1) when the market breaks through the moving average line from below, a technical

analyst would probably suggest that it is a good time to ___________.

a.buy the stock

b.hold the stock

c.sell the stock

d.short the stock

2) the exchange of one bond for a bond that has similar attributes but is more

attractively priced is called ______________.

a.a substitution swap

b.an intermarket spread swap

c.a rate anticipation swap

d.a pure yield pickup swap

3) members of the board of governors of the federal reserve system are appointed by

____________ to serve _____________ terms.

a.the senate; 10-year

b.the house of representatives; 8-year

c.the president; 14-year

d.the secretary of the treasury; 6-year

4) the risk that can be diversified away is __________.

a.beta

b.firm-specific risk

c.market risk

d.systematic risk

5) ______ option can only be exercised on the expiration date.

a.a mexican

b.an asian

c.an american

d.a european

6) in his 1970 study, malkiel found that mutual funds that do well in one period have an

approximately ________ chance of doing well in the subsequent-year period.

a.33%

b.52%

c.65%

d.85%

7) a 20-year maturity corporate bond has a 6.5% coupon rate (the coupons are paid

annually). the bond currently sells for $925.50. a bond market analyst forecasts that in 5

years yields on such bonds will be at 7%. you believe that you will be able to reinvest

the coupons earned over the next 5 years at a 6% rate of return. what is your expected

annual compound rate of return if you plan on selling the bond in 5 years?

a.7.37%

b.7.56%

c.8.12%

d.8.54%

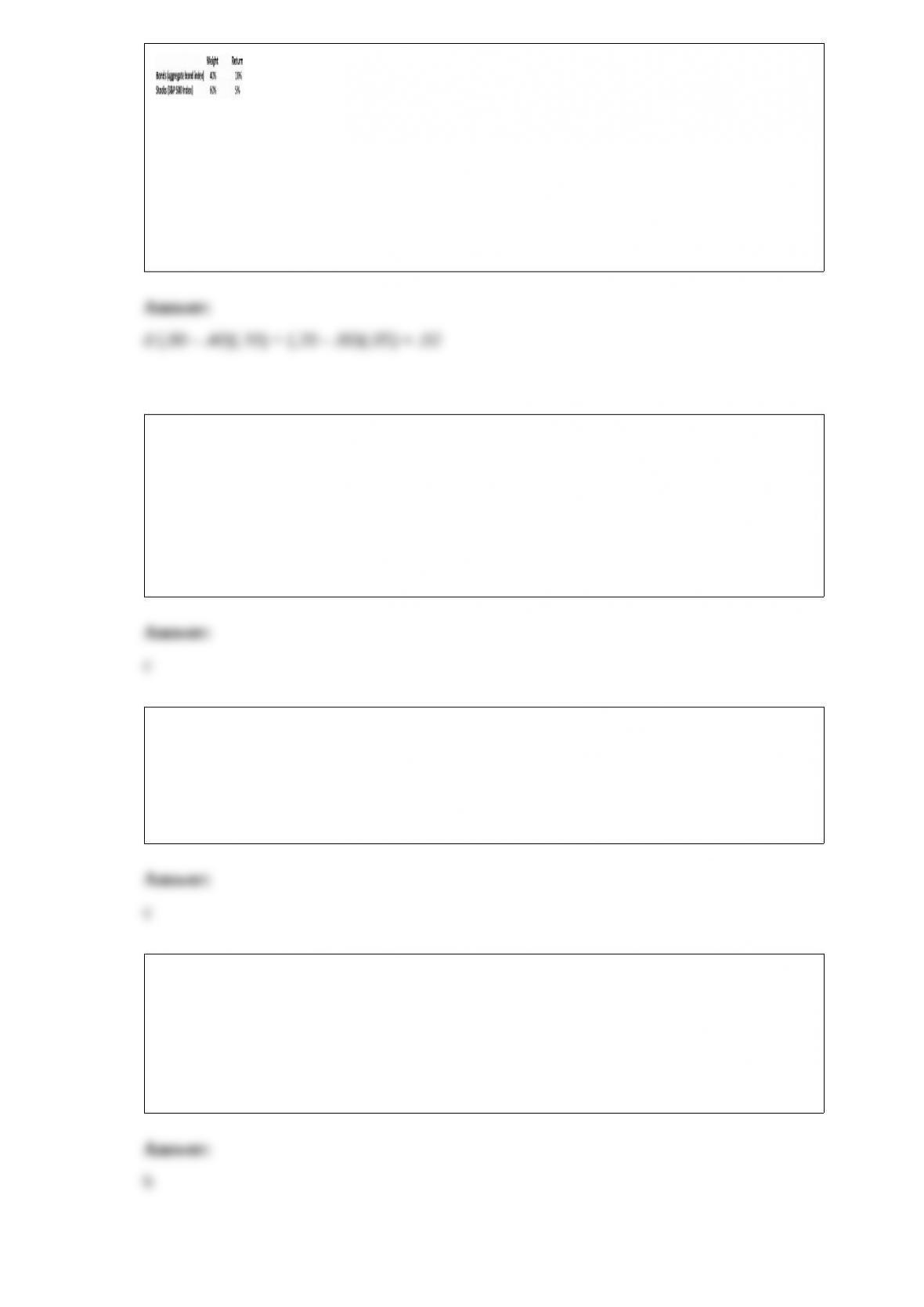

8) in a particular year, lost hope mutual fund made the following investments in asset

classes:

the return on a bogey portfolio was 12%, based on the following:

the contribution of asset allocation across markets to the total extra return was

__________.

a.-1%

b.0%

c.1%

d.2%

9) which of the following would violate the efficient market hypothesis?

a.intel has consistently generated large profits for years.

b.prices for stocks before stock splits show, on average, consistently positive abnormal

returns.

c.investors earn abnormal returns months after a firm announces surprise earnings.

d.high-earnings growth stocks fail to generate higher returns for investors than do low

earnings growth stocks.

10) _____ is considered to be an emerging market country.

a.france

b.norway

c.brazil

d.canada

11) which of the following is not an issue that is central to the debate regarding market

efficiency?

a.the magnitude issue

b.the tax-loss selling issue

c.the lucky event issue

d.the selection bias issue

12) a stock priced at $65 has a standard deviation of 30%. three-month calls and puts

with an exercise price of $60 are available. the calls have a premium of $7.27, and the

puts cost $1.10. the risk-free rate is 5%. since the theoretical value of the put is $1.525,

you believe the puts are undervalued.

if you want to construct a riskless arbitrage to exploit the mispriced puts, you should

____________.

a.buy the call and sell the put

b.write the call and buy the put

c.write the call and buy the put and buy the stock and borrow the present value of the

exercise price

d.buy the call and buy the put and short the stock and lend the present value of the

exercise price

13) which of the following is not a characteristic of a money market instrument?

a.liquidity

b.marketability

c.low risk

d.maturity greater than 1 year

14) if an asset price declines, the investor with a _______ is exposed to the largest

potential loss.

a.long call option

b.long put option

c.long futures contract

d.short futures contract

15) a “bet” option is also called a ____ option.

a.barrier

b.lookback

c.digital

d.foreign exchange

16) according to a model that was estimated using monthly excess returns from january

2005 through november 2011, average returns of equity hedge funds are __________

the s&p 500 index.

a.equal to

b.considerably higher than

c.slightly lower than

d.slightly higher than

17) a restriction under which investors cannot withdraw their funds for as long as

several months or years is called __________.

a.transparency

b.a lock-up period

c.a back-end load

d.convertible arbitrage

18) the standard deviation of return on investment a is .10, while the standard deviation

of return on investment b is .05. if the covariance of returns on a and b is .0030, the

correlation coefficient between the returns on a and b is _________.

a..12

b..36

c..60

d..77

19) a bond with a 9-year duration is worth $1,080, and its yield to maturity is 8%. if the

yield to maturity falls to 7.84%, you would predict that the new value of the bond will

be approximately _________.

a.$1,035

b.$1,036

c.$1,094

d.$1,124

20) the percentage change in the call option price divided by the percentage change in

the stock price is the __________ of the option.

a.delta

b.elasticity

c.gamma

d.theta