1) Financial reporting assists statement users to forecast future cash flows by providing

an income statement format that segregates components of income.

2) Research indicates that fewer firms report slightly negative earnings than slightly

positive earnings, suggesting that managers of firms that would otherwise report a slight

loss are finding ways to prop up earnings.

3) A periodic inventory system is preferable if avoiding ‘stock-outs” is of paramount

importancefor example in manufacturing firms that use just-in-time systems.

4) With respect to revenue generated by selling goods, IFRS prescribes that revenue

should be recognized using the percentage-of-completion method.

5) Some companies have adopted formal “compensation recovery” policies whereby

executives forfeit various incentive payments if it is later discovered that they engaged

in conduct detrimental to the company.

6) Riskier firms have a lower risk-adjusted cost of capital resulting in lower share prices

for those companies.

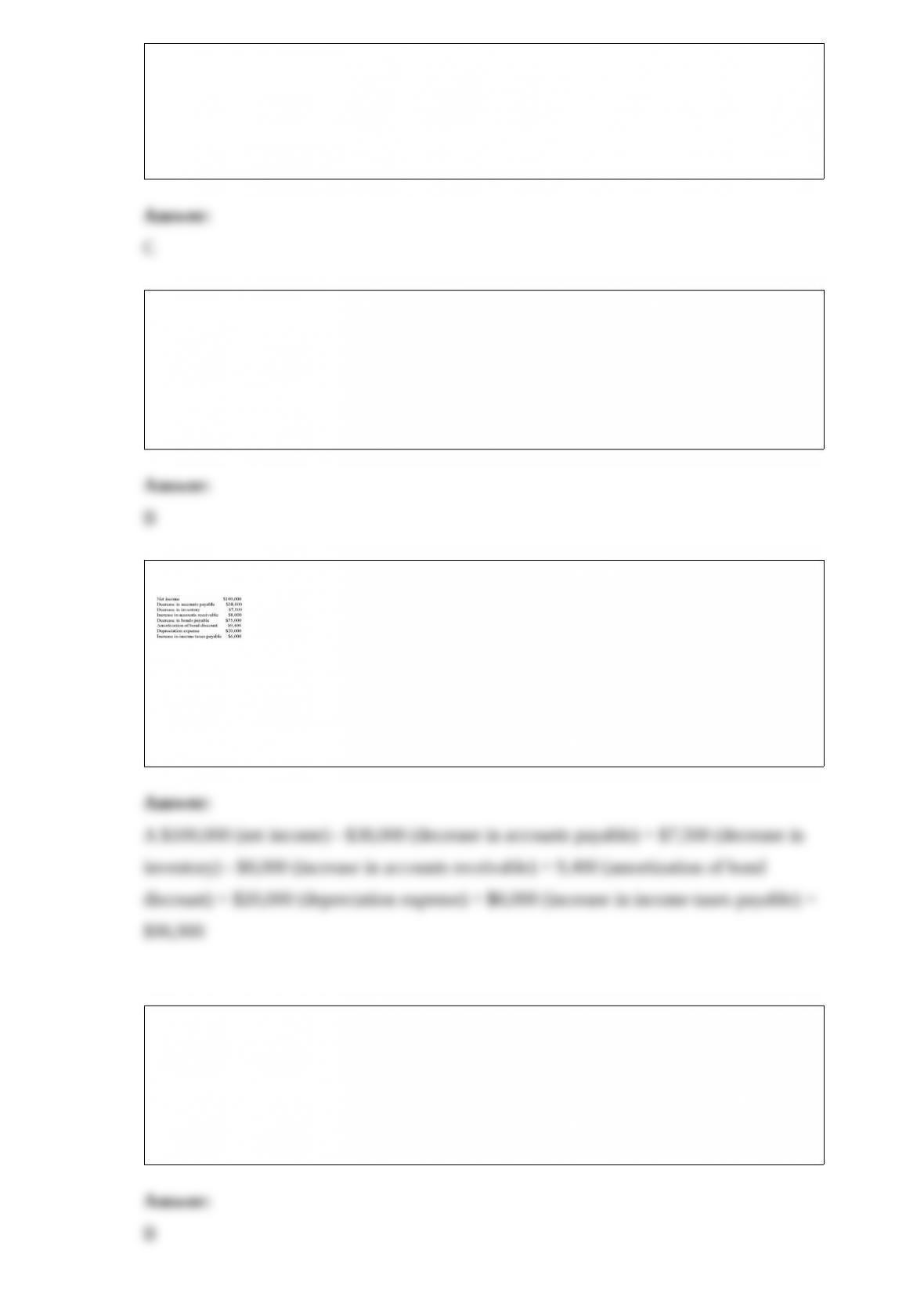

7) Cash collected from customers can be derived by appropriately adjusting revenue for

changes in accounts receivable.

8) For a lessee, the current ratio deteriorates with a capitalized lease.

9) The gross accounts receivable approach is consistent with the accrual accounting

philosophy of recording estimated bad debt expense when the sale was made.

10) To avoid providing an incentive for managers to engage in intentional LIFO

liquidation, bonus contracts should subtract out LIFO liquidation profits.

11) Investors are uncertain about the quality of each company’s debt or equity offerings

because the ultimate return from the security depends on the company’s past

performance which is difficult to accurately measure.

12) Book value reflects the economic worth of an asset.

13) The role of financial accounting information is to facilitate economic transactions

and to foster efficient allocation of resources among businesses and individuals.

14) Established growth companies require substantial investments in property, plant,

and equipment at a stage when operating cash flows are typically negative.

15) A firm with most of its assets invested in manufacturing facilities has considerable

operating flexibility.

16) Under U.S. GAAP, current assets are generally listed on the balance sheet in

descending order of liquidity.

17) The Common Stock account is reported on the balance sheet at the current market

price of the stock.

18) Current GAAP requires that share-based compensation be expensed at the grant

date of the stock options award.

19) Being verifiable and neutral is part of what makes financial information

A.useful

B.consistent

C.comparable

D.relevant

20) Based on a comprehensive survey of U.S. companies, the most common

performance measure used in annual and long-term incentive plans for senior

executives is

A.return on equity

B.economic value added

C.return on capital

D.net income or revenues

21) The ability to raise additional cash by selling assets, issuing stock, or borrowing

more is

A.financial flexibility

B.a credit risk indicator

C.a stock price predictor

D.one way to project earnings

22) Island Corporation owes Mutual Bank a 10% note payable for $100,000 plus

$8,000 accrued interest on October 1, 2011 . Island and Mutual Bank enter into an

agreement whereby Island will pay Mutual $128,000 on the due date of the note on

October 1, 2013 .

What will be Island’s carrying value of the restructured note?

A.$100,000

B.$108,000

C.$118,000

D.$128,000

23) Regal has elected the fair value option to account for equity method investments.

The fair value of the Air investment as of December 31, 2012 was $295,000. The

income reported by Regal during 2012 pertaining to the Air investment was

A.$9,000

B.$22,500

C.$19,500

D.$4,000

24) To apply the discounted free cash flow approach, the analyst needs to estimate

A.net cash flows from operations for each and every future period, starting one year

hence

B.free cash flows for each and every future period, starting one year hence

C.free cash flows for approximately ten years as the present value of cash flows

occurring beyond that point are insignificant

D.net cash flows from operations for approximately ten years as the present value of

cash flows occurring beyond that point are insignificant

25) Smith Company reported $350,000 in book income before income tax during 2012,

its first year of operation. The tax depreciation exceeded its book depreciation by

$30,000. The tax rate for 2012 and all future years was 40%.

What amount of deferred income tax liability should Smith report in its December 31,

2012, balance sheet?

A.$8,000

B.$9,000

C.$10,000

D.$12,000

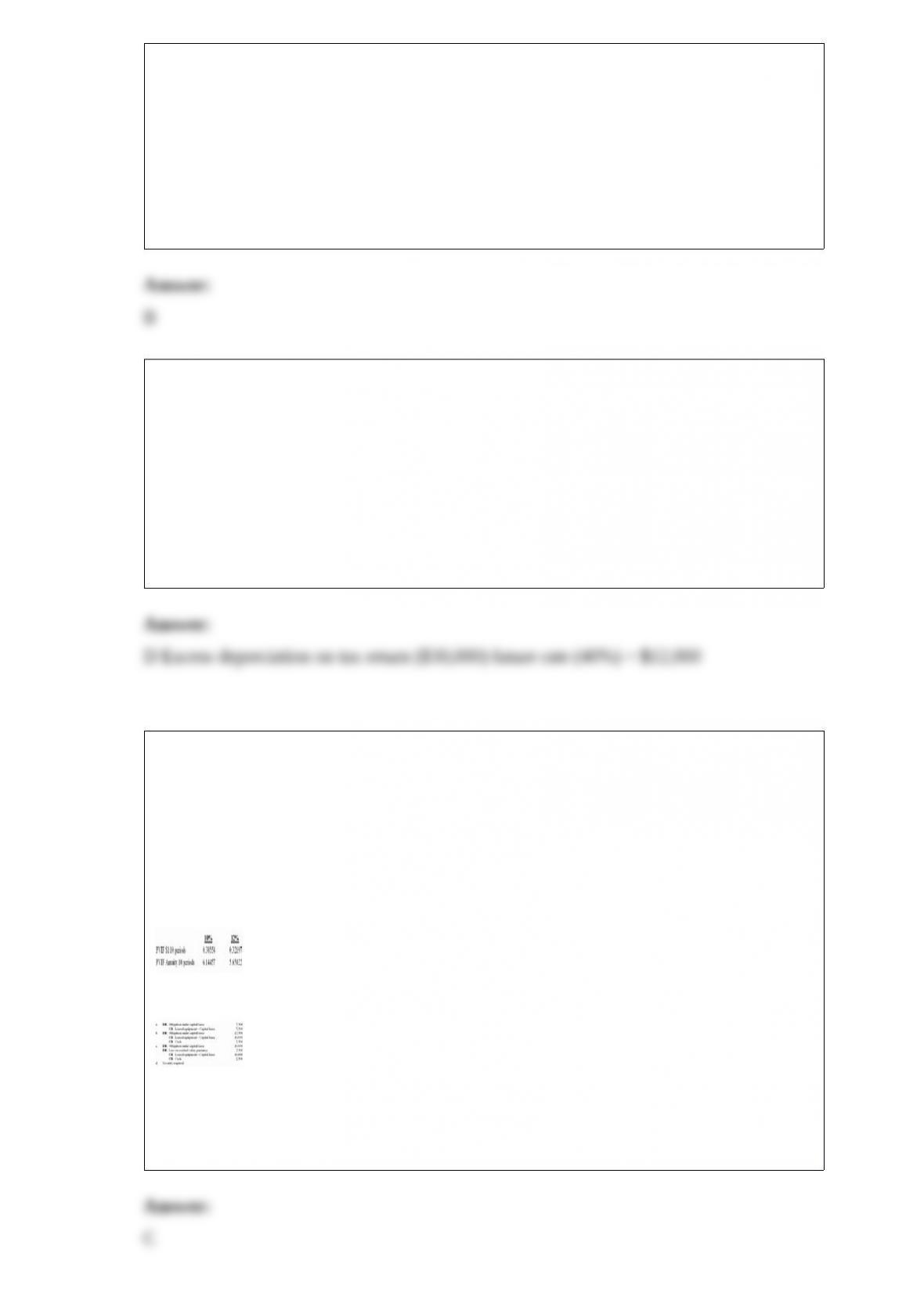

26) Pepper, Inc. agrees to lease equipment from the Blue Corporation for 10 years at

$25,000 at the end of each year. The equipment has a fair value of $175,000 and an

estimated useful life of 10 years. The lease includes a guaranteed residual value of

$10,000. In addition to the lease payments, Pepper will pay $5,000 per year for a

maintenance agreement. Pepper can finance this lease with its bank at a 12% rate. The

lessor’s implicit lease rate, known to the lessee, is 10%. Round all calculations to the

nearest whole dollar amount.

Present value interest factors are:

If the equipment is worth $7,500 at the end of the lease, Pepper will make which one of

the following journal entries?

A.Option a

B.Option b

C.Option c

D.Option d

27) According to the abnormal earnings approach of equity valuation, investors

willingly pay a premium for those firms that

A.earn less than the cost of equity capital

B.produce negative abnormal earnings

C.produce positive abnormal earnings

D.earn an amount equal to the equity cost of capital

28) Operating cash flows are typically negative for

A.established growth companies

B.emerging companies

C.mature companies

D.blue-chip companies

29) The net present value of future growth opportunities (NPVGO) will contribute to an

above average P/E multiple when the additional share value created is

A.positive and the return on new investment is lower than the cost of equity capital

B.positive and the return on new investment is greater than the cost of equity capital

C.negative and the return on new investment is lower than the cost of equity capital

D.negative and the return on new investment is greater than the cost of equity capital

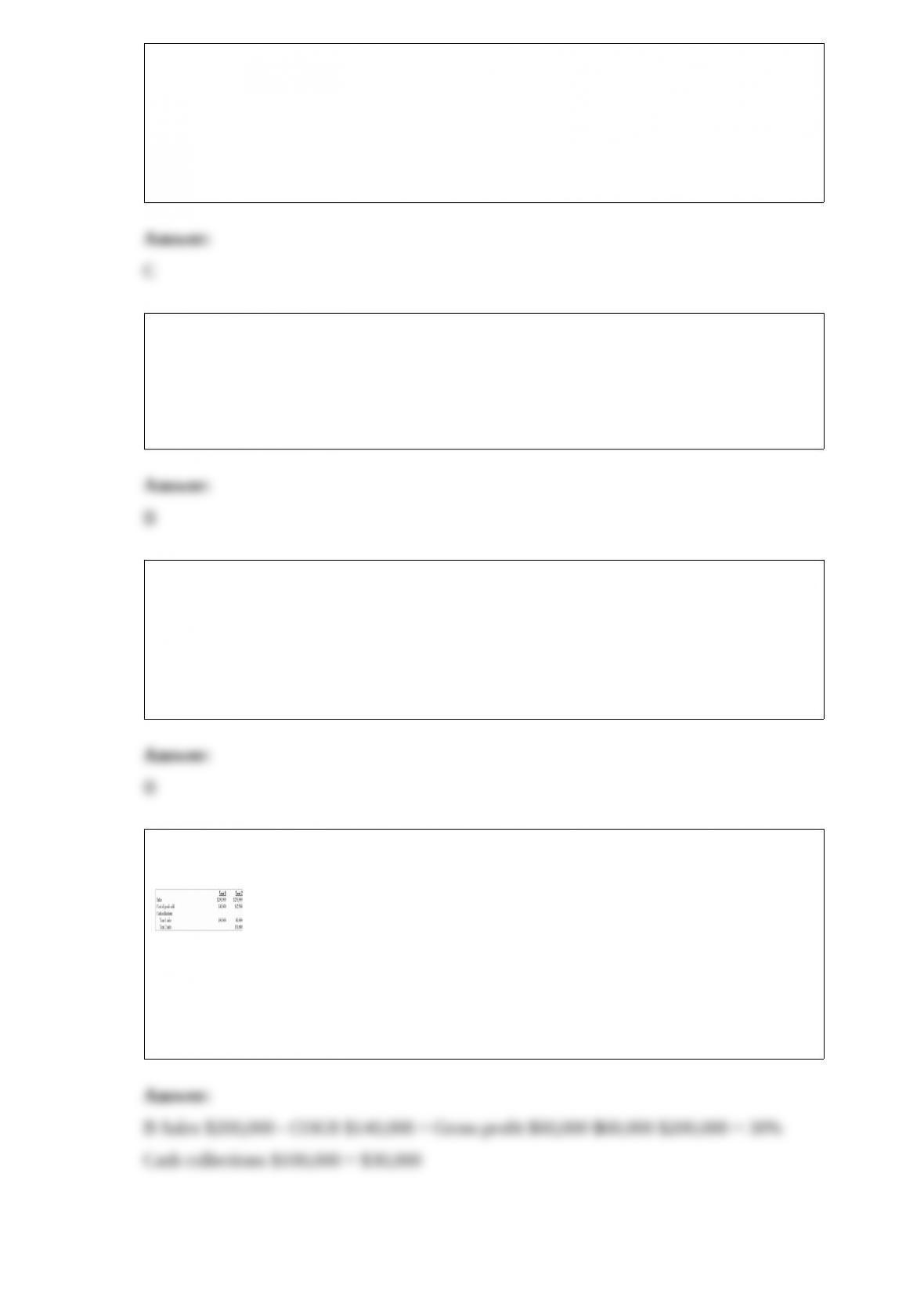

30) Ford Appliance Center records revenue on the installment sales method. The

following information is available for the first two years of business.

How much realized gross profit on installment sales will Ford recognize in Year 1?

A.$20,000

B.$30,000

C.$60,000

D.$100,000

31) The unpaid amount of income taxes due to the government for a given year are

found on the

A.balance sheet in the account Deferred Income Taxes

B.balance sheet in the account Income Taxes Payable

C.income statement in the account Income Tax Expense Current

D.income statement in the account Income Tax Expense Deferred

32) The size of the divergence between FIFO cost of goods sold and replacement cost

of goods sold depends on the rapidity of the inventory turnover and the

A.change in accounts receivable turnover

B.divergence of total asset turnover from previous periods

C.severity of input cost change

D.rapidity of fixed asset turnover

33) The Ness Company sells $5,000,000 of five-year, 10% bonds at the start of the year.

The bonds have an effective yield of 9%. Present value factors are below:

The amount of bond interest expense for Year 2 is

A.$450,000

B.$464,578

C.$500,000

D.$535,422

34) Transitory earnings components fall into all of the following categories except

A.special or unusual items

B.discontinued operations

C.extraordinary items

D.cumulative effect of accounting changes

35) A hedged item can be any of the following except:

A.an anticipated (forecasted) transaction

B.an existing asset or liability on the company’s books

C.a past transaction

D.a firm commitment

36) If the proper correcting entries were made at the end of 2010, how much will 2011

income before taxes be overstated or understated?

A.$2,000 understated

B.$2,000 overstated

C.$10,000 understated

D.$10,000 overstated

37) The FASB justified expensing research and development costs for all of the

following reasons except

A.The future benefits accruing from these expenditures are highly uncertain

B.Expensing R&D conforms to the conservatism principle

C.A causal relationship between current R&D and future revenue has not been

demonstrated

D.Whatever benefits may arise cannot be objectively measured

38) Cash flow assessment plays a central role in analyzing

A.the credit risk of a company

B.management’s effectiveness

C.the future earnings potential of a company

D.the company’s investment potential

39) When a company uses absorption costing

A.only fixed costs are inventoried

B.only variable costs are inventoried

C.all production costs are inventoried

D.fixed costs are expensed as incurred

40) When a bond is sold at a discount the effective interest rate is

A.equal to the stated rate

B.above the stated rate

C.below the stated rate

D.equal to the stated rate for a period of time and then above the stated rate for a period

of time

41) The following information has been provided to you by your controller:

What is the net cash flow from operating activities?

A.$96,900

B.$97,900

C.$112,900

D.$94,100

42) The ratio that captures information about property, plant, and equipment utilization

is

A.current asset turnover

B.long-term asset turnover

C.asset turnover

D.property turnover

43) The components of pension expense are

A.service cost, plus interest cost, plus net amortization

B.service cost, plus interest cost, plus return on plan assets, plus net amortization

C.service cost, plus interest cost, minus return on plan assets, plus (or minus) net

amortization

D.service cost, plus interest cost, minus return on plan assets, minus net amortization

44) Companies that fail to meet analysts’ earnings expectations are

A.often rewarded by investors

B.often penalized by investors

C.have had no consequences to the companies

D.forced into reorganization

45) GAAP’s goals are to ensure that financial statements

A.do not contain any representation that could jeopardize management

B.provide stockholders all of the information they need to assess management’s

performance

C.are accurate and free from fraud

D.clearly reflect the economic condition and performance of the company

46) Morey Corporation leases a tractor from Equity Leasing with a five-year

non-cancelable lease on January 1, 2011 under the following terms:

1> Five payments of $26,379.74 (a 9% implicit rate, known to Morey) due at the end

each year.

2> The payments were calculated based on the fair value (which is also the book value

for Equity) of the tractor.

3> The lease is nonrenewable and the tractor reverts to Equity at the end of the lease

term.

4> The tractor has a six-year economic life.

5> Morey has an excellent credit rating.

6> Equity offers no warranty on the tractor other than the manufacturer’s two-year

warranty that is handled directly with the manufacturer.

For Morey, this lease is treated as a/an

A.operating lease

B.capital lease

C.direct financing capital lease

D.sales-type capital lease

47) The weighted average number of common shares used to compute earnings per

share for 2011 is

A.100,000

B.102,500

C.105,000

D.110,000

48) Island Corporation owes Mutual Bank a 10% note payable for $100,000 plus

$8,000 accrued interest on October 1, 2011 . Island and Mutual Bank enter into an

agreement whereby Island will pay Mutual $128,000 on the due date of the note on

October 1, 2013 .

Mutual Bank will record this transaction to recognize

A.an extraordinary receivable restructuring gain of $2,214

B.an extraordinary debt restructuring loss of $2,214

C.neither a gain nor a loss from debt restructuring

D.an ordinary debt restructuring loss of $2,214

49) Analysts should expect to see stock option information in

A.the auditor’s report

B.a note to the financial statements

C.a separate report to the SEC

D.a separate report to shareholders

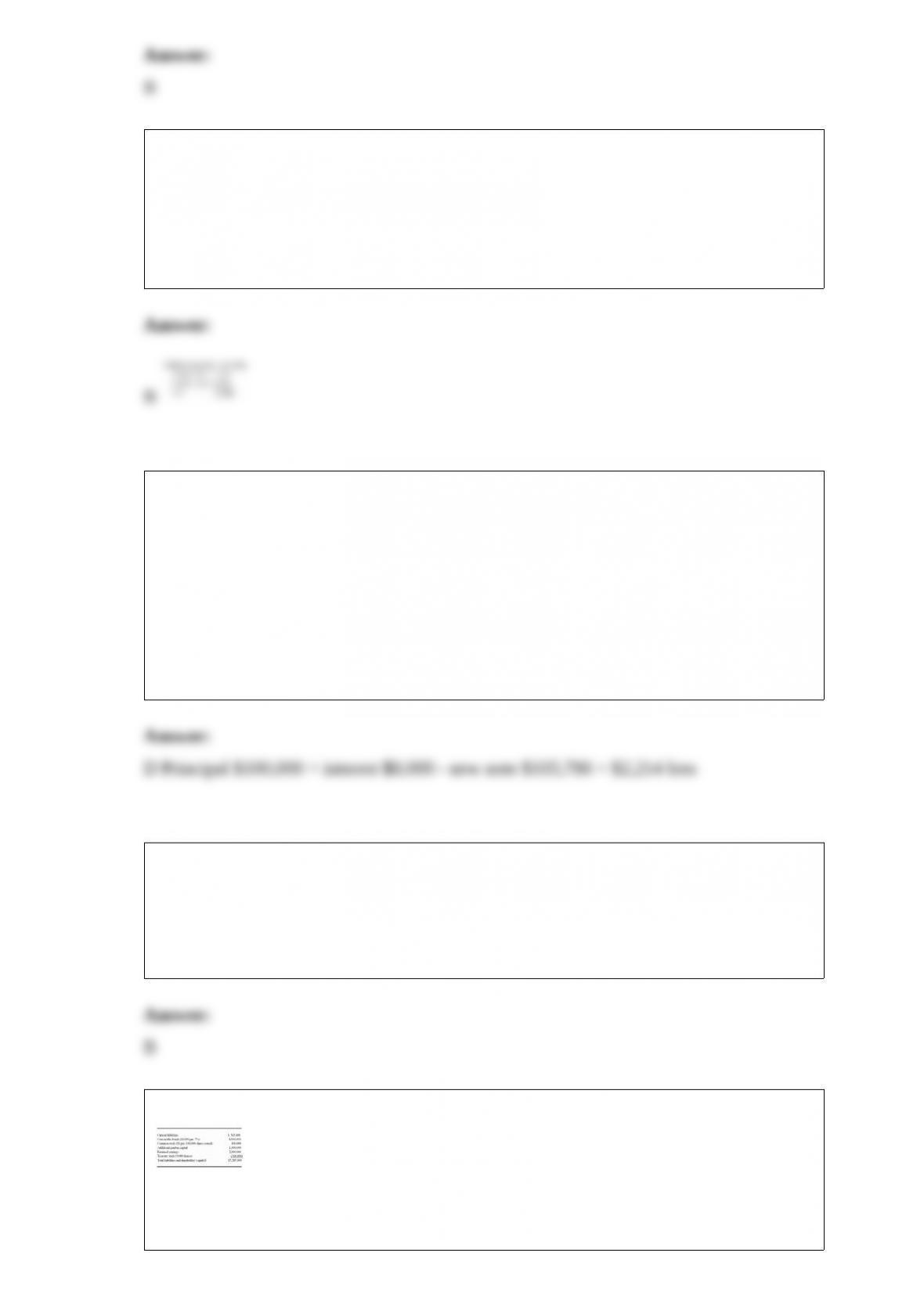

50) Prince Corp. has the following balance sheet information at December 31, 2011 .

The convertible bonds were issued at par on April 1, 2011 and are convertible into

Prince’s common stock at a ratio of 25 shares of stock to 1 bond. Prince did not have

any treasury stock at December 31, 2010 and purchased the 9,000 shares evenly

throughout 2011. The average price of the common stock for the year was $40, and the

year end price was $45.

Prince Corp. also has 60,000 outstanding and exercisable qualified employee stock

options. Employees obtain one share of stock for each option exercised. The exercise

price for each option is $21 per share.

Prince’s net income for the year ended 2011 was $292,500. Its tax rate for the year was

35%.

Required:

1> Compute basic EPS for the year ended December 31, 2011 . Show all computations.

2> Compute diluted EPS for the year ended December 31, 2011 . Show all

computations.

51) Investors who compare a firm’s discounted future cash flows to the current market

price of a stock are using the

A.efficient market hypothesis

B.market-to-market approach

C.fundamental analysis approach

D.technical analysis approach

52) The amount reported as net cash from investing activities is

A.$(175,000)

B.$(150,000)

C.$87,500

D.$575,000

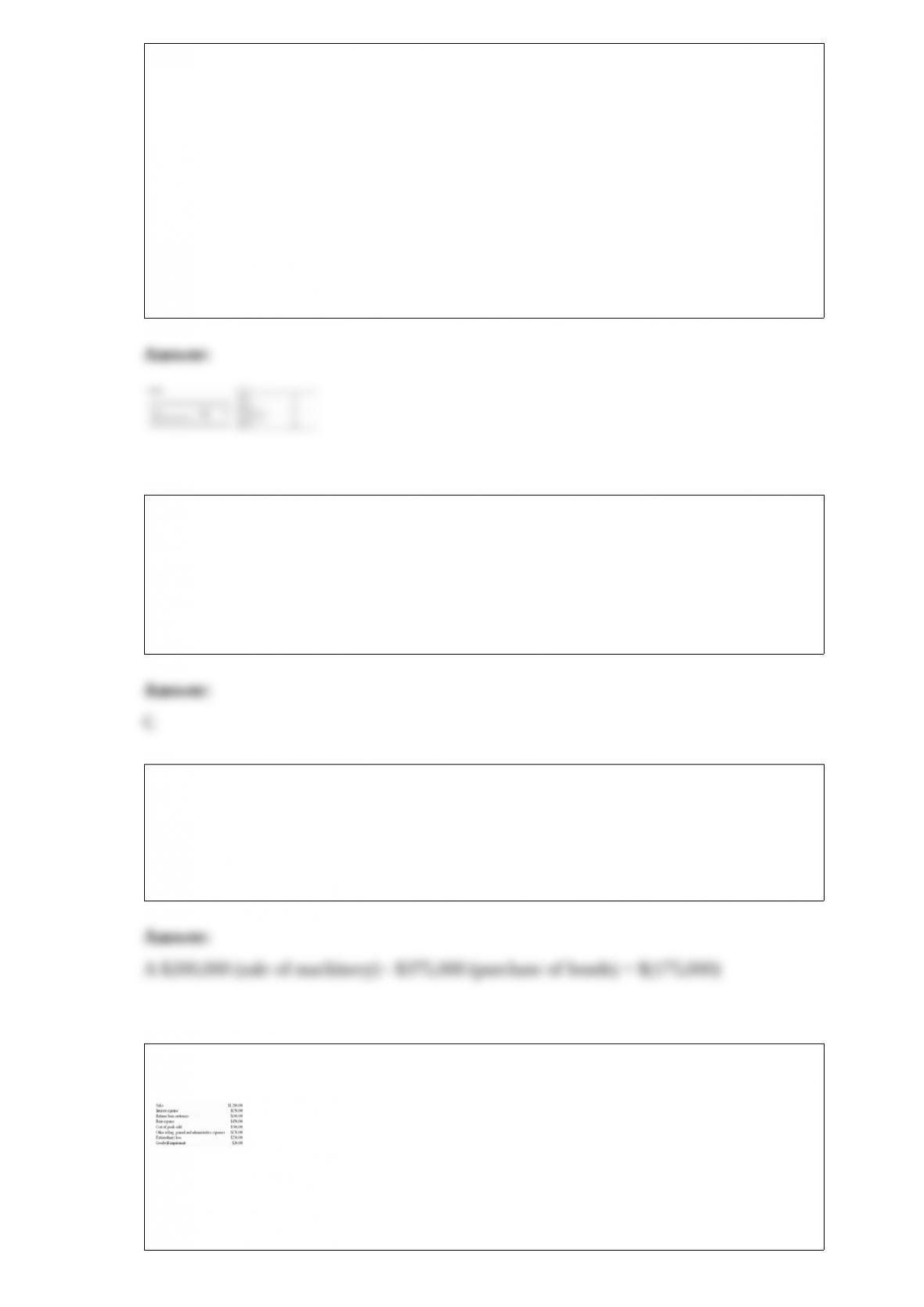

53) Lazer Industries, Inc. manufactures medical equipment parts and accessories.

Assume all amounts are pre-tax and a 30% tax rate for 2011 .

Required:

Provide a condensed income statement for Lazer Industries, Inc. based on the available

information. Include all subtotals needed (appropriately labeled) to present your income

statement in good form.

54) Explain the difference between affirmative and negative debt covenants and provide

two examples of each.

55) On January 1, 2012, Cole Corporation entered into a ten-year lease agreement. The

following summarizes the agreement:

Payments of $30,000 are due at the beginning of each year; the first payment was made

on January 1, 2012 .

The leased asset has an estimated useful life of 15 years.

Title to the leased asset is transferred to Cole at the end of the lease term.

The implicit interest rate known by Cole is 10%.

Cole’s incremental borrowing rate is 12%.

Cole uses the straight-line depreciation method.

The asset’s estimated salvage value is $50,000 after 10 years and is $15,000 after 15

years.

Required:

1> Determine the interest expense associated with the lease for the year ended

December 31, 2012 .

2> Determine the depreciation expense for the year ended December 31, 2012 .

56) Mercedes Company paid $20,000,000 to purchase 100% of the outstanding

common stock of Benz Incorporated on January 1, 2012 . The book value of Benz’s net

assets on the date of acquisition was $17,000,000. Benz’s buildings were undervalued

by $1,500,000 as of January 1, 2012; the buildings had a ten-year remaining life as of

the date of acquisition. All other assets and liabilities of Benz are being reported at

market value. Mercedes retained earnings as of January 1, 2012 was $5,750,000, while

Benz reported retained earnings of $3,175,000. Mercedes net income was $1,750,000

during 2012 and was $2,035,000 during 2013; the 2012 and 2013 net income amounts

did not include any amounts pertaining to the Benz investment. Benz’s retained earnings

increased $1,050,000 from January 1, 2012 to December 31, 2013 even though Benz

declared $225,000 of dividends during that two-year period.

Required:

Determine the December 31, 2013 consolidated retained earnings balance.

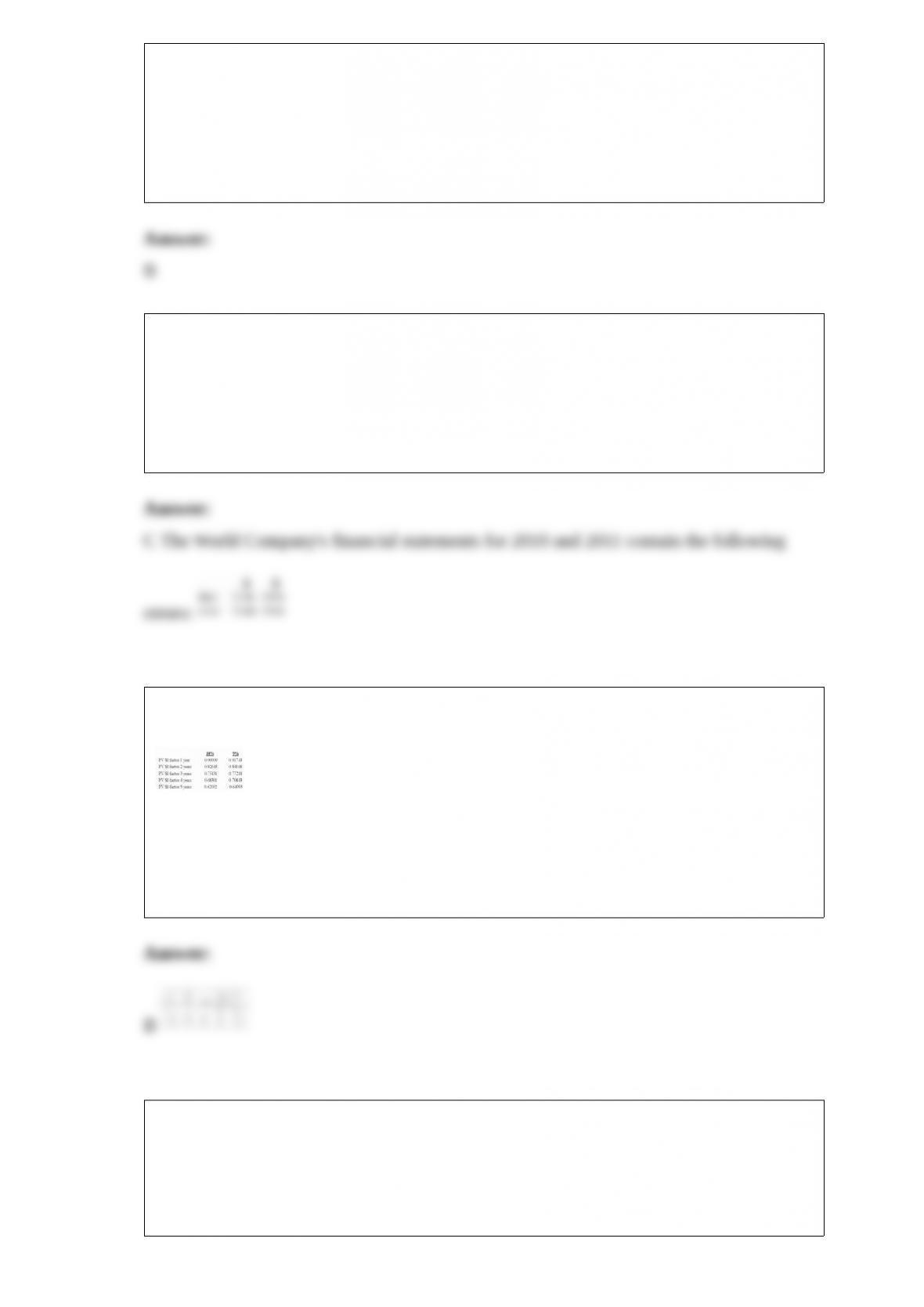

57) On July 1, 2012, The Wings Corporation paid $460,000 plus accrued interest to

retire bonds with a maturity value of $500,000. The bonds had a book value of

$475,131 on January 1, 2012 . The stated interest rate is 8% with interest payments

being made annually on December 31; the bonds were issued at a time when the market

interest rate was 10%.

Requirement:

Determine the gain or loss on the bond retirement.

58) Rick Company uses straight-line depreciation for its property, plant, and equipment

whichstated at costconsisted of the following:

Rick’s depreciation expense for 2012 and 2011 was $115,000 and $110,000

respectively.

Required: What amount was debited to accumulated depreciation during 2012 because

of property, plant, and equipment retirements?

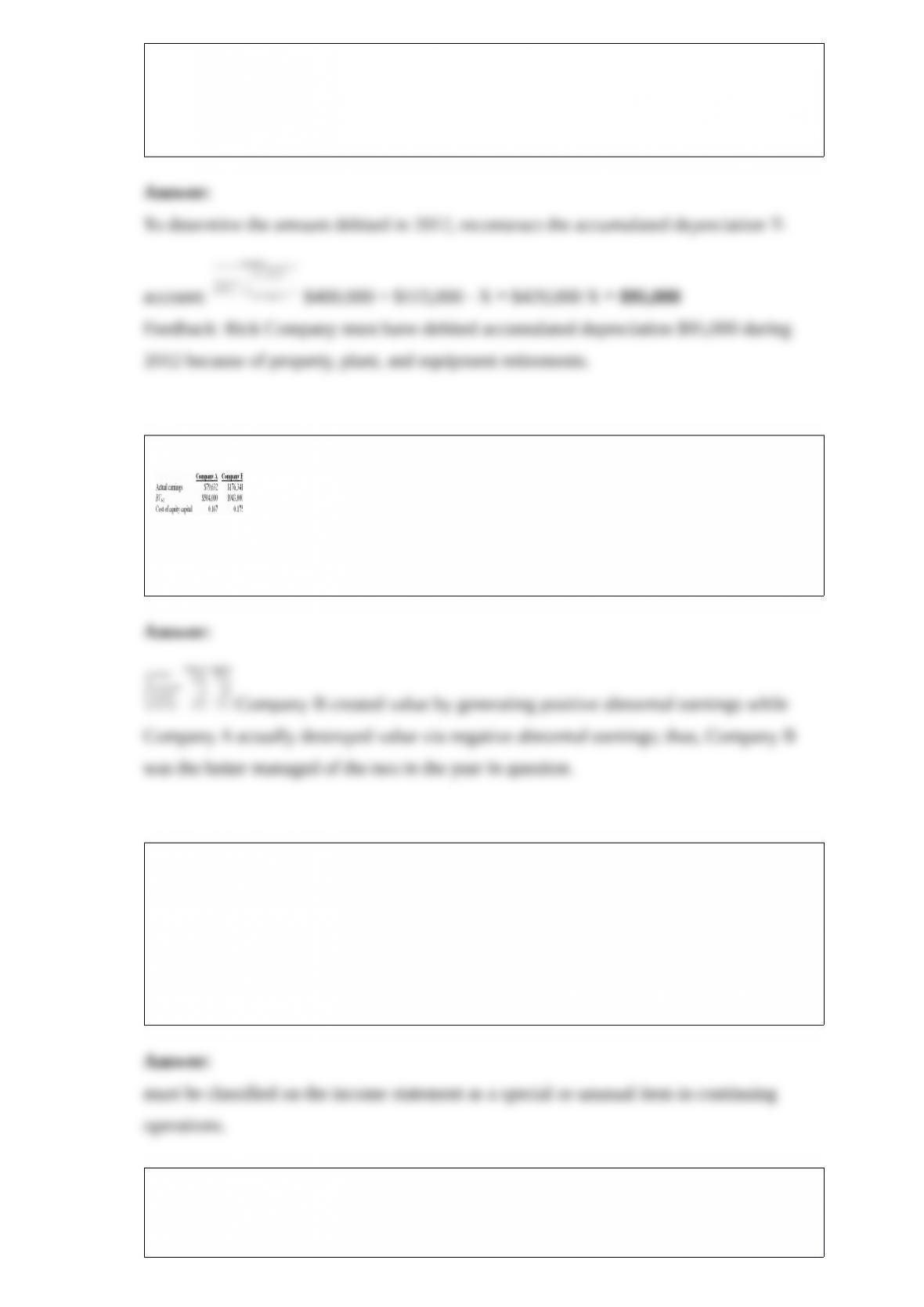

59) Selected data are presented below for two companies.

Required:

Calculate each firm’s abnormal earnings and indicate which firm was better managed

during the year in question.

60) If a material event is either unusual in nature or an infrequent occurrencesuch as a

one-time charge resulting from a major restructuringit may be classified on the income

statement as a special or unusual item in continuing operations or treated as an

extraordinary item if it has been a number of years since the company’s last major

restructuring.

FALSE

Such items

61) On December 15, 2011, The International Company received and accepted an order

to deliver goods to a foreign customer on February 1, 2012 in exchange for 3 million

euros. International must deliver the goods on February 1, 2012 and the foreign

customer is required to pay for the goods at the time of delivery. On December 15,

2011, International agreed to a forward contract to deliver 3 million euros to the

Speculative Bank on February 1, 2012 in exchange for $2,730,000. The forward rate as

of December 31, 2011 was $.915; the spot rate as of February 1, 2012 was $.904.

Requirement:

Prepare the necessary journal entries on December 31, 2011 and February 1, 2012

assuming that the forward contract is being used as a fair value hedge.