You sold short 100 shares of common stock at $45 per share. The initial margin is 50%.

Your initial investment was

A. $4,800.

B. $12,000.

C. $2,250.

D. $7,200.

If a portfolio had a return of 12%, the risk-free asset return was 4%, and the standard

deviation of the portfolio’s

excess returns was 25%, the risk premium would be

A. 8%.

B. 16%.

C. 37%.

D. 21%.

E. 29%.

The Sharpe, Treynor, and Jensen portfolio performance measures are derived from the

CAPM,

A. therefore, it does not matter which measure is used to evaluate a portfolio manager.

B. however, the Sharpe and Treynor measures use different risk measures. Therefore,

the measures vary as to . whether or not they are appropriate, depending on the

investment scenario.

C. therefore, all measure the same attributes.

D. therefore, it does not matter which measure is used to evaluate a portfolio manager.

However, the Sharpe and

Treynor measures use different risk measures, so therefore, the measures vary as to

whether or not they are appropriate, depending on the investment scenario.

E. None of the options are correct.

In a multifactor APT model, the coefficients on the macro factors are often called

A. systematic risk.

B. factor sensitivities.

C. idiosyncratic risk.

D. factor betas.

E. factor sensitivities and factor betas.

Which of the following is used extensively in foreign trade when the creditworthiness

of one trader is unknown to the trading partner?

A. Repos

B. Bankers’acceptances

C. Eurodollars

D. Federal funds

One way that Black, Jensen and Scholes overcame the problem of measurement error

was to

A. group securities into portfolios.

B. use a two stage regression methodology.

C. reduce the precision of beta estimates.

D. set alpha equal to one.

E. None of the options are correct.

If you begin with a ______ and obtain additional data from an experiment, you can

form a ______.

A. posterior distribution; prior distribution

B.prior distribution; posterior distribution

C. tight posterior; Bayesian analysis

D. tight prior; Bayesian analysis

E. None of the options are correct.

Which one of the following statements about convertibles are false?

I) The longer the call protection on a convertible, the less the security is worth.

II) The more volatile the underlying stock, the greater the value of the conversion

feature.

III) The smaller the spread between the dividend yield on the stock and the

yield-to-maturity on the bond, the more the convertible is worth.

IV) The collateral that is used to secure a convertible bond is one reason convertibles

are more attractive than the underlying stock.

A. I only

B. II only

C. I and III

D. IV only

E. I, III, and IV

Which one of the following statements regarding “basis” is true?

A. The basis is the difference between the futures price and the spot price.

B. The basis risk is borne by the hedger.

C. A short hedger suffers losses when the basis decreases.

D. The basis increases when the futures price increases by more than the spot price.

E. The basis is the difference between the futures price and the spot price, basis risk is

borne by the hedger, and basis increases when the futures price increases by more than

the spot price.

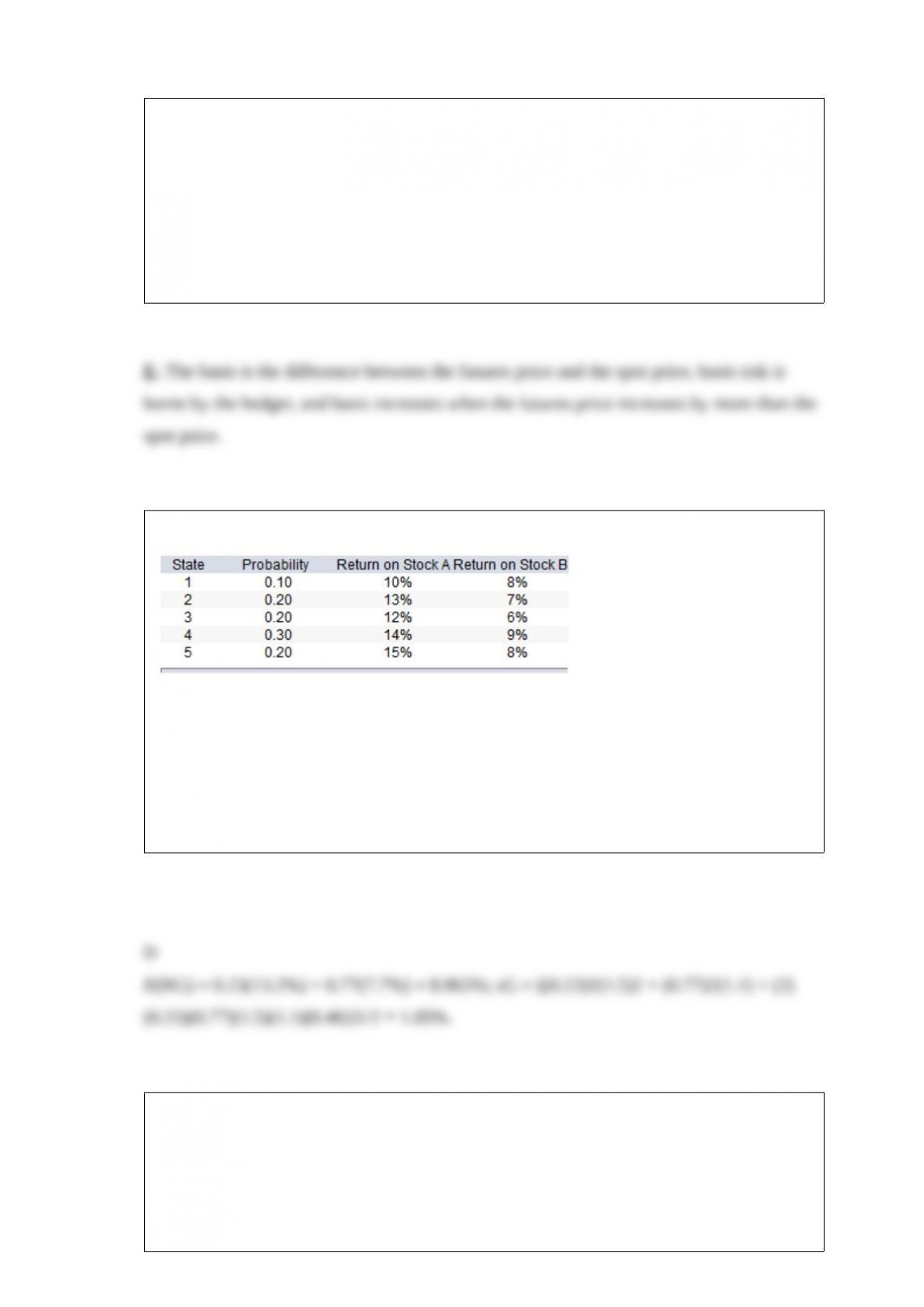

Consider the following probability distribution for stocks A and B:

The expected rate of return and standard deviation of the global minimum variance

portfolio, G, are

__________ and __________, respectively.

A. 10.07%; 1.05%

B. 8.97%; 2.03%

C. 10.07%; 3.01%

D. 8.97%; 1.05%

Over the past year, you earned a nominal rate of interest of 14% on your money. The

inflation rate was 2% over

the same period. The exact actual growth rate of your purchasing power was

A. 11.76%.

B. 16.00%.

C. 15.02%.

D. 14.32%.

An 8%, 15-year bond has a yield to maturity of 10% and duration of 8.05 years. If the

market yield changes by 25 basis points, how much change will there be in the bond’s

price?

A. 1.83%

B. 2.01%

C. 3.27%

D. 6.44%

According to the Capital Asset Pricing Model (CAPM), overpriced securities have

A. positive betas.

B. zero alphas.

C. negative alphas.

D. positive alphas.

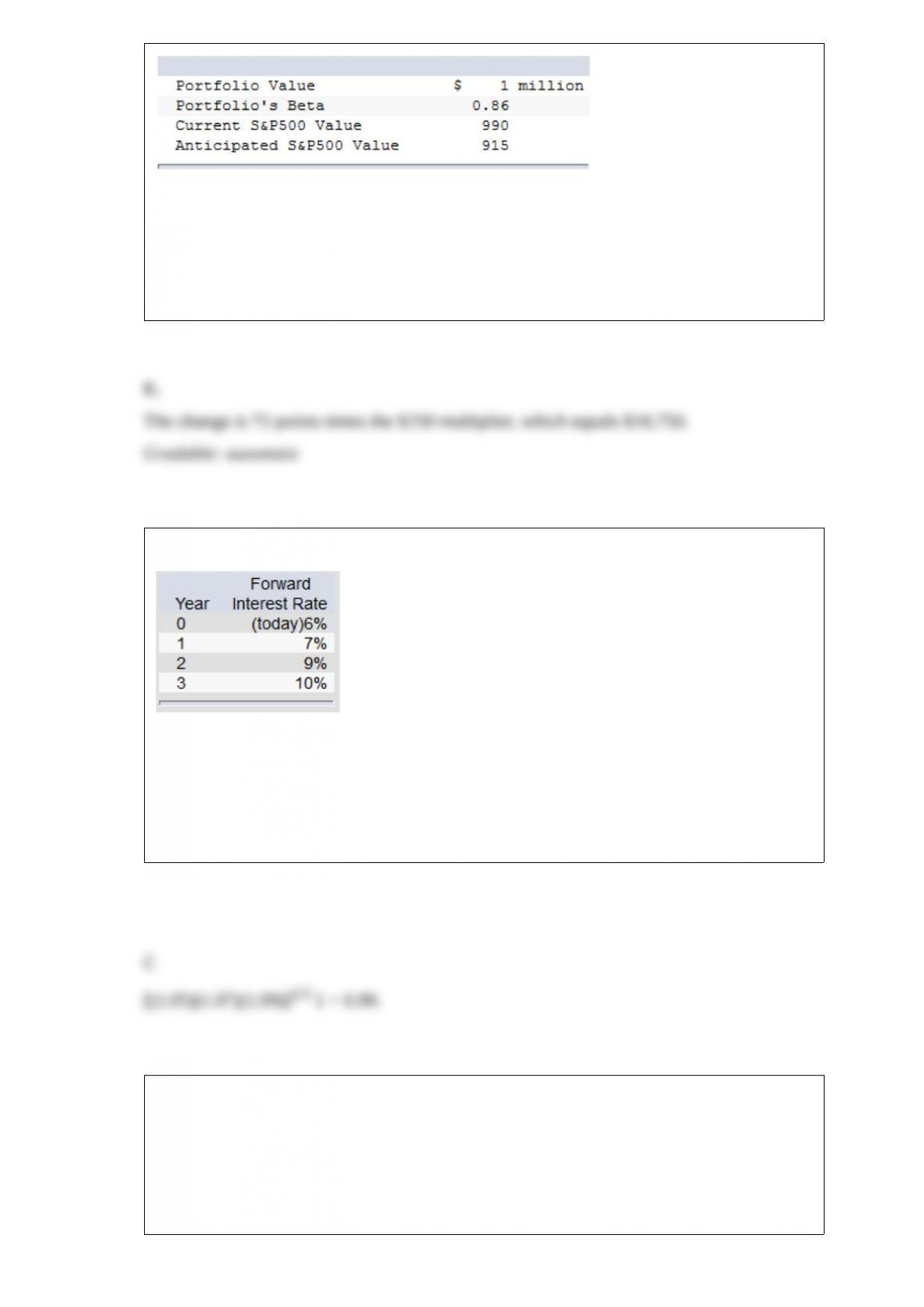

You are given the following information about a portfolio you are to manage. For the

long term, you are bullish, but you think the market may fall over the next month.

For a 75-point drop in the S&P 500, by how much does the futures position change?

A. $200,000

B. $50,000

C. $250,000

D. $500,000

E. $18,750

Suppose that all investors expect that interest rates for the 4 years will be as follows:

What is the yield to maturity of a 3-year zero-coupon bond?

A. 7.03%

B. 9.00%

C. 6.99%

D. 7.49%

E. None of the options are correct.

All else equal, call option values are lower

A. in the month of May.

B. for low dividend-payout policies.

C.for high dividend-payout policies.

D. in the month of May and for low dividend-payout policies.

E. in the month of May and for high dividend-payout policies.

Which of the following bonds has the longest duration?

A. A 12-year maturity, 0% coupon bond.

B. A 12-year maturity, 8% coupon bond.

C. A 4-year maturity, 8% coupon bond.

D. A 4-year maturity, 0% coupon bond.

E. Cannot tell from the information given

Equity premium puzzle studies may be subject to survivorship bias because

A. the time period covered was not long enough.

B. an inappropriate index was used.

C. the indexes used did not exist for the whole period of the study.

D. both U.S. and foreign data were used.

E. only U.S. data was used.

Since 1955, Treasury bond yields and earnings yields on stocks have been

A. identical.

B. negatively correlated.

C. positively correlated.

D. uncorrelated.

You invest $100 in a risky asset with an expected rate of return of 0.11 and a standard

deviation of 0.20 and a

T-bill with a rate of return of 0.03.

What percentages of your money must be invested in the risky asset and the risk-free

asset, respectively, to

form a portfolio with an expected return of 0.08?

A. 85% and 15%

B. 75% and 25%

C. 62.5% and 37.5%

D. 57% and 43%

E. Cannot be determined.

Which of the following are not true regarding the Treynor-Black model?

A. It considers both macroeconomic and microeconomic risks.

B. It considers security selection only.

C. It is nearly impossible to implement.

D. It considers both macroeconomic and microeconomic risks, and it is nearly

impossible to implement.

E.It considers security selection only, and it is nearly impossible to implement.

There appears to be a role for a theory of active portfolio management because

A. some portfolio managers have produced sequences of abnormal returns that are

difficult to label as lucky

outcomes.

B.the “noise” in the realized returns is enough to prevent the rejection of the hypothesis

that some money

managers have outperformed a passive strategy by a statistically small, yet economic,

margin.

C.some anomalies in realized returns have been persistent enough to suggest that

portfolio managers who

identified these anomalies in a timely fashion could have outperformed a passive

strategy over prolonged

periods.

D.some portfolio managers have produced sequences of abnormal returns that are

difficult to label as lucky

outcomes, and the “noise” in the realized returns is enough to prevent the rejection of

the hypothesis that

some money managers have outperformed a passive strategy by a statistically small, yet

economic, margin.

E.All of the options are correct.

The Black-Litterman model is geared toward ____________ while the Treynor-Black

model is geared toward

____________.

A. security analysis; security analysis

B. asset allocation; asset allocation

C. security analysis; asset allocation

D. asset allocation; security analysis

E. None of the options are correct.

The intrinsic value of an in-of-the-money call option is equal to

A. the call premium.

B. zero.

C. the stock price minus the exercise price.

D. the striking price.

E. None of the options are correct.

The _________ is the fraction of earnings reinvested in the firm.

A. dividend payout ratio

B. retention rate

C. plowback ratio

D. dividend payout ratio and plowback ratio

E. retention rate or plowback ratio

If a firm’s beta was calculated as 1.6 in a regression equation, a commonly-used

adjustment technique would provide an adjusted beta of

A. less than 0.6 but greater than zero.

B. between 0.6 and 1.0.

C. between 1.0 and 1.6.

D. greater than 1.6.

E. zero or less.

Cumulative abnormal returns (CAR)

A. are used in event studies.

B. are better measures of security returns due to firm-specific events than are abnormal

returns (AR).

C. are cumulated over the period prior to the firm-specific event.

D. are used in event studies and are better measures of security returns due to

firm-specific events than are abnormal returns (AR).

E. are used in event studies and are cumulated over the period prior to the firm-specific

event.

An important difference between CAPM and APT is

A. CAPM depends on risk-return dominance; APT depends on a no-arbitrage condition.

B. CAPM assumes many small changes are required to bring the market back to

equilibrium; APT assumes a few large changes are required to bring the market back to

equilibrium.

C. implications for prices derived from CAPM arguments are stronger than prices

derived from APT arguments.

D. Both CAPM depends on risk-return dominance; APT depends on a no-arbitrage

condition and CAPM assumes many small changes are required to bring the market

back to equilibrium; APT assumes a few large changes are required to bring the market

back to equilibrium.

E. All of the options are true.

______ uses quantitative techniques, and often automated trading systems, to seek out

many temporary misalignments among securities.

A. Covered interest arbitrage

B. Locational arbitrage

C. Triangular arbitrage

D. Statistical arbitrage

E. All arbitrage

An investor purchased a bond 63 days ago for $980. He received $17 in interest and

sold the bond for $987.

What is the holding-period return on his investment?

A. 1.52%

B. 2.45%

C. 1.92%

D. 2.68%

________ refers to sorting through huge amounts of historical data to uncover

systematic patterns in returns that can be exploited by traders.

A. Data mining

B. Pairs trading

C. Alpha transfer

D. Beta shifting

The risk-free rate is 4%. The expected market rate of return is 11%. If you expect CAT

with a beta of 1.0 to offer

a rate of return of 13%, you should

A. buy CAT because it is overpriced.

B. sell short CAT because it is overpriced.

C. sell short CAT because it is underpriced.

D. buy CAT because it is underpriced.

E. None of the options, as CAT is fairly priced.

Consider a bond selling at par with modified duration of 22 years and convexity of 415.

A 2% decrease in yield would cause the price to increase by 44% according to the

duration rule. What would be the percentage price change according to the

duration-with-convexity rule?

A. 21.2%

B. 25.4%

C. 17.0%

D. 52.3%