Financial institutions are subject to economies of scale in the collection of information.

Answer:

International expansion by a commercial bank should provide increased access to

funding sources.

Answer:

Merger premiums tend to be higher for target banks in competitive environments, but

for which the target bank’s loan portfolios are of high quality.

Answer:

The Economist Intelligence Unit is a rating of sovereign risk based on economic and

political risk within a country.

Answer:

The immunization of a portfolio against interest rate risk means that the portfolio will

neither gain nor lose value when interest rates change.

Answer:

One reason for the recent decline in the expense ratio for PC insurers is an increase

dependence on independent brokers to sell and distribute insurance policies.

Answer:

The 1993 Depositor Protection legislation gives equal claim to the value of liquidated

assets less the amount of insured deposits to foreign uninsured depositors, domestic

uninsured depositors, and the FDIC.

Answer:

During 2012, the top four banks that operate in foreign currency trading comprised

almost half of the market.

Answer:

The spot foreign exchange market is where forward and futures contracts and swap

agreements are transacted.

Answer:

The Financial Services Modernization Act repealed the Glass-Steagall barriers between

commercial banking and investment banking.

Answer:

Economies of scope opportunities seem to be available in the financial services

industry, but economies of scale opportunities do not seem to exist.

Answer:

Basel III capital ratios were enacted due to Basel II weaknesses exposed during the

financial crisis of 2008-20009.

Answer:

Large money center banks finance most of their activities by using retail consumer

deposits as the primary source of funds.

Answer:

Immunizing the balance sheet against interest rate risk means that gains (losses) from

an off-balance-sheet hedge will exactly offset losses (gains) from the balance sheet

position.

Answer:

During the 1980s, a high proportion of brokered deposits at a DI became an early

warning signal of its risk for failure.

Answer:

If ACX + Y < ACX + ACY, where AC is average production cost and X and Y are

products, economies of scope are present.

Answer:

One of the overall objectives in using subordinated debt in addition to common stock

for a DI’s capital base is to improve market discipline of a DI’s risk structure.

Answer:

FDICIA imposed additional regulatory discipline as a substitute for increased

stockholder and depositor discipline.

Answer:

Deep discount bonds are semi-annual fixed-rate coupon bonds that sell at a market price

that is less than par value.

Answer:

In most countries FIs report their balance sheet using market value accounting.

Answer:

The buyer of a loan participation bears double monitoring costs.

Answer:

For a given maturity fixed-income asset, duration increases as the promised interest

payment declines.

Answer:

By decreasing the use of the discount window as a source of funding for a DI, the

Federal Reserve hopes to reduce volatility in the fed funds market.

Answer:

Credit scoring models are advantageous because of their ability to sort borrowers into

different default risk classes.

Answer:

Mutual fund supermarkets often allow investors to purchase funds within large number

of fund companies with no transaction fees.

Answer:

Which of the following observations is NOT TRUE of a liquid asset?A. It can be

turned into cash quickly.

B. Conversion to cash entails low transaction costs.

C. Conversion to cash happens with little or no loss in principal value.

D. It is traded in an active market.

E. Large transactions may move its market price substantially.

Answer:

The barriers among nonbank financial service firms and commercial firms are generally

much stronger than the barriers separating banking and commercial sector activities.

Answer:

Under Basel II (2006), total capital is equal to Tier I capital plus Tier II capital.

Answer:

As of the first half of 2009, income generated by securities brokerage accounted for

over 65% of commercial bank holding company fee income.

Answer:

The ability of diversification to eliminate much of the risk from the asset side of the

balance sheet of an FI is the result of choosing assets that are less than perfectly

positively correlated.

Answer:

The number of savings associations has been declining since

Answer:

Which of the following observations is NOT TRUE of a letter of credit?A. It is a credit

guarantee.

B. It is issued by an FI.

C. It is issued for a fee.

D. Payment on the letter is contingent on some future event occurring.

E. It appears on the FI’s current balance sheet.

Answer:

Junk bonds are bonds that are rated less than investment grade by bond-rating agencies.

Answer:

Derivative contracts allow an FI to manage interest rate and foreign exchange risk.

Answer:

The Expected Shortfall (ES) is a measure of market risk that estimates the expected

losses beyond a given confidence level.

Answer:

An increase in the cost of the joint production of services as compared to the production

of those services independently is an example of diseconomies of scale.

Answer:

Recent evidence suggests that economies of scale may exist for banks up to the $10

billion to $25 billion range.

Answer:

Most of the change in the number of commercial banks since 1990 has been due to

bank failures.

Answer:

Liquidity planning primarily is designed to assist management in dealing with relatively

predictable events.

Answer:

Although growing, the notional value of bank OBS activities remained less than the

value of on-balance-sheet activities at the end of 2012.

