If the hedge ratio for a stock call is 0.50, the hedge ratio for a put with the same

expiration date and exercise price as the call would be

A. 0.30.

B. 0.50.

C. −0.60.

D. −0.50.

E. −0.17.

A Treasury bill with a par value of $100,000 due two months from now is selling today

for $98,039 with an effective annual yield of

A. 12.40%.

B. 12.55%.

C. 12.62%.

D. 12.68%.

E. None of the options are correct.

Which equity index had the highest volatility in terms of U.S. dollar-denominated

returns for the period of five years ending in October 2016?

A. Shanghai

B. India

C. Nikkei

D. U.S.

You want to buy 100 shares of Hotstock Inc. at the best possible price as quickly as

possible. You would most likely place a

A. stop-loss order.

B. stop-buy order.

C. market order.

D. limit-sell order.

E. limit-buy order.

Which of the following statement(s) is(are) false regarding the selection of a portfolio

from those that lie on the

capital allocation line?

I) Less risk-averse investors will invest more in the risk-free security and less in the

optimal risky portfolio than

more risk-averse investors.

II) More risk-averse investors will invest less in the optimal risky portfolio and more in

the risk-free security than

less risk-averse investors.

III) Investors choose the portfolio that maximizes their expected utility.

A. I only

B. II only

C. III only

D. I and II

E. I and III

Consider the single factor APT. Portfolio A has a beta of 0.5 and an expected return of

12%. Portfolio B has a beta of 0.4 and an expected return of 13%. The risk-free rate of

return is 5%. If you wanted to take advantage of an arbitrage opportunity, you should

take a short position in portfolio _________ and a long position in portfolio _________.

A. A; A

B. A; B

C. B; A

D. B; B

Proponents of the EMH typically advocate

A. buying individual stocks on margin and trading frequently.

B. investing in hedge funds.

C. a passive investment strategy.

D. buying individual stocks on margin, trading frequently, and investing in hedge funds.

E. investing in hedge funds and a passive investment strategy.

The prudent investor rule requires

A. executives of companies to avoid investing in options of companies by which they

are employed.

B. executives of companies to disclose their transactions in stocks of companies by

which they are employed.

C. professional investors who manage money for others to avoid all risky investments.

D. professional investors who manage money for others to constrain their investments

to those that would have been approved by the prudent investor.

The expected impact of unanticipated macroeconomic events on a security’s return

during the period is

A. included in the security’s expected return.

B. zero.

C. equal to the risk-free rate.

D. proportional to the firm’s beta.

E. infinite.

Of the following types of mutual funds, an investor who wishes to invest in a

diversified portfolio of stocks worldwide (including the U.S.) should choose

A. international funds.

B. global funds.

C. regional funds.

D. emerging-market funds.

Your opinion is that Boeing has an expected rate of return of 0.0952. It has a beta of

0.92. The risk-free rate is

0.04 and the market expected rate of return is 0.10. According to the Capital Asset

Pricing Model, this security

Is

A. underpriced.

B. overpriced.

C. fairly priced.

D. Cannot be determined from data provided.

You invest $100 in a risky asset with an expected rate of return of 0.11 and a standard

deviation of 0.20 and a

T-bill with a rate of return of 0.03.

The slope of the capital allocation line formed with the risky asset and the risk-free

asset is equal to

A. 0.47.

B. 0.80.

C. 2.14.

D. 0.40.

E. Cannot be determined.

Which of the following statements is(are) true?

I) Risk-averse investors reject investments that are fair games.

II) Risk-neutral investors judge risky investments only by the expected returns.

III) Risk-averse investors judge investments only by their riskiness.

IV) Risk-loving investors will not engage in fair games.

A. I only

B. II only

C. I and II only

D. II and III only

E. II, III, and IV only

The riskmanagement section of an Investment Policy Statement for individual investors

typically contains

A. relevant constraints.

B. other relevant considerations.

C. performance measurement accountabilities, metrics for risk measurement, and the

rebalancing process.

D. relevant constraints and other relevant considerations.

E. All of the options are correct.

The efficient market hypothesis

A. implies that security prices properly reflect information available to investors.

B. has little empirical validity.

C. implies that active traders will find it difficult to outperform a buy and hold strategy.

D. has little empirical validity and implies that active traders will find it difficult to

outperform a buy and hold strategy.

E. implies that security prices properly reflect information available to investors and

that active traders will find it difficult to outperform a buy and hold strategy.

__________ in the process of asset allocation.

A. Deriving the efficient portfolio frontier is a step

B. Specifying asset classes to be included in the portfolio is a step

C. Specifying the capital market expectations is a step

D. All of the options are steps.

E. None of the options are steps.

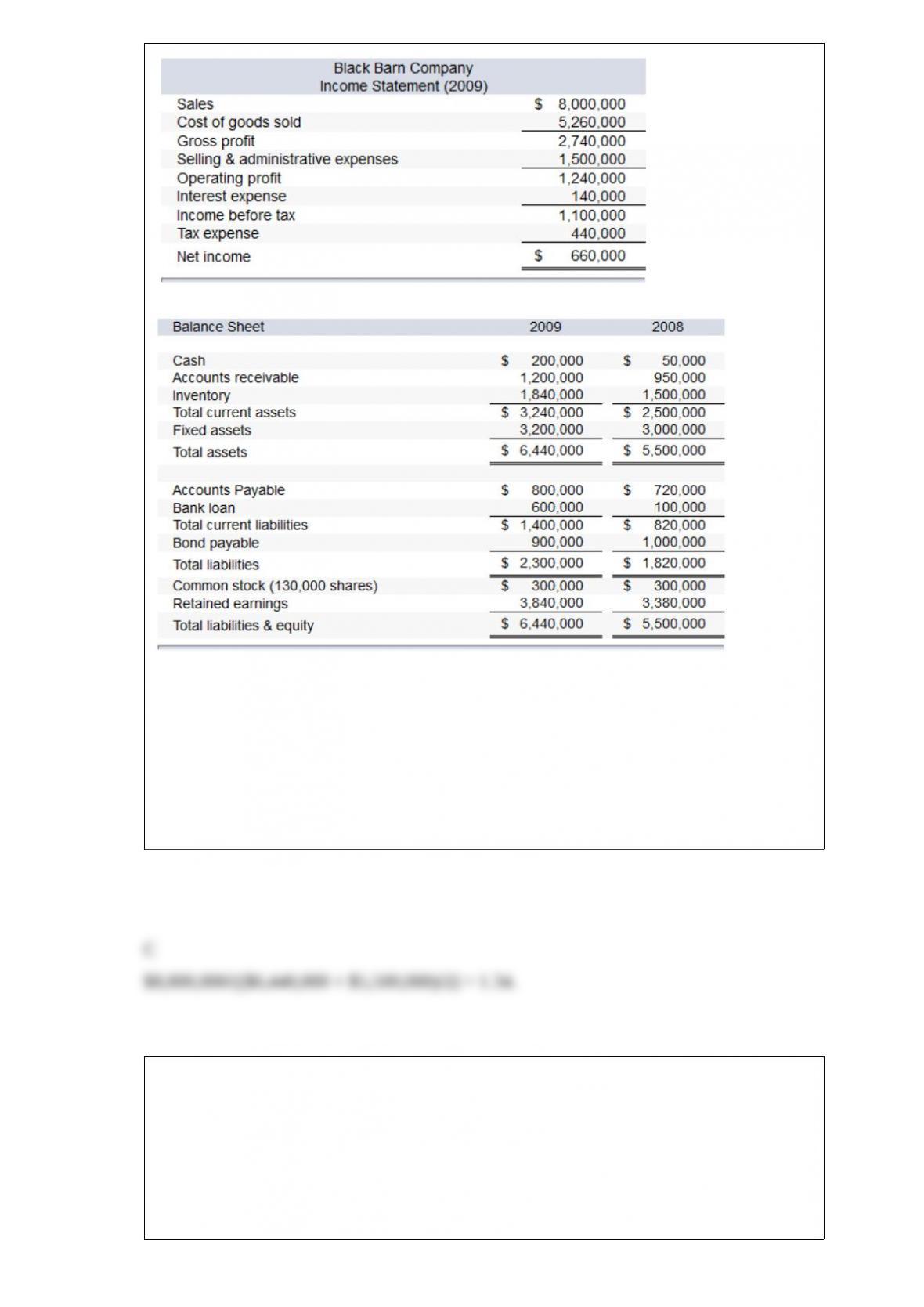

The financial statements of Black Barn Company are given below.

Note: The common shares are trading in the stock market for $40 each.

Refer to the financial statements of Black Barn Company. The firm’s asset turnover

ratio for 2009 is

A. 1.79.

B. 1.63.

C. 1.34.

D. 2.58.

E. None of the options are correct.

One of the assumptions of the CAPM is that investors exhibit myopic behavior. What

does this mean?

A. They plan for one identical holding period.

B. They are price takers who can’t affect market prices through their trades.

C. They are mean-variance optimizers.

D. They have the same economic view of the world.

E. They pay no taxes or transactions costs.

You are considering acquiring a common stock that you would like to hold for one year.

You expect to receive both $3.50 in dividends and $42 from the sale of the stock at the

end of the year. The maximum price you would pay for the stock today is _____ if you

wanted to earn a 10% return.

A. $23.91

B. $24.11

C. $26.52

D. $27.50

E. None of the options are correct.

The Yachtsman Fund had NAV per share of $36.12 on January 1, 2016. On December

31 of the same year, the fund’s NAV was $39.71. Income distributions were $0.64, and

the fund had capital gain distributions of $1.13. Without considering taxes and

transactions costs, what rate of return did an investor receive on the Yachtsman Fund

last year?

A. 22.92%

B. 17.68%

C. 14.39%

D. 18.52%

E. 14.84%

Assume you sold short 100 shares of common stock at $50 per share. The initial margin

is 60%. What would be the maintenance margin if a margin call is made at a stock price

of $60?

A. 40%

B. 33%

C. 35%

D. 25%

The current market price of a share of MSI stock is $15. If a put option on this stock has

a strike price of $20, the put

A. is out of the money.

B. is in the money.

C. can be exercised profitably.

D. is out of the money and can be exercised profitably.

E.is in the money and can be exercised profitably.

Jagannathan and Wang (2006) find that the CCAPM explains returns ______ the Fama

French three factor model, and that the Fama French three factor model explains returns

______ the traditional CAPM.

A. worse than; worse than

B. worse than; better than

C. better than; better than

D. better than; worse than

E. equally as well as; equally as well as

The most common short-term interest rate used in the swap market is

A. the U.S. discount rate.

B. the U.S. prime rate.

C. the U.S. fed funds rate.

D. LIBOR.

E. None of the options are correct.

Suppose you purchase one WFM May 100 call contract at $5 and write one WFM May

105 call contract at $2. The maximum loss you could suffer from your strategy is

A. $200.

B.$300.

C. zero.

D. $500.

Which of the following is true about the security market line (SML) derived from the

APT?

A. The SML has a downward slope.

B. The SML for the APT shows expected return in relation to portfolio standard

deviation.

C. The SML for the APT has an intercept equal to the expected return on the market

portfolio.

D. The benchmark portfolio for the SML may be any well-diversified portfolio.

E. The SML is not relevant for the APT.

If the stock price decreases, the price of a put option on that stock __________, and that

of a call option __________.

A. decreases; increases

B. decreases; decreases

C. increases; decreases

D. increases; increases

E. does not change; does not change

A protective put strategy is

A.a long put plus a long position in the underlying asset.

B.a long put plus a long call on the same underlying asset.

C. a long call plus a short put on the same underlying asset.

D. a long put plus a short call on the same underlying asset.

E. None of the options are correct.

The put-call parity theorem

A. represents the proper relationship between put and call prices.

B. allows for arbitrage opportunities if violated.

C. may be violated by small amounts, but not enough to earn arbitrage profits, once

transaction costs are considered.

D.All of the options are correct.

E. None of the options are correct.

One year ago, you purchased a newly-issued TIPS bond that has a 6% coupon rate, five

years to maturity, and a par value of $1,000. The average inflation rate over the year

was 4.2%. What is the amount of the coupon payment you will receive, and what is the

current face value of the bond?

A. $60.00, $1,000

B. $42.00, $1,042

C. $60.00, $1,042

D. $62.52, $1,042

E. $102.00, $1,000

Fools Gold Mining Company is expected to pay a dividend of $8 in the upcoming year.

Dividends are expected to decline at the rate of 2% per year. The risk-free rate of return

is 6%, and the expected return on the market portfolio is 14%. The stock of Fools Gold

Mining Company has a beta of 0.25. The return you should require on the stock is

A. 2%.

B. 4%.

C. 6%.

D. 8%.

Which of the following functions do investment companies perform for their investors?

A. Record keeping and administration

B. Diversification and divisibility

C. Professional management

D. Lower transaction costs

E. All of the options.

The investment horizon is

A. the investor’s expected age at death.

B. the starting date for establishing investment constraints.

C. based on the investor’s risk tolerance.

D. the date at which the portfolio is expected to be fully or partially liquidated.

The duration of a coupon bond

A. does not change after the bond is issued.

B. can accurately predict the price change of the bond for any interest-rate change.

C. will decrease as the yield to maturity decreases.

D. All of the options are true.

E. None of the options are true.

A security has an expected rate of return of 0.13 and a beta of 2.1. The market expected

rate of return is 0.09,

and the risk-free rate is 0.045. The alpha of the stock is

A. –0.95%.

B. –1.7%.

C. 8.3%.

D. 5.5%.