The savings association industry continues to be the primary lender of residential

mortgages.

Answer:

As the economic expansion continued through the 1990s, the demand for finance

company loans increased.

Answer:

Determining risk-adjusted asset values for OBS market contracts requires multiplying

the notional values by the appropriate risk weights.

Answer:

An expected net deposit drain on any given day means that deposit withdrawals are less

than deposit inflows.

Answer:

Market risk management is important as a source of information on risk exposure for

senior management.

Answer:

The greater the Tier I leverage using the Standardized Approach under Basel III, the

more highly leveraged the bank.

Answer:

The market value of capital is equal to market value of assets minus the market value of

liabilities.

Answer:

The Federal safety net to protect the integrity of the payments system consists of

deposit insurance and social welfare.

Answer:

In the use of modern portfolio theory (MPT), the sum of the credit risks of loans under

estimates the risk of the whole portfolio.

Answer:

As of 2012, equity capital in the securities industry measured over 12 percent.

Answer:

Implicit interest involves the process of crediting the interest payment directly to a

deposit account as opposed to sending an explicit interest check to the customer.

Answer:

In order for an investment bank to perform a firm commitment offering of securities,

they must maintain at least 20% equity on their balance sheet.

Answer:

A perfect hedge, or perfect immunization, seldom occurs.

Answer:

From the perspective of the lending FI, the risk of a well-diversified portfolio of loans

should be less than weighted average risk of the individual loans.

Answer:

A major problem in estimating RAROC is the measurement of loan risk.

Answer:

Managing a bank’s reserve position requires knowing only the target reserve ratio and

the period over which reserves must be maintained.

Answer:

The Securities Act of 1933 sets rules and procedures regarding a mutual fund’s

prospectus sent to potential investors.

Answer:

Despite the complexity of measuring the risk of asset-backed securities, credit rating

agencies continued to use their own measures to quantify risks involved.

Answer:

Depository institutions are prohibited from proprietary trading by the Volker Rule.

Answer:

Property insurance involves coverage against the loss of personal property as well as

protection against legal liability claims.

Answer:

By converting to a bank holding company, an investment bank gains access to Federal

Reserve lending facilities.

Answer:

The insured depositor transfer method of least-cost bank failure resolution requires the

FDIC to employ the method that imposes the highest amount of failure costs on

uninsured depositors.

Answer:

Which of the following statements is TRUE?A. An increase in interest rates leads to an

increase in the market value of financial securities.

B. Value of longer term securities decreases at a diminishing rate for increases in

interest rates.

C. Value of longer term securities increases at an increasing rate for any decline in

interest rates.

D. The shorter the maturity of a fixed income asset or liability, the greater the fall in

market value for any given interest rate increase.

E. The longer the maturity of a fixed income asset or liability, the greater the fall in

market value for any given interest rate decrease.

Answer:

The use of the Herfindahl-Hirschman Index (HHI) to measure market concentration is

encouraged for banks because of the ease of separating banks from thrifts and insurance

companies.

Answer:

National full-line investment banks and securities firms provide business services to

both retail and corporate customers.

Answer:

The delta of an option is the sensitivity of an option’s value to a unit change in the value

of the underlying asset.

Answer:

Venture capital firms often make loans to finance new and often high-risk companies

that may have no business history.

Answer:

Interest rate risk stems from the impact of both anticipated and unanticipated changes in

interest rates on FI profitability.

Answer:

FX trading income is derived only from profit (or loss) on the FI’s speculative currency

positions.

Answer:

Of the ten largest financial service firms in the world, none are headquartered in the

U.S.

Answer:

For given changes in interest rates, the change in the market value of net worth of an FI

is equal to the difference between the changes in the market value of the assets and

market value of the liabilities.

Answer:

The debt service ratio of a country should be negatively related to the probability of

rescheduling.

Answer:

Under the lagged reserve accounting system, the A. reserve maintenance period is two

days longer than the reserve computation period.

B. reserve maintenance period starts two days after the start of the reserve computation

period.

C. reserve maintenance period does not begin until seventeen days after the end of the

computation period.

D. reserve computation period starts on the same date as the reserve maintenance

period.

E. reserve computation period is two days longer than the reserve maintenance period.

Answer:

Which of the following refers to restrictions in loan and bond agreements that

encourage or forbid certain actions by the borrower? A. Mortality rates.

B. RAROC.

C. Implicit contracts.

D. Covenants.

E. Credit rationing.

Answer:

Which of the following describes a firm commitment underwriting?A. Finding a large

institutional buyer or investor such as another FI for a private placement.

B. Investment bankers acting as agents on a fee basis related to their success in placing

the issue.

C. Investment bankers act as agents and purchase securities from the issuer at one price

for sale to the public at a different price.

D. Bank using its lending powers to coerce customers to buy the products sold by its

securities affiliate.

E. Purchase of securities from the issuer at one price for resale to the public at a

slightly higher price.

Answer:

A US bank has fixed-rate assets in US dollars and variable-rate liabilities in Euros. This

bank is exposed to A. interest rate increases and an appreciation of the dollar.

B. interest rate declines and an appreciation of the dollar.

C. interest rate increases and a depreciation of the dollar.

D. interest rate declines and a depreciation of the dollar.

E. zero exposure to interest rate and exchange rate exposures.

Answer:

Which of the following is a non-schedule L off-balance-sheet risk? A. Takedown risk.

B. Settlement risk.

C. Aggregate funding risk.

D. When-issued trading.

E. Credit risk with derivative securities.

Answer:

Wholesale certificates of deposit A. are less than $100,000 in denomination.

B. cannot be rolled over prior to maturity.

C. can be resold on the secondary market.

D. are sold only to other financial intermediaries.

E. are covered by Federal deposit insurance.

Answer:

Identify a problem associated with using the Black-Scholes model to value bond

options.A. It assumes short-term interest rates are constant.

B. It assumes that commissions are charged.

C. It assumes fluctuating variance of returns on the underlying asset.

D. It assumes that the variance of bond prices is constant over time.

E. All of the above.

Answer:

The passage of which regulation extended the interstate acquisition powers of banks to

encompass healthy thrifts?A. Bank Holding Company Act.

B. McFadden Act.

C. Garn-St. Germain Act.

D. Financial Institutions Reform, Recovery, and Enforcement Act.

E. Glass-Steagall Act.

Answer:

Which of the following transactions meets the legal definition of a highly leveraged

transaction (HLT)? A. A buyout that increases debt from $100 million to $150 million

resulting in a 25 percent leverage ratio.

B. An investment project that increases debt from $100 million to $250 million

resulting in a 55 percent leverage ratio.

C. An acquisition that increases debt from $100 million to $250 million resulting in a

65 percent leverage ratio.

D. An acquisition that increases debt from $100 million to $150 million resulting in a

70 percent leverage ratio.

E. An investment project that results in an 80 percent leverage ratio.

Answer:

A swap used to hedge against exchange rate risk from mismatched currencies on assets

and liabilities is A. a commodity swap.

B. a credit swap.

C. a currency swap.

D. an equity swap.

E. an interest rate swap.

Answer:

The packaging of loans into asset pools and then selling portions of the pool to

investors is known as A. security creation.

B. securitization.

C. loan transfer.

D. loan collateralization.

E. mutual fund management.

Answer:

Considering the Capital Asset Pricing Model, which of the following observations is

incorrect? A. In a well-diversified portfolio, unsystematic risk can be largely

diversified away.

B. Systematic risk is considered to be a diversifiable risk.

C. Total risk is the sum of systematic risk and unsystematic risk.

D. Systematic risk reflects the co-movement of a stock with the market portfolio.

E. Unsystematic risk is specific to the firm.

Answer:

As banks have increased the use of technology over the past 20 years, A. noninterest

income as a percent of total operating income has approximately doubled.

B. there has been a decrease in the importance of both Fedwire and CHIPS.

C. there has been an increase in negative net present value because of the speed in

which rivals can replicate innovations.

D. banks no longer need to consolidate because they can access customers worldwide

through internet services.

E. noninterest expense as a percent of total operating income has decreased as

supporting branch banking has decreased in importance.

Answer:

The Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA)

restructured the savings association deposit insurance fund and transferred its

management to the FDIC.

Answer:

In the NAIC model for life insurance companies, which risk covers the amount of

capital necessary to meet the maximum contribution that an insurance company may

need to make to the state guarantee fund? A. Interest rate risk.

B. Business risk.

C. Asset risk.

D. Foreign exchange risk.

E. Insurance risk.

Answer:

Which approach to measuring market risk, in effect, amounts to simulating or creating

artificial trading days and FX rate changes? A. Back simulation approach.

B. Variance/covariance approach.

C. Monte Carlo simulation approach.

D. RiskMetrics Model.

E. All of the above.

Answer:

Required reserve ratios in the U.S. for demand deposits are A. 0 percent, 3 percent, and

10 percent.

B. 10 percent on all deposits.

C. 3 percent on all deposits.

D. 0 percent on all deposits.

E. 0 percent and 3 percent.

Answer:

An insurance policy that allows both the premium amount and the maturity of the life

contract to be changed by the insured is calledA. term life.

B. universal life.

C. whole life.

D. endowment life.

E. variable life.

Answer:

The effect to an FI of default by the counterparty to a derivative contract is LEAST

serious with A. options contracts.

B. futures contracts.

C. swap agreements.

D. forward contracts.

E. loan commitments.

Answer:

Which of the following involves fixed premium payments and a benefit payout at the

time of death that will depend on investment returns over the life of the policy?A. Term

life.

B. Variable life.

C. Whole life.

D. Endowment life.

E. Universal life.

Answer:

An interest rate increase A. benefits the FI by increasing the market value of the FI’s

liabilities.

B. harms the FI by increasing the market value of the FI’s liabilities.

C. harms the FI by decreasing the market value of the FI’s liabilities.

D. benefits the FI by decreasing the market value of the FI’s liabilities.

E. benefits the FI by decreasing the market value of the FI’s assets.

Answer:

Which of the following is an example of an exogenous risk? A. Blocking reform

implementation.

B. Regional economic crisis.

C. Increase in political instability.

D. Social tensions that undermine implementation of reforms.

E. Reversing of reform actions by powerful interest groups.

Answer:

The following question are based on material in Appendix 8B

The yield curve A. relates rates for different maturities of assets.

B. for U.S. Treasury securities is the most commonly reported yield curve.

C. may change shape over time.

D. which is inverted does not last very long.

E. All of the above.

Answer:

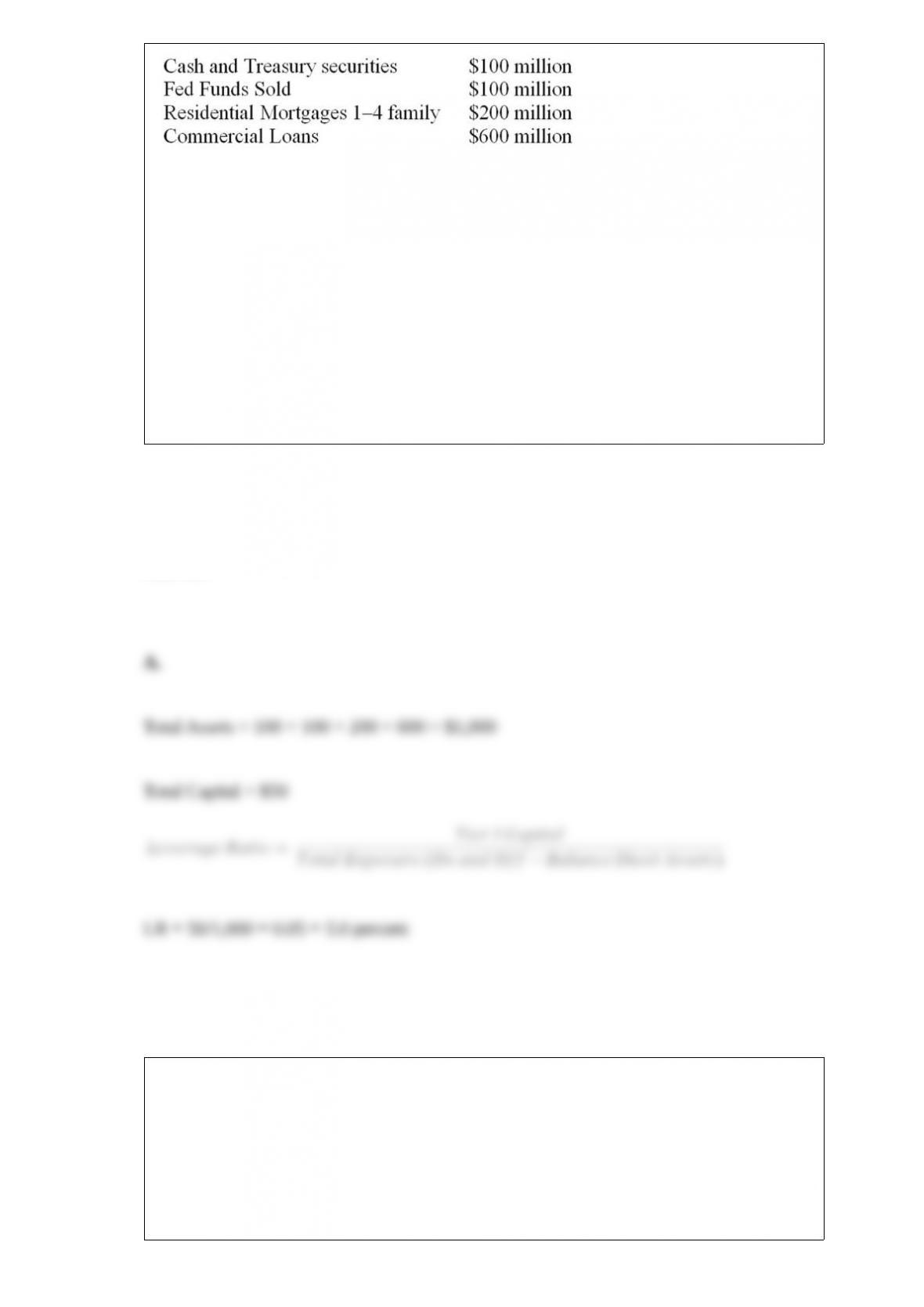

Note: The residential

mortgages all have a loan-to-value of between 60 and 80 percent.

If the bank has capital of $50 million, what is the leverage ratio using the standardized

approach? A. 5.00 percent.

B. 8.33 percent.

C. 25.0 percent.

D. 50.0 percent.

E. None of the above.

Answer:

Commodity price and quantity risk is measured by which of the following variables in

the credit scoring model to estimate sovereign country risk exposure? A. The debt

service ratio.

B. The import ratio.

C. The variance of export revenue.

D. The investment ratio.

E. Domestic money supply growth.

Answer:

The system of flat deposit insurance premium formerly used in the U.S.A. enhances

bank safety and soundness because it discourages bank risk taking.

B. reduces bank safety and soundness because it encourages bank risk taking.

C. has no impact on bank safety and soundness.

D. places banks that are considered “too big to fail” at a disadvantage.

E. provides unfair advantage to small community banks.

Answer:

Which of the following risk categories is NOT covered by the risk-based model for the

life insurance industry? A. Interest rate risk.

B. Business risk.

C. Asset risk.

D. Foreign exchange risk.

E. Insurance risk.

Answer:

Which of the following is an incentive to securitize mortgage assets?A. To reduce the

regulatory tax burden on the FI.

B. To adjust the gap exposure of the FI.

C. To improve the liquidity of the FI.

D. To generate non-interest sensitive fee income.

E. All of the above.

Answer:

Which of the following is a condition for a DI to be growing? A. Net positive drain on

deposits.

B. Peak of the net deposit drain probability distribution should lie at a point to the right

of zero.

C. Average deposit drain such that new deposit funds more than offset deposit

withdrawals.

D. The liability side of its balance sheet is decreasing.

E. Unused loan commitments is increasing.

Answer:

The FI is acting as a FX market agent for its customers when it A. buys or sells

currency to balance the FI’s net exposure.

B. takes a nonzero net position in a particular currency.

C. processes an exporter’s transaction in a foreign currency.

D. makes a market in its domestic currency.

E. advises customers on their international business.

Answer:

The insurance company that was the largest beneficiary of federal bailout funds during

the most recent financial crisis was A. Globe Life.

B. UBS.

C. State Farm.

D. AIG.

E. New York Life.

Answer:

What is the 20-day VAR?A. $5,000.

B. $10,000.

C. $15,811.

D. $22,361.

E. $50,000.

Answer:

New SEC rules call for shareholder reports to includeA. clear information to investors

on brokerage commissions and discounts.

B. information on how the fund compares with industry averages on fees and loads.

C. information on eligibility for breakpoint discounts.

D. All of the above.

E. Only two of the above.

Answer: