The U.S. Securities Act of 1933 requires that all securities offered to the public must be

registered with the government. True or False

Answer:

The methodology for valuing cross-border transactions using discounted cash flow

analysis is substantially different from that employed when both the acquiring and

target firms are within the same country. True of False

Answer:

Alliances and joint ventures are likely to receive more intensive scrutiny by regulators

because of their tendency to be more anti-competitive than M&As. True or False

Answer:

Preferred stock exhibits some of the characteristics of long-term debt in that its

dividend is generally constant and preferred

stockholders are paid before common shareholders in the event the firm is liquidated.

True or False

Answer:

Like the recent transactions method, comparable company valuation estimates do not

require the addition of a purchase price premium. True or False

Answer:

An acquisition plan defines the objectives to be achieved by acquiring another firm,

management’s preferences as to how the acquisition process should be managed,

resources required, and the roles and responsibilities of those responsible for

implementing the plan. True or False

Answer:

Very few closely held businesses are family owned. True or False

Answer:

If a creditor is owed a large amount of money, it could become a major or even the

controlling shareholder in the reorganized firm. True or False

Answer:

The primary advantage of the cost of capital method is its relative computational

simplicity. True or False

Answer:

By law, corporate liquidation can only be conducted outside of the U.S. bankruptcy

court.

True or False

Answer:

Total consideration refers to what is to be paid for the target firm and usually only

consists of cash or stock, exclusively. True or False

Answer:

Because they can be potentially so lucrative to sellers, earn-outs are sometimes used to

close the gap between what the seller wants and what the buyer might be willing to pay.

True or False

Answer:

Under purchase price accounting, the excess of the purchase price paid over the book

value of equity of the target firm is assigned only to the tangible assets up to their fair

market value or to goodwill. True or False

Answer:

If the buyer believes that the seller has overstated revenue in a specific accounting

period, the buyer can reconstruct revenue by examining usage levels, in the same

accounting period, of the key inputs required to produce the product or service. True or

False

Answer:

Market-based valuation measures are meaningful only for firms with a stable earnings,

cash flow, or sales history. True or False

Answer:

Automatic stays are granted by the court only when the debtor files for bankruptcy.

True or False

Answer:

The seller’s preference for stock or cash will reflect their desire for liquidity, the

attractiveness of the acquirer’s shares, and whether the seller is organized as a joint

venture corporation. True or False

Answer:

In a reverse triangular merger, the acquirer retains the target’s tax attributes. True or

False

Answer:

A debt-for-equity swapoccurs when creditors surrender a portion of their claims on the

firm in exchange for an ownership position in the firm. True or False

Answer:

To qualify for a 1031 exchange, the property must be an investment property or one that

is used in a trade or business (e.g., a warehouse, store, or commercial office building).

True or False

Answer:

Whenever an investor accumulates 5% or more of a public company’s stock, it must

make a so-called 13(d) filing with the SEC. True or False

Answer:

For developed countries, such as Western Europe, the interest rate parity theory

provides a useful framework for estimating forward currency exchange rates (i.e.,

future spot exchange rates). True or False

Answer:

Subchapter S Corporation shareholders, and LLC members, are taxed at their personal

tax rates. True or False

Answer:

The Herfindahl-Hirschman Index is a measure of industry concentration used by U.S.

antitrust regulators in determining whether to accept or reject a proposed merger. True

or False

Answer:

The growth in LBO activity is not simply a U.S. phenomenon. Western Europe has seen

a veritable explosion in private equity investors taking companies private, reflecting

ongoing liberalization in the European Union as well as cheap financing and industry

consolidation. True or False

Answer:

The replacement cost approach to valuation estimates what it would cost to replace the

target firm’s assets at current market prices using professional appraisers less the

present value of the firm’s liabilities. True or False

Answer:

The primary shortcoming of industry concentration ratios is the frequent inability of

antitrust regulators to define accurately what constitutes an industry, the failure to

reflect ease of entry or exit, foreign competition, and the distribution of firm size. True

or false

Answer:

The NPV of an acquisition of a manufacturer operating at full capacity may have a

lower value than if the NPV is adjusted for a decision made at a later date to expand

capacity. If the additional capacity is fully utilized, the resulting higher level of future

cash flows may increase the acquisition’s NPV. In this instance, the value of the real

option to expand is the difference between the NPV with and without expansion. True

or False

Answer:

When a public company is subject to an LBO, it is said to be going private, because

more than 50% of the equity of the firm has been purchased by a small group of

investors and is no longer publicly traded. True or False

Answer:

Alliance agreements must be flexible enough to be revised when necessary and contain

mechanisms for breaking deadlocks, transferring ownership interests, and dealing with

the potential for termination. True or False

Answer:

Projecting future annual debt-to-equity ratios depends on knowing the firm’s debt

repayment schedules and projecting growth in the market value of shareholders’ equity.

True or False

Answer:

A spin-off may create shareholder wealth for all of the following reasons except for

a. Spin-offs are generally not taxable if properly structured

b. The spin-off’s management and board is independent of the former parent

c. Investors will be better able to value the spin-off

d. The cost of capital of the spin-off is generally higher than when it was part of the

parent

e. The spin-off may be subsequently acquired by another firm

Answer:

All of the following are true of reverse mergers except for.

a. May be used to take a private firm public

b. May represent an effective alternative to an IPO

c. Commonly use private equity placements for financing

d. Requires 2 years of audited financial statements to take a private firm public

e. A and B

Answer:

Prior to the Bankruptcy Abuse Protection and Consumer Protection Act of 2005

(BAPCPA), commercial enterprises used Chapter 11 Reorganization to continue

operating a business and to repay creditors through a court-approved plan of

reorganization. True or False

Answer:

Which of the following are generally not considered motives for mergers?

a. Desire to achieve economies of scale

b. Desire to achieve economies of scope

c. Desire to achieve antitrust regulatory approval

d. Strategic realignment

e. Desire to purchase undervalued assets

Answer:

Foreign direct investment in U.S. companies that may threaten national security is

regulated by which of the following:

a. Hart-Scott-Rodino Antitrust Improvements Act

b. Defense Production Act

c. Sherman Act

d. Federal Trade Commission Act

e. Clayton Act

Answer:

Around the announcement date of a merger, acquiring firm shareholders normally earn

a. 30% positive abnormal returns

b. 20% abnormal returns

c. Zero to slightly negative returns

d. 100% positive abnormal returns

e. 10% positive abnormal returns

Answer:

All of the following are true of tender offers except for

a. Tender offers consist only of offers of cash for target stock

b. Are generally considered an expensive takeover tactic

c. Are extended for a specific period of time

d. Are sometimes over subscribed

e. Must be filed with the SEC

Answer:

All of the following factors are considered by U.S. antitrust regulators except for

a. Market share

b. Potential adverse competitive effects

c. Barriers to entry

d. Purchase price paid for the target firm

e. Efficiencies created by the combination

Answer:

Which of the following is generally not true about leveraged buyouts?

a. Borrowed funds are used to pay for all or most of the purchase price, perhaps as

much as 90%

b. Tangible assets of the target firm are often used as collateral for loans.

c. Bank loans are often secured by the target firm’s intangible assets

d. Secured debt is often referred to as junk bond financing.

e. C and D only

Answer:

All of the following are generally true about creating new organizations except for

a. Learn from prior organizational strengths and weaknesses

b. Business needs should drive structure and not the reverse

c. Centralized organizations facilitate the pace of the integration

d. The structure employed during the integration must be the one used in the long-run

e. Senior managers should be given responsibility for selecting their own subordinates

Answer:

Which of the following government agencies can discipline firms with inappropriate

governance practices?

a. Securities and Exchange Commission

b. Federal Trade Commission

c. The Department of Justice

d. A & C only

e. A, B, & C

Answer:

The actual price paid by the buyer for the target firm is determined when

a. The initial offer is made

b. As a result of the negotiation process

c. When the letter of intent is signed

d. Following the completion of due diligence

e. Once a financing plan has been approved

Answer:

Which of the following is not true of mergers?

a. Liabilities and assets transfer automatically

b. May be subject to transfer taxes.

c. No minority shareholders remain.

d. May be time consuming due to need for shareholder approvals.

e. May have to pay dissenting shareholders appraised value of stock

Answer:

Which of the following is generally not true of integration planning?

a. Is of secondary importance in the acquisition process.

b. Is crucial to the ultimate success of the merger or acquisition

c. Represents an opportunity to earn trust among all parties to the transaction

d. Involves developing effective communication strategies for employees, customers,

and suppliers.

e. Is often neglected in the heat of negotiation.

Answer:

Which of the following represent advantages of the comparable companies’ valuation

method?

a. Uses the most accurate market-based valuation at a point in time

b. Valuations need to be adjusted to reflect control premiums

c. Adjusts for risk of future cash flows

d. Adjusts for the timing of future cash flows

e. A & B only

Answer:

A diligent buyer must ensure that the target is in compliance with the labyrinth of labor

and benefit laws, including those covering all of the following except for

a. Sexual harassment

b. Age discrimination,

c. National security

d. Drug testing

e. Wage and hour laws.

Answer:

Which of the following may be used as acquisition vehicles?

a. Partnership

b. Limited liability corporation

c. Corporate shell

d. ESOP

e. All of the above

Answer:

Which one of the following factors is not considered in calculating the firm’s cost of

capital?

a. cost of equity

b. interest rate on debt

c. the firm’s marginal tax rate

d. book value of debt and equity

e. the firm’s target debt to equity ratio

Answer:

Financially distressed firms often are characterized by all of the following except for:

a. Underinvestment in operations

b. Employee layoffs

c. High levels of research and development spending

d. Declining product quality

e. Slower payments to suppliers

Answer:

All of the following are true of buyer due diligence except for

a. Due diligence is the process of validating assumptions underlying valuation.

b. Can be replaced by appropriate representations and warranties in the agreement of

purchase and sale.

c. Primary objectives are to identify and to confirm sources and destroyers of value

d. Consists of operational, financial, and legal reviews.

e. Endeavors to identify the “fatal flaw” that could destroy the deal

Answer:

A merger which is expected to produce synergy

a. Should be rejected because the synergy will dilute the combined firm’s earnings per

share

b. Should be rejected because the first year’s cash flow is negative

c. Has a negative NPV

d. Should be pursued because it creates value

e. Reduces target firm revenues

Answer:

The acquirer’s sales force sells very complex software solutions to its customers. The

target firm manufactures commodity hardware products. Customers of the two firms

sometimes buy both products. The benefits of integrating the sales force of both the

acquirer and target firms includes all of the following except for

a. Generates significant cost savings by eliminating duplicate sales representatives

b. Eliminates related sales support expenses

c. Minimizes potential customer confusion by enabling customers to deal with a single

sales representative

d. Facilitates communication of a consistent brand image

e. Makes product cross-selling more effective

Answer:

A firm decides to distribute all of the shares it holds in a subsidiary to its shareholders.

The distribution would be called a

a. Divestiture

b. Split-up

c. Spin-off

d. Split-up

e. Equity carveout

Answer:

All of the following are true about voluntary liquidations except for

a. They can be conducted outside of court in a private auction.

b. They can be done within the protection of the bankruptcy court.

c. Creditors normally prefer liquidations to be conducted by the bankruptcy court..

d. A trustee is assigned to sell the debtor firm’s assets as quickly as possible while

obtaining the best possible price.

e. If the insolvent firm is willing to accept liquidation and all creditors agree, legal

proceedings are not necessary.

Answer:

The scrupulous application of GAAP ensures both consistency in comparing one firm’s

financial

performance with another and the accuracy of the data. True or False

Answer:

Target is a wholly owned subsidiary of MegaCorp Inc. MegaCorp supplies a number of

services to target. Target sells some of its products to other MegaCorp subsidiaries.

Target also buys products from other MegaCorp subsidiaries that are used as inputs in

producing Target’s products. Which of the following adjustments should the acquirer

make to Target’s financial statements before valuing the firm?

a. Deduct the actual cost of services required by Target that are being supplied by the

parent without charge from target’s cost of sales.

b. Deduct the difference between the cost of products purchased from other MegaCorp

subsidiaries at below market prices and the actual market prices for such products from

Target’s cost of sales.

c. Deduct the difference between the cost of products purchased from other MegaCorp

subsidiaries at above market prices and the actual cost of such products if purchased

from other sources from Target’s cost of sales

d. A and B only.

e. None of the above.

Answer:

A holding company may be used as a post-closing organizational structure for all but

which of the following reasons?

a. A portion of the purchase price for the target firm included an earn-out

b. The target firm has a substantial amount of unknown liabilities

c. The acquired firm’s culture is very different from that of the acquiring firm

d. Profits from operations are not taxable

e. The transaction involves a cross border transaction

Answer:

Asset based lending is commonly used to finance leveraged buyouts. Which of the

following is not true about such financing?

a. The borrower generally pledges tangible assets as collateral.

b. Lenders look at the target firm’s assets as their primary protection.

c. Bank loans are secured frequently by receivables and inventory.

d. Loans maturing in more than one year are often referred to as term loans.

e. The target firm’s most liquid assets generally secure longer-term loans.

Answer:

All of the following questions are relevant for conducting a self-assessment or internal

analysis of the firm except for

a. What are the firm’s critical strengths and weaknesses as compared to the competition?

b. Can the firm’s critical strengths be easily duplicated and surpassed by the

competition?

c. Can the firm’s critical strengths be used to gain strategic advantage in the firm’s

chosen market?

d. What are the least important factors customers consider in making purchasing

decisions?

e. Can the firm’s key weaknesses be exploited by the competition?

Answer:

Tribune Company Acquires the Times Mirror Corporation

in a Tale of Corporate Intrigue

Background: Oh, What Tangled Webs We Weave. .

.

CEO Mark Willes had reason to be optimistic about the future. Operating profits had

grown at a double-digit rate, and earnings per share had grown at a 55% annual rate

between 1995 to 1999. Many shareholders appeared to be satisfied. However, some

were not. Although pleased with the improvement in profitability, they were concerned

about the long-term growth prospects of the firm. Reflecting this disenchantment,

Times Mirror’s largest shareholder, the Chandler family, was contemplating the sale of

the company and along with it the crown jewel Los Angeles Times. It had been assumed

for years that the Chandler family trusts made a sale of Times Mirror out of the

question. The Chandler’s super voting stock (i.e., stock with multiple voting rights)

allowed them to exert a disproportionate influence on corporate decisions. The

Chandler Trusts controlled more than two-thirds of voting shares, although the family

owned only about 28% of the total shares of the outstanding stock.

In May 1999 the Tribune Chairman John Madigan contacted Willes and made an offer

for the company, but Willes, with the help of his then-chief financial officer (CFO),

Thomas Unterman, made it clear to Madigan that the company was not for sale. What

Willes did not realize was that Unterman soon would be serving in a dual role as CFO

and financial adviser to the Chandlers and that he would eventually step down from his

position at Times Mirror to work directly for the family. In his dual role, he worked

without Willes’ knowledge to structure the deal with the Tribune.

Following months of secret negotiations, the Chicago-based Tribune Company and the

Times Mirror Corporation announced a merger of the two companies in a cash and

stock deal valued at approximately $7.2 billion, including $5.7 billion in equity and

$1.5 billion in assumed debt. The transaction, announced March 13, 2000, created a

media giant that has national reach and a major presence in 18 of the nation’s top 30

U.S. markets, including New York, Los Angeles, and Chicago. The combined company

has 22 television stations, four radio stations, and 11 daily newspapersincluding the Los

Angeles Times, the nation’s largest metropolitan daily newspaper and flagship of the

Times Mirror chain.

Transaction Terms: Tribune Shareholders Get Choice of Cash or Stock

The Tribune agreed to buy 48% of the outstanding Times Mirror stock, about 28 million

shares, through a tender offer. After completion of the tender offer, each remaining

Times Mirror share would be exchanged for 2.5 shares of Tribune stock. Under the

terms of the transaction, Times Mirror shareholders could elect to receive $95 in cash or

2.5 shares of Tribune common stock in exchange for each share of Times Mirror stock.

Holders of 27.2 million shares of Times Mirror stock elected to receive Tribune stock,

whereas holders of 10.6 million elected to receive cash. Because the amount of cash

offered in the merger was limited and the cash election was oversubscribed, Times

Mirror shareholders electing to receive cash actually received a combination of cash

and stock on a pro rata basis (Table 1).

Newspaper Advertising Revenues Continue to Shrink

Most U.S. newspapers are mired in the mature or declining phase of their product life

cycle. For the past half-century, newspapers have watched their portion of the

advertising market shrink because of increased competition from radio and television.

By the early 1990s, all major media began taking a significant hit in their advertising

revenue streams as businesses discovered that direct mail could target their message

more precisely. Moreover, consolidation among major retailers further reduced the size

of advertising dollar pool. The same has happened with numerous large supermarket

chain mergers. Newspaper advertising revenues also have been threatened by increasing

competition from advertising and editorial content delivered on the internet. Finally,

newspapers simply have become less attractive places to advertise as readership

continues to decline as a result of an aging population and new generations that do not

see newspapers as relevant.

Times Mirror: A Largely Traditional Business Model

As essentially a traditional newspaper, Times Mirror publishes five metropolitan and

two suburban daily newspapers, a variety of magazines, and professional information

such as flight maps for commercial airline pilots. The Los Angeles Times, a southern

California institution founded in 1881, is Times Mirror’s largest holding and operates

some two dozen expensive foreign news bureausmore than any other newspaper in the

country. The Los Angeles Times has more than 1200 Los Angeles Times reporters and

editors around the world (CNNfn, March 13, 2000).

Tribune Company Profile: The Face of New Media?

Unlike the Times Mirror, Tribune has built its strategy around four business groups:

broadcasting, publishing, education, and interactive. The Tribune is also an equity

investor in America Online and other leading internet companies, underscoring the

company’s commitment to new-media technologies. Applying leading edge new-media

technology has allowed the Tribune to transform they way it does business, and the

technology commitment creates the opportunity for future growth. The internet has

been the greatest driver for change, and the Tribune’s interactive business group

continues to focus on capitalizing on emerging Web technologies. Throughout the

company, new technologies have been applied aggressively to create new products,

improve existing products, and make operations more efficient. The Tribune’s

non-newspaper revenues accounted for more than half of its earnings by 2000.

Anticipated Synergy

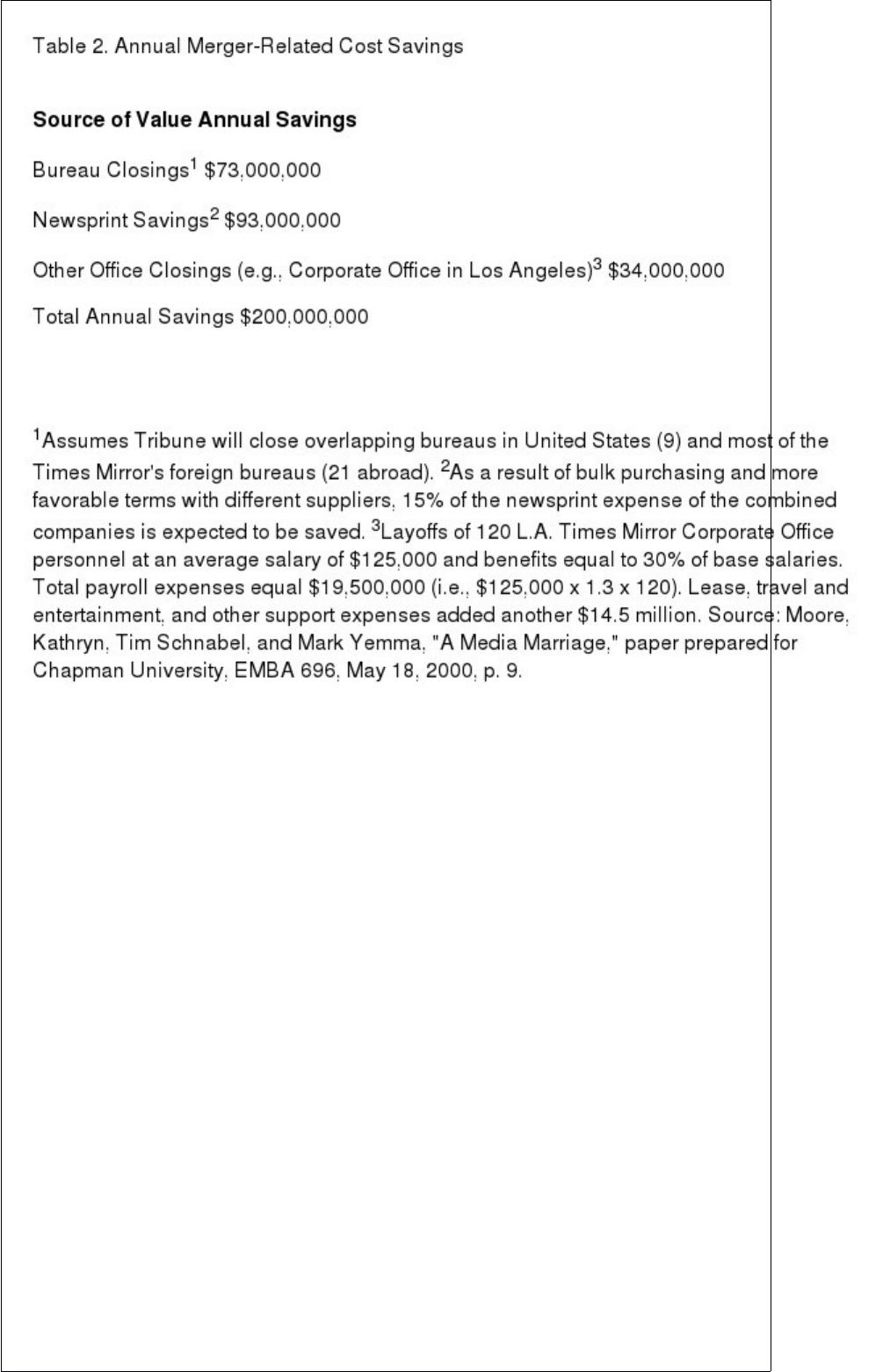

Cost Savings: Opportunities Abound

Cost savings are expected because of the closing of selected foreign and domestic news

bureaus, a reduction in the cost of newsprint through greater volume purchases, the

closing of the Times Mirror corporate headquarters, and elimination of corporate staff.

Such savings are expected to reach $200 million per year (Table 2).

Revenue: Great Potential . . . But Is It Achievable?

The combined companies will have a major presence in 18 of the nation’s top 30 U.S.

advertising markets, including New York, Los Angeles, and Chicago. The combined

companies provide unprecedented opportunities for advertisers to reach major market

consumers in any media formbroadcast, newspapers, or interactive. In addition, the

combined companies will benefit consumers by giving them rich and diverse choices

for obtaining the news, information, and entertainment they want anytime, anywhere.

These factors provide an increased ability to capture national advertising in the most

important U.S. population centers. The significantly greater breadth of the combined

firm’s geographic coverage is expected to boost advertising revenues from about 3% to

6% annually.

Integration Challenges: Cultural Warfare?

Based on the current, traditional culture found at theLos Angeles Times and other Times

Mirror properties, integration following the merger was likely to be slow and painful.

Concerns among journalists about spreading their talents thin across three or four

mediaprint, television, online, and radioin the course of a day’s work raised the stress

level. Although the Tribune has been able to make the transition to a largely multimedia

company more rapidly than the more traditional newspapers, it has been costly. For

example, development losses in 1999 were $3035 million at Chicagotribune.com and an

estimated $45 million in 2000. The bleeding was expected to continue for some time

and to constitute a major distraction for the management of the new company.

Financial Analysis

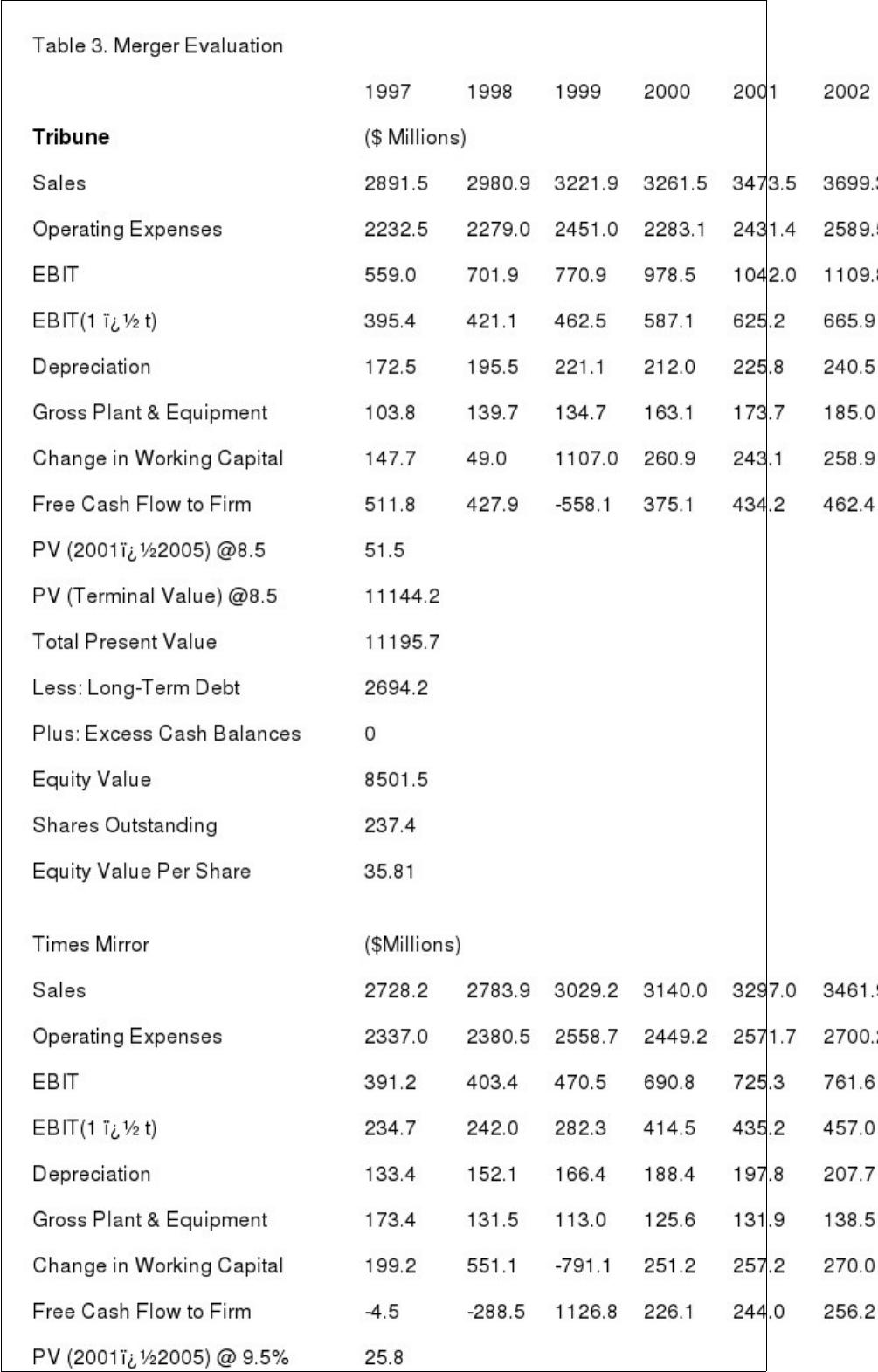

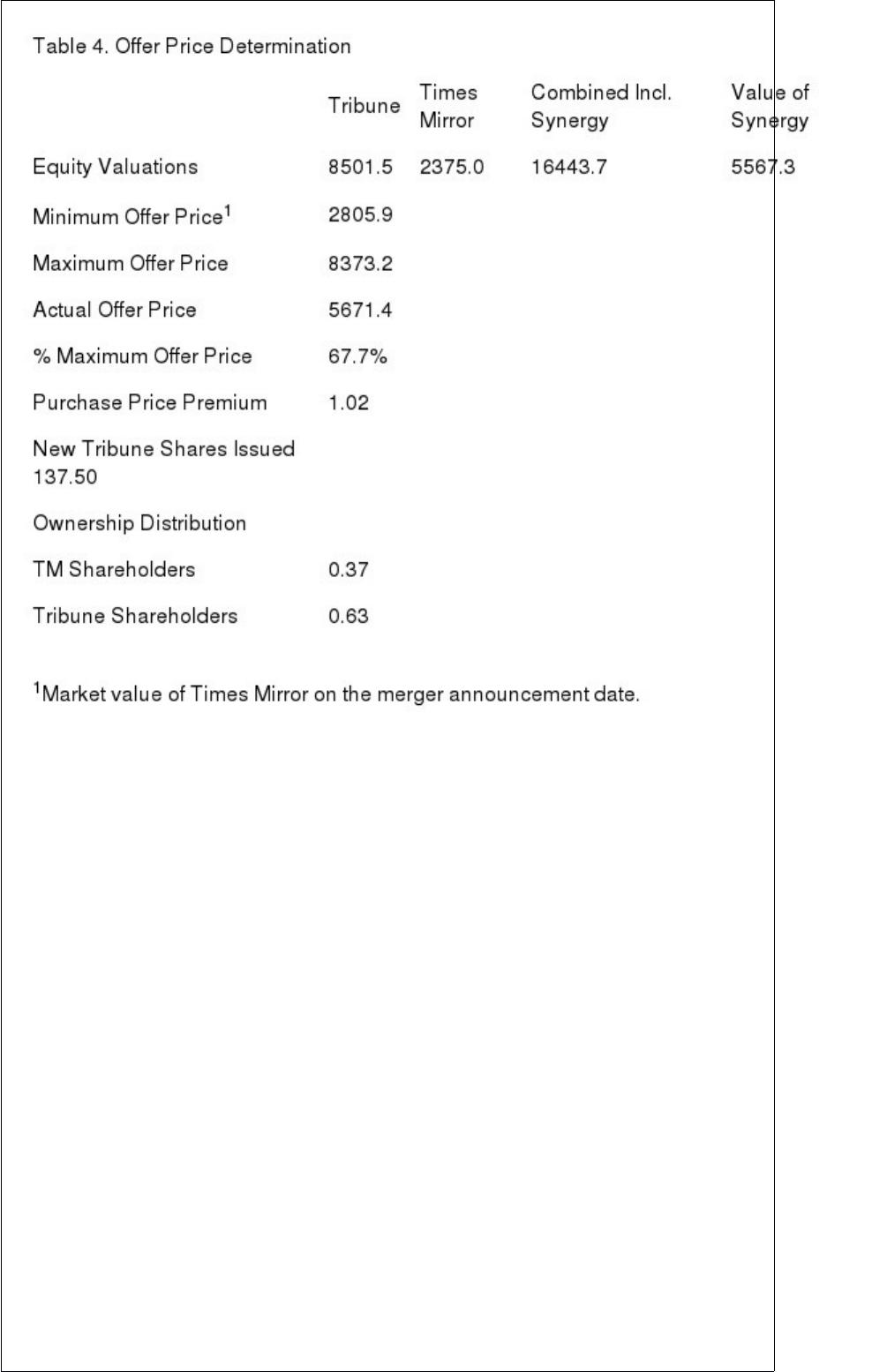

The present values of the Tribune, Times Mirror, and the combined firms are $8.5

billion, $2.4 billion, and $16.5 billion, respectively; the estimated present value of

synergy is $5.6 billion (Table 3). This assumes that pretax cost savings are phased in as

follows: $25 million in 2000, $100 million in 2001, and $200 million thereafter. The

cost savings are net of all expenses related to realizing such savings such as severance,

lease buyouts, and legal fees. Table 4 describes how the initial offer price could have

been determined and the postmerger distribution of ownership between Times Mirror

and Tribune shareholders.

Epilogue

Only time will tell if actual returns to shareholders in the combined Tribune and Times

Mirror company exceed the expected financial returns provided in the valuation models

in this case study. Times Mirror shareholders earned a substantial 102% purchase price

premium over the value of their shares on the day the merger was announced. Some

portion of those undoubtedly “cashed out” of their investment following receipt of the

new Tribune shares. However, for those former Times Mirror shareholders continuing

to hold their Tribune stock and for Tribune shareholders of record on the day the

transaction closed, it is unclear if the transaction made good economic sense.

Discussion Questions:

1) In your judgment, did it make good strategic sense to combine the Tribune and Times

Mirror

corporations? Why? / Why not?

2) Using the Merger Evaluation table given in the case, determine the estimated equity

values of Tribune, Times Mirror and the combined firms. Why is long-term debt

deducted from the total present value estimates in order to obtain equity value?

3) Despite the merger having closed in mid-2000, the full effects of synergy are not

expected until 2002. Why? What factors could account for the delay?

4) The estimated equity value for the Times Mirror Corporation on the day the merger

was announced was about $2.8 billion. Moreover, as shown in the offer price evaluation

table, the equity value estimated using discounted cash flow analysis is given has $2.4

billion. Why is the minimum offer price shown as $2.8 billion rather than the lower

$2.4 billion figure? How is the maximum offer price determined in the Offer Price

Evaluation Table? How much of the estimated synergy value generated by combining

the two businesses is being transferred to the Times Mirror shareholders? Why?

5) Does the Times Mirror-Tribune Corporation merger create value? If so, how much?

What percentage of this value goes to Times Mirror shareholders and what percentage

to Tribune shareholders? Why?

Answer:

Poorly executed integration often results in high employee turnover. The costs of such

turnover include which of the following?

a. Declining morale among those that remain

b. Retraining costs

c. Declining productivity

d. Deteriorating customer service

e. All of the above

Answer:

Corporate shells have value because they enable the buyer to

a. Avoid the cost of going public

b. Exploit intangible value such as brand name

c. A and D only

d. Provide limited liability

e. A, B, and D only

Answer:

All of the following are true of the Hart-Scott-Rodino Antitrust Improvements Act

except for

a. Acquisitions involving firms of a certain size cannot be completed until certain

information is supplied to the FTC

b. Only the acquiring firm is required to file with the FTC

c. An acquiring firm may agree to divest certain businesses following the completion of

a transaction in order to get regulatory approval.

d. The Act is intended to give regulators time to determine whether the proposed

combination is anti-competitive.

e. The FTC may file a lawsuit to block a proposed transaction

Answer:

Which of the following are examples of intangible assets that may have value to the

acquiring company?

a. Patents

b. Trade names

c. Customer lists and relationships

d. Covenants not to compete

e. All of the above

Answer:

Intangible assets often constitute a substantial source of value to the acquiring firm.

Which of the following are not generally considered intangible assets?

a. Patents and technical know-how

b. Warranty and contingent claims

c. Trademarks and customer lists

d. Covenants not to compete and franchises

e. Copyrights and software

Answer: