An American-style call option with six months to maturity has a strike price of $35. The

underlying stock now sells for $43. The call premium is $12. If the company

unexpectedly announces it will pay its first-ever dividend three months from today, you

would expect that

A. the call price would increase.

B. the call price would decrease.

C. the call price would not change.

D. the put price would decrease.

E. the put price would not change.

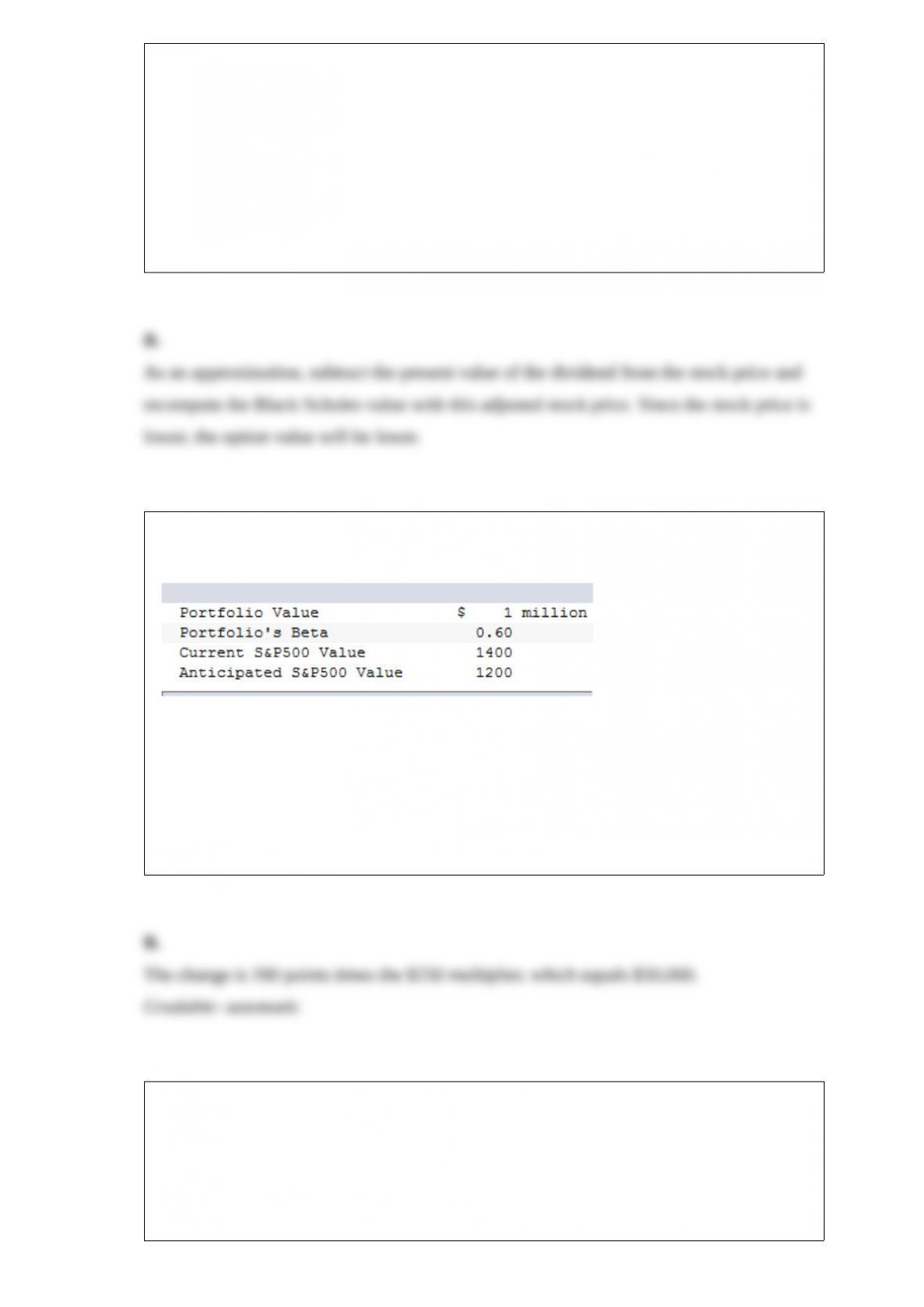

You are given the following information about a portfolio you are to manage. For the

long term, you are bullish, but you think the market may fall over the next month.

For a 200-point drop in the S&P 500, by how much does the value of the futures

position change?

A. $200,000

B. $50,000

C. $250,000

D. $500,000

E. $100,000

Liquidity is

A. the ease with which an asset can be sold.

B. the ability to sell an asset for a fair price.

C. the degree of inflation protection an asset provides.

D. the ease with which an asset can be sold and the ability to sell an asset for a fair

price.

E. All of the options are correct.

The feedback phase of the CFA Institute’s investment management process

A. uses data about the client and capital market.

B. uses details of optimal asset allocation and security selection.

C. uses changes in expectations and objectives.

D. All of the options are correct.

E. None of the options are correct.

Imposing the no-arbitrage condition on a single-factor security market implies which of

the following statements?

I) The expected return-beta relationship is maintained for all but a small number of

well-diversified portfolios.

II) The expected return-beta relationship is maintained for all well-diversified

portfolios.

III) The expected return-beta relationship is maintained for all but a small number of

individual securities.

IV) The expected return-beta relationship is maintained for all individual securities.

A. I and III

B. I and IV

C. II and III

D. II and IV

E. Only I is correct.

According to the Capital Asset Pricing Model (CAPM), a well diversified portfolio’s

rate of return is a function

Of

A. market risk.

B. unsystematic risk.

C. unique risk.

D. reinvestment risk.

E. None of the options are correct.

A coupon bond that pays interest annually has a par value of $1,000, matures in eight

years, and has a yield to maturity of 9%. The intrinsic value of the bond today will be

______ if the coupon rate is 6%.

A. $833.96

B. $620.92

C. $1,123.01

D. $886.28

E. $1,000.00

The APT was developed in 1976 by

A. Lintner.

B. Modigliani and Miller.

C. Ross.

D. Sharpe.

In order for you to be indifferent between the after-tax returns on a corporate bond

paying 7% and a tax-exempt municipal bond paying 5.5%, what would your tax bracket

need to be?

A. 22.6%

B. 21.4%

C. 26.2%

D. 19.8%

E. Cannot be determined from the information given.

Which one of the following statements regarding orders is false?

A. A market order is simply an order to buy or sell a stock immediately at the prevailing

market price.

B. A limit-sell order is where investors specify prices at which they are willing to sell a

security.

C. If stock ABC is selling at $50, a limit-buy order may instruct the broker to buy the

stock if and when the share price falls below $45.

D. A market order is an order to buy or sell a stock on a specific exchange (market).

A firm with a low rating from the bond-rating agencies would have

A. a low times-interest-earned ratio.

B. a low debt-to-equity ratio.

C. a low quick ratio.

D. a low debt-to-equity ratio and a low quick ratio.

E. a low times-interest-earned ratio and a low quick ratio.

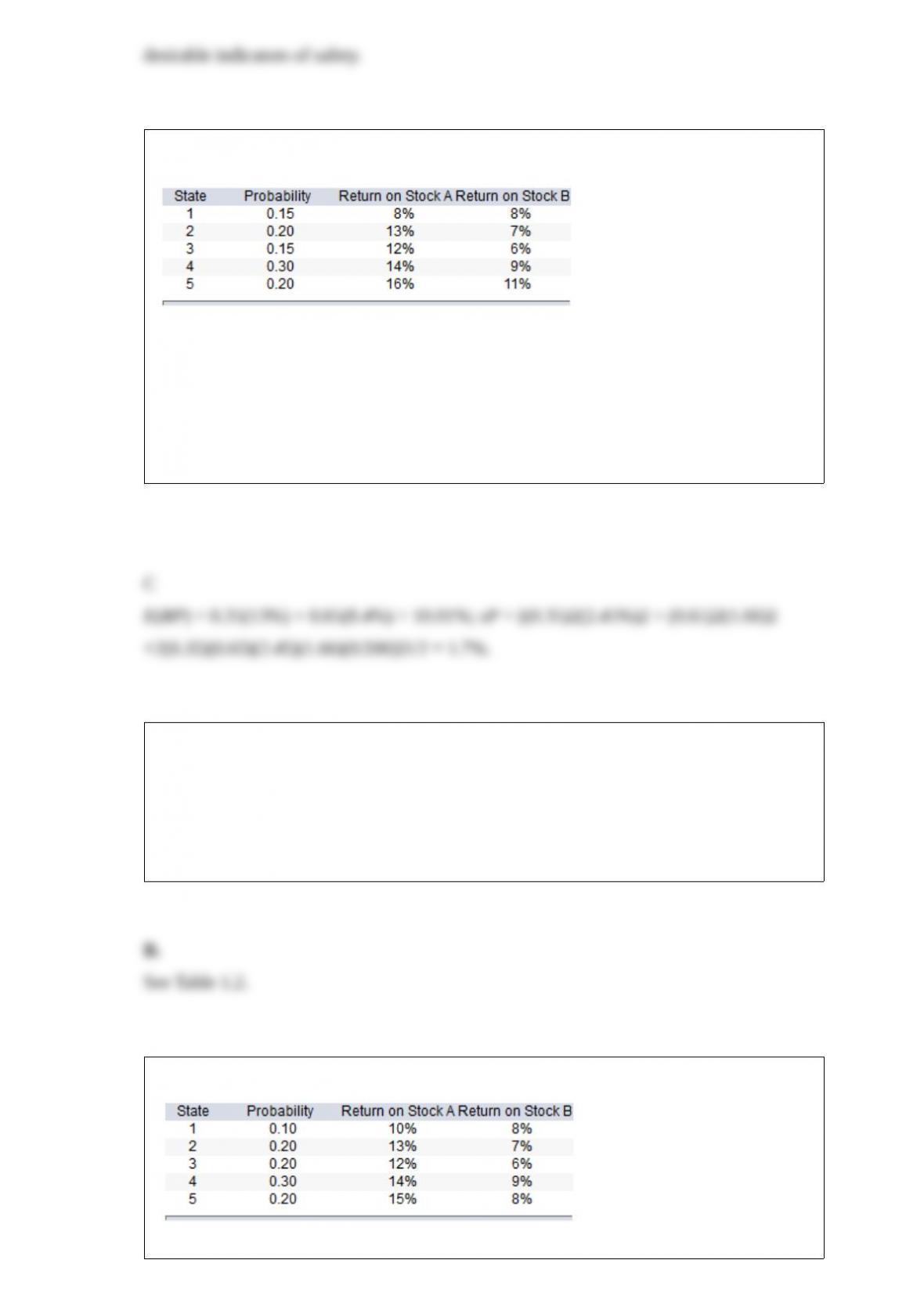

Consider the following probability distribution for stocks A and B:

If you invest 35% of your money in A and 65% in B, what would be your portfolio’s

expected rate of return and

standard deviation?

A. 9.9%; 3%

B. 9.9%; 1.1%

C. 10%; 1.7%

D. 10%; 3%

The largest component of domestic net worth in 2016 was

A. nonresidential real estate.

B. residential real estate.

C. inventories.

D. consumer durables.

E. equipment and software.

Consider the following probability distribution for stocks A and B:

Which of the following portfolio(s) is(are) on the efficient frontier?

A. The portfolio with 20 percent in A and 80 percent in B.

B. The portfolio with 15 percent in A and 85 percent in B.

C. The portfolio with 26 percent in A and 74 percent in B.

D. The portfolio with 10 percent in A and 90 percent in B.

E. A and B are both on the efficient frontier.

If a 7.5% coupon bond is trading for $1,050.00, it has a current yield of

A. 7.0%.

B. 7.4%.

C. 7.1%.

D. 6.9%.

E. 6.7%.

An investor purchases one municipal and one corporate bond that pay rates of return of

6% and 8%, respectively. If the investor is in the 25% marginal tax bracket, his or her

after-tax rates of return on the municipal and corporate bonds would be ________ and

______, respectively.

A. 6%; 8%

B. 4.5%; 6%

C. 4.5%; 8%

D. 6%; 6%

The beta of a stock has been estimated as 0.85 using regression analysis on a sample of

historical returns. A commonly-used adjustment technique would provide an adjusted

beta of

A. 1.01.

B. 0.95.

C. 1.13.

D. 0.90.

Liew and Vassalou (2000) show that returns on style portfolios (SMB and HML)

A. seem like statistical flukes.

B. seem to predict GDP growth.

C. may be proxies for business cycle risk.

D. seem to predict GDP growth and may be proxies for business cycle risk.

E. None of the options are correct.

In the empirical study of a multifactor model by Chen, Roll, and Ross, a factor that did

not appear to have significant explanatory power in explaining security returns was

A. the change in the expected rate of inflation.

B. the risk premium on corporate bonds.

C. the unexpected change in the rate of inflation.

D. industrial production.

Suppose the following equation best describes the evolution of β over time:

βt = 0.3 + 0.2βt– 1

If a stock had a β of 0.8 last year, you would forecast the β to be _______ in the coming

year.

A. 0.46

B. 0.60

C. 0.70

D. 0.94

______ bias arises when the returns of unsuccessful funds are left out of the sample.

A. Survivorship

B. Backfill

C. Omission

D. Incubation

E. None of the options are correct.

Hedge funds differ from mutual funds in terms of

A. transparency.

B. investors.

C. investment strategy.

D. liquidity.

E. All of the options are correct.

Callable bonds

A. are called when interest rates decline appreciably.

B. have a call price that declines as time passes.

C. are called when interest rates increase appreciably.

D. are more likely to be called when interest rates decline and have a call price that

declines as time passes.

E. have a call price that declines as time passes and are called when interest rates

increase appreciably.

The goal of fundamental analysts is to find securities

A. whose intrinsic value exceeds market price.

B. with a positive present value of growth opportunities.

C. with high market capitalization rates.

D. All of the options are correct.

E. None of the options are correct.

The APT requires a benchmark portfolio

A. that is equal to the true market portfolio.

B. that contains all securities in proportion to their market values.

C. that need not be well-diversified.

D. that is well-diversified and lies on the SML.

E. that is unobservable.

Consider the free cash flow approach to stock valuation. Utica Manufacturing Company

is expected to have before-tax cash flow from operations of $500,000 in the coming

year. The firm’s corporate tax rate is 30%. It is expected that $200,000 of operating cash

flow will be invested in new fixed assets. Depreciation for the year will be $100,000.

After the coming year, cash flows are expected to grow at 6% per year. The appropriate

market-capitalization rate for unleveraged cash flow is 15% per year. The firm has no

outstanding debt. The projected free cash flow of Utica Manufacturing Company for the

coming year is

A. $150,000.

B. $180,000.

C. $300,000.

D. $380,000.

The beta of an active portfolio is 1.20. The standard deviation of the returns on the

market index is 20%. The

nonsystematic variance of the active portfolio is 1%. The standard deviation of the

returns on the active portfolio

is

A. 3.84%.

B. 5.84%.

C. 19.60%.

D. 24.17%.

E.26.0%.

All the inputs in the Black-Scholes option pricing model are directly observable except

A. the price of the underlying security.

B. the risk-free rate of interest.

C. the time to expiration.

D. the variance of returns of the underlying asset return.

Two firms, C and D, both produce coat hangers. The price of coat hangers is $1.20

each. Firm C has total fixed costs of $750,000 and variable costs of 30 per coat hanger.

Firm D has total fixed costs of $400,000 and variable costs of 50 per coat hanger. The

corporate tax rate is 40%. If the economy is strong, each firm will sell 2,000,000 coat

hangers. If the economy enters a recession, each firm will sell 1,400,000 coat hangers.

If the economy enters a recession, the before-tax profit of firm C will be

A. $1,680,000.

B. $1,170,000.

C.-$510,000.

D. $204,000.

Until 1999, the ________ Act(s) prohibited banks in the United States from both

accepting deposits and underwriting securities.

A. Sarbanes-Oxley

B. Glass-Steagall

C. SEC

D. Sarbanes-Oxley and SEC

E. None of the options

A hedge ratio of 0.85 implies that a hedged portfolio should consist of

A. long 0.85 calls for each short stock.

B. short 0.85 calls for each long stock.

C. long 0.85 shares for each short call.

D. long 0.85 shares for each long call.

E. None of the options are correct.

Which of the following are examples of defensive industries?

A. Food producers

B. Durable goods producers

C. Pharmaceutical firms

D. Public utilities

E.-Food producers, pharmaceutical firms, and public utilities

Which statement is true regarding the capital market line (CML)?

I) The CML is the line from the risk-free rate through the market portfolio.

II) The CML is the best attainable capital allocation line.

III) The CML is also called the security market line.

IV) The CML always has a positive slope.

A. I only

B. II only

C. III only

D. IV only

E. I, II, and IV

Annual percentage rates (APRs) are computed using

A. simple interest.

B. compound interest.

C. either simple interest or compound interest.

D. best estimates of expected real costs.

E. None of the options are correct.

The previous value of a portfolio that must be reattained before a hedge fund can charge

incentive fees is known as a

A. benchmark.

B. water stain.

C. water mark.

D. high water mark.

E. low water mark.