Prepayment risk means that realized cash flows on pass-through securities may be more

than expected cash flows.

Answer:

The passage of legislation to prevent discrimination in lending is an example of

regulation to protect investors.

Answer:

The net stable funds ratio (NSFR) is a longer-term measure than the liquidity coverage

ratio (LCR).

Answer:

The economic definition of the value of an FI’s equity is the book value of assets minus

the market value of liabilities.

Answer:

The losses on a purchased put option position when rates fall are limited to the option

premium paid.

Answer:

Lehman Brothers failed during the recent financial crisis despite having access to the

low cost sources of funds offered by the Federal Reserve.

Answer:

Market risk is the uncertainty of an FI’s earnings resulting from changes in market

conditions such as interest rates and asset prices.

Answer:

Term life insurance includes a savings element as well as the pure insurance element.

Answer:

If the fees charged on demand deposit accounts do not cover the cost of providing

demand deposit services, the bank receives a subsidy or implicit interest payment.

Answer:

As securitization of assets continues to expand, the management of market risk will

become more important to FIs.

Answer:

Because finance companies do not accept deposits, they do not have bank regulators

providing oversight of their activities.

Answer:

As of 2012, banks must report their The Liquidity Coverage Ratio (LCR) to the FDIC

rather than to the Federal Reserve.

Answer:

The goal of credit allocation is the encouragement of FIs to diversity the composition of

their assets.

Answer:

Loans sold without recourse have contingent liability off-balance-sheet implications for

the FI that sells the loan.

Answer:

When a portion of a loan is sold from a large bank to a small bank, it is often called a

participation.

Answer:

Duration measures the average life of a financial asset.

Answer:

As of 2012, the combined value of payments sent over Fedwire and CHIPS often

exceeded $5.0 trillion a day.

Answer:

Counterparty credit risk is the risk that the other party of a contract will default on

contract obligations.

Answer:

At some point, further increases in interest rates on specific loans may decrease

expected loan returns because of increased probability of default by the borrower.

Answer:

State guaranty funds for insurance companies are sponsored by state insurance

regulators rather than by a federal agency such as the FDIC.

Answer:

As of January 2012, credit cards used in either a credit or debit function accounted for

over 60 percent of the number of payments made in the U.S.

Answer:

The securities that form a GNMA pass-through are U.S. Treasury bonds, bills, and

notes.

Answer:

Capital is the primary protection for an FI against the risk of insolvency and failure.

Answer:

Contingent credit risk on derivative contracts is more serious for futures contracts than

for forward contracts.

Answer:

Certificates of Amortizing Revolving Debts are asset-backed securities that have a

claim on automobile installment loans.

Answer:

Market risk is the potential gain caused by an adverse movement in market conditions.

Answer:

Savings associations and savings banks both are insured by insurance funds that are

managed by the FDIC.

Answer:

Large money center banks are often primary dealers in the U.S. Treasury markets.

Answer:

Explicit deposit insurance premiums applied by regulators can involve restricting and

more closely monitoring the risky activities of banks.

Answer:

Using a fixed-rate bond to immunize a desired investment horizon means that the

reinvested coupon payments are not affected by changes in market interest rates.

Answer:

A bad news effect of increased mortgage prepayments on a mortgage pool caused by

decreasing market interest rates includes a reduction in the discount rate on the

mortgage cash flow.

Answer:

Off-balance sheet positions are risky because they may yield negative future cash

flows.

Answer:

As recent economic conditions improved, trading volumes in the secondary market for

LCD and EM debt reached approximately $6.5 trillion in

Answer:

Based on your answers to the previous three question, which of the following is TRUE?

A. Security Alpha represents the riskier of the two assets in the trading portfolio

because there is a one-percent probability of loss the following day.

B. Both securities have the same expected payoff; therefore, it makes no difference

which is in the trading portfolio.

C. Security Beta is the better asset to have in the trading portfolio since there is a 50

percent probability of a $400 payoff versus only $355 with security Alpha.

D. Both securities have the same expected payoff and value at risk (VAR), therefore it

makes no difference which is in the trading portfolio.

E. According to the expected shortfall measure, if tomorrow is a bad trading day, losses

will exceed $25 million.

Answer:

Off-balance-sheet activities often affect the shape of an FIs current balance sheet

through the creation of contingent claims.

Answer:

One of the goals of mutual funds is to achieve superior diversification through fund and

risk pooling compared to what individual investors can achieve.

Answer:

Asset-side liquidity risk may be a result of OBS lending commitments.

Answer:

Off-balance-sheet activities have become an important source of fee income, even

though losses on these activities can cause a financial institution to fail.

Answer:

The probability that a borrower would default in any specific time period is a marginal

default probability.

Answer:

One hundred identical mortgages are pooled together into a pass-through security. Each

mortgage has a $150,000 principal, a fixed annual interest rate of 8 percent (paid

monthly), and is fully amortized over a term of 30 years.

What is the present value of the mortgage pass-through if, immediately after

origination, interest rates increase to 8.25 percent per annum?A. $15,000,000.

B. $14,650,591.

C. $14,000,000.

D. $15,115,493.

E. $15,267,549.

Answer:

One hundred identical mortgages are pooled together into a pass-through security. Each

mortgage has a $150,000 principal, a fixed annual interest rate of 8 percent (paid

monthly), and is fully amortized over a term of 30 years.

What is the monthly payment on the mortgage pass-through if a 44 basis point servicing

fee is deducted monthly? A. $105,499.

B. $114,700.

C. $11,340.

D. $1,055.

E. $1,277,494.

Answer:

How many options should the FI purchase, and what will be the cost? A. 1,600

contracts for $16.96.

B. 1,600 contracts for $1,060,000.

C. 3,200 contracts for $44.80.

D. 3,200 contracts for $1,400,000.

E. 3,200 contracts for $2,800,000.

Answer:

If an FIs trading portfolio of stock is not well-diversified, the additional risk that must

be taken into account is A. unsystematic risk.

B. default risk.

C. timing risk.

D. interest rate risk.

E. systematic risk.

Answer:

Which of the following statements best describes the treatment of adjusting for credit

risk of off-balance-sheet activities? A. All OBS activities are treated equally in making

credit-risk adjustments.

B. Standby letter of credit guarantees issued by banks to back commercial paper have a

50 percent conversion factor.

C. The credit or default risk of over-the-counter contracts is approximately zero.

D. The current exposure component of the credit equivalent amount of OBS derivative

contracts reflects the credit risk if the contract counterparty defaults.

E. The treatment of interest rate forward, option, and swap contracts differs from the

treatment of contingent or guarantee contracts.

Answer:

Assume that the portfolio manager sells the bonds at a price of 87-05/32, and that she

closes out the futures hedge position at a price of 81-17/32. What will be the net gain or

loss on the entire bond transaction from the time that the hedge was placed?A. Gain of

$2,583,125.

B. Loss of $93,750.

C. Loss of $2,583,125.

D. Gain of $93,750.

E. Gain of $812,700.

Answer:

All else equal, advantages of a DI operating as an asset broker in regard to mortgages

includes all of the following EXCEPT A. lower regulatory taxes.

B. increased fee-based income.

C. increased liquidity.

D. decreased asset and liability duration mismatch.

E. increased capital requirements.

Answer:

An investment company has purchased $100 million of 10 percent annual coupon,

6-year Eurobonds. The bonds have a duration of 4.79 years at the current market yields

of 10 percent. The company wishes to hedge these bonds with Treasury-bond options

that have a delta of 0.7. The duration of the underlying asset is 8.82, and the market

value of the underlying asset is $98,000 per $100,000 face value. Finally, the volatility

of the interest rates on the underlying bond of the options and the Eurobond is 0.84.

Using the above information and your answer to the previous question, will the

investment company gain or lose on the option position if interest rates decrease 1

percent to 9 percent? A. Lose $4,352,414.

B. Gain $4,352,414.

C. Lose $2,559,700.

D. Gain $3,659,354.

E. Lose $3,659,354.

Answer:

Safety and soundness regulations include all of the following layers of protection

EXCEPT A. the provision of guaranty funds.

B. requirements encouraging diversification of assets.

C. the creation of money for those FIs in financial trouble.

D. requiring minimum levels of capital.

E. monitoring and surveillance.

Answer:

In international finance, the investment ratio is determined by dividing the value of real

investment by the A. total foreign exchange reserves.

B. real investment.

C. gross national product.

D. value of exports.

E. money supply.

Answer:

A $200 million loan commitment has an up-front fee of 20 basis points and a back-end

fee of 25 basis points on the unused portion.

The up-front fee is A. $250,000.

B. $4,000,000.

C. $400,000.

D. $775,000.

E. $375,000.

Answer:

As of January 2012, which of the following accounts for the highest volume of noncash

transactions in the United States? A. Checks.

B. Card payments.

C. Debit transfers.

D. E-money payments.

E. Credit transfers.

Answer:

The economic value of narrowly defined bank franchises has declined becauseA.

product line restrictions inhibit the ability of an FI to optimize the set of financial

services it can offer.

B. product restrictions limit the ability of FI managers to adjust flexibly to shifts in the

demand for financial products.

C. product restrictions limit the ability of FI managers to adjust flexibly to shifts in

costs due to technology and related innovations.

D. All of the above.

E. Answers A and B only.

Answer:

A commercial bank operating under an originate-to-distribute model is acting most like

A. an asset transformer.

B. an asset broker.

C. a portfolio lender.

D. an asset accumulator.

E. an investment bank.

Answer:

Settlement risk is important because A. of the interdependent nature of many

international transactions.

B. of the impact on sovereign country risk.

C. problems may induce countries to limit the freedom of international capital flows.

D. the electronic funds transfer network itself may become insolvent.

E. the Fed’s guarantee may prove to be even more costly to the Federal government

than the thrift debacle.

Answer:

The function of institutional venture capital firms is to A. find and fund the most

promising new firms.

B. lend funds on a long-term basis to promising new companies with no track record.

C. take equity positions in successful established companies.

D. lend funds to established companies that are faltering.

E. none of the above.

Answer:

How can interest income of an FI be increased by improved technological efficiency?

A. By improving the efficiency of management of information flows.

B. By obtaining access to low cost sources of funds.

C. By linking services to the quality of the FI’s technology.

D. By innovating new interest earning products.

E. By complying with all government regulations.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

Provided for state regulation of insurance.

Answer:

An exporter demands a letter of credit in order to A. guarantee safe delivery of goods

to the importer.

B. guarantee receipt of payment from the importer upon receipt of the goods.

C. protect against adverse changes in foreign exchange rates.

D. protect against adverse changes in international interest rates.

E. ascertain the creditworthiness of the importer.

Answer:

A company that provides financing to corporations, especially through equipment

leasing and factoring would best be categorized as a A. sales finance institution.

B. personal credit institution.

C. subprime lender.

D. loan shark.

E. business credit institution.

Answer:

Which of the following is traditionally the major type of consumer loans for finance

companies? A. Revolving loans.

B. Motor vehicle loans and leases.

C. Wholesale loans.

D. Equipment leases.

E. Home equity loans.

Answer:

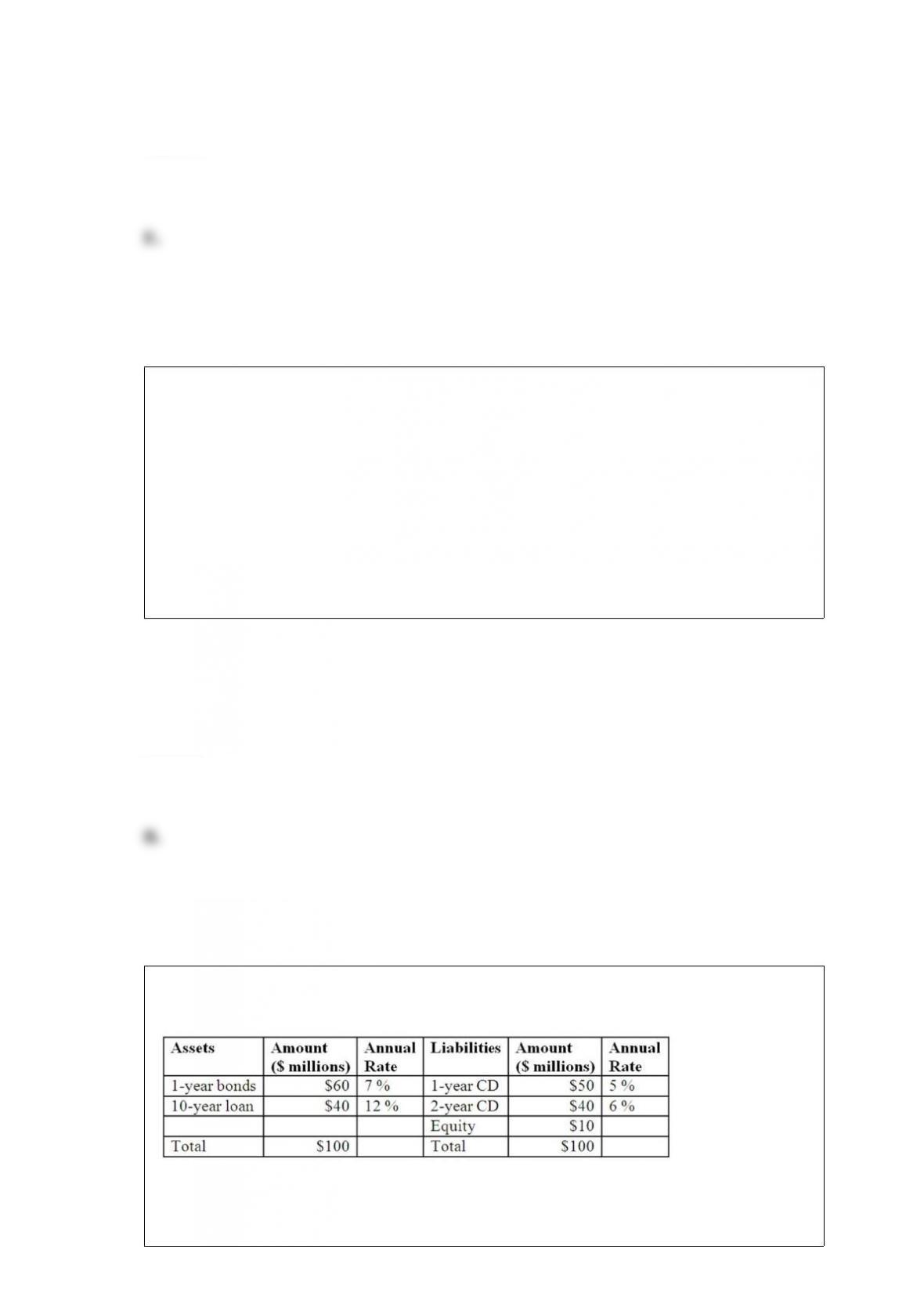

Hadbucks National Bank current balance sheet appears below. All assets and liabilities

are currently priced at par and pay interest annually.

What is market

value of the one-year CD if all market interest rates increase by 2 percent? A. $49.065

million.

B. $50.481 million.

C. $49.528 million.

D. $50.971 million.

E. $50.000 million.

Answer:

As of June 2012, the vast majority of OBS activities of commercial banks was A.

future and forward contracts.

B. credit derivatives.

C. commitments to buy FX.

D. swap contracts.

E. loans sold with recourse.

Answer:

Net regulatory burden for FIs is higher because regulators may require the FI to A. hold

more capital than what would be held without regulation.

B. produce less information than would be produced without regulation.

C. hold more debt than what would be held without regulation.

D. hold fewer reserves than they would without regulation.

E. All of the above.

Answer:

A mutual fund that charges investors a fee similar to a commission charge is called a A.

12b-1 fee.

B. no-load fund.

C. load fund.

D. long-term fund.

E. short-term fund.

Answer:

A value below 1,000 of the Herfindahl-Hirschman Index (HHI) is considered to reflect

A. a highly concentrated market.

B. an unconcentrated market.

C. a high growth market.

D. a moderately concentrated market.

E. an untapped market.

Answer:

Which of the following refers to an FI’s ability to generate cost synergies by producing

more than one output with the same inputs?A. Market intermediation.

B. Economies of scope.

C. Break-even point.

D. Economies of scale.

E. Business continuity plan.

Answer:

Takedown risk in a loan commitment exposes the FI to A. immediate liquidity risk.

B. basis risk.

C. spread risk.

D. externality effects.

E. future liquidity risk.

Answer:

When purchasing and selling foreign currencies to allow customers to take positions in

foreign real and financial investments, the FI A. acts defensively as a hedger.

B. acts aggressively as a speculator.

C. assumes the FX risk itself.

D. acts as an agent.

E. acts as a market maker.

Answer:

Which of the following balance sheet entries is not a tool used in purchased liquidity

management? A. Bonds.

B. Federal fund.

C. Demand deposit.

D. Repurchase agreement.

E. Subordinated note.

Answer:

An investment banker agrees to underwrite an issue of 10 million shares of stock for

Rochester Industries on a best-efforts basis. The investment banker is able to sell 8

million shares for $10.50 per share, and it charges Rochester Industries $0.225 per share

sold.

How much money does Rochester Industries receive? A. $15,000,000.

B. $84,000,000.

C. $76,200,000.

D. $82,200,000.

E. $110,000,000.

Answer:

In the early 1980s A. banks increased their off-balance-sheet activities to avoid

competition from nonbank banks.

B. banks decreased their off-balance-sheet activities to avoid regulatory taxes.

C. banks decreased their off-balance-sheet activities to avoid competition from

nonbank banks.

D. banks increased their off-balance-sheet activities to avoid regulatory costs.

E. banks increased their off-balance-sheet activities to avoid interest rate risk exposure.

Answer:

Mutual fund shares that are offered for sale at the NAV without a front-end load, but

which charge a combination of 12b-1 fees and a back-end load, and whose back-end

load typically remains in effect for 6 to 8 years, are A. Class A shares.

B. Class B shares.

C. Class C shares.

D. Class D shares.

E. either Class A or Class C shares.

Answer:

How would you characterize the FI’s risk exposure to fluctuations in the yen/dollar

exchange rate? A. The FI is net short in the yen and therefore faces the risk that the yen

will rise in value against the U.S. dollar.

B. The FI is net short in the yen and therefore faces the risk that the yen will fall in

value against the U.S. dollar.

C. The FI is net long in the yen and therefore faces the risk that the yen will fall in

value against the U.S. dollar.

D. The FI is net long in the yen and therefore faces the risk that the yen will rise in

value against the U.S. dollar.

E. The FI has a balanced position in the Japanese yen.

Answer:

Which of the following hedge fund objectives would be classified under the “moderate

risk” category? A. Distressed securities funds.

B. Market neutral-arbitrage funds.

C. Value funds.

D. Short selling funds.

E. Market timing funds.

Answer: