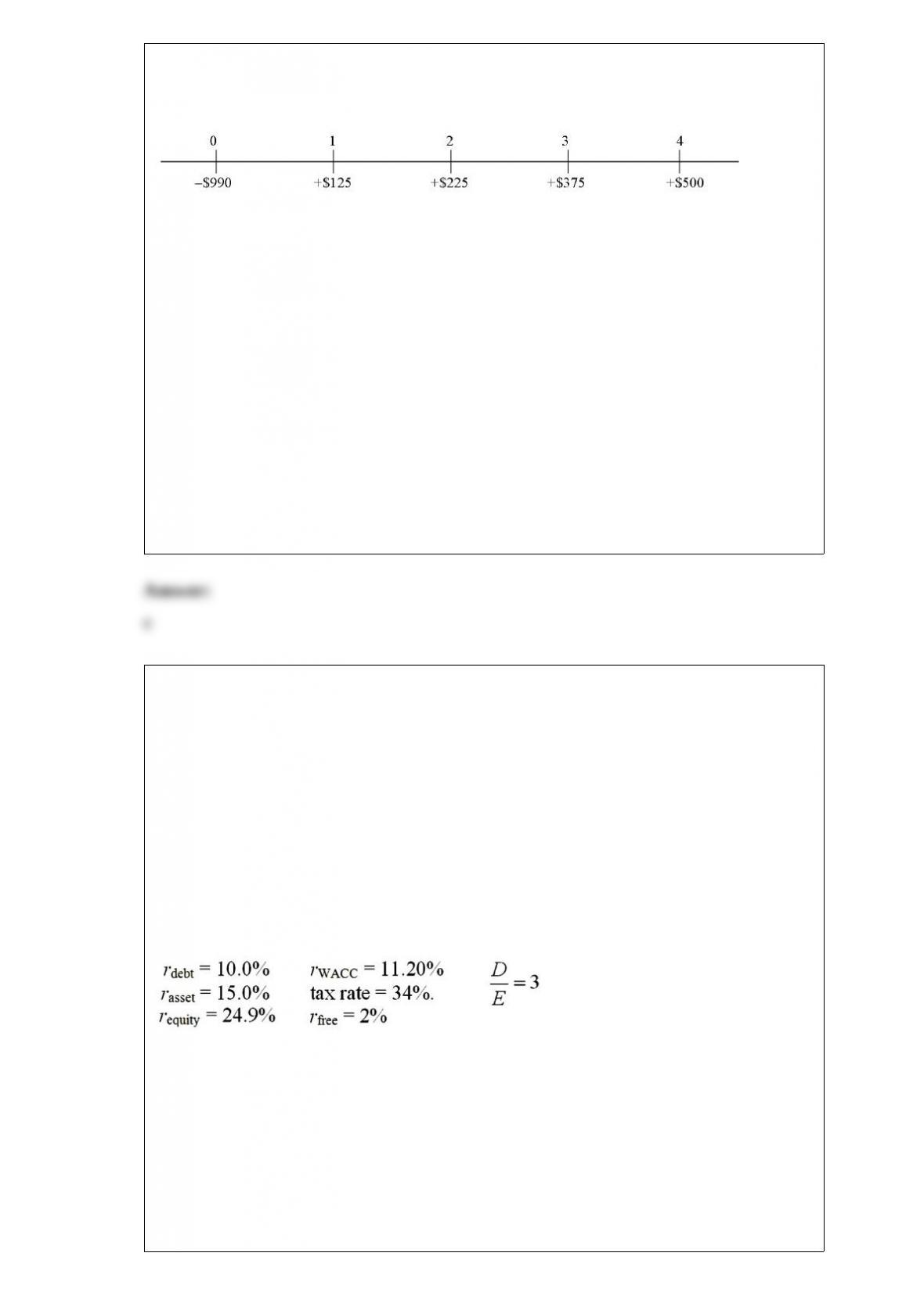

1) consider a project of the cornell haul moving company, the timing and size of the

incremental after-tax cash flows (for an all-equity firm) are shown below in millions:

the firm’s tax rate is 34%; the firm’s bonds trade with a yield to maturity of 8%; the

current and target debt-equity ratio is 3; if the firm were financed entirely with equity,

the required return would be 10%

using the flow to equity methodology, what is the value of the equity claim?

a.-$1,540,000

b.$446,570,866.00

c.$36,580,767.55

d.$470,953,393.70

e.$30,716,236.13

2) tiger towers, inc. is considering an expansion of their existing business, student

apartments. the new project will be built on some vacant land that the firm has just

contracted to buy. the land cost $1,000,000 and the payment is due today. construction

of a 20-unit office building will cost $3 million; this expense will be depreciated

straight-line over 30 years to zero salvage value; the pretax value of the land and

building in year 30 will be $18,000,000. the $3,000,000 construction cost is to be paid

today. the project will not change the risk level of the firm. the firm will lease 20 offices

suites at $20,000 per suite per year; payment is due at the start of the year; occupancy

will begin in one year. variable cost is $3,500 per suite. fixed costs, excluding

depreciation, are $75,000 per year. the project will require a $10,000 investment in net

working capital.

what is the unlevered after-tax incremental cash flow for year 2?

a.-$4,610

b.$102,300

c.$202,300

d.$255,000

e.none of the above

3) assume that you have invested $100,000 in japanese equities. when purchased the

stock’s price and the exchange rate were ¥100 and ¥100/$1.00 respectively. at selling

time, one year after purchase, they were ¥110 and ¥110/$1.00. if the investor had sold

¥10,000,000 forward at the forward exchange rate of ¥105/$1.00 the dollar rate of

return would be:

a.-27.27%

b.4.32%

c.28.00%

d.-9.09%

4) a value-maximizing firm’s would

a.undertake an investment project as long as the irr exceeds the npv

b.undertake an investment project as long as the irr is less than the cost of capital

c.undertake an investment project as long as the irr exceeds the cost of capital

d.none of the above

5) the required return on equity for an all-equity firm is 10.0%. they are considering a

change in capital structure to a debt-to-equity ratio of the tax rate is 40%, the pre-tax

cost of debt is 8%. find the new cost of capital if this firm changes capital structure.

a.14.93%

b.8.67%

c.7.40%

d.none of the above

6) with regard to research on the stock price reaction to mandated accounting changes

such as fasb 52

a.the results suggest that market participants seem to think that changes in reported

earnings do not change the actual cash flows in multinational firms

b.the results suggest that market agents react to “cosmetic” earning changes

c.the results suggest that market agents do not react to cosmetic earning changes that do

not affect value

d.none of the above

7) the current exchange rate is 1.25 = £1.00 and a british firm offers a french customer

the choice of paying a £10,000 bill due in 90 days with either £10,000 or 12,500.

a.the seller has given the buyer an at-the-money put option

b.the seller has given the buyer an at-the-money call option

c.both a and b are correct

d.none of the above

8) assume the time from acceptance to maturity on a $10,000,000 banker’s acceptance is

90 days. further assume that the importing bank’s acceptance commission is 1 percent

and that the market rate for 90-day b/as is 3.0 percent. calculate the amount the exporter

will receive if he discounts the b/a with the importer’s bank.

a.$9,993,750

b.$9,900,000

c.$9,975,000

d.$9,009,375

9) the current exchange rate is £1.00 = $2.00. compute the correct balances in bank a’s

correspondent account(s) with bank b if a currency trader employed at bank a buys

£45,000 from a currency trader at bank b for $90,000 using its correspondent

relationship with bank b.

a.bank a’s dollar-denominated account at b will fall by $90,000

b.bank b’s dollar-denominated account at a will rise by $90,000

c.bank a’s pound-denominated account at b will rise by £45,000

d.bank b’s pound-denominated account at a will fall by £45,000

e.all of the above are correct

10) a u.s.-based mnc with exposure to the swedish krona could best cross-hedge with

a.forward contracts on the euro

b.forward contracts on the ruble

c.forward contracts on the pound

d.forward contracts on the yen