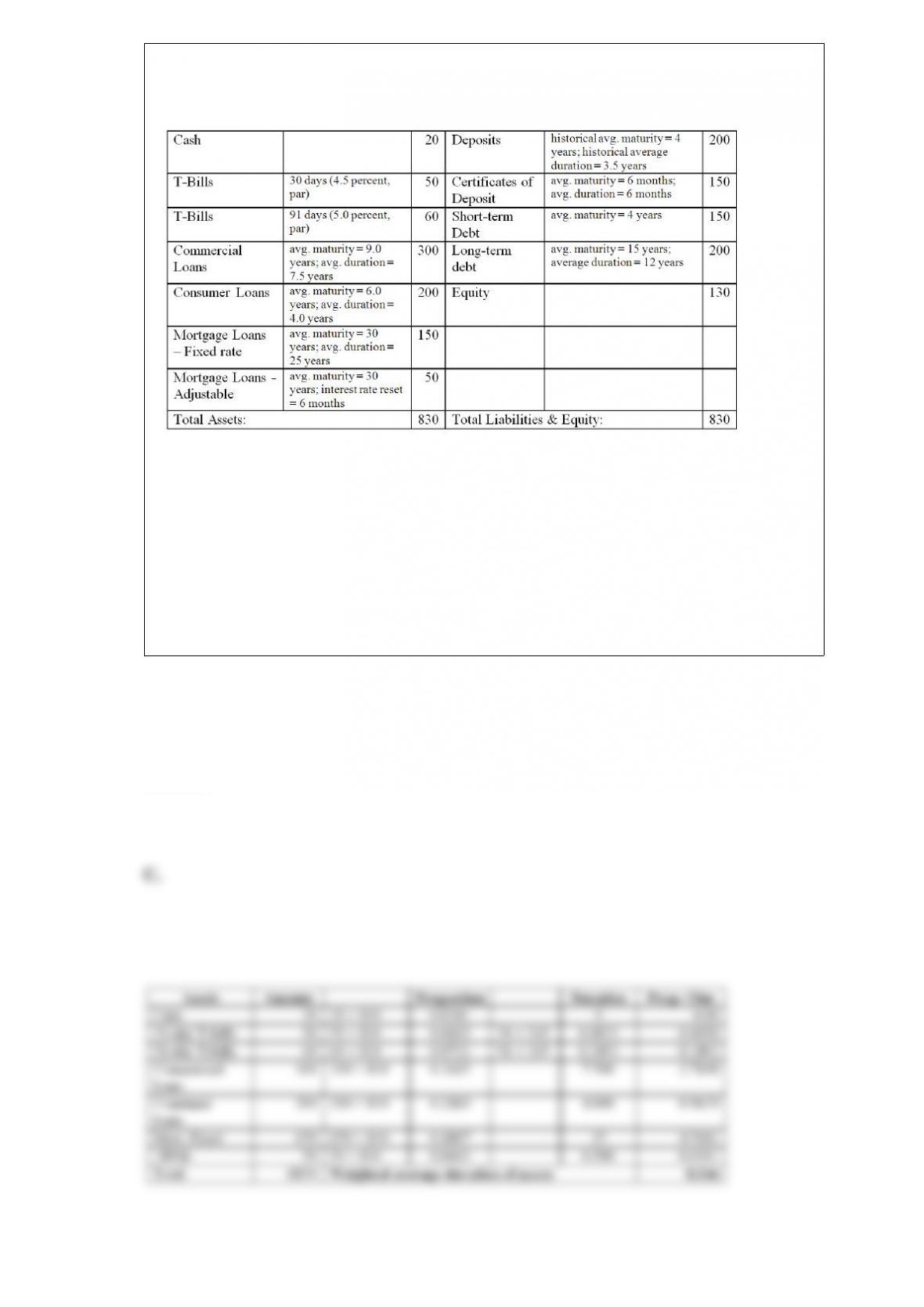

The numbers provided are in millions of dollars and reflect market values:

What is

the weighted average duration of the assets of the FI?A. 7.25 years.

B. 7.75 years.

C. 8.25 years.

D. 8.75 years.

E. 9.25 years.

Answer:

The following information is for a collateralized mortgage obligation (CMO). Tranche

A has a face value of $110 million and pays 5 percent annually. Tranche B has a face

value of $90 million and pays 7 percent annually.

If at the end of the first year, the CMO trustee receives total cash flows of $15 million,

how are they distributed? A. $7.5 million to Tranche A and $7.5 million to Tranche B.

B. $15 million to Tranche A and nothing to Tranche B.

C. $5.5 million to Tranche A and $9.5 million to Tranche B.

D. $8.7 million to Tranche A and $6.3 million to Tranche B.

E. $7.1 million to Tranche A and $7.9 million to Tranche B.

Answer:

What is the portfolio weight of the Japanese yen in this FI’s portfolio of foreign

currency?A. +0.18 percent.

B. -36.62 percent.

C. +75.20 percent.

D. -5.47 percent.

E. +66.70 percent.

Answer:

According to SEC Rule 415, A. larger corporations can register their new issues with

the SEC up to two years in advance.

B. firms should disclose soft dollar arrangements to their clients.

C. large investors are allowed to begin trading privately placed securities among

themselves.

D. firms are required to maintain records of the information used to verify the identity

of a person opening an account.

E. publicly held companies must disclose all material information that might affect

investment decisions to all investors at the same time.

Answer:

A thrift has funded 10 percent fixed-rate assets with variable-rate liabilities at LIBOR +

2 (L + 2) percent. A bank has funded variable-rate assets with fixed-rate liabilities at 6

percent. The bank’s variable-rate assets earn LIBOR + 1 (L + 1) percent. The thrift and

the bank have reached agreement on an interest-rate swap with the fixed-rate swap

payment at 6 percent and the variable-rate swap payment at LIBOR.

What will be the net after-swap cost of funds for the thrift if the cash market liabilities

are included in the analysis? A. Variable-rate at LIBOR.

B. Fixed-rate at 8 percent.

C. Fixed-rate at 1 percent.

D. Fixed-rate at 2 percent.

E. None of the above.

Answer:

An investment banker agrees to underwrite an issue of 5 million shares of stock for

NetChoice, Inc. on a best-efforts basis. The investment banker is able to sell 4.5 million

shares for $31.00 per share and it charges NetChoice, Inc. $0.375 per share sold.

How much money does NetChoice, Inc. receive? A. $139,500,500.

B. $137,812,500.

C. $155,000,000.

D. $153,125,000.

E. $105,000,000.

Answer:

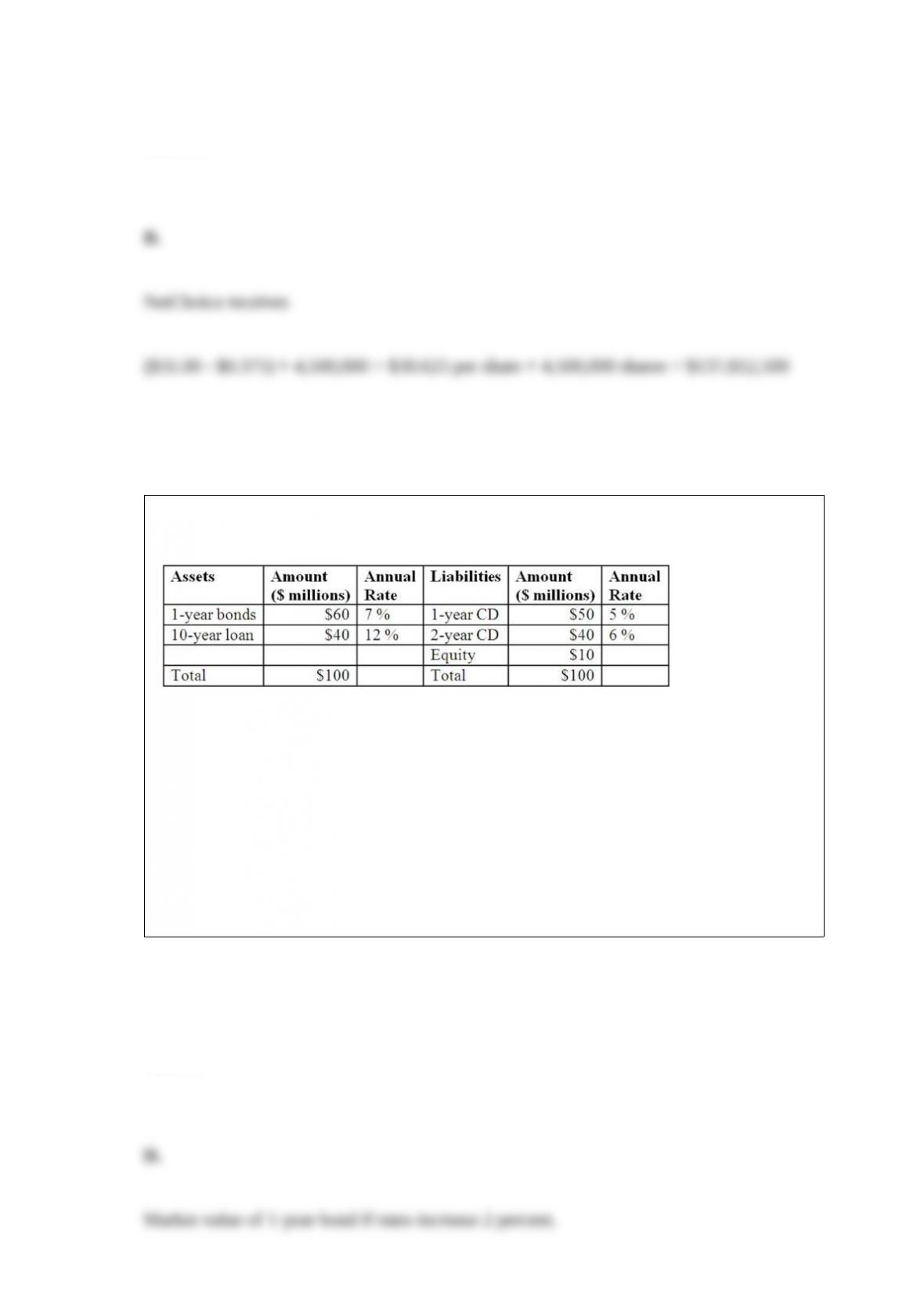

Hadbucks National Bank current balance sheet appears below. All assets and liabilities

are currently priced at par and pay interest annually.

What is market

value of the one-year bond if all market interest rates increase by 2 percent? A. $60.000

million.

B. $60.566 million.

C. $59.444 million.

D. $58.899 million.

E. $61.142 million.

Answer:

What does the loss ratio measure in any particular year? A. Payouts on policies to

premiums earned.

B. Amount of premiums earned relative to the payout on policies.

C. Overall underwriting profitability of a line.

D. Loss adjustment expenses to premiums earned.

E. Commission and other acquisition costs to premiums written.

Answer:

If over the first 12 days of the current reserve maintenance period the average daily

reserve held were $37 million, what does the bank need to hold as reserves over the last

two days to meet the maximum reserve? A. $125.552 million.

B. $111.453 million.

C. $135.690 million.

D. $141.914 million.

E. $129.110 million.

Answer:

The changes implemented by the Fed in January 2003 to its discount window lending

A. decreased the cost of borrowing.

B. eased the terms of borrowing.

C. terms of borrowing became less flexible.

D. resulted in reduction of outstanding discount loan volumes.

E. None of the above.

Answer:

Match the following pieces of legislation with the function achieved by each regulation

as stated in question

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Advisers Act

D. Investment Company Act

E. Insider Trading and Securities Fraud Enforcement Act of 1988

F. Market Reform Act of 1990

G. National Securities Markets Improvement Act of 1996

Requires a mutual fund to furnish full and accurate information on all financial and

corporate matters to prospective fund purchasers.

Answer:

The bank would like to limit the average return (both explicit and implicit) earned by

the account holder to 5 percent per year. How much should it charge for processing

each check to this Account holder assuming that it will pay annual interest of 5 percent

and minimum balances of $200 are maintained?A. 1 cent per check.

B. 2 cent per check.

C. 3 cent per check.

D. 4 cent per check.

E. 5 cent per check.

Answer:

Contrast the marking to market characteristics of options versus futures contracts. A.

Options are marked to market continuously while futures are marked to market at the

close of trading each day.

B. Options are marked to market at expiration while futures are marked to market at

the close of trading each day.

C. Options are marked to market daily while futures are marked to market at the close

of trading each day.

D. Options are marked to market monthly while futures are marked to market at the

close of trading each day.

E. There is no difference in the marking to market characteristics.

Answer:

Financial futures can be used by FIs to manage A. credit risk.

B. interest rate risk.

C. liquidity risk.

D. foreign exchange risk.

E. Answers A, B, and D only.

Answer:

The underlying GNMA 15-year mortgage pool has a principal amount of $50 million

and an annual yield of 6 percent (paid monthly). Assume that there are no prepayments.

What is the first monthly payment on the Principal Only (PO) strip?A. $3 million.

B. $421,928.

C. $250,000.

D. $299,775.

E. $171,928.

Answer:

Since 1998, interest rate variability in the fed funds market has decreased because A.

fewer institutions were allowed to participate in the fed funds market.

B. of the introduction of lagged reserve accounting.

C. new securities were approved that participants can use instead of fed funds to meet

liquidity needs.

D. of the introduction of contemporaneous reserve accounting.

E. more participants were allowed to enter the fed funds market.

Answer:

According to this credit scoring model, the variable that has the highest positive impact

on the probability of rescheduling isA. debt service ratio.

B. import ratio.

C. investment ratio.

D. variance of export revenue.

E. rate of growth of the domestic money supply.

Answer:

Which method is preferable, between the loan commitment and the standby letter of

credit? A. The loan commitment is preferable because the savings are greater.

B. The standby letter of credit is preferable because the savings are greater.

C. The loan commitment is preferable it has a lower risk of default.

D. The standby letter of credit is preferable because it has a lower risk of default.

E. The loan commitment is preferable because the back-end fee is payable at the end of

the year.

Answer:

Home equity loans have A. become less profitable for finance companies.

B. seen reduced demand since the Tax Reform Act of 1986 was passed.

C. interest charges that are not tax deductible.

D. a higher bad debt expense than those on other finance company loans.

E. allows customers to borrow on a line of credit secured with a second mortgage on

their home.

Answer:

Which of the following is consistent with economies of scope? The subscript “b” refers

to a banking firm, ‘s” for a securities firm, “AC” is average costs and “TC” is total costs.

A. ACb + s > ACb + ACs.

B. ACb + s = ACb + ACs.

C. ACb + s < ACb + ACs.

D. TCb + s < TCb + TCs.

E. TCb + s > TCb + TCs.

Answer:

Which of the following is the legislation that required bank regulators to incorporate

credit concentration risk into their evaluation of bank insolvency risk. A. The Bank

Holding Company Act (1956).

B. FDIC Improvement Act (1991).

C. Depository Institutions Deregulation and Monetary Control Act (1980).

D. Garn-St. Germain Depository Institutions Act (1982).

E. Financial Institutions Reform Recovery and Enforcement Act (1989).

Answer:

What is the risk (standard deviation of returns) on the bank’s loan portfolio if loan

returns are uncorrelated (ρ = 0)?A. 1.41 percent.

B. 1.63 percent.

C. 0.93 percent.

D. 3.57 percent.

E. 1.18 percent.

Answer:

Which of the following is a method that may overcome weaknesses in the historic or

back simulation model? A. The use of smaller sample sizes to estimate return

distributions.

B. Weight sample size observations so that the more recent observations contribute a

larger amount to the model.

C. Decrease the number of assets in the trading portfolio so that past returns will

provide more accuracy to the model.

D. Increase the number of assets in the trading portfolio in order to benefit from higher

levels of diversification.

E. The weaknesses in the model cannot be overcome.

Answer:

If the manager buys a one-year option with an exercise price equal to the expected price

of the bond in one year, what will be the exercise price of the option? A. $862.10.

B. $743.23.

C. $900.93.

D. $811.70.

E. $917.36.

Answer:

Which of the following is NOT a differentiation between deposit insurance and state

guaranty funds for the insurance industry? A. The required contributions provided by

surviving insurers differs widely across states.

B. The annual pro rata contributions often are legally capped for each insurer as a

percent of premium income.

C. A permanent guaranty fund does not exist for the insurance industry.

D. Contributions by surviving firms into the guaranty fund occur before an insurance

company has failed.

E. The programs that are sponsored by state insurance regulators are administered by

private insurance companies.

Answer:

When the assets and liabilities of an FI are not equal in size, efficient hedging of

interest rate risk can be achieved by A. increasing the duration of assets and increasing

the duration of equity.

B. issuing more equity and reducing the amount of borrowed funds.

C. not exactly matching the maturities of assets and liabilities.

D. issuing more equity and investing the funds in higher-yielding assets.

E. efficient hedging cannot be achieved without the use of derivative securities.

Answer:

One of the primary reasons that investment banks were allowed to convert to bank

holding companies during the recent financial crisis was recognition that A. their

operating activities were too risky and they needed the cushion of bank deposits to

alleviate funding risks.

B. the industry had acquired too much capital during the previous decade.

C. bank holding companies needed the ability to underwrite new issues of corporate

securities.

D. it was the only way an investment bank could qualify for federal bailout funds.

E. the Federal Reserve was unable to purchase troubled assets from investment banks,

but they could from bank holding companies.

Answer:

The implementation of BIS capital requirements may be expected to A. increase the

downward trend in loan sales because of higher required capital levels.

B. increase the downward trend in loan sales because of the use of risk adjusted assets.

C. decrease the downward trend in loan sales because of the use of risk adjusted assets.

D. decrease the downward trend in loan sales because of higher required capital levels.

E. Answers C and D only.

Answer:

All of the following are examples of participants in the shadow banking system

EXCEPT A. money market mutual funds (MMMFs).

B. structured investment vehicles (SIVs).

C. credit hedge funds.

D. limited-purpose finance companies.

E. credit unions.

Answer:

An FI purchases at par value a $100,000 Treasury bond paying 10 percent interest with

a 7.5 year duration. If interest rates rise by 4 percent, calculate the bond’s new value.

Recall that Treasury bonds pay interest semiannually. Use the duration valuation

equation. A. $28,572

B. $20,864

C. $15,000

D. $22,642

E. $71,428

Answer: