1) information exposure is a type of foreign exchange risk.

2) the spread is the average of deposit and loan interest rates.

3) in the uncovered interest rate parity, the forward rate is assumed to be the unbiased

predictor of the future spot exchange rate.

4) in general, the smaller the country is, the more likely it is to peg its exchange rate.

5) the degree to which a firm is affected by exchange rate changes is known as currency

risk.

6) inflation from one country can be transmitted to another if a floating exchange rate is

being used.

7) multinational cash management is used by the firm to move cash to keep overall cash

needs low.

8) under the monetary approach to exchange rate, a rise in domestic income will cause a

depreciation of domestic currency.

9) a managed floating exchange rate is a market determined exchange system as long as

rates stay between target zones as mandated by legislative commitments.

10) an example of a fixed exchange rate was the gold standard.

11) the variability of the firms foreign exchange risk arises from uncertainty about

future exchange rates.

12) under the fixed exchange rate, inflation from one country can be transmitted to the

other country.

13) multinational cash management involves managing the parent-firms capital

holdings separately from any foreign capital holdings.

14) deviations from interest rate parity could be the result of:

a.different tax treatment of income and foreign exchange earnings

b.political risk

c.transaction costs

d.all of the above are correct

15) the risk present in all investment opportunities is known as ________ risk.

a.systematic

b.nonsystematic

c.portfolio

d.diversification

16) if you hold the futures contract until september 15th and the spot rate for pounds on

september 15th is $1.67 per pound, you will:

a.not exercise the futures contract

b.lose on your position by $1,250

c.gain on your position by $1,250

d.break even by the amount of the margin

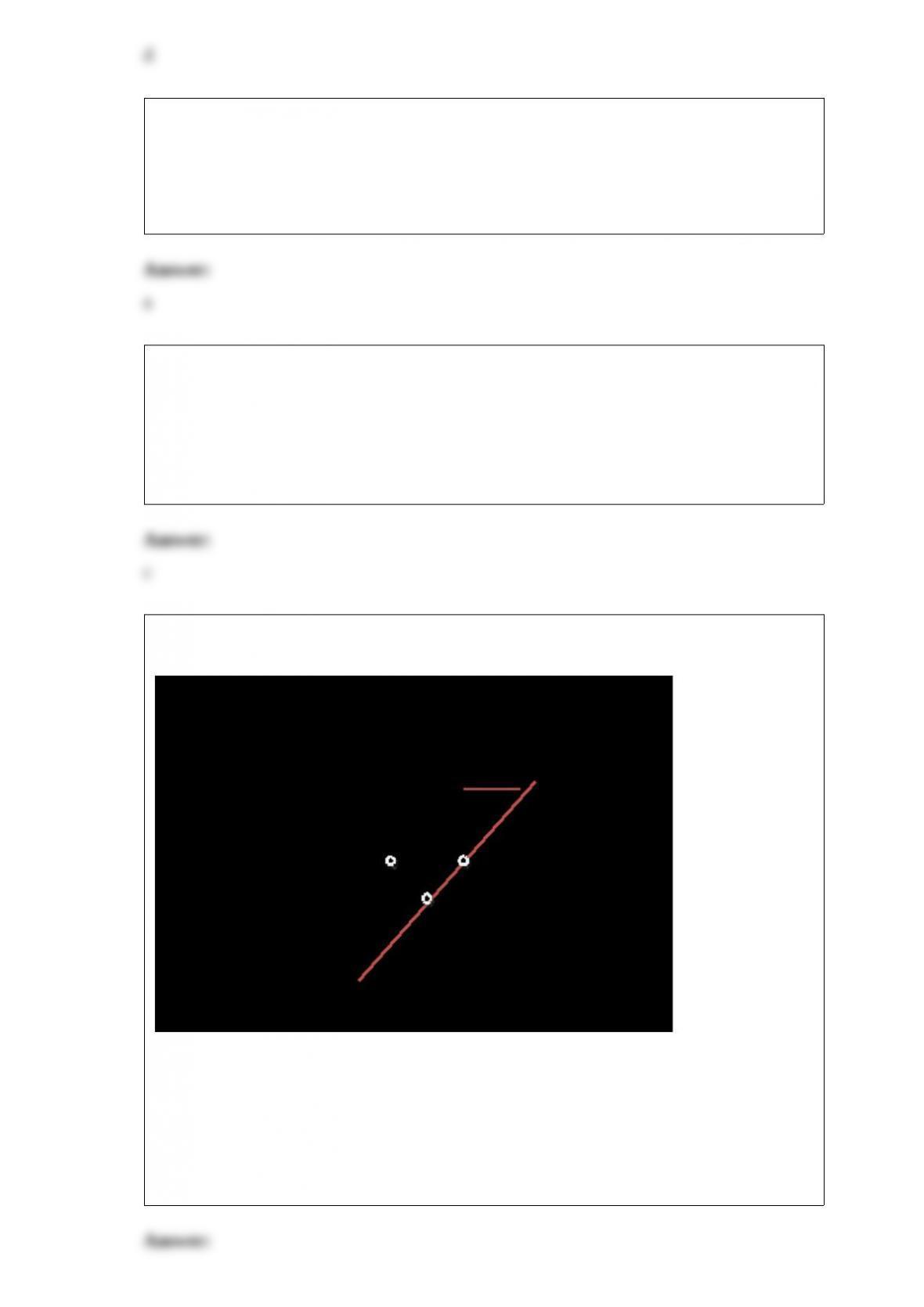

17) figure 1.2

to figure 1.2. suppose that the market for euro is initially in equilibrium at point a with

the exchange rate $2.00 per euro. then the supply curve shifts to s2. if the european

central bank wants to fix the exchange rate at $2.00/euro, they have to:

a.buy euro and sell dollar by the amount of q3 q1

b.sell euro and buy dollar by the amount of q3 q1

c.sell only euro by the amount of q3 q1 and leave dollar alone

d.buy only euro by the amount of q3 q1 and leave dollar alone

18) a documentary credit is issued to importer to pay exporter for an amount of gbp

40,000 payable with drafts drawn at 30 days from the date of shipment. document is

presented with bills of lading. this is an example of:

a.export netting

b.swap contract

c.letter of credit

d.future contract

19) a detailed list of the content that is shipped, and can be used to identify missing or

damaged items is called a(n):

a.adjusted payment

b.import contract

c.contract guarantee

d.bill of lading

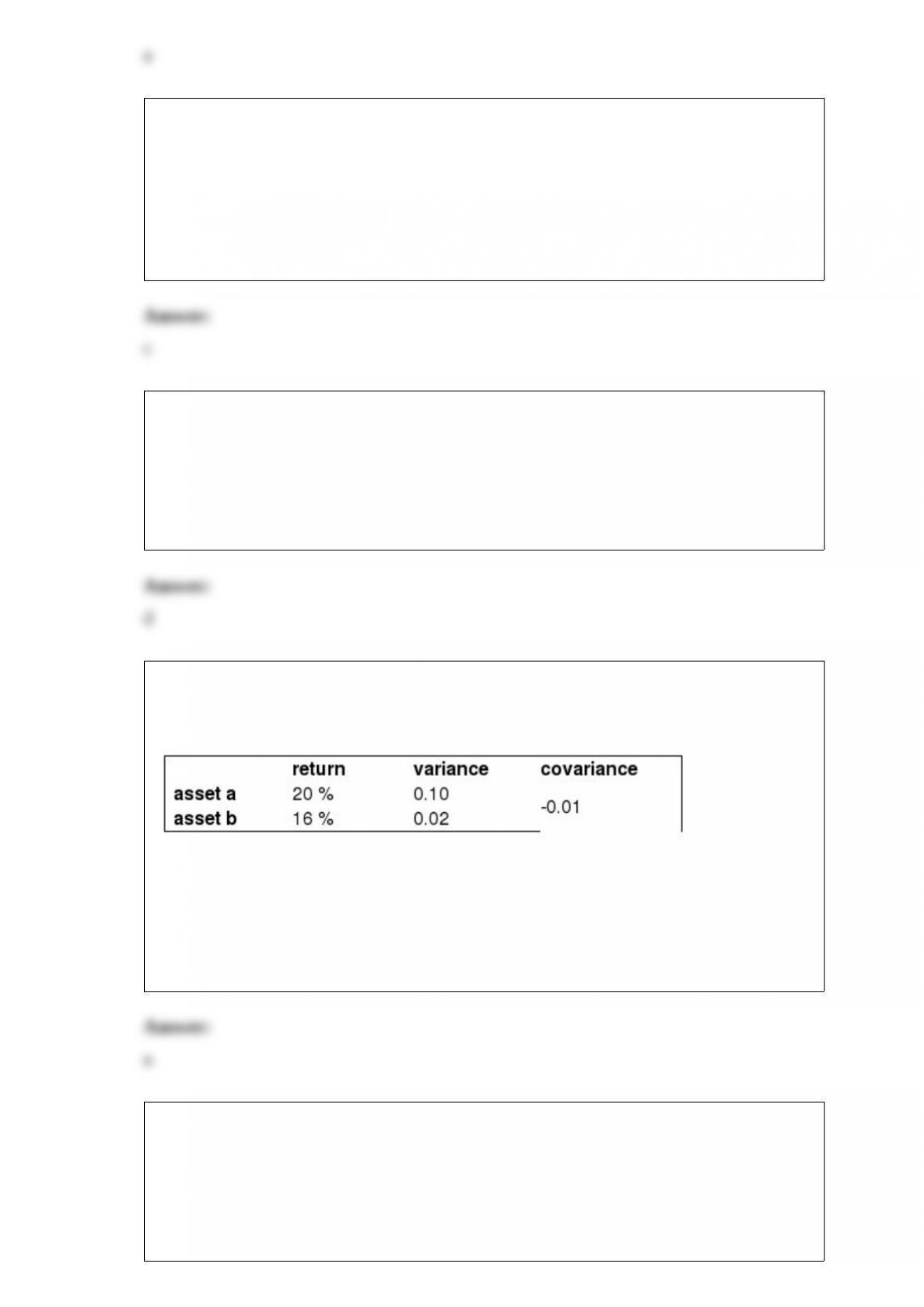

20) assume that you have a choice of two assets, a and b, and a portfolio of an equal

share of the two assets. assume also that the assets have the following statistics:

table 10-1:

see table 10-1. if your portfolio includes a combination of 20% asset a and 80% asset b,

then your expected return is:

a.16.8 %

b.18 %

c.19.2 %

d.24 %

21) which of the following are advantages of netting?

i.avoiding transaction costs

ii.shifting profits to different subsidiaries

iii.avoiding taxes for the parent firm

iv.increasing flexibility in the parent firm

a.i only

b.ii only

c.i and iv

d.ii, iii, and iv

22) what did the great recession in 2007 show about financial markets?

a.financial markets throughout the world are highly connected

b.segmented markets are those most exposed to risk during financial crises

c.the imf failed to target corruption in financial markets before 2007 effectively

d.the housing bubble only affected investors with a direct connection to the housing

market

23) currency plus commercial bank reserves held against deposits:

a.base money

b.temporary money

c.international credit

d.domestic reserves

24) assume that citibank quotes you a buy rate of $1.50 per pound and a sell rate of

$1.60 per pound. how much will you receive in dollars, if you sell 1,000 pound to

citibank?

a.$625

b.$666.67

c.$1,500

d.$1,600