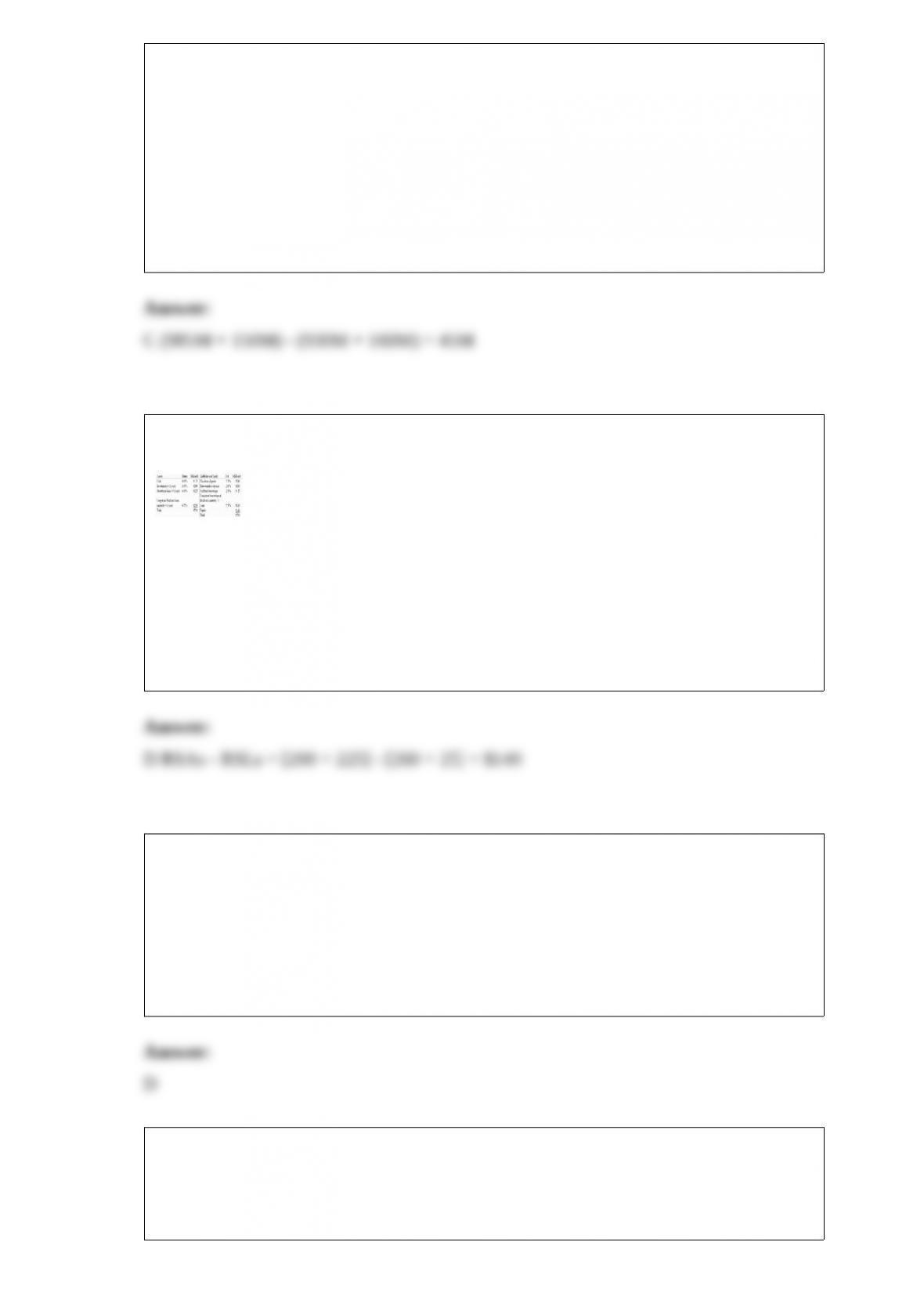

14) A bank has the following balance sheet:

The bank’s one-year repricing gap is (Million $)

A.$425.

B.$285.

C.$74.

D.$140.

E.$66.

15) In 2013, _______________ had on average the greatest amount of equity as a

percentage of assets and ______________ had the lowest.

A.savings institutions; credit unions

B.banks; credit unions

C.credit unions; finance companies

D.finance companies; credit unions

E.finance companies; banks

16) In the post-Depression era the largest number of bank failures occurred in which

time period?

A.1955€1965

B.1965€1975

C.1975€1985

D.1985€1995

E.1995€2005

17)

Big Valley’s current ratio indicates that Big Valley is ______ liquid than the typical firm

in the industry, and Big Valley’s quick ratio indicates that Big Valley is _______ liquid

than the typical firm.

A.more; more

B.more; less

C.less; less

D.less; more

E.similar; similar

18) A three-class sequential pay CMO has an initial principal balance of $50 million per

class. In the first month, interest payments of $5 million and principal payments of $2

million are received. In the second month, Class A holders receive interest on _____

principal and Class B holders receive interest on _____ principal.

A.$30 million; $30 million

B.$28 million; $28 million

C.$27 million; $27 million

D.$28 million; $30 million

E.$30 million; $28 million

19)

Big Valley has a times interest earned ratio that is _________, which indicates that Big

Valley has _________ long-term insolvency risk than the typical firm in the industry.

A.4; the same

B.3.91; less

C.3.91; more

D.4.58; more

E.4.58; less

20)

What are Second National Bank’s total sources of liquidity?

A.$6,520

B.$13,500

C.$14,200

D.$12,280

E.$5,760

21) Is it safer to hedge a contingent liability with options, futures, forwards, or swaps?

22) You have the following data for a bank (Million $):

Calculate the net funding requirement for each period and the cumulative net funding

requirement over the month. What does the plan reveal?

23) How sound is the PBGC? How much do firms pay for pension fund insurance?

Describe then-President Bush’s proposal to increase funding for PBGC.

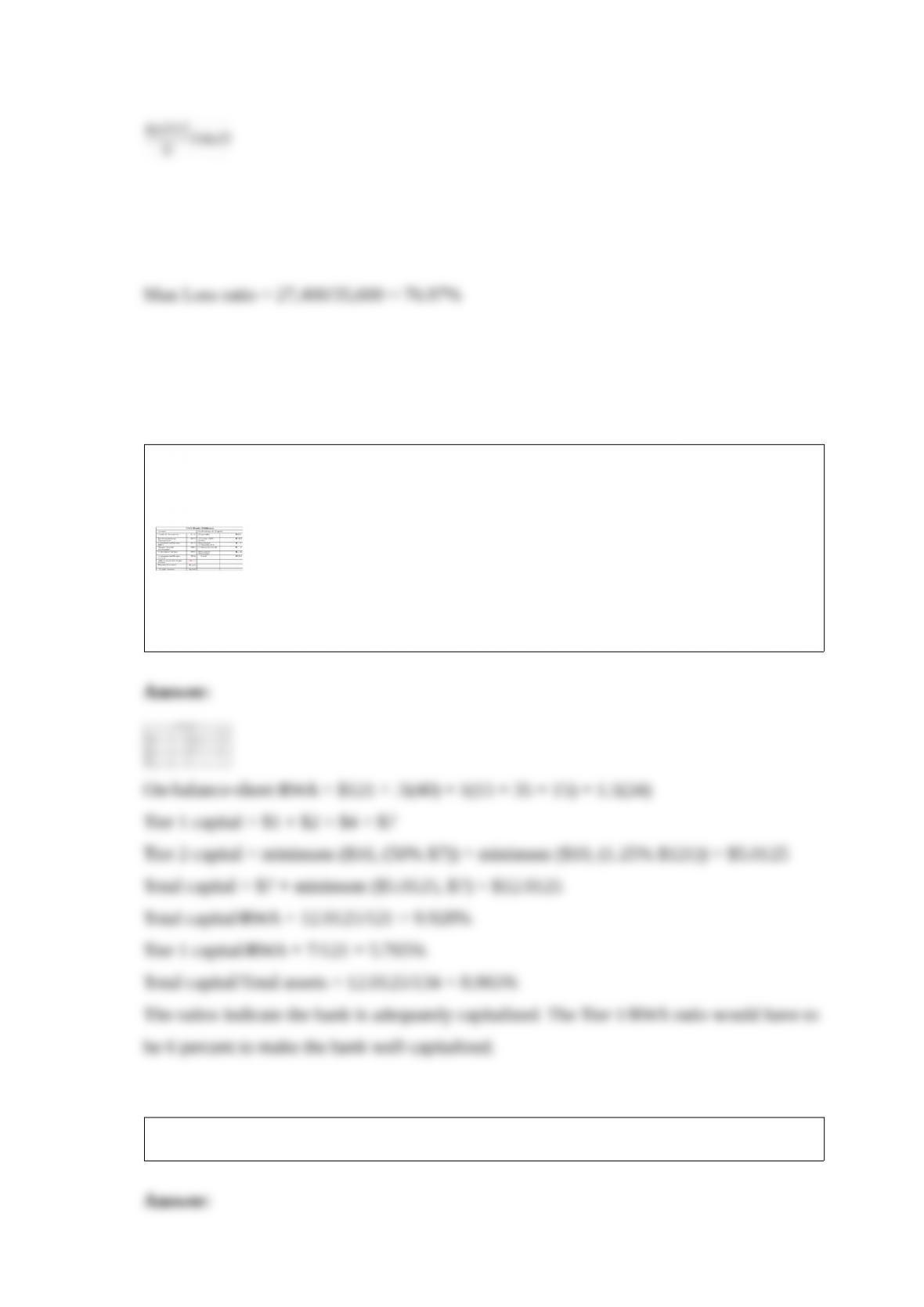

25) Look at the following simplified bank balance sheet. Assume that the bank has no

off-balance-sheet commitments.

Using the three capital adequacy ratios, determine if the bank is well-capitalized,

adequately capitalized, undercapitalized, significantly undercapitalized, or critically

undercapitalized.