1) Currency options are only traded on exchanges. That is, there is no over-the-counter

market for options.

a. True

b. False

2) Assume zero transaction costs. If the 90-day forward rate of the euro underestimates

the spot rate 90 days from now, then the real cost of hedging payables will be:

a. positive

b. negative

c. positive if the forward rate exhibits a premium, and negative if the forward rate

exhibits a discount

d. zero

3) If potential acquirers are based in different countries, their required rates of return

when considering a specific target will only vary if the desired use of the target is

different.

a. True

b. False

4) The Direct Loan Program is administered by the:

a. Private Export Funding Corporation (PEFCO)

b. Overseas Private Investment Corporation (OPIC)

c. Ex-Imbank

d. Foreign Credit Insurance Association (FCIA)

5) Use the following information to calculate the dollar cost of using a money market

hedge to hedge 200,000 pounds of payables due in 180 days. Assume the firm has no

excess cash. Assume the spot rate of the pound is $2.02, the 180-day forward rate is

$2.00. The British interest rate is 5%, and the U.S. interest rate is 4% over the 180-day

period.

a. $391,210

b. $396,190

c. $388,210

d. $384,761

e. none of the above

6) According to the international Fisher effect, if U.S. investors expect a 5% rate of

domestic inflation over one year, and a 2% rate of inflation in European countries that

use the euro, and require a 3% real return on investments over one year, the nominal

interest rate on one-year U.S. Treasury securities would be:

a. 2%

b. 3%

c. -2%

d. 5%

e. 8%

7) An MNC should periodically reassess its investments to determine whether to divest

them.

a. True

b. False

8) When determining whether a particular proposed project in a foreign country is

feasible:

a. a country risk rating can adequately substitute for a capital budgeting analysis

b. country risk analysis should be incorporated within the capital budgeting analysis

c. the effect of country risk on sales revenue is more important than the effect on cash

flows

d. the project with the highest country risk rating (lowest country risk) should be

accepted

e. B and D

9) As a result of the European Union, restrictions on exports between ____ were

reduced or eliminated.

a. member countries and the U.S

b. member countries

c. member countries and European non-members

d. none of the above

10) The U.S. dollar is not ever used as a medium of exchange in:

a. industrialized countries outside the U.S

b. in any Latin American countries

c. in Eastern European countries where foreign exchange restrictions exist

d. none of the above

11) Assume zero transaction costs. If the 180-day forward rate overestimates the spot

rate 180 days from now, then the real cost of hedging payables will be:

a. positive

b. negative

c. positive if the forward rate exhibits a premium, and negative if the forward rate

exhibits a discount

d. zero

12) According to the text, international trade activity has generally ____ over time. This

should cause the popularity of trade finance techniques to ____ over time.

a. increased; increase

b. increased; decrease

c. decreased; increase

d. decreased; decrease

13) The following regression model was estimated to forecast the value of the

Malaysian ringgit (MYR):

MYRt = a0 + a1INCt – 1 + a2INFt – 1 + mt,

where MYR is the quarterly change in the ringgit, INF is the previous quarterly

percentage change in the inflation differential, and INC is the previous quarterly

percentage change in the income growth differential. Regression results indicate

coefficients of a0 = .005; a1 = .4; and a2 = .7. The most recent quarterly percentage

change in the inflation differential is -5%, while the most recent quarterly percentage

change in the income differential is 3%. Using this information, the forecast for the

percentage change in the ringgit is:

a. 4.60%

b. -1.80%

c. 5.2%

d. -4.60%

e. none of the above

14) The Bretton Woods Agreement is an agreement to standardize banks’ capital

requirements across countries; the resulting capital ratios are computed using

risk-weighted assets.

a. True

b. False

15) Assume that the inflation rate becomes much higher in the U.K. relative to the U.S.

This will place ____ pressure on the value of the British pound. Also, assume that

interest rates in the U.K. begin to rise relative to interest rates in the U.S. The change in

interest rates will place ____ pressure on the value of the British pound.

a. upward; downward

b. upward; upward

c. downward; upward

d. downward; downward

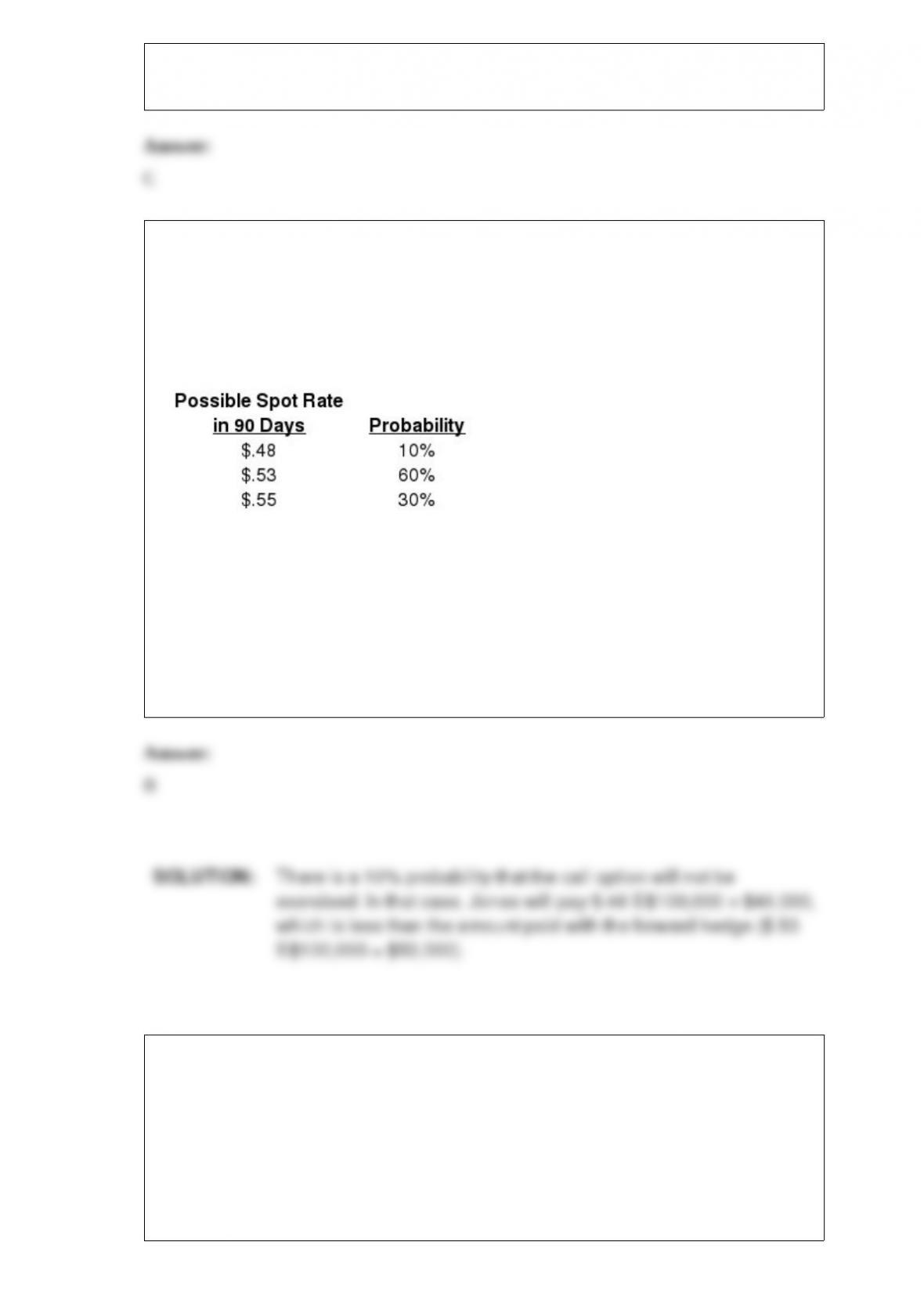

16) Assume that Jones Co. will need to purchase 100,000 Singapore dollars (S$) in 180

days. Today’s spot rate of the S$ is $.50, and the 180-day forward rate is $.53. A call

option on S$ exists, with an exercise price of $.52, a premium of $.02, and a 180-day

expiration date. A put option on S$ exists, with an exercise price of $.51, a premium of

$.02, and a 180-day expiration date. Jones has developed the following probability

distribution for the spot rate in 180 days:

The probability that the forward hedge will result in a higher payment than the options

hedge is ____ (include the amount paid for the premium when estimating the U.S.

dollars required for the options hedge).

a. 0%

b. 10%

c. 30%

d. 40%

e. 70%

17) Magent Co. is a U.S. company that has exposure to the Swiss francs (SF) and

Danish kroner (DK). It has net inflows of SF200 million and net outflows of DK500

million. The present exchange rate of the SF is about $.40 while the present exchange

rate of the DK is $.10. Magent Co. has not hedged these positions. The SF and DK are

highly correlated in their movements against the dollar. If the dollar weakens, then

Magent Co. will:

a. benefit, because the dollar value of its SF position exceeds the dollar value of its DK

position

b. benefit, because the dollar value of its DK position exceeds the dollar value of its SF

position

c. be adversely affected, because the dollar value of its SF position exceeds the dollar

value of its DK position

d. be adversely affected, because the dollar value of its DK position exceeds the dollar

value of its SF position

18) To hedge a payable position in a foreign currency with a money market hedge, the

MNC would borrow the foreign currency, convert it to dollars, and invest that amount

in the U.S. until the payable is due.

a. True

b. False

19) The ____ the existing spot price relative to the strike price, the ____ valuable the

call options will be.

a. higher; less

b. higher; more

c. lower; less

d. lower; more

20) A country’s net outflow of funds ____ affect its interest rates, and ____ affect its

economic conditions.

a. does; does

b. does; does not

c. does not; does not

d. does not; does

21) Which of the following is not true regarding a banker’s acceptance?

a. It can be beneficial to the exporter, as he does not have to worry about the credit risk

of the importer

b. It can be beneficial to the importer, as he may have greater access to foreign markets

when purchasing supplies

c. It can be beneficial to the bank accepting the draft in that it earns a commission for

creating an acceptance

d. It is a sight draft

e. All of the above are true

22) ____ is not a cost-related motive for direct foreign investment.

a. Exploiting monopolistic advantages

b. Fully benefiting from economies of scale

c. Using foreign factors of production

d. Using foreign raw materials

23) A strong dollar places ____ pressure on U.S. inflation, which in turn places ____

pressure on U.S. interest rates, which in turn place ____ pressure on U.S. bond prices.

a. downward; upward; upward

b. downward; downward; upward

c. upward; upward; downward

d. upward; downward; upward

24) Which of the following countries have not adopted the euro?

a. Germany

b. Italy

c. Switzerland

d. France

25) Since forward contracts are easy to use for hedging, any exposure to exchange rate

movements should be hedged.

a. True

b. False

26) The real cost of hedging payables with a forward contract equals:

a. the nominal cost of hedging minus the nominal cost of not hedging

b. the nominal cost of not hedging minus the nominal cost of hedging

c. the nominal cost of hedging divided by the nominal cost of not hedging

d. the nominal cost of not hedging divided by the nominal cost of hedging

27) In general, MNCs probably prefer to use ____ foreign debt when their foreign

subsidiaries are subject to ____ local interest rates.

a. more; low

b. more; high

c. less; low

d. B and C

e. none of the above

28) If the spot rate of the euro increased substantially over a one-month period, the

futures price on euros would likely ____ over that same period.

a. increase slightly

b. decrease substantially

c. increase substantially

d. stay the same

29) In comparing exporting to direct foreign investment (DFI), an exporting operation

will likely incur ____ fixed production costs and ____ transportation costs than DFI.

a. higher; higher

b. higher; lower

c. lower; lower

d. lower; higher

30) Which of the following is not true regarding ADRs?

a. ADRs are denominated in the currency of the stock’s home country

b. ADRs enable U.S. investors to avoid cross-border transactions

c. ADRs allow non-U.S. firms to tap into U.S. market for funds

d. ADRs sometimes allow for arbitrage opportunities

31) An increase in U.S. interest rates relative to German interest rates would likely ____

the U.S. demand for euros and ____ the supply of euros for sale.

a. reduce; increase

b. increase; reduce

c. reduce; reduce

d. increase; increase

32) Which of the following is not a technique to assess country risk?

a. Gamma technique

b. Delphi technique

c. checklist approach

d. inspection visits

33) Which of the following countries was probably the least affected (directly or

indirectly) by the Asian crisis?

a. Thailand

b. Indonesia

c. Russia

d. China

e. Malaysia

34) ____ is not a revenue-related motive for direct foreign investment.

a. Attracting new sources of demand

b. Fully benefiting from economies of scale

c. Exploiting monopolistic advantages

d. Entering profitable markets

35) The currency of Country X is pegged to the currency of Country Y. Assume that

Country Y’s currency depreciates against the currency of Country Z. It is likely that

Country X will export ____ to Country Z and import ____ from Country Z.

a. more; more

b. less; less

c. more; less

d. less; more

36) A share of the ADR of a Dutch firm represents one share of that firm’s stock that is

traded on a Dutch stock exchange. The share price of the firm was 15 euros when the

Dutch market closed. As the U.S. market opens, the euro is worth $1.10. Thus, the price

of the ADR should be ____.

a. $13.64

b. $15.00

c. $16.50

d. 16.50 euros

e. none of the above