1) under fasb 52, when a net translation exposure exists,

a.a derivatives hedge is necessary to bring balance to the consolidated balance sheet

after an exchange rate change

b.a money market hedge is necessary to bring balance to the consolidated balance sheet

after an exchange rate change

c.a cumulative translation adjustment account is necessary to bring balance to the

consolidated balance sheet after an exchange rate change

d.none of the above

2) a country’s international transactions can be grouped into the following three main

types:

a.current account, medium term account, and long term capital account

b.current account, long term capital account, and official reserve account

c.current account, capital account, and official reserve account

d.capital account, official reserve account, trade account

3) you are a u.s.-based treasurer with $1,000,000 to invest. the dollar-euro exchange

rate is quoted as $1.60 = 1.00 and the dollar-pound exchange rate is quoted at $2.00 =

£1.00. if a bank quotes you a cross rate of £1.00 = 1.20 how can you make money?

a.no arbitrage is possible

b.buy euro at $1.60/, buy £ at 1.20/£, sell £ at $2/£

c.buy £ $2/£, buy at 1.20/£, sell at $1.60/

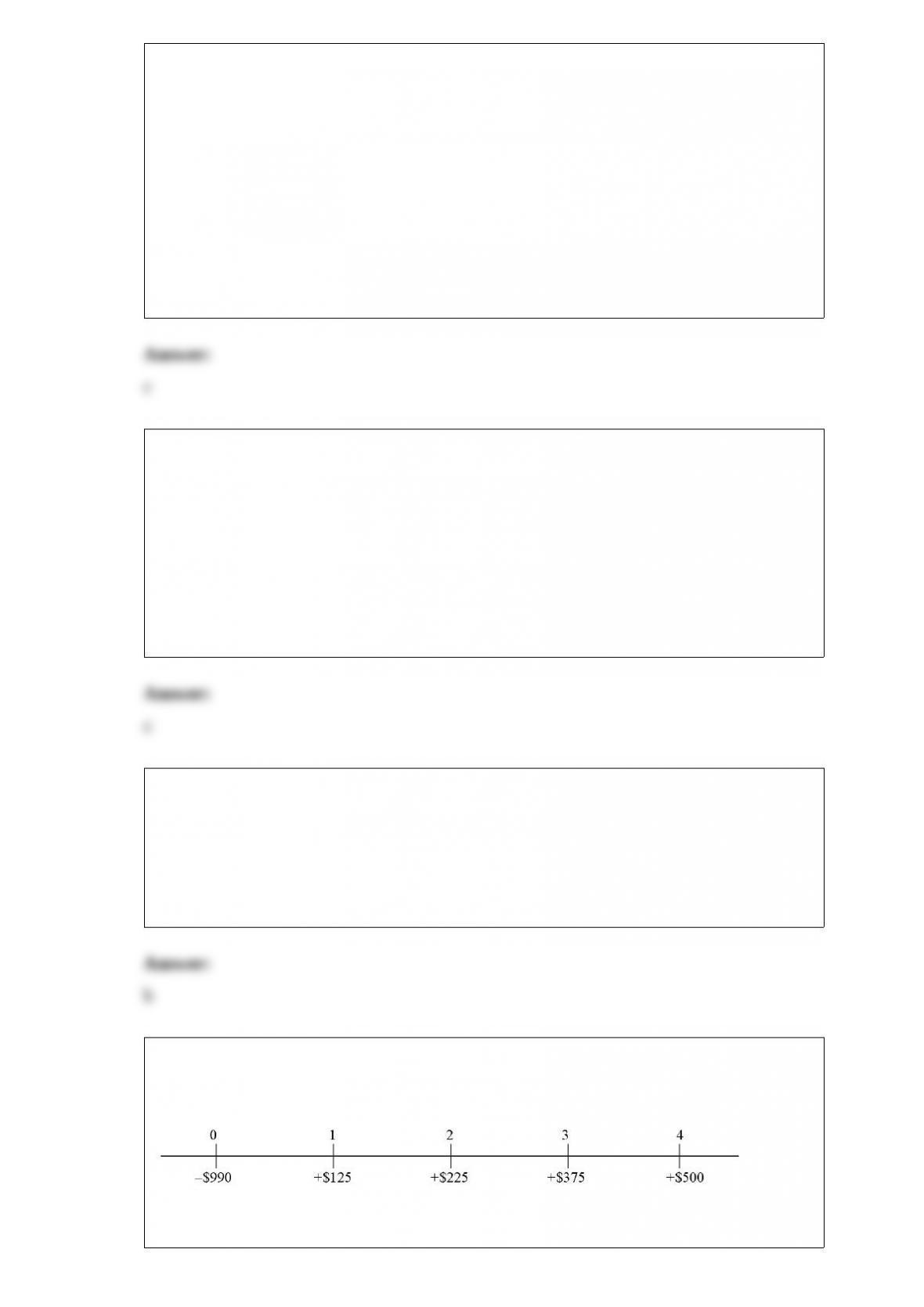

4) consider a project of the cornell haul moving company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

the firm’s tax rate is 34%; the firm’s bonds trade with a yield to maturity of 8%; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity,

the required return would be 10%

what is the levered after-tax incremental cash flow for year 2?

a.$185,796,000

b.$215,152,000

c.$267,952,000

d.$284,848,000

e.none of the above

5) for a firm confronted with a fixed schedule of possible new investments, any policy

that lowers the firm’s cost of capital will increase the profitable capital expenditures the

firm takes on and increase the wealth of the firm’s shareholders. one such policy is

a.internationalizing the firm’s capital budgeting opportunities

b.internationalizing the firm’s cost of capital

c.investing in riskier projects financed with debt

d.none of the above

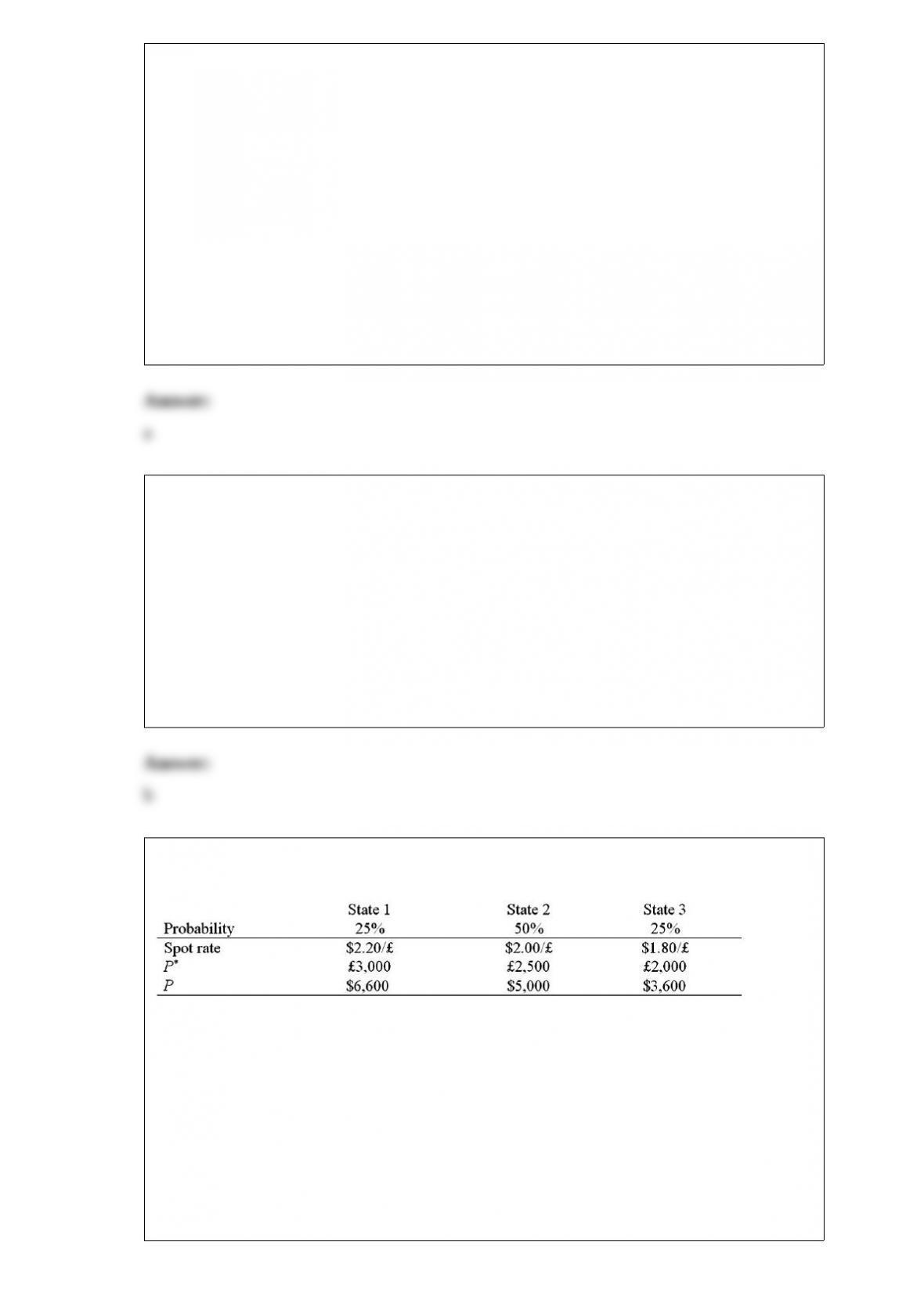

6) a u.s. firm holds an asset in great britain and faces the following scenario:

where,

p* = pound sterling price of the asset held by the u.s. firm

p = dollar price of the same asset

which of the following conclusions are correct?

a.most of the volatility of the dollar value of the british asset can be removed by

hedging exchange risk because b2[var(s)] and var(e) are 1,125,000 ($)2 and 2,500 ($)2

respectively

b.most of the volatility of the dollar value of the british asset cannot be removed by

hedging exchange risk because b2[var(s)] and var(e) are 236,717 ($)2 and 493,751 ($)2

respectively

c.most of the volatility of the dollar value of the british asset cannot be removed by

hedging exchange risk because b2[var(s)] and var(e) are 125,000 ($)2 and -127,500

($)2 respectively

d.most of the volatility of the dollar value of the british asset can be removed by

hedging exchange risk because b2[var(s)] and var(e) are 125,000 ($)2 and -127,500

($)2 respectively

7) u.s.-based mutual funds known as country funds.

a.invest in the government securities of different sovereign governments, giving

risk-free portfolios effective exchange rate diversification

b.invests exclusively in stocks of a single country

c.invests exclusively in government securities of a single country

d.none of the above

8) consider the position of a treasurer of a mnc, who has $20,000,000 that his firm will

not need for the next 90 days.

a.he could borrow the $20,000,000 in the money market

b.he could take a long position in the eurodollar futures contract

c.he could take a short position in the eurodollar futures contract

d.none of the above

9) suppose you observe the following exchange rates: 1 = $1.60; £1 = $2.00. calculate

the euro-pound exchange rate.

a.1.3333 = £1.00

b.£1.3333 = 1.00

c.3.00 = £1

d.1.25 = £1.00

10) in the problem just previous, company x

a.is probably british

b.is probably american

c.has a comparative advantage in borrowing pounds

d.both a and c

11) find the present value of a 30-year bond that pays an annual coupon, has a coupon

rate of 6%, a yield to maturity of 5%, a par value of 1,000 when the yield to maturity is

5%.

a.1,018.81

b.1,027.23

c.1,153.73

d.none of the above

12) the withholding tax on bond income was originally called the interest equalization

tax.

a.you can thank john f. kennedy for imposing this tax

b.you can thank ronald reagan for imposing this tax

c.you can thank jimmy carter for imposing this tax

d.you can thank george washington for imposing this tax

13) under the bretton woods system

a.there was an explicit set of rules about the conduct of international monetary policies

b.each country was responsible for maintaining its exchange rate within 1 percent of the

adopted par value by buying or selling foreign exchanges as necessary

c.the u.s. dollar was the only currency that was fully convertible to gold

d.all of the above

14) if the domestic currency is strong or expected to become strong,

a.a firm can choose to locate production facilities in a foreign country where costs are

low due to either the undervalued currency or underpriced factors of production

b.a firm should curtail r&d efforts until the exchange rate situation improves

c.a firm should abandon international sales and focus on domestic market share

d.the firm should focus on profiting in the currency futures market based on its

forecasts

15) today is january 1, 2009. the state of iowa has offered your firm a subsidized loan. it

will be in the amount of $10,000,000 at an interest rate of 5% and have annual

(amortizing) payments over 3 years. the first payment is due today and your taxes are

due january 1 of each year on the previous year’s income. the yield to maturity on your

firm’s existing debt is 8%. what is the apv of this subsidized loan?

notethatididnotroundmyintermediatesteps.ifyoudid,youranswermaybeoffbyabit.selectthe

answerclosesttoyours.

a.$406,023.10

b.$840,797

c.$64,157.38

d.$20,659.77

e.none of the other answers are within $100 of my answer

16) an american hedge fund is considering a one-year investment in an italian

government bond with a one-year maturity and a euro-denominated rate of return of i =

5%. the bond costs 1,000 today and will return 1,050 at the end of one year without

risk. the current exchange rate is 1.00 = $1.50. u.s. dollar-denominated government

bonds currently have a yield to maturity of 4%. suppose that the european central bank

is considering either tightening or loosening its monetary policy. it is widely believed

that in one year there are only two possibilities:

following revaluation, the exchange rate is expected to remain steady for at least

another year

find the irr in dollars for the american firm if they wait one year to buy the bond after

the exchange rate rises to s1($|) = $1.80 per . assume that i doesn’t change.