Answer:

If an option’s price increases 1.4 percent for every 2 percent change in the price of the

underlying security, what is the value of the option’s delta? A. 0.60.

B. 1.40.

C. 0.70.

D. 2.00.

E. 3.00.

Answer:

Subordinate debt (SD) has been proposed as a means of increasing the degree of overall

market discipline at a depository institution. Which of the following objectives is

considered to be achievable when attempting to increase market discipline?A. Issuing

SD might increase the size of the DI’s capital cushion.

B. The expected cost of issuing SD should decrease as the risk of the DI increased.

C. Mandatory SD would reduce transparency at DIs.

D. SD would further emphasize the use of capital forbearance.

E. Secondary market yields on the SD would be inversely related to an increase in the

risk of the DI.

Answer:

Swaps create value ifA. relative prices differ across markets.

B. there are barriers to entry in some markets.

C. information is costly.

D. All of the above.

E. None of the above.

Answer:

Matching the foreign currency book of assets and liability maturity does not protect the

FI from A. sovereign country risk.

B. interest rate risk.

C. liquidity risk.

D. foreign exchange risk.

E. off-balance-sheet risk.

Answer:

Which of the following has NOT been a factor deterring U.S. bank expansion abroad?

A. The implementation of risk-based capital requirements effective in 1993.

B. The increased competition from the large Japanese banks through the mid-1990s.

C. The effects of the collapse of the financial markets in several emerging markets.

D. The ability of the U.S. banks to achieve large excess capital positions in the second

half of the 1990s.

E. The passage of the European Community Second Banking Derivative.

Answer:

A bank has an average balance of transactions accounts, August 10 to 23, of $824.46

million. The average balance in the cash account is $42.014 million over this period.

The bank is carrying forward a deficit of $1.276 million from the last reserve period.

The rules require no reserves to be maintained for the first $8.5 million, 3 percent for

amounts between $8.5 million and $45.8 million, and 10 percent thereafter.

What is the gross reserve requirement? A. $74.653 million.

B. $78.985 million.

C. $76.747 million.

D. $72.461 million.

E. $77.866 million.

Answer:

According to economists, this is the main reason for underpricing of new issues. A.

Lack of competition among existing investment banks.

B. Entry of banks into the investment banking sector.

C. Monopoly power of the existing investment banks.

D. Mismatch of demand and supply of securities.

E. Risk premium for information advantage possessed by issuers.

Answer:

Identify the fundamental regulatory philosophy underlying the International Banking

Act. A. Too big to fail.

B. National treatment.

C. Reciprocal arrangement.

D. X efficiencies.

E. Unit banks.

Answer:

The maximum cost savings that can be generated with this new equipment has been

estimated to be $264,237. In order to accept this project, what is the minimum number

of years the projected savings must be realized before the project breaks even?A. 3.7

years.

B. 4.7 years.

C. 5.7 years.

D. 6.7 years.

E. 7.7 years.

Answer:

Annuities offered by life insurance companies are a financial contract that A. is used to

build up a fund.

B. pays only fixed returns to groups of employees.

C. is used to liquidate a fund.

D. pays only variable returns to individuals.

E. None of the above are correct.

Answer:

The largest asset category of mutual funds as of 2012 was A. corporate equities.

B. credit market instruments.

C. U.S. government securities.

D. corporate and foreign bonds.

E. municipal securities.

Answer:

The duration of a consol bond is A. less than its maturity.

B. infinity.

C. 30 years.

D. more than its maturity.

E. given by the formula D = 1/(1-R).

Answer:

A finance company may be classified as a subprime lender if it A. charges interest rates

below those charged by commercial banks.

B. lends to low-risk customers.

C. lends to high-risk customers.

D. originated from check cashing outlets in the early 1990s.

E. is wholly owned by a parent corporation.

Answer:

A positive gap implies that an increase in interest rates will cause _______ in net

interest income. A. no change

B. a decrease

C. an increase

D. an unpredictable change

E. Either A or B.

Answer:

What was the primary objective of the Bank Holding Company Act of 1956? A.

Permitted bank holding companies to acquire banks in other states.

B. Restricted the banking and nonbanking acquisition activities of multibank holding

companies.

C. Regulated foreign bank branches and agencies in the United States.

D. Bank holding companies were permitted to convert out-of-state subsidiary banks

into branches of a single interstate bank.

E. Allowed for the creation of a financial services holding company.

Answer:

Back-end fees on loan commitments are charged as a certain percentage ofA.

commitment size.

B. loan taken down.

C. utilized portion of commitment size.

D. unused portion of commitment size.

E. interest payable on the loan commitment.

Answer:

What is the purpose of a credit forward agreement? A. To allow property-casualty

insurers to hedge the extreme losses that occur after major catastrophes.

B. To adjust prices on outstanding futures each day to reflect current futures market

conditions.

C. To facilitate the future exchange of an asset for cash at a price that is determined

daily.

D. To hedge a cash asset on a direct dollar-for-dollar basis with a forward or futures

contract.

E. To hedge against an increase in the default risk of a loan.

Answer:

Concern about the cost of managing a widely diversified financial company has been

used to justify product segmentation on the grounds of A. safety and soundness issues.

B. economy of scale and scope issues.

C. conflict of interest issues.

D. deposit insurance issues.

E. regulatory oversight issues.

Answer:

Finance companies that prey on desperate higher-risk customers charging unfairly

exorbitant interest rates are referred to as A. refinancing companies.

B. captive companies.

C. business credit companies.

D. loan shark companies.

E. personal credit companies.

Answer:

Deposit insurance contracts can be structured to reduce moral hazard behavior by A.

increasing depositor discipline.

B. increasing stockholder discipline.

C. increasing regulator discipline.

D. reducing owner incentives to take risks.

E. All of the above.

Answer:

If T-bond futures prices decrease to 81-27/32nds, what is the value of the futures hedge

position? A. $81,270,000.

B. $24,553,125.

C. $26,700,000.

D. $812,700.

E. $28,387,500.

Answer:

A U.S. FI wishes to hedge a €10,000,000 loan using euro currency futures. Each euro

futures contract is for 125,000 euros, and the hedge ratio is 1.40. The loan is payable in

one year in euros.

What type of currency hedge is necessary to protect the FI from exchange rate risk? A.

Buy € currency futures.

B. Sell € currency futures.

C. Finance the loan with € deposits.

D. Finance the loan with Eurodollar deposits.

E. Either B or D.

Answer:

On December 31, 2001 Historic Bank had long positions of 200,000,000 Japanese Yen

and 50,000,000 Swiss Francs. The closing exchange rates were ¥92/$ and Swf1.89/$.

What were the respective positions of the two currencies in dollars? A. $2,173,913 and

$94,500,000.

B. $18,400,000,000 and $26,455,026.

C. $2,173,913 and $26,455,026.

D. $18,400,000,000 and $94,500,000.

E. None of the above.

Answer:

Which of the following FX trading activities is used to hedge FX risk? A. The purchase

and sale of foreign currencies for the purpose of profiting from forecasting or

anticipating future movements in FX rates.

B. The purchase and sale of foreign currencies to allow customers to partake in and

complete international commercial trade transactions.

C. The purchase and sale of foreign currencies for the purpose of offsetting customer

exposure in any given currency.

D. The purchase and sale of foreign currencies to allow customers to take positions in

foreign real and financial investments.

E. None of the above.

Answer:

One hundred identical mortgages are pooled together into a pass-through security. Each

mortgage has a $150,000 principal, a fixed annual interest rate of 8 percent (paid

monthly), and is fully amortized over a term of 30 years.

What is the present value of the mortgage pass-through if the entire pool is repaid after

two months and there is no change in interest rates? A. $14,989,935.

B. $15,089,868.

C. $15,000,000.

D. $15,110,065.

E. $14,889,935.

Answer:

Assume that the thrift variable-rate liabilities are CDs indexed to some domestic rate.

Which of the following statements describes the hedge characteristics of the above

example?A. The thrift is exposed to basis risk because the CD rates may not be

perfectly correlated with the LIBOR rates.

B. Only the bank is fully hedged.

C. The thrift is exposed to basis risk if the credit/default risk premium on the thrift’s

CDs increases over time.

D. All of the above.

E. Answers A and C only.

Answer:

An investment banker agrees to underwrite an issue of 10 million shares of stock for

TWResearch, Inc. on a firm commitment basis. The investment banker pays $10.50 per

share to TWResearch, Inc. for the 10 million shares of stock. It then sells those shares

to the public for $11.20 per share.

What is the profit (loss) to the investment banker? A. Profit of $1,000,000.

B. Profit of $2,000,000.

C. Profit of $7,000,000.

D. Loss of $7,500,000.

E. Loss of $1,000,000.

Answer:

The NAV of a closed-end investment company shares is determined at any point in time

by A. the number of shares available.

B. the value of the underlying shares owned by the company.

C. the demand for the investment company’s shares.

D. Answers A and B only.

E. Answers B and C only.

Answer:

What will be the net after-swap cost of funds for the bank if the cash market liabilities

are included in the analysis? A. Variable-rate at LIBOR.

B. Fixed-rate at 8 percent.

C. Fixed-rate at 1 percent.

D. Fixed-rate at 2 percent.

E. None of the above.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation permits bank holding companies to acquire banks in other states.

Answer:

The FASB set its guidelines to allow for the valuation of assets to be based on A. prices

at the discretion of the DI’s management.

B. book values rather than market values.

C. market values that existed when the assets were last marked to market.

D. prices that would be received as part of a forced liquidation.

E. prices that would be received in an orderly market.

Answer:

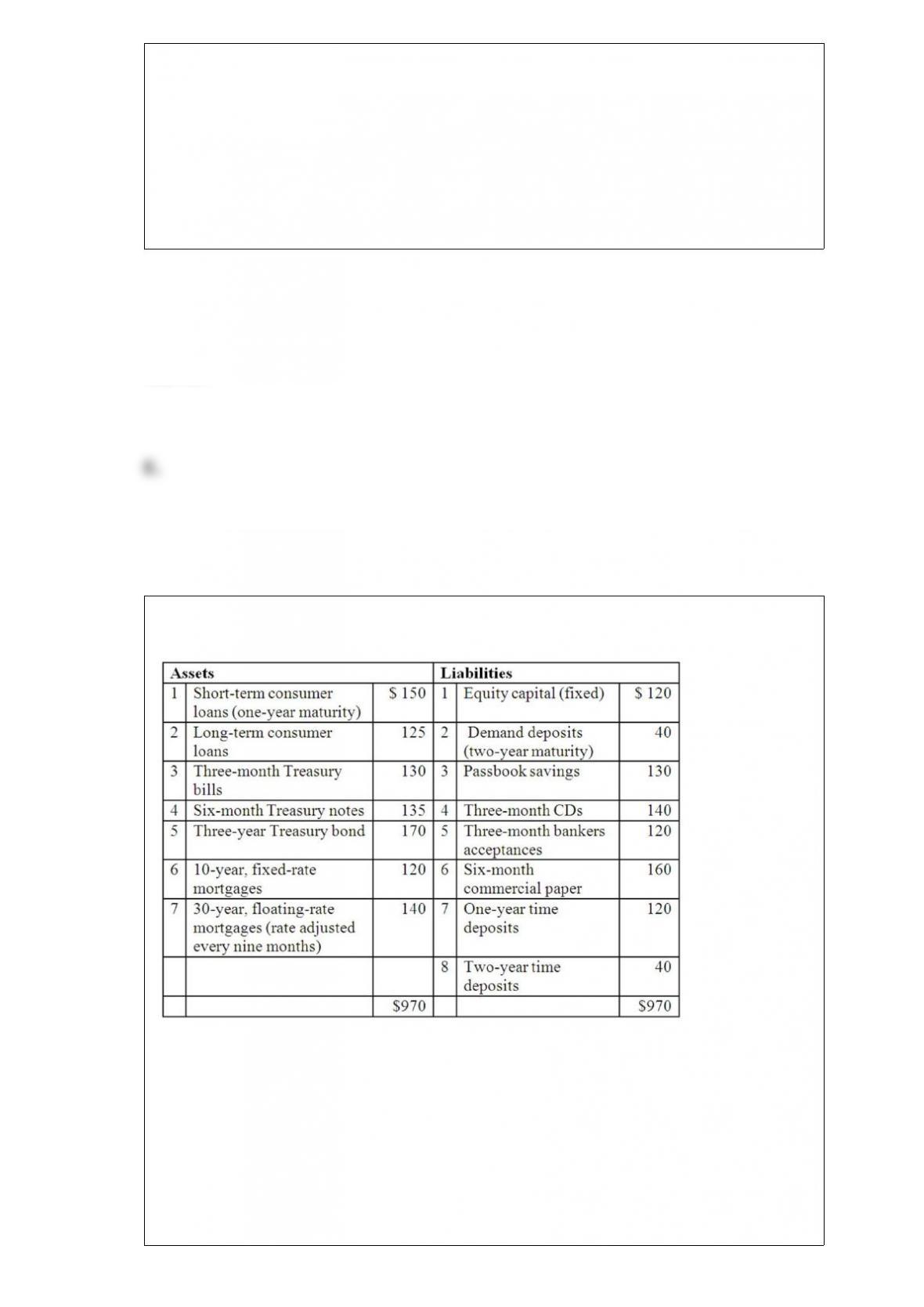

The balance sheet of XYZ Bank appears below. All figures in millions of US Dollars.

Total one-year

rate-sensitive liabilities is A. $540 million.

B. $580 million.

C. $555 million.

D. $415 million.

E. $720 million.

Answer:

The writer of a bond put option A. receives a premium in return for standing ready to

sell the bond at the exercise price.

B. receives a premium in return for standing ready to buy bonds at the exercise price.

C. pays a premium and has the right to sell the underlying bond at the agreed exercise

price.

D. pays a premium and has the right to buy the underlying bond at the agreed exercise

price

E. pays a premium and has the obligation to buy the underlying bond at the agreed

exercise price

Answer: