Which of the following statement(s) is(are) true?

I) The real rate of interest is determined by the supply and demand for funds.

II) The real rate of interest is determined by the expected rate of inflation.

III) The real rate of interest can be affected by actions of the Fed.

IV) The real rate of interest is equal to the nominal interest rate plus the expected rate of

inflation.

A. I and II only

B. I and III only

C. III and IV only

D. II and III only

E. I, II, III, and IV only

Given a stock index with a value of $1,100, an anticipated dividend of $27, and a

risk-free rate of 3%, what should be the value of one futures contract on the index?

A. $943.40

B. $970.00

C. $913.40

D. $1,106.00

E. $1,000.00

In terms of the risk/return relationship in the APT,

A. only factor risk commands a risk premium in market equilibrium.

B. only systematic risk is related to expected returns.

C. only nonsystematic risk is related to expected returns.

D. only factor risk commands a risk premium in market equilibrium, and only

systematic risk is . related to expected returns.

E. only factor risk commands a risk premium in market equilibrium, and only

nonsystematic risk is related to expected returns.

In a multifactor APT model, the coefficients on the macro factors are often called

A. systematic risk.

B. firm-specific risk.

C. idiosyncratic risk.

D. factor betas.

Some of the problems with immunization are

A. duration assumes that the yield curve is flat.

B. duration assumes that if shifts in the yield curve occur, these shifts are parallel.

C. immunization is valid for one interest-rate change only.

D. durations and horizon dates change by the same amounts with the passage of time.

E. immunization is valid for one interest-rate change only, duration assumes that the

yield curve is flat, and that if shifts in the yield curve occur, these shifts are parallel.

Currency-translated options have

A. only asset prices denoted in a foreign currency.

B. only exercise prices denoted in a foreign currency.

C. payoffs that only depend on the maximum price of the underlying asset during the

life of the option.

D.either asset or exercise prices denoted in a foreign currency.

The duration of a par-value bond with a coupon rate of 8.7% and a remaining time to

maturity of 6 years is

A. 6.0 years.

B. 5.1 years.

C. 4.27 years.

D. 3.95 years.

E. None of the options are correct.

Which of the following are mechanisms that have evolved to mitigate potential agency

problems?

I) Using the firm’s stock options for compensation

II) Hiring bickering family members as corporate spies

III) Boards of directors forcing out underperforming management

IV) Security analysts monitoring the firm closely

V) Takeover threats

A. II and V

B. I, III, and IV

C. I, III, IV, and V

D. III, IV, and V

E. I, III, and V

In a well-diversified portfolio,

A. market risk is negligible.

B. systematic risk is negligible.

C. unsystematic risk is negligible.

D. nondiversifiable risk is negligible.

The major concern that has been raised with respect to the weighting of countries

within the EAFE index is

A. currency volatilities are not considered in the weighting.

B. cross-correlations are not considered in the weighting.

C. inflation is not represented in the weighting.

D. the weights are not proportional to the asset bases of the respective countries.

E. None of the options are correct.

On November 22, the stock price of WalMart was $69.50, and the retailer stock index

was 600.30. On November 25, the stock price of WalMart was $70.25, and the retailer

stock index was 605.20. Consider the ratio of WalMart to the retailer index on

November 22 and November 25. WalMart is _______ the retail industry, and technical

analysts who follow relative strength would advise _______ the stock.

A. outperforming; buying

B. outperforming; selling

C. underperforming; buying

D. underperforming; selling

E. equally performing; neither buying nor selling

The “modified duration” used by practitioners is equal to the Macaulay duration

A. times the change in interest rate.

B. times (one plus the bond’s yield to maturity).

C. divided by (one minus the bond’s yield to maturity).

D. divided by (one plus the bond’s yield to maturity).

E. None of the options are correct.

You are a U.S. investor who purchased British securities for 2,000 pounds, one year ago

when the British pound cost $1.50. No dividends were paid on the British securities in

the past year. Your total return based on U.S. dollars was __________ if the value of the

securities is now 2,400 pounds and the pound is worth $1.60.

A. 16.7%

B. 20.0%

C. 28.0%

D. 40.0%

E. None of the options are correct.

An option with an exercise price equal to the underlying asset’s price is

A. worthless.

B. in the money.

C.at the money.

D. out of the money.

E. theoretically impossible.

An underpriced security will plot

A. on the security market line.

B. below the security market line.

C. above the security market line.

D. either above or below the security market line depending on its covariance with the

market.

E. either above or below the security-market line depending on its standard deviation.

When assessing tail risk by looking at the 5% worst-case scenario, the most realistic

view of downside

exposure would be

A. expected shortfall.

B. value at risk.

C. conditional tail expectation.

D. expected shortfall and value at risk.

E. expected shortfall and conditional tail expectation.

Delta neutral

A. is the volatility level for the stock that the option price implies.

B. is the continued updating of the hedge ratio as time passes.

C. is the percentage change in the stock call-option price divided by the percentage

change in the stock price.

D. means the portfolio has no tendency to change value as the underlying portfolio

value changes.

Of the following types of ETFs, an investor who wishes to invest in a diversified

portfolio that tracks the MSCI Japan Index should choose

A. SPY.

B. EWJ.

C. QQQQ.

D. IWM.

E. VTI.

Agricultural futures contracts are actively traded on

A. corn.

B. oats.

C. pork bellies.

D. corn and oats.

E. All of the options are correct.

You invest $100 in a risky asset with an expected rate of return of 0.12 and a standard

deviation of 0.15 and a

T-bill with a rate of return of 0.05.

The slope of the capital allocation line formed with the risky asset and the risk-free

asset is equal to

A. 0.4667.

B. 0.8000.

C. 2.14.

D. 0.41667.

E. Cannot be determined.

A mutual fund had year-end assets of $700,000,000 and liabilities of $7,000,000. There

were 40,150,000 shares in the fund at year end. What was the mutual fund’s net asset

value?

A. $9.63

B. $57.71

C. $16.42

D. $17.87

E. $17.26

In calculating the Standard and Poor’s stock price indices, the adjustment for stock split

occurs

A. by adjusting the divisor.

B. automatically.

C. by adjusting the numerator.

D. quarterly on the last trading day of each quarter.

In periods of inflation, accounting depreciation is __________ relative to replacement

cost, and real economic income is________.

A. overstated; overstated

B. overstated; understated

C. understated; overstated

D. understated; understated

E. correctly stated; correctly stated

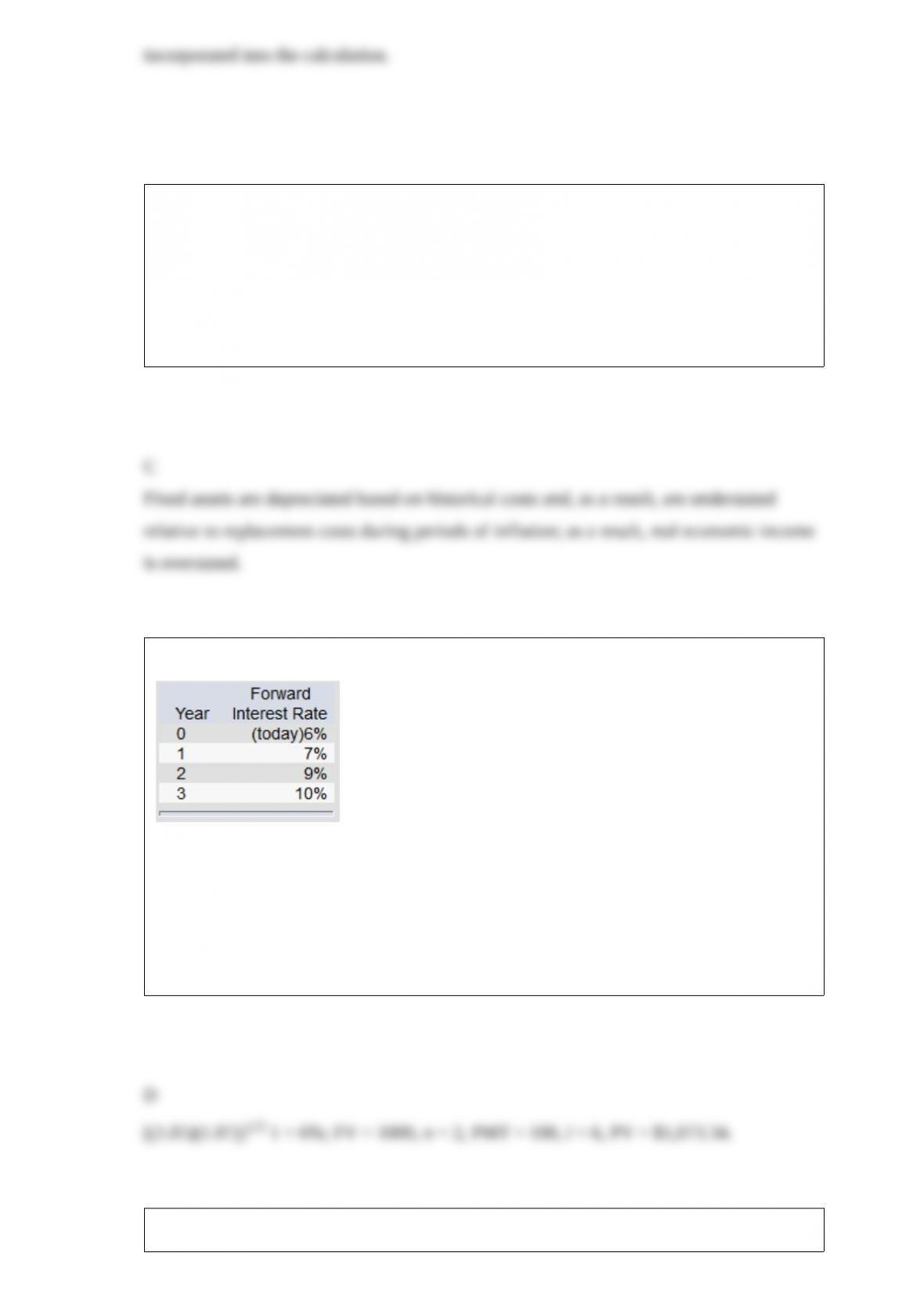

Suppose that all investors expect that interest rates for the 4 years will be as follows:

What is the price of a 2-year maturity bond with a 10% coupon rate paid annually? (Par

value = $1,000)

A. $1,092

B. $1,054

C. $1,000

D. $1,073

E. None of the options are correct.

Assume that at retirement you have accumulated $825,000 in a variable annuity

contract. The assumed investment return is 5.5%, and your life expectancy is 18 years.

What is the hypothetical constantbenefit payment?

A. $73,358.93

B. $33,333.33

C. $51,481.38

D. $52,452.73

E. The answer cannot be determined from the information provided.

A 9%, 16-year bond has a yield to maturity of 11% and duration of 9.25 years. If the

market yield changes by 32 basis points, how much change will there be in the bond’s

price?

A. 1.85%

B. 2.01%

C. 2.67%

D. 6.44%

A call option on a stock is said to be in the money if

A. the exercise price is higher than the stock price.

B.the exercise price is less than the stock price.

C. the exercise price is equal to the stock price.

D. the price of the put is higher than the price of the call.

E. the price of the call is higher than the price of the put.

The ________ is used to calculate the present value of a bond.

A. nominal yield

B. current yield

C. yield to maturity

D. yield to call

E. None of the options are correct.

The difference between a random walk and a submartingale is the expected price

change in a random walk is ______, and the expected price change for a submartingale

is ______.

A. positive; zero

B. positive; positive

C. positive; negative

D. zero; positive

E. zero; zero

Consider the Treynor-Black model. The alpha of an active portfolio is 3%. The

expected return on the market

index is 10%. The variance of the return on the market portfolio is 4%. The

nonsystematic variance of the active

portfolio is 2%. The risk-free rate of return is 3%. The beta of the active portfolio is

1.15. The optimal proportion

to invest in the active portfolio is

A. 48.7%.

B.98.4%.

C. 51.3%.

D. 100.0%.

A Treasury bond due in one year has a yield of 5.7%; a Treasury bond due in 5 years

has a yield of 6.2%. A bond issued by Ford Motor Company due in 5 years has a yield

of 7.5%; a bond issued by Shell Oil due in one year has a yield of 6.5%. The default

risk premiums on the bonds issued by Shell and Ford, respectively, are

A. 1.0% and 1.2%.

B. 0.7% and 1.5%.

C. 1.2% and 1.0%.

D. 0.8% and 1.3%.

E. None of the options are correct.

The process of marking to market

A. posts gains or losses to each account daily.

B. may result in margin calls.

C. impacts only long positions.

D. posts gains or losses to each account daily and may result in margin calls.

E. All of the options are correct.