1) an investor can design a risky portfolio based on two stocks, a and b. stock a has an

expected return of 21% and a standard deviation of return of 39%. stock b has an

expected return of 14% and a standard deviation of return of 20%. the correlation

coefficient between the returns of a and b is .4. the risk-free rate of return is 5%. the

standard deviation of the returns on the optimal risky portfolio is _________.

a.25.5%

b.22.3%

c.21.4%

d.20.7%

2) the assets of a mutual fund are $25 million. the liabilities are $4 million. if the fund

has 700,000 shares outstanding and pays a $3 dividend, what is the dividend yield?

a.5%

b.10%

c.15%

d.20%

3) venture capital is _________.

a.frequently used to expand the businesses of well-established companies

b.supplied by venture capital funds and individuals to start-up companies

c.illegal under current u.s. laws

d.most frequently issued with the help of investment bankers

4) ______________ in interest rates are associated with stock market declines.

a.anticipated increases

b.unanticipated increases

c.anticipated decreases

d.unanticipated decreases

5) the __________ system enables exchange members to send orders directly to a

specialist over computer lines.

a.fax

b.direct plus

c.nasdaq

d.superdot

6) diversification is most effective when security returns are _________.

a.high

b.negatively correlated

c.positively correlated

d.uncorrelated

7) as of 2011, approximately _____ of mutual fund assets were invested in bond funds.

a.14%

b.19%

c.37%

d.47%

8) if all investors become more risk averse, the sml will _______________ and stock

prices will _______________.

a.shift upward; rise

b.shift downward; fall

c.have the same intercept with a steeper slope; fall

d.have the same intercept with a flatter slope; rise

9) the semistrong form of the efficient market hypothesis implies that ____________

generate abnormal returns and ____________ generate abnormal returns.

a.technical analysis cannot; fundamental analysis can

b.technical analysis can; fundamental analysis can

c.technical analysis can; fundamental analysis cannot

d.technical analysis cannot; fundamental analysis cannot

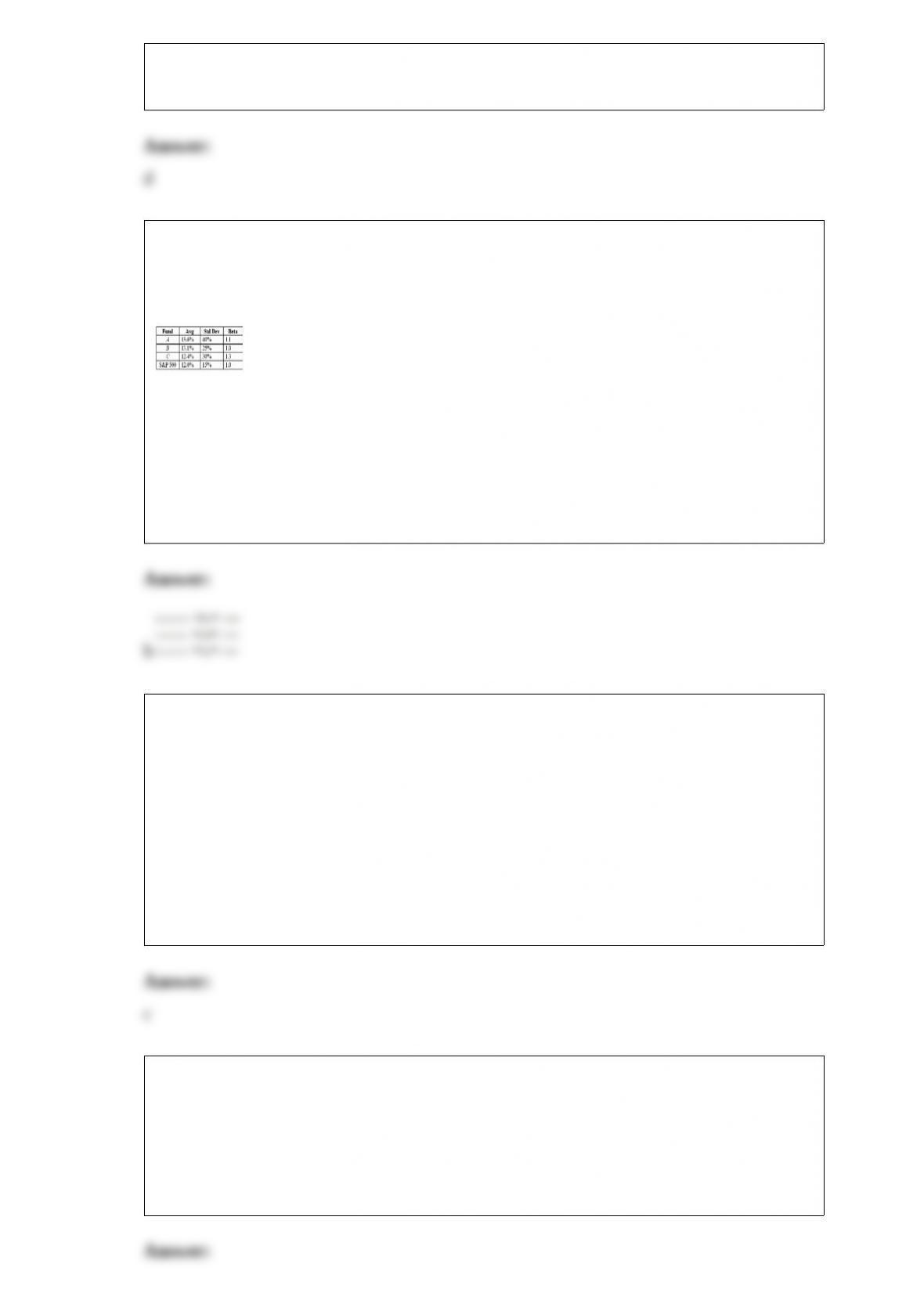

10) the average returns, standard deviations, and betas for three funds are given below

along with data for the s&p 500 index. the risk-free return during the sample period is

6%.

you want to evaluate the three mutual funds using the treynor measure for performance

evaluation. the fund with the highest treynor measure of performance is __________.

a.fund a

b.fund b

c.fund c

d.the answer cannot be determined from the information given.

11) which of the following is not a type of real estate investment trust?

i. equity trust

ii. debt trust

iii. mortgage trust

iv. unit trust

a.i and ii only

b.ii only

c.ii and iv only

d.i, ii, and iii

12) a safe driver who drives faster as a result of purchasing collision car insurance

would be an example of the ___________ problem.

a.moral hazard

b.adverse selection

c.texas hedge

d.actuarial error

13) the geometric average of -12%, 20%, and 25% is _________.

a.8.42%

b.11%

c.9.7%

d.18.88%

14) as you get older, you decide to reduce the risk level of your retirement portfolio

because your portfolio is nearing your minimum acceptable level. as the portfolio does

better, you reallocate funds into higher-risk categories. you are practicing a form of

____________.

a.manipulating tax shelters

b.involuntary intergenerational transfers

c.excessive savings

d.dynamic hedging

15) financial intermediaries exist because small investors cannot efficiently _________.

a.diversify their portfolios

b.gather information

c.monitor their portfolios

d.all of these options

16) all but which one of the following indices is value weighted?

a.nasdaq composite

b.s&p 500

c.wilshire 5000

d.djia

17) you would like to hold a protective put position on the stock of avalon corporation

to lock in a guaranteed minimum value of $50 at year-end. avalon currently sells for

$50. over the next year, the stock price will increase by 10% or decrease by 10%. the

t-bill rate is 5%. unfortunately, no put options are traded on avalon co.

suppose the desired put options with x = 50 were traded. how much would it cost to

purchase?

a.$1.19

b.$2.38

c.$5

d.$3.33

18) if an investor is a successful market timer, his distribution of monthly portfolio

returns will __________.

a.be skewed to the left

b.be skewed to the right

c.exhibit kurtosis

d.exhibit neither skewness nor kurtosis

19) all other things equal, a bond’s duration is _________.

a.higher when the coupon rate is higher

b.lower when the coupon rate is higher

c.the same when the coupon rate is higher

d.indeterminable when the coupon rate is high

20) an example of a neutral pure play is _______.

a.pairs trading

b.statistical arbitrage

c.convergence arbitrage

d.directional strategy