Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Buyers generally want to complete due diligence on the seller as quickly as possible.

True or False

Answer:

Arbitrage should drive the prices in different markets to be the same, as investors sell

those assets that are undervalued to buy those that are overvalued. True or False

Answer:

Contingency plans are actions that are taken as an alternative to the firm's current

business strategy. True or False

Answer:

A substantial body of evidence indicates that increasing a firm's degree of

diversification can improve substantially financial returns to shareholders. True or False

Answer:

A leveraged buyout is the purchase of a company financed primarily by debt. This is a

term more frequently applied to a firm going private financed primarily by debt. True or

False

Answer:

In a statutory merger, only assets and liabilities shown on the target firm's balance sheet

automatically transfer to the acquiring firm. True or False

Answer:

Large companies often have a difficult time achieving out-of-court settlements because

they usually have hundreds of creditors. True or False

Answer:

In many family owned firms, family influence is exercised by family members holding

senior management positions, seats on the board of directors, and through holding

super-voting stock (i.e., stock with multiple voting rights). True or False

Answer:

According to the capital asset pricing model, risk consists of both diversifiable and

non-diversifiable components. True or False

Answer:

Fees charged by investment bankers are never negotiable. True or False

Answer:

Through a process called an assignment, a committee representing creditors grants the

power to liquidate the firm's assets to a third party called an assignee or trustee. True or

False

Answer:

The decision to buy political risk insurance depends on the size of the investment and

the perceived level of political and economic risk. True or False

Answer:

Financial information for both public and private firms is equally reliable because their

statements are audited by outside accounting firms to ensure that are developed in a

manner consistent with GAAP.

True or False

Answer:

State antitrust laws are usually quite similar to federal laws. True or False

Answer:

An effective starting point in setting up a structure is to learn from the past and to

recognize that the needs of the business drive structure and not the other way around.

True or False

Answer:

Net synergy is the difference between the present value of the estimated sources of

value and destroyers of value. True of False

Answer:

Despite accounting practices varying widely from country to country, the seller should

not be required to confirm that their financial statements have been prepared in

accordance with generally accepted accounting principles if to do so would endanger

the deal. True or False

Answer:

A holding company structure is the preferred post-closing organization if the acquiring

firm is interested in integrating the target firm immediately following acquisition. True

or False

Answer:

The share exchange ratio indicates the number of acquirer shares to be exchanged for

each share of target stock based on the target firm's current share price. True or False

Answer:

The number of business alliances established each year is usually much smaller than the

number of mergers and acquisitions. True or False

Answer:

Synergy is the notion that the combination of two or more firms will create value

exceeding what either firm could have achieved if they had remained independent. True

or False

Answer:

A bear hug involves mailing a letter containing an acquisition proposal to the target's

board without warning and demanding an immediate response. True or False

Answer:

Using the adjusted present value method to value a LBA assumes the total value of the

firm is the present value of the firm's free cash flows to lenders plus the present value of

future tax savings discounted at the firm's unlevered cost of equity. True or False

Answer:

High growth firms with high reinvestment requirements often make attractive LBO

targets. True or False

Answer:

The risk associated with overpaying is magnified for leveraged buyout transactions.

True or False

Answer:

A firm is said to be bankrupt once it defaults on a bond payment. True or False

Answer:

In adjusting base year income, an appraiser must be aware of the implications of

various accounting methods for value. During periods of inflation, businesses

frequently use the last-in, first out method to value inventories. This approach results a

reduction in the cost of sales and an increase in gross profits and taxable income. True

or False

Answer:

The estimation of present value using the constant growth model involves the

calculation of a terminal value. True or False

Answer:

It is generally more important to respond to current issues as they arise in your

communication plans even if it results in the appearance of a somewhat inconsistent

theme throughout communications made to stakeholders. True or False

Answer:

Private businesses may need to be valued to settle shareholder disputes, court cases,

divorce, or the payment of gift or estate taxes. True or False

Answer:

Unlike limited partnerships, LLC organization agreements do not require that they be

dissolved in case of the death or retirement or resignation of any member. True or False

Answer:

A cost leadership strategy is most appropriate when pursued concurrently by a number

of firms in the same industry with approximately the same market share. True or False

Answer:

The requirements to be listed on most major public exchanges far exceed the auditor

independence requirements of the Sarbanes-Oxley Act. True or False

Answer:

It is easier to obtain the fair market value of private companies than for public

companies because of the absence of volatile stock markets. True or False

Answer:

Overpayment risk involves the dilution of EPS or a reduction in its growth rate

resulting from paying significantly more than the economic value of the acquired firm.

True or False

Answer:

Employees of both the target and acquiring firms are likely to resist change following a

takeover. True or False

Answer:

The calculation of free cash flow to equity includes all of the following except for

a. Operating income

b. Preferred dividends

c. Change in working capital

d. Gross plant and equipment spending

e. Principal repayments

Answer:

Which of the following is not true of a taxable purchase of stock?

a. Taxable transactions usually involve the purchase of the target's voting stock with

acquirer stock.

b. Taxable transactions usually involve the purchase of the target's voting stock, because

the purchase of assets automatically will trigger a taxable gain for the target if the fair

market value of the acquired assets exceeds the target firm's tax basis in the assets.

c. All stockholders are affected equally in a taxable purchase of assets.

d. The target firm does not pay any taxes on the transaction.

e. The effect of the tax liability will vary depending on the individual shareholder's tax

basis.

Answer:

Which of the following is true about so-called shark repellants?

a. They are put in place to strengthen the board

b. They include poison pills

c. Often consist of the right to issue greenmail

d. Involve White Knights

e. Involve corporate restructuring

Answer:

Which of the following do not represent typical closing documents in an asset

purchase?

a. Letter of intent

b. Listing of any liabilities to be assumed by the buyer

c. Loan and security agreements if the transaction is to be financed with debt

d. Complete descriptions of all patents, facilities, and investments

e. Listing of assets to be acquired

Answer:

If one party chooses to exit an alliance, the remaining party or parties often have the

contractual right to

a. First offer their ownership interests to the other partners

b. Sell their ownership interests to the highest bidder

c. Put their interests to a third party that has no relationship to the alliance

d. Require that the other parties to the alliance buy them out

e. Dissolve the partnership

Answer:

Alcoa Easily Overwhelms Reynolds' Takeover Defenses

Alcoa reacted quickly to a three-way intercontinental combination of aluminum

companies aimed at challenging its dominance of the Western World aluminum market

by disclosing an unsolicited takeover bid for Reynolds Metals in early August 1999.

The offer consisted of $4.3 billion, or $66.44 a share, plus the assumption of $1.5

billion in Reynolds' outstanding debt. Reynolds, a perennial marginally profitable

competitor in the aluminum industry, appeared to be particularly vulnerable, since other

logical suitors or potential white knights such as Canada's Alcan Aluminum, France's

Pechiney SA, and Switzerland's Alusuisse Lonza Group AG were already involved in a

three-way merger.

Alcoa's letter from its chief executive indicated that it wanted to pursue a friendly deal

but suggested that it may pursue a full-blown hostile bid if the two sides could not

begin discussions within a week. Reynolds appeared to be highly vulnerable because of

its poor financial performance amid falling aluminum prices worldwide and because of

its weak takeover defenses. It appeared that a hostile bidder could initiate a mail-in

solicitation for shareholder consent at any time. Moreover, major Reynolds'

shareholders began to pressure the board. Its largest single shareholder, Highfields

Capital Management, a holder of more than four million shares, demanded that the

Board create a special committee of independent directors with its own counsel and

instruct Merrill Lynch to open an auction for Reynolds.

Despite pressure, the Reynolds' board rejected Alcoa's bid as inadequate. Alcoa's

response was to say that it would initiate an all cash tender offer for all of Reynolds'

stock and simultaneously solicit shareholder support through a proxy contest for

replacing the Reynolds' board and dismantling Reynolds' takeover defenses.

Notwithstanding the public posturing by both sides, Reynolds capitulated on August 19,

slightly more than two weeks from receipt of the initial solicitation, and agreed to be

acquired by Alcoa. The agreement contained a thirty-day window during which

Reynolds could entertain other bids. However, if Reynolds should choose to go with

another offer, it would have to pay Alcoa a $100 million break-up fee.

Under the agreement, which was approved by both boards, each share of Reynolds was

exchanged for 1.06 shares of Alcoa stock. When announced, the transaction was worth

$4.46 billion and valued each Reynolds share at $70.88, based on an Alcoa closing

price of $66.875 on August 19, 1999. The $70.88 price per share of Reynolds suggested

a puny 3.9 percent premium to Reynolds' closing price of $68.25 as of the close of

August 19. The combined annual revenues of the two companies totaled $20.5 billion

and accounted for about 21.5 percent of the Western World market for aluminum. To

receive antitrust approval, the combined companies were required divest selected

operations.

Discussion Questions:

1) What was the dollar value of the purchase price Alcoa offered to pay for Reynolds?

2) Describe the various takeover tactics Alcoa employed in its successful takeover of

Reynolds. Why were these

tactics employed?

3) Why do you believe Reynolds' management rejected Alcoa's initial bid as

inadequate?

4) In your judgment, why was Alcoa able to complete the transaction by offering such a

small premium

over Reynolds' share price at the time the takeover was proposed?

Answer:

The negotiation process consists of all of the following concurrent activities except for

a. Refining valuation

b. Deal structuring

c. Integration planning

d. Due Diligence

e. Developing the financing plan

Answer:

A firm's leveraged beta reflects all of the following except for

a. unleveraged beta

b. the firm's debt

c. marginal tax rate

d. the firm's cost of equity

e. the firm's equity

Answer:

All of the following are common takeover defenses except for

a. Poison pills

b. Litigation

c. Tender offers

d. Staggered boards

e. Golden parachutes

Answer:

Which of the following represent important decisions that must be made early in the

integration process?

a. Identifying the appropriate organizational structure

b. Defining key reporting relationships

c. Selecting the right managers

d. Identifying and communicating key roles and responsibilities

e. All of the above

Answer:

Which of the following are common objectives of an external analysis?

a. Determining where to compete

b. Determining how to compete

c. Identifying core competencies

d. A & B only

e. A, B, & C

Answer:

Which of the following is not true of a split-off?

a. A split-off is a variation of a spin-off

b. Parent company shareholders receive shares in a subsidiary in return for surrendering

their parent company shares

c. Split-offs are best suited for disposing of a less than 100 percent investment stake in a

subsidiary,

d. A split-off reduces the parent firm's earnings per share.

e. The split-off reduces the pressure on the spun-off firm's share price

Answer:

Cerberus Capital Management Acquires Chrysler Corporation

According to the terms of the transaction, Cerberus would own 80.1 percent of

Chrysler's auto manufacturing and financial services businesses in exchange for $7.4

billion in cash. Daimler would continue to own 19.9 percent of the new business,

Chrysler Holdings LLC. Of the $7.4 billion, Daimler would receive $1.35 billion while

the remaining $6.05 billion would be invested in Chrysler (i.e., $5.0 billion is to be

invested in the auto manufacturing operation and $1.05 billion in the finance unit).

Daimler also agreed to pay to Cerberus $1.6 billion to cover Chrysler's long-term debt

and cumulative operating losses during the four months between the signing of the

merger agreement and the actual closing. In acquiring Chrysler, Cerberus assumed

responsibility for an estimated $18 billion in unfunded retiree pension and medical

benefits. Daimler also agreed to loan Chrysler Holdings LLC $405 million.

The transaction is atypical of those involving private equity investors, which usually

take public firms private, expecting to later sell them for a profit. The private equity

firm pays for the acquisition by borrowing against the firm's assets or cash flow.

However, the estimated size of Chrysler's retiree health-care liabilities and the

uncertainty of future cash flows make borrowing impractical. Therefore, Cerberus

agreed to invest its own funds in the business to keep it running while it restructured the

business.

By going private, Cerberus would be able to focus on the long-term without the

disruption of meeting quarterly earnings reports. Cerberus was counting on paring

retiree health-care liabilities through aggressive negotiations with the United Auto

Workers (UAW). Cerberus sought a deal similar to what the UAW accepted from

Goodyear Tire and Rubber Company in late 2006. Under this agreement, the

management of $1.2 billion in health-care liabilities was transferred to a fund managed

by the UAW, with Goodyear contributing $1 billion in cash and Goodyear stock. By

transferring responsibility for these liabilities to the UAW, Chrysler believed that it

would be able to cut in half the $30 dollar per hour labor cost advantage enjoyed by

Toyota. Cerberus also expected to benefit from melding Chrysler's financial unit with

Cerberus's 51 percent ownership stake in GMAC, GM's former auto financing business.

By consolidating the two businesses, Cerberus hoped to slash cost by eliminating

duplicate jobs, combining overlapping operations such as data centers and field offices,

and increasing the number of loans generated by combining back-office operations.

However, the 2008 credit market meltdown, severe recession, and subsequent free fall

in auto sales threatened the financial viability of Chrysler, despite an infusion of U.S.

government capital, and its leasing operations as well as GMAC. GMAC applied for

commercial banking status to be able to borrow directly from the U.S. Federal Reserve.

In late 2008, the U.S. Treasury purchased $6 billion in GMAC preferred stock to

provide additional capital to the financially ailing firm. To avoid being classified as a

bank holding company under direct government supervision, Cerberus reduced its

ownership in 2009 to 14.9 percent of voting stock and 33 percent of total equity by

distributing equity stakes to its coinvestors in GMAC. By surrendering its controlling

interest in GMAC, it is less likely that Cerberus would be able to realize anticipated

cost savings by combining the GMAC and Chrysler Financial operations. In early 2009,

Chrysler entered into negotiations with Italian auto maker Fiat to gain access to the

firm's technology in exchange for a 20 percent stake in Chrysler.

Discussion Questions and Answers:

1) What were the motivations for this deal from Cerberus' perspective? From Daimler's

perspective?

2) What are the risks to this deal's eventual success? Be specific.

3) Cite examples of economies of scale and scope?

4) Cerberus and Daimler will own 80.1% and 19.9% of Chrysler Holdings LLC,

respectively. Why do you think the two parties agreed to this distribution of ownership?

5) Which of the leading explanations of why deals sometimes fail to meet expectations

best explains why the combination of Daimler and Chrysler failed? Explain your

answer.

6) The new company, Chrysler Holdings, is a limited liability company. Why do you

think CCM chose this legal structure over a more conventional corporate structure?

Answer:

Cerberus Capital Management Acquires Chrysler Corporation

According to the terms of the transaction, Cerberus would own 80.1 percent of

Chrysler's auto manufacturing and financial services businesses in exchange for $7.4

billion in cash. Daimler would continue to own 19.9 percent of the new business,

Chrysler Holdings LLC. Of the $7.4 billion, Daimler would receive $1.35 billion while

the remaining $6.05 billion would be invested in Chrysler (i.e., $5.0 billion is to be

invested in the auto manufacturing operation and $1.05 billion in the finance unit).

Daimler also agreed to pay to Cerberus $1.6 billion to cover Chrysler's long-term debt

and cumulative operating losses during the four months between the signing of the

merger agreement and the actual closing. In acquiring Chrysler, Cerberus assumed

responsibility for an estimated $18 billion in unfunded retiree pension and medical

benefits. Daimler also agreed to loan Chrysler Holdings LLC $405 million.

The transaction is atypical of those involving private equity investors, which usually

take public firms private, expecting to later sell them for a profit. The private equity

firm pays for the acquisition by borrowing against the firm's assets or cash flow.

However, the estimated size of Chrysler's retiree health-care liabilities and the

uncertainty of future cash flows make borrowing impractical. Therefore, Cerberus

agreed to invest its own funds in the business to keep it running while it restructured the

business.

By going private, Cerberus would be able to focus on the long-term without the

disruption of meeting quarterly earnings reports. Cerberus was counting on paring

retiree health-care liabilities through aggressive negotiations with the United Auto

Workers (UAW). Cerberus sought a deal similar to what the UAW accepted from

Goodyear Tire and Rubber Company in late 2006. Under this agreement, the

management of $1.2 billion in health-care liabilities was transferred to a fund managed

by the UAW, with Goodyear contributing $1 billion in cash and Goodyear stock. By

transferring responsibility for these liabilities to the UAW, Chrysler believed that it

would be able to cut in half the $30 dollar per hour labor cost advantage enjoyed by

Toyota. Cerberus also expected to benefit from melding Chrysler's financial unit with

Cerberus's 51 percent ownership stake in GMAC, GM's former auto financing business.

By consolidating the two businesses, Cerberus hoped to slash cost by eliminating

duplicate jobs, combining overlapping operations such as data centers and field offices,

and increasing the number of loans generated by combining back-office operations.

However, the 2008 credit market meltdown, severe recession, and subsequent free fall

in auto sales threatened the financial viability of Chrysler, despite an infusion of U.S.

government capital, and it's leasing operations as well as GMAC. GMAC applied for

commercial banking status to be able to borrow directly from the U.S. Federal Reserve.

In late 2008, the U.S. Treasury purchased $6 billion in GMAC preferred stock to

provide additional capital to the financially ailing firm. To avoid being classified as a

bank holding company under direct government supervision, Cerberus reduced its

ownership in 2009 to 14.9 percent of voting stock and 33 percent of total equity by

distributing equity stakes to its coinvestors in GMAC. By surrendering its controlling

interest in GMAC, it is less likely that Cerberus would be able to realize anticipated

cost savings by combining the GMAC and Chrysler Financial operations. In early 2009,

Chrysler entered into negotiations with Italian auto maker Fiat to gain access to the

firm's technology in exchange for a 20 percent stake in Chrysler.

Discussion Questions and Answers:

1) What were the motivations for this deal from Cerberus' perspective? From Daimler's

perspective?

2) What are the risks to this deal's eventual success? Be specific.

3) Cite examples of economies of scale and scope?

4) Cerberus and Daimler will own 80.1% and 19.9% of Chrysler Holdings LLC,

respectively. Why do you think the two parties agreed to this distribution of ownership?

5) Which of the leading explanations of why deals sometimes fail to meet expectations

best explains why the combination of Daimler and Chrysler failed? Explain your

answer.

6) The new company, Chrysler Holdings, is a limited liability company. Why do you

think CCM chose this legal structure over a more conventional corporate structure?

Answer:

Purchase accounting requires that

a. The excess amount paid for the target firm be recorded as an intangible asset on the

books of the acquirer and immediately written off

b. Target firm assets must be recorded on the acquirer's balance sheet at their fair

market value

c. The excess of the purchase price of the purchase price of the target firm must be

recorded as asset and expensed over a period of 10 years

d. Goodwill once established is never written off

e. Target firm liabilities are recorded on the balance sheet of the acquirer at their book

value

Answer:

Which of the following is not true about LBO models?

a. They rarely use IRR calculations

b. Borrowing capacity is relatively unimportant

c. The financial sponsor's equity contribution is determined before the target firm's

borrowing capacity

d. A, B, and C

e. A and B only

Answer:

In determining the purchase price for an acquisition target, which one of the following

valuation methods does not require the addition of a purchase price premium?

a. Discounted cash flow method

b. Comparable companies' method

c. Comparable industries' method

d. Recent transactions' method

e. A & B only

Answer:

Overcoming Political Risk in Cross-Border Transactions:

China's CNOOC Invests in Chesapeake Energy

Cross-border transactions often are subject to considerable political risk. In emerging

countries, this may reflect the potential for expropriation of property or disruption of

commerce due to a breakdown in civil order. However, as Chinese efforts to secure

energy supplies in recent years have shown, foreign firms have to be highly sensitive to

political and cultural issues in any host country, developed or otherwise.

In addition to a desire to satisfy future energy needs, the Chinese government has been

under pressure to tap its domestic shale gas deposits due to the clean burning nature of

such fuels to reduce its dependence on coal, the nation's primary source of power.

However, China does not currently have the technology for recovering gas and oil from

shale. In an effort to gain access to the needed technology and to U.S. shale gas and oil

reserves, China National Offshore Oil Corporation Ltd. in October 2010 agreed to

invest up to $2.16 billion in selected reserves of U.S. oil and gas producer Chesapeake

Energy Corp. Chesapeake is a leader in shale extraction technologies and an owner of

substantial oil and gas shale reserves, principally in the southwestern United States.

The deal grants CNOOC the option of buying up to a third of any other fields

Chesapeake acquires in the general proximity of the fields the firm currently owns. The

terms of the deal call for CNOOC to pay Chesapeake $1.08 billion for a one-third stake

in a South Texas oil and gas field. CNOOC could spend an additional $1.08 billion to

cover 75 percent of the costs of developing the 600,000 acres included in this field.

Chesapeake will be the operator of the JV project in Texas, handling all leasing and

drilling operations, as well as selling the oil and gas production. The project is expected

to produce as much as 500,000 barrels of oil daily within the next decade, about 2.5

percent of the current U.S. daily oil consumption.

Having been forced in 2005 to withdraw what appeared to be a winning bid for U.S. oil

company Unocal, CNOOC stayed out of the U.S. energy market until 2010. The firm's

new strategy includes becoming a significant partner in joint ventures to develop largely

untapped reserves. The investment had significant appeal to U.S. interests because it

represented an opportunity to develop nontraditional sources of energy while creating

thousands of domestic jobs and millions of dollars in tax revenue. This investment was

particularly well timed, as it coincided with a nearly double-digit U.S. jobless rate;

yawning federal, state, and local budget deficits; and an ongoing national desire for

energy independence. The deal makes sense for debt-laden Chesapeake, since it lacked

the financial resources to develop its shale reserves.

In contrast to the Chesapeake transaction, CNNOC tried to take control of Unocal,

triggering what may be the most politicized takeover battle in U.S. history. Chevron, a

large U.S. oil and gas firm, had made an all-stock $16 billion offer (subsequently raised

to $16.5 billion) for Unocal, which was later trumped by an all-cash $18.5 billion bid

by CNOOC. About three-fourths of CNOOC's all-cash offer was financed through

below-market-rate loans provided by its primary shareholder: the Chinese government.

CNOOC's all-cash offer sparked instant opposition from members of Congress, who

demanded a lengthy review and introduced legislation to place even more hurdles in

CNOOC's way. Hoping to allay fears, CNOOC offered to sell Unocal's U.S. assets and

promised to retain all of Unocal's workers, something Chevron was not prone to do.

U.S. lawmakers expressed concern that Unocal's oil drilling technology might have

military applications and CNOOC's ownership structure (i.e., 70 percent owned by the

Chinese government) would enable the firm to secure low-cost financing that was

unavailable to Chevron. The final blow to CNOOC's bid was an amendment to an

energy bill passed in July requiring the Departments of Energy, Defense, and Homeland

Security to spend four months studying the proposed takeover before granting federal

approval.

Perhaps somewhat naively, the Chinese government viewed the low-cost loans as a way

to "recycle" a portion of the huge accumulation of dollars it was experiencing. While

the Chinese remained largely silent through the political maelstrom, CNOOC's

management appeared to be greatly surprised and embarrassed by the public criticism

in the United States about the proposed takeover of a major U.S. company. Up to that

point, the only other major U.S. firm acquired by a Chinese firm was the 2004

acquisition of IBM's personal computer business by Lenovo, the largest PC

manufacturer in China.

Many foreign firms desirous of learning how to tap shale deposits from U.S. firms like

Chesapeake and to gain access to such reserves have invested in U.S. projects,

providing a much-needed cash infusion. In mid-2010, Indian conglomerate Reliance

Industries acquired a 45 percent stake in Pioneer Natural Resources Company's Texas

natural gas assets and has negotiated deals totaling $2 billion for minority stakes in

projects in the eastern United States. Norwegian oil producer Statoil announced in late

2010 that it would team up with Norwegian oil producer Talisman Energy to buy $1.3

billion worth of assets in the Eagle Ford fields, the same shale deposit being developed

by Chesapeake and CNOOC.

Discussion Questions

1) Do you believe that countries should permit foreign ownership of vital scarce natural

resources? Explain your answer.

2) What real options (see Chapter 8) might be implicit in CNNOC's investment in

Chesapeake? Be specific.

3) To what extent does the Chesapeake transaction represent the benefits of free global

trade and capital movements? In what way might it reflect the limitations of free trade?

4) Compare and contrast the Chesapeake and Unocal transactions. Be specific.

5) Describe some of the ways in which CNOOC could protect its rights as a minority

investor in the joint venture project with Chesapeake? Be specific.

Answer:

Which one of the following statements is true?

a. Target firm shareholders may accept cash or acquirer stock in exchange for their

shares for the transaction to be considered tax free

b. To be tax free, the target firm shareholders must receive acquirer firm shares for all

of the target firm's shares outstanding

c. At least one-half of the assets of the target firm are recorded on the balance sheet of

the acquirer at their book rather than market value in a tax free transaction

d. If the assets of a firm are written up to fair market value as part of the transaction, the

increase in value is considered a taxable gain

e. Target firm shareholders are required by law to pay taxes on any writeup of the firm's

assets to fair market value

Answer:

Which factors would be considered in determining the feasibility of financing a

proposed takeover?

a. Potential dilution in EPS of the combined firms.

b. Impact on overall borrowing costs of the combined firms.

c. Possible violation of loan covenants on existing debt of the acquiring company

d. Return on total capital of the combined firms

e. All of the above.

Answer:

All of the following represent generic business strategies except for

a. Cost leadership

b. Differentiation

c. Focus

d. Market segmentation

e. A and D

Answer:

Which one of the following is not one of the steps in the M&A model building process?

a. Valuing the acquirer and the target firms as standalone businesses

b. Valuing the target and acquiring firms including synergy

c. Determining the initial offer price for the target firm

d. Establishing search criteria for the potential target firm

e. Determining the combined firm's ability to finance the transaction.

Answer:

Which of the following phases of the acquisition process contains a "feedback" loop?

a. Negotiation phase

b. Search phase

c. Integration phase

d. Post-closing evaluation phase

e. Closing

Answer:

Around the announcement date of a merger or acquisition, abnormal returns to target

firm shareholders

normally average

a. 10%

b. 30%

c. 3%

d. 100%

e. 50%

Answer:

Over the years, the U.S. Congress has transferred some of the enforcement of securities

laws to organizations other than the SEC such as

a. Public stock exchanges

b. Financial Accounting Standards Board

c. Public Accounting Oversight Board

d. State regulatory agencies

e. All of the above

Answer:

The negotiation process consists of all of the following except for

a. Refining valuation

b. Due diligence

c. Closing

d. Developing a financing plan

e. Deal structuring

Answer:

LBOs often exhibit very high financial returns during the years following their creation.

Which of the following best describes why this might occur?

a. LBOs invariably improve the firm's operating efficiency

b. LBOs tend to increase investment in plant and equipment

c. The only LBOs that are taken public are those that have been the most successful

d. LBOs experience improved decision making during the post-buyout period

e. None of the above

Answer:

All of the following are true of poison pills except for

a. They are a new class of security

b. Generally prevent takeover attempts from being successful

c. Enable target shareholders to buy additional shares in the new company if an

unwanted shareholder's ownership exceeds a specific percentage of the target's stock

d. Delays the completion of a takeover attempt

e. May be removed by the target's board if an attractive bid is received from a so-called

"white knight."

Answer:

Examples of corporate level strategies include which of the following:

a. Growth

b. Diversification

c. Operational

d. Financial

e. All of the above

Answer:

Assessing Procter & Gamble's Acquisition of Gillette

The potential seemed almost limitless, as Procter & Gamble Company (P&G)

announced that it had completed its purchase of Gillette Company (Gillette) in late

2005. P&G's chairman and CEO, A.G. Lafley, predicted that the acquisition of Gillette

would add one percentage point to the firm's annual revenue growth rate, while

Gillette's chairman and CEO, Jim Kilts, opined that the successful integration of the two

best companies in consumer products would be studied in business schools for years to

come.

Five years after closing, things have not turned out as expected. While cost savings

targets were achieved, operating margins faltered due to lagging sales. Gillette's

businesses, such as its pricey razors, have been buffeted by the 20082009 recession and

have been a drag on P&G's top line rather than a boost. Moreover, most of Gillette's top

managers have left. P&G's stock price at the end of 2010 stood about 12 percent above

its level on the acquisition announcement date, less than one-fourth the appreciation of

the share prices of such competitors as Unilever and Colgate-Palmolive Company

during the same period.

On January 28, 2005, P&G enthusiastically announced that it had reached an agreement

to buy Gillette in a share-for-share exchange valued at $55.6 billion. This represented

an 18 percent premium over Gillette's preannouncement share price. P&G also

announced a stock buyback of $18 billion to $22 billion, funded largely by issuing new

debt. The combined companies would retain the P&G name and have annual 2005

revenue of more than $60 billion. Half of the new firm's product portfolio would consist

of personal care, healthcare, and beauty products, with the remainder consisting of

razors and blades, and batteries. The deal was expected to dilute P&G's 2006 earnings

by about 15 cents per share. To gain regulatory approval, the two firms would have to

divest overlapping operations, such as deodorants and oral care.

P&G had long been viewed as a premier marketing and product innovator.

Consequently, P&G assumed that its R&D and marketing skills in developing and

promoting women's personal care products could be used to enhance and promote

Gillette's women's razors. Gillette was best known for its ability to sell an inexpensive

product (e.g., razors) and hook customers to a lifetime of refills (e.g., razor blades).

Although Gillette was the number 1 and number 2 supplier in the lucrative toothbrush

and men's deodorant markets, respectively, it has been much less successful in

improving the profitability of its Duracell battery brand. Despite its number 1 market

share position, it had been beset by intense price competition from Energizer and

Rayovac Corp., which generally sell for less than Duracell batteries.

Suppliers such as P&G and Gillette had been under considerable pressure from the

continuing consolidation in the retail industry due to the ongoing growth of Wal-Mart

and industry mergers at that time, such as Sears and Kmart. About 17 percent of P&G's

$51 billion in 2005 revenues and 13 percent of Gillette's $9 billion annual revenue came

from sales to Wal-Mart. Moreover, the sales of both Gillette and P&G to Wal-Mart had

grown much faster than sales to other retailers. The new company, P&G believed,

would have more negotiating leverage with retailers for shelf space and in determining

selling prices, as well as with its own suppliers, such as advertisers and media

companies. The broad geographic presence of P&G was expected to facilitate the

marketing of such products as razors and batteries in huge developing markets, such as

China and India. Cumulative cost cutting was expected to reach $16 billion, including

layoffs of about 4 percent of the new company's workforce of 140,000. Such cost

reductions were to be realized by integrating Gillette's deodorant products into P&G's

structure as quickly as possible. Other Gillette product lines, such as the razor and

battery businesses, were to remain intact.

P&G's corporate culture was often described as conservative, with a

"promote-from-within" philosophy. While Gillette's CEO was to become vice chairman

of the new company, the role of other senior Gillette managers was less clear in view of

the perception that P&G is laden with highly talented top management. To obtain

regulatory approval, Gillette agreed to divest its Rembrandt toothpaste and its Right

Guard deodorant businesses, while P&G agreed to divest its Crest toothbrush business.

The Gillette acquisition illustrates the difficulty in evaluating the success or failure of

mergers and acquisitions for acquiring company shareholders. Assessing the true impact

of the Gillette acquisition remains elusive, even after five years. Though the acquisition

represented a substantial expansion of P&G's product offering and geographic presence,

the ability to isolate the specific impact of a single event (i.e., an acquisition) becomes

clouded by the introduction of other major and often uncontrollable events (e.g., the

20082009 recession) and their lingering effects. While revenue and margin

improvement have been below expectations, Gillette has bolstered P&G's competitive

position in the fast-growing Brazilian and Indian markets, thereby boosting the firm's

longer-term growth potential, and has strengthened its operations in Europe and the

United States. Thus, in this ever-changing world, it will become increasingly difficult

with each passing year to identify the portion of revenue growth and margin

improvement attributable to the Gillette acquisition and that due to other factors.

Discussion Questions:

1) Is this deal a merger or a consolidation from a legal standpoint? Explain your answer.

2) Is this a horizontal or vertical merger? What is the significance of this distinction?

Explain your answer.

3) What are the motives for the deal? Discuss the logic underlying each motive you

identify.

4) Immediately following the announcement, P&G's share price dropped by 2 percent

and Gillette's share price rose by 13 percent. Explain why this may have happened?

5) P&G announced that it would be buying back $18 to $22 billion of its stock over the

eighteen months

following closing. Much of the cash required to repurchase these shares requires

significant new borrowing by

the new companies. Explain what P&G's objective may have been trying to achieve in

deciding to repurchase

stock? Explain how the incremental borrowing help or hurt P&G achieve their

objectives?

6) Explain how actions required by antitrust regulators may hurt P&G's ability to realize

anticipated synergy. Be

specific.

7) Explain some of the obstacles that P&G and Gillette are likely to face in integrating

the two businesses. Be specific. How would you overcome these obstacles?

Answer:

U.S. antitrust regulators are most concerned about what types of transaction?

a. Vertical mergers

b. Horizontal mergers

c. Alliances

d. Joint ventures

e. Minority investments

Answer:

Realizing synergy often requires spending money. Which of the following are examples

of such expenditures?

a. Employee recruitment and training expenses

b. Severance expenses

c. Investment in equipment to improve employee productivity

d. Redesigning workflow

e. All of the above

Answer:

Valuation Methods Employed in Investment Bank Fairness Opinion Letters

Background

A fairness opinion letter is a written third-party certification of the appropriateness of

the price of a proposed transaction such as a merger, acquisition, leveraged buyout, or

tender offer. A typical fairness opinion provides a range of what is believed to be fair

values, with a presumption that the actual deal price should fall within this range. The

data used in this case study is found in SunGard's Schedule 14A Proxy Statement

submitted to the SEC in May 2005.

On March 27, 2005, the investment banking behemoth Lazard Freres (Lazard)

submitted a letter to the board of directors of SunGard Corporation pertaining to the

fairness of a $10.9 billion bid to take the firm private made by an investor group.

Lazard employed a variety of valuation methods to evaluate the offer price. These

included the comparable company approach, the recent transactions method, discounted

cash flow analysis, and an analysis of recent transaction premiums. The analyses were

applied to each of the firm's major businesses: software services and recovery

availability services. The software services' business provides software systems and

support for application and transaction processing to financial services firms,

universities, and government agencies. The recovery availability services business

provides businesses and government agencies with backup and recovery support in the

event their data processing systems are disrupted.

Comparable Company Analysis

Using publicly available information, Lazard reviewed the market values and trading

multiples of the selected publicly held companies for each business segment. Multiples

were based on stock prices as of March 24, 2005 and specific company financial data

on publicly available research analysts' estimates for 2005. In the case of SunGard's

software business, Lazard reviewed the market values and trading multiples of four

publicly traded financial services companies and three publicly traded securities trading

companies. In the case of SunGard's recovery availability services business, Lazard

reviewed the market values and trading multiples of the six selected publicly traded

business continuity services (i.e., recoverability services firms) companies. These firms

were believed to be representative of these segments of SunGard's operations.

Lazard calculated enterprise values for these comparable companies as equity value

plus debt, preferred stock, and all out-of-the-money convertibles (i.e., convertible debt

whose conversion price exceeded the merger offer price), less cash and cash equivalents

(i.e., short-term liquid securities). Estimated enterprise value multiples of earnings

before interest, taxes, depreciation and amortization (i.e., EBITDA) were created for

2005 by dividing enterprise values by publicly available estimates of EBITDA for each

comparable company. Similarly, price-to-earnings ratios were created by dividing

equity values per share by earnings per share for each comparable company for

calendar 2005. See Tables 8-1 and 8.2.

Based on this analysis, Lazard determined an enterprise value to estimated 2005

EBITDA multiple range for SunGard's recovery availability services business of 5.5x to

7.0x. Lazard also determined a 2005 estimated P/E range for this segment of 14.0x to

16.0x. Multiplying SunGard's projected EBITDA and earnings per share for 2005 by

these ranges, Lazard calculated an enterprise value range for SunGard's recovery

availability services business of approximately $3.1 billion to $3.7 billion. Financial

projections for SunGard were provided by SunGard's management.

Based on the results in Table 8-2, Lazard determined an enterprise value to estimated

2005 EBITDA multiple range for SunGard's software business of 7.5x to 9.5x. Lazard

also determined a 2005 estimated P/E range for SunGard's software business of 17.0 to

19.0x. Multiplying SunGard's projected EBITDA and earnings per share for 2005 by

these ranges, Lazard calculated an enterprise value range for SunGard's software

business of approximately $4.3 billion to $5.2 billion.

Lazard then summed the enterprise value ranges for SunGard's software business and

recovery availability services business to calculate a consolidated enterprise value range

for SunGard of approximately $7.4 billion to $8.9 billion. Using this consolidated

enterprise value range and assuming net debt (i.e., total debt less cash and cash

equivalents on the balance sheet) of $273 million, Lazard calculated an implied price

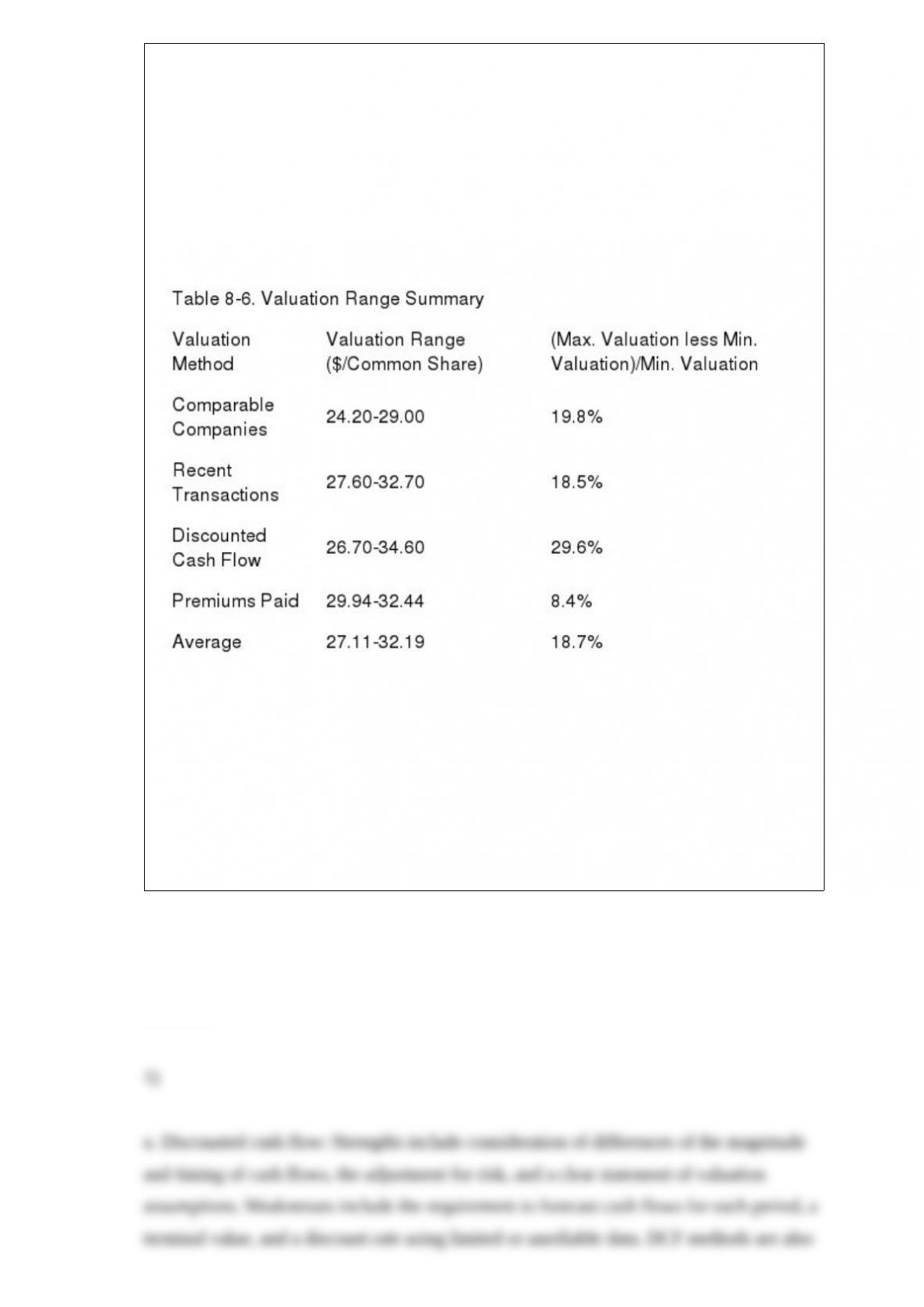

per share range for SunGard common stock of $24.20 to $29.00 by dividing the

enterprise value less net debt by the SunGard shares outstanding.

Recent Transactions Method

For the recovery availability services business, Lazard reviewed ten merger and

acquisition transactions since October 2001 for companies in the information

technology outsourcing business. To the extent publicly available, Lazard reviewed the

transaction enterprise values of the recent transactions as a multiple of the last twelve

months EBITDA for the period ending on the recent transaction announcement date.

See Table 8-3.

Based on Table 8-3, Lazard determined an EBITDA multiple range of 6.5x to 5x and

multiplied this range by the last twelve months EBITDA for SunGard's recovery

availability business to calculate an implied enterprise value range of approximately

$3.4 billion to $4.0 billion.

Lazard reviewed 21 merger and acquisition transactions since February 2003 with a

value greater than approximately $100 million for companies in the software business.

To the extent publicly available, Lazard examined the transaction enterprise values of

the recent transactions as a multiple of EBITDA for the last twelve months prior to the

public announcement of the relevant recent transaction. See Table 8-4.

Based on the information contained in Table 8-5, Lazard determined an EBITDA

multiple range of 9.0x to 11.0x and multiplied this range by the last twelve month

EBITDA for SunGard's software business to calculate an implied enterprise value range

for this business segment of approximately $5.0 billion to $6.1 billion.

Lazard then summed the enterprise value ranges for SunGard's software business and

recovery availability services business to calculate a consolidated enterprise value range

for SunGard of approximately $8.4 billion to $10.1 billion. Using this consolidated

enterprise value range and assuming net debt of $273 million, Lazard calculated the

value per share of SunGard common stock of $27.60 to $32.70 by dividing the

estimated consolidated enterprise value less net debt by common shares outstanding.

Discounted Cash Flow Analysis

Using projections provided by SunGard's management, Lazard performed an analysis of

the present value, as of March 31, 2005, of the free cash flows that SunGard could

generate annually from calendar year 2005 through calendar year 2009. Lazard

analyzed separately the cash flows for SunGard's software business and recovery

availability services business.

For SunGard's software business, in calculating the terminal value, Lazard assumed

perpetual growth rates (i.e., constant growth model) of 3.5% to 4.5% for the projected

free cash flows for the periods subsequent to 2009. The projected annual cash flows

through 2009 and beyond were then discounted to present value using discount rates

ranging from 10.0% to 12.0%. Based on this analysis, Lazard calculated an implied

enterprise value range for the software business of approximately $5.6 billion to $7.4

billion.

For SunGard's recovery availability services business, in calculating the terminal value

Lazard assumed perpetual growth rates of 2.0% to 3.0% for the projected free cash

flows for periods subsequent to 2009. The projected cash flows were then discounted to

present value using discount rates ranging from 10.0% to 12.0%. Lazard then calculated

an implied enterprise value range for SunGard's recovery availability business of

approximately $2.6 billion to $3.3 billion.

Lazard then aggregated the enterprise value ranges for SunGard's two business

segments to calculate a consolidated enterprise value range for SunGard of

approximately $8.2 billion to $10.7 billion. Using this consolidated enterprise value

range and assuming net debt of $273 million, Lazard calculated an implied price per

share range for SunGard common stock of $26.70 to $34.60.

Premiums Paid Analysis

Lazard performed a premiums paid analysis based upon the premiums paid in 73 recent

transactions (not involving "mergers of equals" transactions) that were announced from

January 2004 through March 2005 and involved transaction values in excess of $1

billion. In conducting its analysis, Lazard analyzed the premiums paid for recent

transactions over $1 billion and those over $5 billion, since premiums paid may vary

with the size of the transaction.

The analysis was based on the one day, one week and four week implied premiums for

the transactions examined. The implied premiums were calculated by comparing the

offer price for the target firm on the announcement date with the per share price of the

target firm one day, one week, and four weeks prior to the announcement of the

transaction. The results of these calculations are given in Table 8-5.

Based on this analysis, Lazard determined an applicable premium range of 20% to 30%

for SunGard and applied this range to SunGard's share price of $24.95 on March 18,

2005. Using this information, Lazard calculated an implied price per share range for

SunGard common stock of $29.94 (i.e., 1.2 x $24.95) to $32.44 (1.3 x $24.95).

Summary and Conclusions

Table 8-6 summarizes the estimated valuation ranges based on the alternative valuation

methods employed by Lazard Freres. Note that the $36 per offer price compares

favorably to the estimated average valuation range, representing a premium of 12%

(i.e., $36/$27.11) to 33% (i.e., $36/$32.19). Consequently, Lazard Freres viewed the

investor group's offer price for SunGard as fair.

Discussion Questions:

1) Discuss the strengths and weaknesses of each valuation method employed by these

investment banks in constructing estimates of SunGard's value for the Fairness Opinion

Letter. Be specific.

2) Why do you believe that the percentage difference between the maximum and

minimum valuation estimates varies so much from one valuation method to another?

See Table 8-7.

Answer:

Which of the following is not generally considered a valuation method?

a. Discounted cash flow method

b. Comparable companies' method

c. Share exchange ratio method

d. Liquidation value method

e. Comparable transaction's method

Answer: