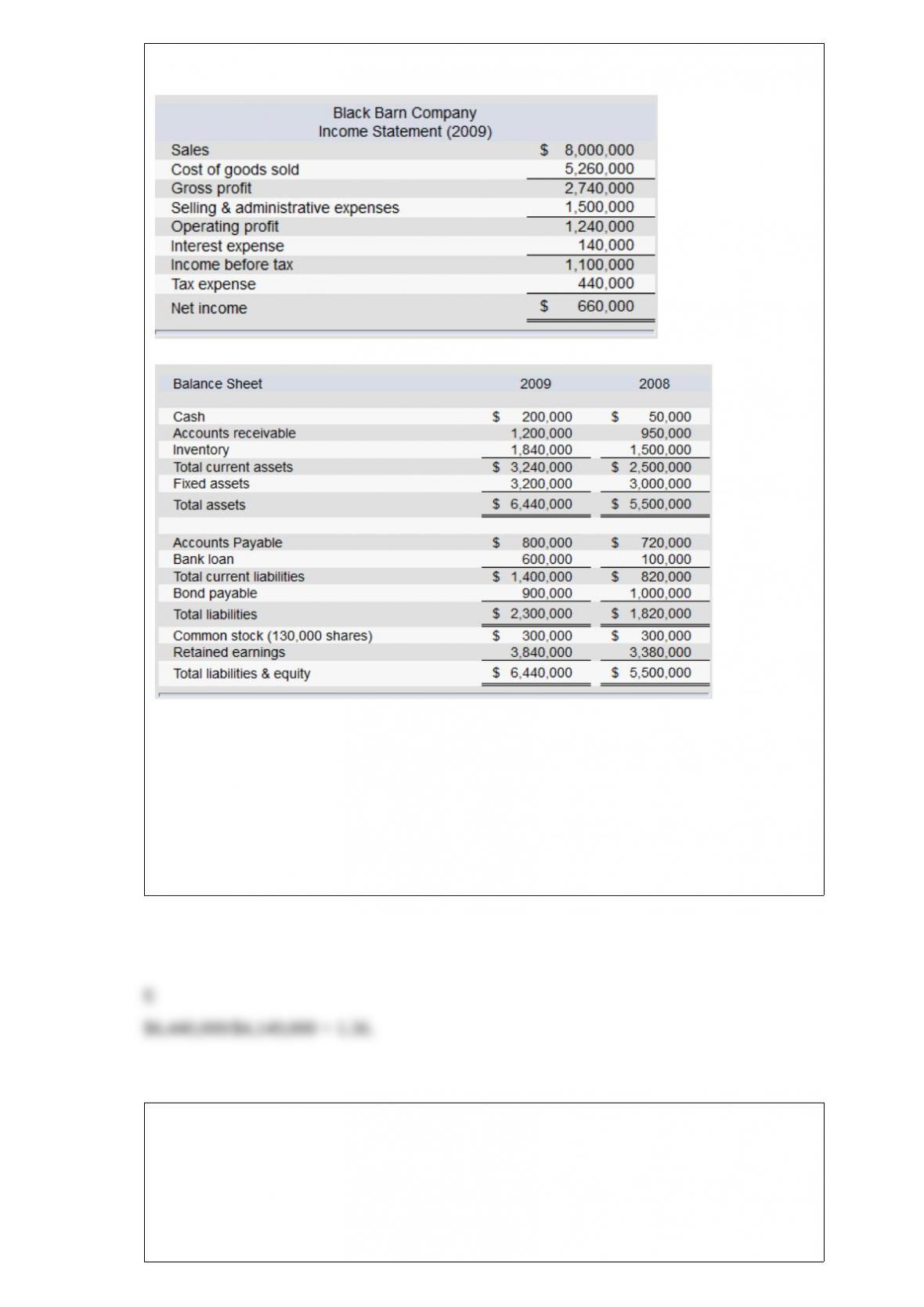

The financial statements of Black Barn Company are given below.

Note: The common shares are trading in the stock market for $40 each.

Refer to the financial statements of Black Barn Company. The firm’s leverage ratio for

2009 is

A. 1.65.

B. 1.89.

C. 2.64.

D. 1.31.

E. 1.56.

Par-value-bond F has a modified duration of 9. Which one of the following statements

regarding the bond is true?

A. If the market yield increases by 1%, the bond’s price will decrease by $90.

B. If the market yield increases by 1%, the bond’s price will increase by $90.

C. If the market yield increases by 1%, the bond’s price will decrease by $60.

D. If the market yield decreases by 1%, the bond’s price will increase by $60.

Par-value-bond GE has a modified duration of 11. Which one of the following

statements regarding the bond is true?

A. If the market yield increases by 1%, the bond’s price will decrease by $55.

B. If the market yield increases by 1%, the bond’s price will increase by $55.

C. If the market yield increases by 1%, the bond’s price will decrease by $110.

D. If the market yield increases by 1%, the bond’s price will increase by $110.

The risk that cannot be diversified away is

A. firm-specific risk.

B. unique.

C. nonsystematic risk.

D. market risk.

According to the Capital Asset Pricing Model (CAPM), a security with a

A. positive alpha is considered overpriced.

B. zero alpha is considered to be a good buy.

C. negative alpha is considered to be a good buy.

D. positive alpha is considered to be underpriced.

The security market line (SML)

A. can be portrayed graphically as the expected return-beta relationship.

B. can be portrayed graphically as the expected return-standard deviation of

market-returns relationship.

C. provides a benchmark for evaluation of investment performance.

D. can be portrayed graphically as the expected return-beta relationship and provides a

benchmark for

evaluation of investment performance.

E. can be portrayed graphically as the expected return-standard deviation of

market-returns relationship and

provides a benchmark for evaluation of investment performance.

You sold short 300 shares of common stock at $55 per share. The initial margin is 60%.

At what stock price would you receive a margin call if the maintenance margin is 35%?

A. $51.00

B. $65.19

C. $35.22

D. $40.36

The _______ is defined as the present value of all cash proceeds to the investor in the

stock.

A. dividend-payout ratio

B. intrinsic value

C. market-capitalization rate

D. plowback ratio

Futures contracts __________ traded on an organized exchange, and forward contracts

__________ traded on an organized exchange.

A. are not; are

B. are; are

C. are not; are not

D. are; are not

E. are; may or may not be

The assumptions concerning the shape of utility functions of investors differ between

conventional theory and prospect theory. Conventional theory assumes that utility

functions are __________, whereas prospect theory assumes that utility functions are

__________.

A. concave and defined in terms of wealth; s shaped (convex to losses and concave to

gains) and defined in terms of losses relative to current wealth

B. convex and defined in terms of losses relative to current wealth; s shaped (convex to

losses and concave to gains) and defined in terms of losses relative to current wealth

C. s shaped (convex to losses and concave to gains) and defined in terms of losses

relative to current wealth; concave and defined in terms of wealth

D. s shaped (convex to losses and concave to gains) and defined in terms of wealth;

concave and defined in terms of losses relative to current wealth

E. convex and defined in terms of wealth; concave and defined in terms of gains

relative to current wealth

Suppose you held a well-diversified portfolio with a very large number of securities,

and that the single index model holds. If the σ of your portfolio was 0.18 and σM was

0.24, the β of the portfolio would be approximately

A. 0.75.

B. 0.56.

C. 0.07.

D. 1.03.

Indexing of bond portfolios is difficult because

A. the number of bonds included in the major indexes is so large that it would be

difficult to purchase them in the proper proportions.

B. many bonds are thinly traded, so it is difficult to purchase them at a fair market price.

C. the composition of bond indexes is constantly changing.

D. All of the options are true.

For an individual investor, the value of home ownership is likely to be viewed

A. as a hedge against increases in rental rates.

B. as a guarantee of availability of a particular residence.

C. as a hedge against inflation.

D. as a hedge against increases in rental rates and as a guarantee of availability of a

particular residence.

E. All of the options are correct.

Fundamental analysis uses

A. earnings and dividends prospects.

B. relative strength.

C. price momentum.

D. earnings, dividend prospects, and relative strength.

E. earnings, dividend prospects, and price momentum.

Music Doctors Company has an expected ROE of 14%. The dividend growth rate will

be ________ if the firm follows a policy of paying 60% of earnings in the form of

dividends.

A. 4.8%

B. 5.6%

C. 7.2%

D. 6.0%

The price quotations of Treasury bonds in the Wall Street Journal show an ask price of

104.25 and a bid price of 104.125. As a buyer of the bond, what is the dollar price you

expect to pay?

A. $1,048.00

B. $1,042.50

C. $1,044.00

D. $1,041.25

E. $1,040.40

T-bills are financial instruments initially sold by ________ to raise funds.

A. commercial banks

B. the U.S. government

C. state and local governments

D. agencies of the federal government

E. the U.S. government and agencies of the federal government

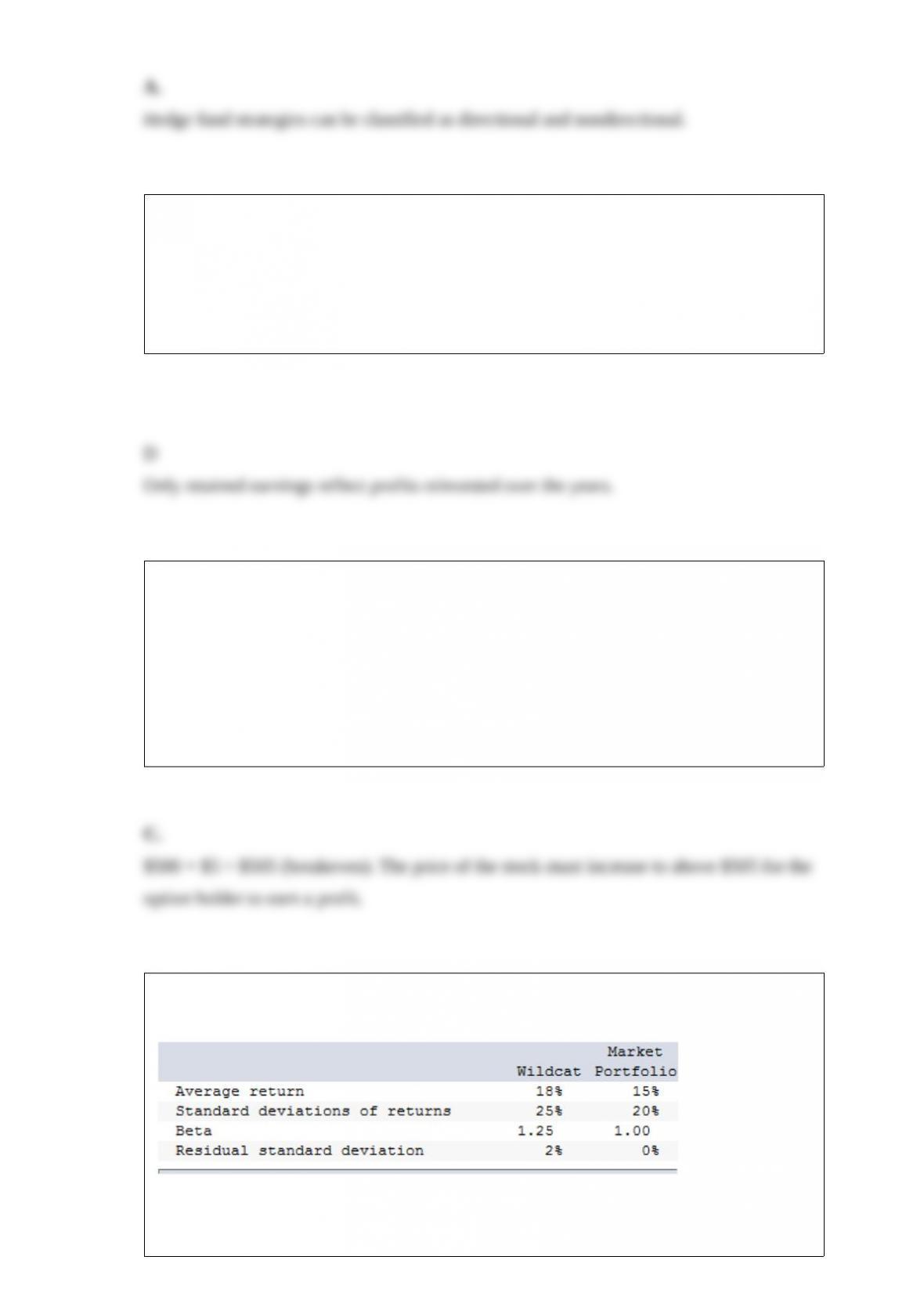

Hedge fund strategies can be classified as

A. directional or nondirectional.

B. stock or bond.

C. arbitrage or speculation.

D. stock or bond and arbitrage or speculation.

E. directional or nondirectional and stock or bond.

Which of the following ratios gives information on the amount of profits reinvested in

the firm over the years?

A. Sales/total assets

B. Debt/total assets

C. Debt/equity

D. Retained earnings/total assets

Suppose the price of a share of Google stock is $500. An April call option on Google

stock has a premium of $5 and an exercise price of $500. Ignoring commissions, the

holder of the call option will earn a profit if the price of the share

A. increases to $504.

B. decreases to $490.

C.increases to $506.

D. decreases to $496.

E. None of the options are correct.

The following data are available relating to the performance of Wildcat Fund and the

market portfolio:

The risk-free return during the sample period was 7%.

Calculate Treynor’s measure of performance for Wildcat Fund.

A. 1.00%

B. 8.80%

C. 44.00%

D. 50.00%

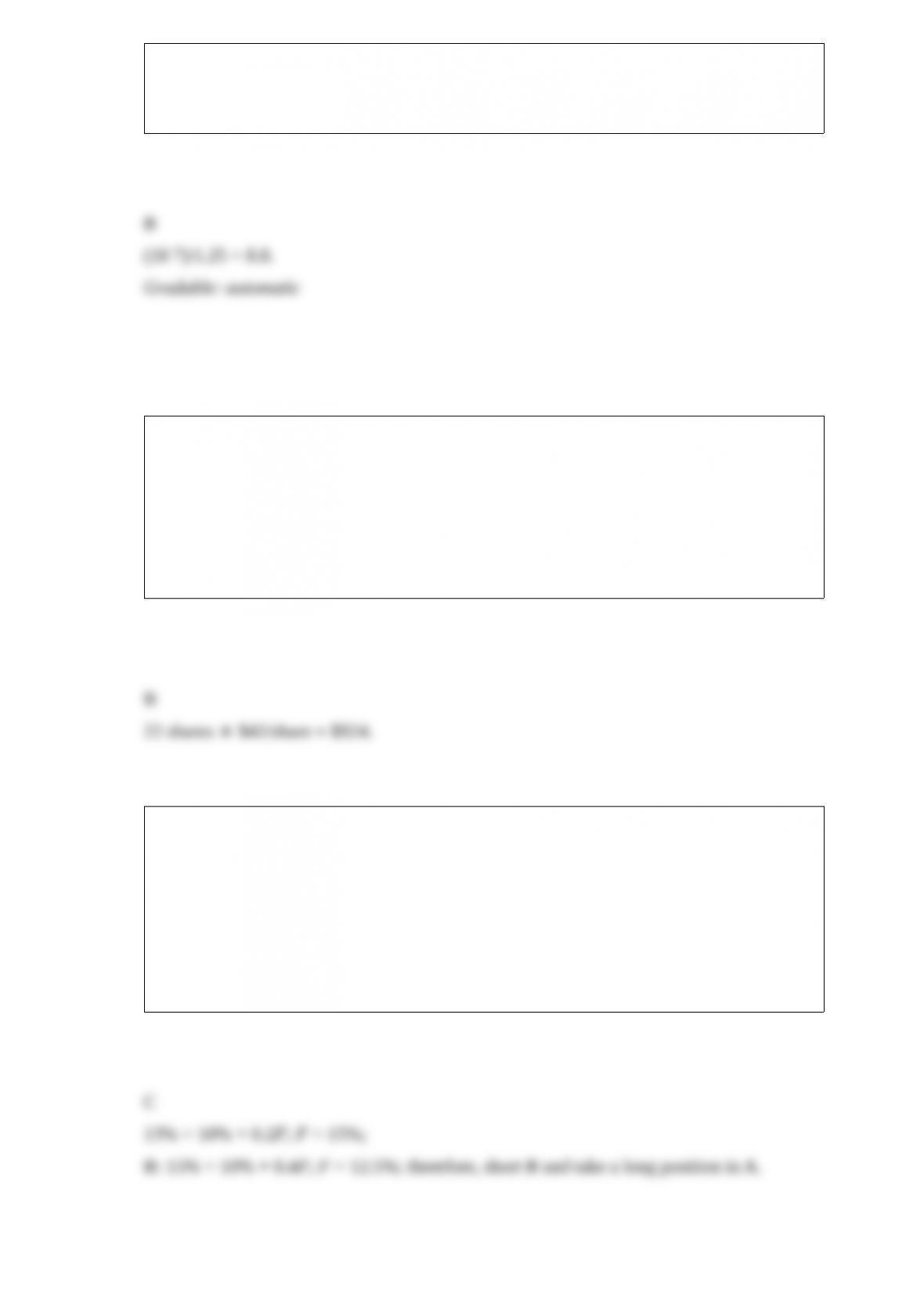

A convertible bond has a par value of $1,000 and a current market price of $975. The

current price of the issuing firm’s stock is $42, and the conversion ratio is 22 shares.

The bond’s market conversion value is

A. $729.

B. $924.

C. $870.

D. $1,000.

Consider the single factor APT. Portfolio A has a beta of 0.2 and an expected return of

13%. Portfolio B has a beta of 0.4 and an expected return of 15%. The risk-free rate of

return is 10%. If you wanted to take advantage of an arbitrage opportunity, you should

take a short position in portfolio _________ and a long position in portfolio _________.

A. A; A

B. A; B

C. B; A

D. B; B

Which of the following factors would not be expected to affect the nominal interest

rate?

A. The supply of loans

B. The demand for loans

C. The coupon rate on previously issued government bonds

D. The expected rate of inflation

E. Government spending and borrowing

Kane, Marcus, and Trippi (1999) show that the annualized fee that investors should be

willing to pay for active

management, over and above the fee charged by a passive index fund, does not depend

on

I) the investor’s coefficient of risk aversion.

II) the value of the at-the-money call option on the market portfolio.

III) the value of the out-of-the-money call option on the market portfolio.

IV) the precision of the security analyst.

V) the distribution of the squared information ratio in the universe of securities.

A. I, II, and IV

B. II, III, and V

C.II and III

D. I, IV, and V

E. II, IV, and V

Cash flow matching on a multiperiod basis is referred to as

A. immunization.

B. contingent immunization.

C. dedication.

D. duration matching.

E. rebalancing.

Which of the following statements about the mutual-fund theorem is true?

I) It is similar to the separation property.

II) It implies that a passive investment strategy can be efficient.

III) It implies that efficient portfolios can be formed only through active strategies.

IV) It means that professional managers have superior security-selection strategies.

A. I and IV

B. I, II, and IV

C. I and II

D. III and IV

E. II and IV

Consider the multifactor model APT with three factors. Portfolio A has a beta of 0.8 on

factor 1, a beta of 1.1 on factor 2, and a beta of 1.25 on factor 3. The risk premiums on

the factor 1, factor 2, and factor 3 are 3%, 5%, and 2%, respectively. The risk-free rate

of return is 3%. The expected return on portfolio A is __________ if no arbitrage

opportunities exist.

A. 13.5%

B. 13.4%

C. 16.5%

D. 23.0%

Before expiration, the time value of an in-the-money put option is always

A. equal to zero.

B. negative.

C. positive.

D. equal to the stock price minus the exercise price.

E. None of the options are correct.

Consider the regression equation:

rirf = g0 + g1bi + g2s2(ei) + eit

where:

rirt = the average difference between the monthly return on stock i and the monthly risk

free rate

bi = the beta of stock i

s2(ei) = a measure of the nonsystematic variance of the stock i

If you estimated this regression equation and the CAPM was valid, you would expect

the estimated coefficient, g2, to be

A. 0.

B. 1.

C. equal to the risk free rate of return.

D. equal to the average difference between the monthly return on the market portfolio

and the monthly risk free rate.

E. None of the options are correct.

Inflation

A. is the rate at which the general level of prices is increasing.

B. rates are high when the economy is considered to be “overheated.”

C. is unrelated to unemployment rates.

D.-is the rate at which the general level of prices is increasing, and rates are high when

the economy is considered to be “overheated.”

E. is the rate at which the general level of prices is increasing and is unrelated to

unemployment rates.

The expected return/beta relationship is not used

A. by regulatory commissions in determining the costs of capital for regulated firms.

B. in court rulings to determine discount rates to evaluate claims of lost future incomes.

C. to advise clients as to the composition of their portfolios.

D. by regulatory commissions in determining the costs of capital for regulated firms

and to advise clients as to the composition of their portfolios.

E. None of the options are correct.

The expected return of a portfolio of risky securities

A. is a weighted average of the securities’ returns.

B. is the sum of the securities’ returns.

C. is the weighted sum of the securities’ variances and covariances.

D. is a weighted average of the securities’ returns and the weighted sum of the

securities’ variances and

covariances.

E. None of the options are correct.