Psychologists have found that people who make decisions that turn out badly blame

themselves more when that decision was unconventional. The name for this

phenomenon is

A. regret avoidance.

B. framing.

C. mental accounting.

D. overconfidence.

E. obnoxicity.

You are considering investing $1,000 in a T-bill that pays 0.05 and a risky portfolio, P,

constructed with two

risky securities, X and Y. The weights of X and Y in P are 0.60 and 0.40, respectively. X

has an expected rate

of return of 0.14 and variance of 0.01, and Y has an expected rate of return of 0.10 and a

variance of 0.0081.

If you want to form a portfolio with an expected rate of return of 0.11, what percentages

of your money must

you invest in the T-bill and P, respectively?

A. 0.25; 0.75

B. 0.19; 0.81

C. 0.65; 0.35

D. 0.50; 0.50

E. Cannot be determined.

Which pricing model provides no guidance concerning the determination of the risk

premium on factor portfolios?

A. The CAPM

B. The multifactor APT

C. Both the CAPM and the multifactor APT

D. Neither the CAPM nor the multifactor APT

E. None of the options are correct.

You purchase a share of Boeing stock for $90. One year later, after receiving a dividend

of $3, you sell the

stock for $92. What was your holding-period return?

A. 4.44%

B. 2.22%

C. 3.33%

D. 5.56%

E. None of the options are correct.

________ is equal to the total market value of the firm’s common stock divided by (the

replacement cost of the firm’s assets less liabilities).

A. Book value per share

B. Liquidation value per share

C. Market value per share

D. Tobin’s Q

E. None of the options are correct.

In the results of the earliest estimations of the security market line by Miller and

Scholes (1972), it was found that the average difference between a stock’s return and

the risk free rate was ________ to its beta.

A. positively related

B. negatively related

C. unrelated

D. inversely related

E. not proportional

When assessing tail risk by looking at the 5% worst-case scenario, the VaR is the

A. most realistic, as it is the most complete measure of risk.

B. most pessimistic, as it is the most complete measure of risk.

C. most optimistic, as it is the most complete measure of risk.

D. most optimistic, as it takes the highest return (smallest loss) of all the cases.

A put option allows the holder to

A. buy the underlying asset at the strike price on or before the expiration date.

B. sell the underlying asset at the strike price on or before the expiration date.

C. sell the option in the open market prior to expiration.

D. sell the underlying asset at the strike price on or before the expiration date and sell

the option in the open market prior to expiration.

E. buy the underlying asset at the strike price on or before the expiration date and sell

the option in the open market prior to expiration.

Alex Goh is 39 years old and has accumulated $128,000 in his selfdirected defined

contribution pension plan. Each year he contributes $2,500 to the plan, and his

employer contributes an equal amount. Alex thinks he will retire at age 62 and figures

he will live to age 86. The plan allows for two types of investments. One offers a 4%

riskfree real rate of return. The other offers an expected return of 11% and has a

standard deviation of 37%. Alex now has 25% of his money in the riskfree investment

and 75% in the risky investment. He plans to continue saving at the same rate and keep

the same proportions invested in each of the investments. His salary will grow at the

same rate as inflation. Of the total amount of new funds that will be invested by Alex

and by his employer on his behalf, how much will Alex put into the safe account each

year; how much into the risky account?

A. $2,500; $2,500

B. $3,200; $1,800

C. $3,000; $2,000

D. $1,250; $3,750

E. $2,400; $2,600

If a person gives too much weight to recent information compared to prior beliefs, they

would make ________ errors.

A. framing

B. selection bias

C. overconfidence

D. conservatism

E. forecasting

Higher dividend-payout policies have a __________ impact on the value of the call and

a __________ impact on the value of the put compared to lower dividend-payout

policies.

A. negative; negative

B. positive; positive

C. positive; negative

D. negative; positive

E. zero; zero

Targetdate retirement funds

A. are funds of funds diversified across stocks and bonds.

B. are inappropriate for most investors.

C. have very high fees.

D. function much like hedge funds.

The security characteristic line (SCL)

A. plots the excess return on a security as a function of the excess return on the market.

B. allows one to estimate the beta of the security.

C. allows one to estimate the alpha of the security.

D. All of the options.

E. None of the options are correct.

The pure yield curve can be estimated

A. by using zero-coupon Treasuries.

B. by using stripped Treasuries if each coupon is treated as a separate “zero.”

C. by using corporate bonds with different risk ratings.

D. by estimating liquidity premiums for different maturities.

E. by using zero-coupon Treasuries and by using stripped Treasuries if each coupon is

treated as a separate “zero.”

The pure yield curve is calculated using stripped or zero-coupon Treasuries.

The line representing all combinations of portfolio expected returns and standard

deviations that can be

constructed from two available assets is called the

A. risk/reward tradeoff line.

B. capital allocation line.

C. efficient frontier.

D. portfolio opportunity set.

E. Security Market Line.

Holding other factors constant, the interest-rate risk of a coupon bond is lower when the

bond’s

A. term to maturity is lower.

B. coupon rate is higher.

C. yield to maturity is higher.

D. term to maturity is lower and coupon rate is higher.

E. All of the options are correct.

Assume you sell short 100 shares of common stock at $45 per share, with initial margin

at 50%. What would be your rate of return if you repurchase the stock at $40 per share?

The stock paid no dividends during the period, and you did not remove any money from

the account before making the offsetting transaction.

A. 20.03%

B. 25.67%

C. 22.22%

D. 77.46%

Which of the following factors might affect stock returns?

A. the business cycle

B. interest rate fluctuations

C. inflation rates

D. All of the options.

Sure Tool Company is expected to pay a dividend of $2 in the upcoming year. The

risk-free rate of return is 4%, and the expected return on the market portfolio is 14%.

The beta of Sure Tool Company’s stock is 1.25.

If Sure’s intrinsic value is $21.00 today, what must be its growth rate?

A. 0.0%

B. 10%

C. 4%

D. 6%

E. 7%

What happens to an option if the underlying stock has a 3-for-1 split?

A. There is no change in either the exercise price or in the number of options held.

B. The exercise price will adjust through normal market movements; the number of

options will remain the same.

C.The exercise price would become one-third of what it was, and the number of options

held would triple.

D. The exercise price would triple, and the number of options held would triple.

E. There is no standard rule— each corporation has its own policy.

Two firms, C and D, both produce coat hangers. The price of coat hangers is $1.20

each. Firm C has total fixed costs of $750,000 and variable costs of 30 per coat hanger.

Firm D has total fixed costs of $400,000 and variable costs of 50 per coat hanger. The

corporate tax rate is 40%. If the economy is strong, each firm will sell 2,000,000 coat

hangers. If the economy enters a recession, each firm will sell 1,400,000 coat hangers.

If the economy is strong, the total cost of firm C will be

A. $1,680,000.

B. $1,170,000.

C.-$1,350,000.

D. $420,000.

In a futures contract, the futures price is

A. determined by the buyer and the seller when the delivery of the commodity takes

place.

B. determined by the futures exchange.

C. determined by the buyer and the seller when they initiate the contract.

D. determined independently by the provider of the underlying asset.

E. None of the options are correct.

Two firms, C and D, both produce coat hangers. The price of coat hangers is $1.20

each. Firm C has total fixed costs of $750,000 and variable costs of 30 per coat hanger.

Firm D has total fixed costs of $400,000 and variable costs of 50 per coat hanger. The

corporate tax rate is 40%. If the economy is strong, each firm will sell 2,000,000 coat

hangers. If the economy enters a recession, each firm will sell 1,400,000 coat hangers.

If the economy enters a recession, the tax of firm C will be

A. $1,680,000.

B. $750,000.

C. $510,000.

D.-$204,000.

What best explains why a firm’s ratio of long-term debt/total capital is lower than the

industry average, while the ratio of income before interest and taxes/debt interest

charges is higher than the industry average?

A. The firm pays lower interest on long-term debt than the average firm.

B. The firm has more short-term debt than average.

C. The firm has a high ratio of current assets/current liabilities.

D. The firm has a high ratio of total cash flow/long term debt.

E. None of the options are correct.

The current market price of a share of CAT stock is $76. If a put option on this stock

has a strike price of $80, the put

A. is out of the money.

B. is in the money.

C. can be exercised profitably.

D. is out of the money and can be exercised profitably.

E.is in the money and can be exercised profitably.

You sold one oil future contract at $70 per barrel. What would be your profit (loss) at

maturity if the oil spot price at that time is $73.12 per barrel? Assume the contract size

is 1,000 barrels and there are no transactions costs.

A. $3.12 profit

B. $31.20 profit

C. $3.12 loss

D. $31.20 loss

E. None of the options are correct.

Assume that stock market returns do not resemble a single-index structure. An

investment fund analyzes 150 stocks in order to construct a mean-variance efficient

portfolio constrained by 150 investments. They will need to calculate _____________

expected returns and ___________ variances of returns.

A. 150; 150

B. 150; 22500

C. 22500; 150

D. 22500; 22500

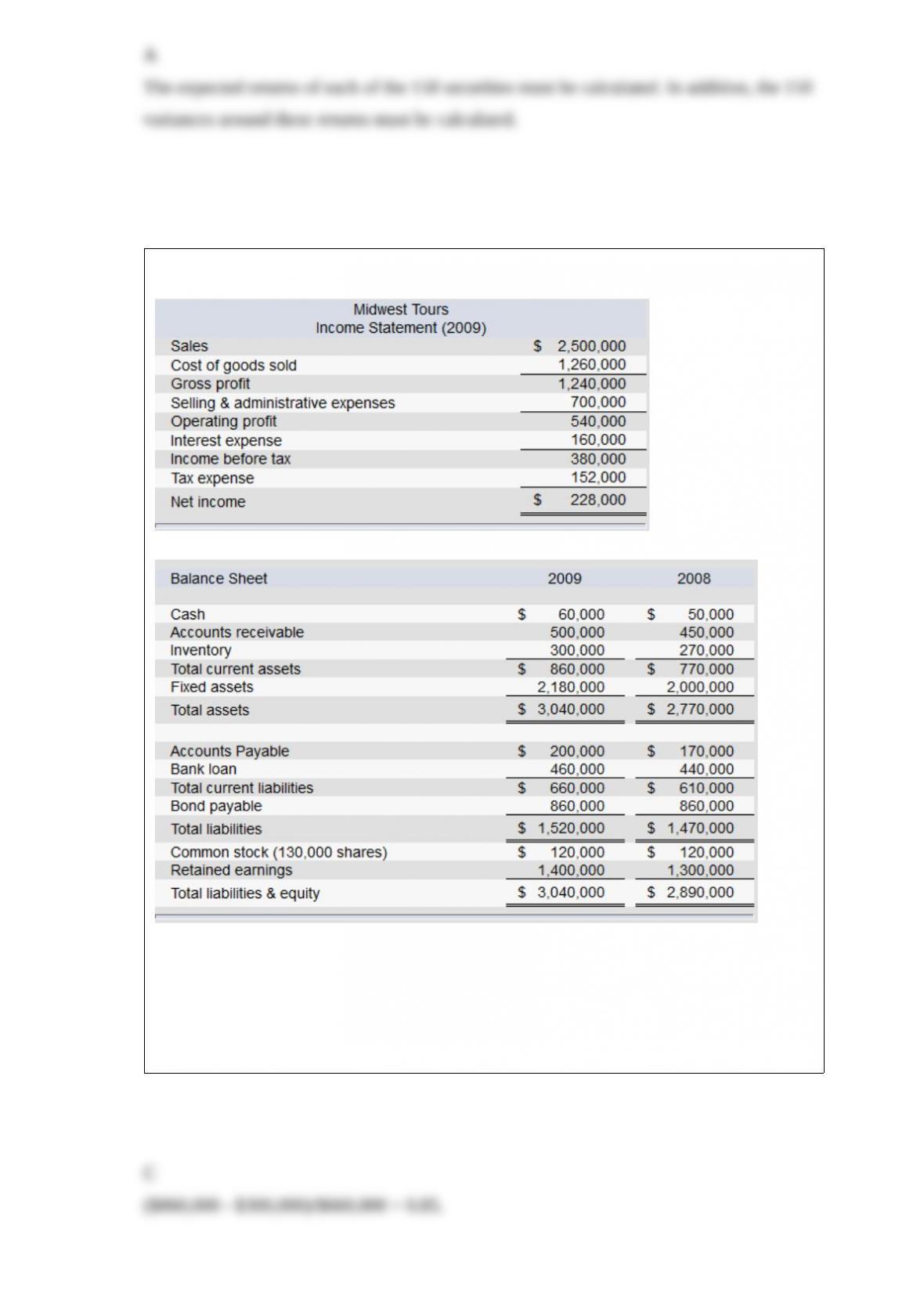

The financial statements of Midwest Tours are given below.

Note: The common shares are trading in the stock market for $36 each.

Refer to the financial statements of Midwest Tours. The firm’s quick ratio for 2009 is

A. 1.71.

B. 0.78.

C. 0.85.

D. 1.56.

Suppose you held a well-diversified portfolio with a very large number of securities,

and that the single index model holds. If the σ of your portfolio was 0.24 and σM was

0.18, the β of the portfolio would be approximately

A. 0.64.

B. 1.33.

C. 1.25.

D. 1.56.

Suppose that you purchased a call option on the S&P 100 Index. The option has an

exercise price of 1,700, and the index is now at 1,760. What will happen when you

exercise the option?

A. You will have to pay $6,000.

B.You will receive $6,000.

C. You will receive $1,700.

D. You will receive $1,760.

E. You will have to pay $7,000.

A single-index model uses __________ as a proxy for the systematic risk factor.

A. a market index, such as the S&P 500

B. the current account deficit

C. the growth rate in GNP

D. the unemployment rate.

Use the two-state put-option value in this problem. SO = $100; X = $120; the two

possibilities for ST are $150 and $80. The range of P across the two states is _____, and

the hedge ratio is _______.

A. $0 and $40; −4/7

B. $0 and $50; +4/7

C. $0 and $40; +4/7

D. $0 and $50; −4/7

E. $20 and $40; +1/2

Given the capital allocation line, an investor’s optimal portfolio is the portfolio that

A. maximizes her expected profit.

B. maximizes her risk.

C. minimizes both her risk and return.

D. maximizes her expected utility.

E. None of the options are correct.

Taxation of futures trading gains and losses

A.is based on cumulative year-end profits or losses.

B. occurs based on the date contracts are sold or closed.

C. can be timed to offset stock-portfolio gains and losses.

D. is based on the contract holding period.

E. None of the options are correct.

An investor invests 40% of his wealth in a risky asset with an expected rate of return of

0.

Morningstar’s RAR method

I) is one of the most widely-used performance measures.

II) indicates poor performance by placing up to 5 darts next to the fund’s name.

III) computes fund returns adjusted for loads. IV) computes fund returns adjusted for

risk.

V) produces ranking results that are the same as those produced with the Sharpe

measure.

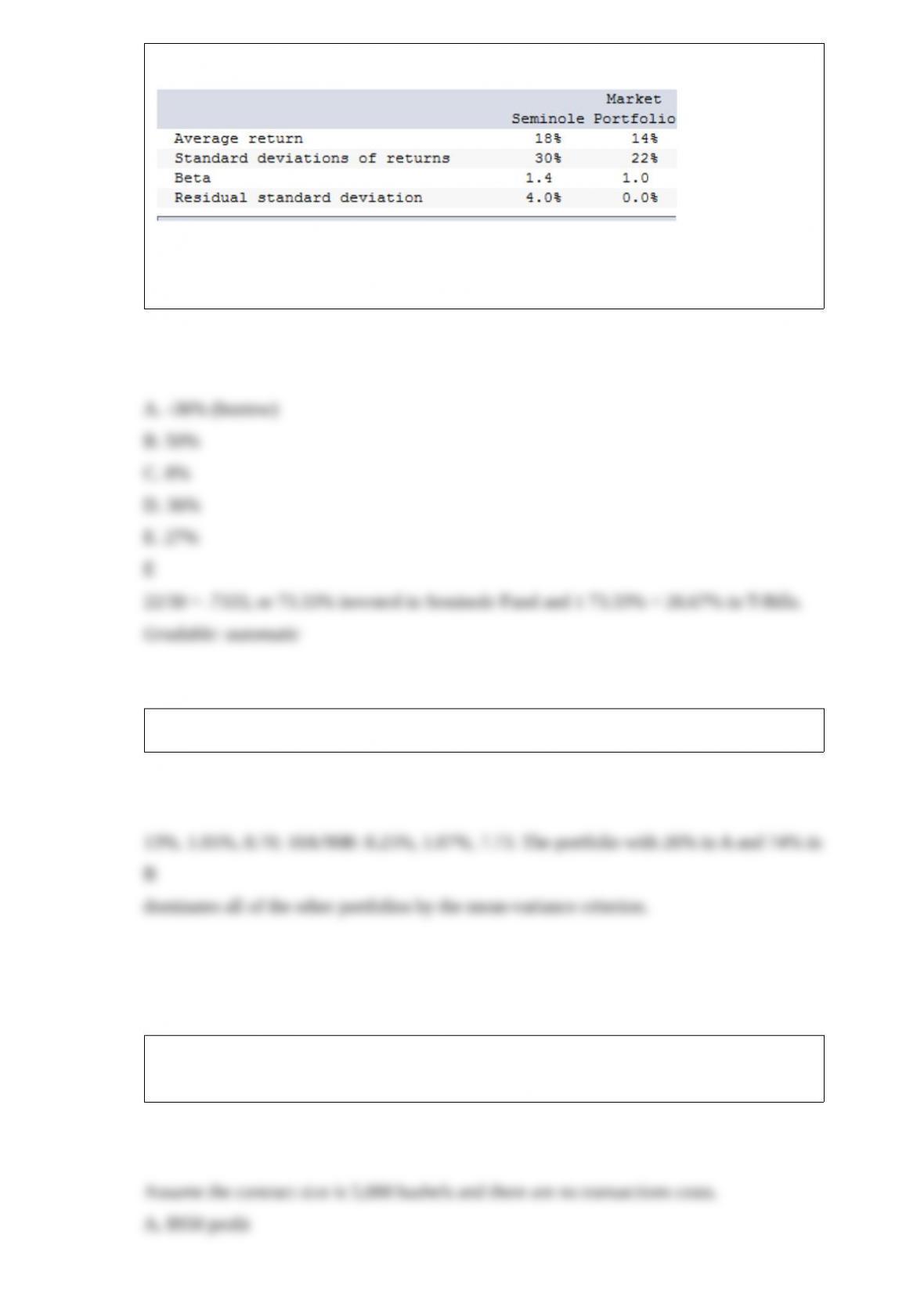

The following data are available relating to the performance of Seminole Fund and the

market portfolio:

The risk-free return during the sample period was 6%.

If you wanted to evaluate the Seminole Fund using the M2 measure, what percent of the

adjusted portfolio would need to be invested in T-Bills?

07; 26A/74B: 9.

You sold one corn future contract at $2.29 per bushel. What would be your profit (loss)

at maturity if the corn spot price at that time were $2.10 per bushel?

You sold one soybean future contract at $5.13 per bushel. What would be your profit

(loss) at maturity if the wheat spot price at that time were $5.26 per bushel?

Assume the contract size is 5,000 bushels and there are no transactions costs.

A. $65 profit

B. $650 profit

C. $650 loss

D. $65 loss

An investor invests 40% of his wealth in a risky asset with an expected rate of return of

0.17 and a variance of

0.08 and 60% in a T-bill that pays 4.5%. His portfolio’s expected return and standard

deviation are __________

and __________, respectively.

A. 0.114; 0.126

B. 0.087; 0.068

C. 0.095; 0.113

D. 0.087; 0.124

E. None of the options are correct.

An investor invests 35% of his wealth in a risky asset with an expected rate of return of

0.18 and a variance of

0.10 and 65% in a T-bill that pays 4%. His portfolio’s expected return and standard

deviation are __________

and __________, respectively.

A. 0.089; 0.111

B. 0.087; 0.063

C. 0.096; 0.126

D. 0.087; 0.144

08 = x(0.

On April 1, you sold one S&P 500 Index futures contract at a futures price of 1,550. If,

on June 15, the futures price was 1,612, what would be your profit (loss) if you closed

your position (without considering transactions costs)?

A. $1,550 loss

B. $15,550 loss

C. $15,550 profit

D. $1,550 profit

Some of the newer futures contracts include

I) fashion futures.

II) weather futures.

III) electricity futures.

IV) entertainment futures.

A. I and II

B. II and III

C. III and IV

D. I, II, and III

E. I, III, and IV

On January 1, you sold one April S&P 500 Index futures contract at a futures price of

1,420. If, on February 1, the April futures price was 1,430, what would be your profit

(loss) if you closed your position (without considering transactions costs)?

A. $2,500 loss

B. $10 loss

C. $2,500 profit

D. $10 profit