Commodity futures pricing

A. must be related to spot prices.

B. includes cost of carry.

C. converges to spot prices at maturity.

D. All of the options are correct.

E. None of the options.

Par-value bond XYZ has a modified duration of 6. Which one of the following

statements regarding the bond is true?

A. If the market yield increases by 1%, the bond’s price will decrease by $60.

B. If the market yield increases by 1%, the bond’s price will increase by $50.

C. If the market yield increases by 1%, the bond’s price will decrease by $50.

D. If the market yield increases by 1%, the bond’s price will increase by $60.

If an investor has a portfolio that has constant proportions in T-bills and the market

portfolio, the portfolio’s characteristic line will plot as a line with ___________. If the

investor can time bull markets, the characteristic line will plot as a line with

___________.

A. a positive slope; a negative slope

B. a negative slope; a positive slope

C. a constant slope; a negative slope

D. a negative slope; a constant slope

E. a constant slope; a positive slope

A European put option allows the holder to

A. buy the underlying asset at the striking price on or before the expiration date.

B. sell the underlying asset at the striking price on or before the expiration date.

C. potentially benefit from a stock price increase.

D.sell the underlying asset at the striking price on the expiration date.

E. potentially benefit from a stock price increase and sell the underlying asset at the

striking price on the expiration date.

An American-style call option with six months to maturity has a strike price of $42. The

underlying stock now sells for $50. The call premium is $14. What is the intrinsic value

of the call?

A. $12

B. $10

C. $8

D. $23

According to the mean-variance criterion, which one of the following investments

dominates all others?

A. E(r) = 0.15; Variance = 0.20

B. E(r) = 0.10; Variance = 0.20

C. E(r) = 0.10; Variance = 0.25

D. E(r) = 0.15; Variance = 0.25

E. None of these options dominates the other alternatives.

Which of the following is true regarding a firm’s securities?

A. Common dividends are paid before preferred dividends.

B. Preferred stockholders have voting rights.

C. Preferred dividends are usually cumulative.

D. Preferred dividends are contractual obligations.

E. Common dividends can usually be paid if preferred dividends have been skipped.

A Treasury bill with a par value of $100,000 due one month from now is selling today

for $99,010. The effective annual yield is

A. 12.40%.

B. 12.55%.

C. 12.62%.

D. 12.68%.

E. None of the options are correct.

Consider the following probability distribution for stocks A and B:

The expected rates of return of stocks A and B are _____ and _____, respectively.

A. 13.2%; 9%

B. 14%; 10%

C. 13.2%; 7.7%

D. 7.7%; 13.2%

The level of real income of a firm can be distorted by the reporting of depreciation and

interest expense. During periods of high inflation, the level of reported depreciation

tends to __________ income, and the level of interest expense reported tends to

__________ income.

A. understate; overstate

B. understate; understate

C. overstate; understate

D. overstate; overstate

E. There is no discernible pattern.

Most actively-managed mutual funds, when compared to a market index such as the

Wilshire 5000,

A. beat the market return in all years.

B. beat the market return in most years.

C. exceed the return on index funds.

D. do not outperform the market.

A coupon bond is reported as having an ask price of 108% of the $1,000 par value in

the Wall Street Journal. If the last interest payment was made one month ago and the

coupon rate is 9%, the invoice price of the bond will be

A. $1,087.50.

B. $1,110.10.

C. $1,150.00.

D. $1,160.25.

E. None of the options are correct.

A mutual fund had NAV per share of $19.00 on January 1, 2016. On December 31 of

the same year, the fund’s NAV was $19.14. Income distributions were $0.57, and the

fund had capital gain distributions of $1.12. Without considering taxes and transactions

costs, what rate of return did an investor receive on the fund last year?

A. 11.26%

B. 10.54%

C. 7.97%

D. 8.26%

E. 9.63%

If an investment provides a 2.1% return quarterly, its effective annual rate is

A. 2.1%.

B. 8.4%.

C. 8.56%.

D. 8.67%.

In order for you to be indifferent between the after-tax returns on a corporate bond

paying 9% and a tax-exempt municipal bond paying 7%, what would your tax bracket

need to be?

A. 17.6%

B. 27%

C. 22.2%

D. 19.8%

E. Cannot be determined from the information given.

Zero had a FCFE of $4.5M last year and has 2.25M shares outstanding. Zero’s required

return on equity is 10%, and WACC is 8.2%. If FCFE is expected to grow at 8%

forever, the intrinsic value of Zero’s shares is

A. $108.00.

B. $1080.00.

C. $26.35.

D. $14.76.

E. None of the options are correct.

Which of the following statements are true?

I) Holding other things constant, the duration of a bond decreases with time to maturity.

II) Given time to maturity, the duration of a zero-coupon increases with yield to

maturity.

III) Given time to maturity and yield to maturity, the duration of a bond is higher when

the coupon rate is lower.

IV) Duration is a better measure of price sensitivity to interest-rate changes than is time

to maturity.

A. I only

B. I and II

C. III only

D. III and IV

E. I, II, and IV

An example of a highly cyclical industry is

A.-the automobile industry.

B. the tobacco industry.

C. the food industry.

D. the automobile industry and the tobacco industry.

E. the tobacco industry and the food industry.

The current market price of a share of IBM stock is $195. If a call option on this stock

has a strike price of $195, the call

A. is out of the money.

B. is in the money.

C.is at the money.

D. None of the options are correct.

Suppose you are doing a portfolio analysis that includes all of the stocks on the NYSE.

Using a single-index model rather than the Markowitz model

A. increases the number of inputs needed from about 1,400 to more than 1.4 million.

B. increases the number of inputs needed from about 10,000 to more than 125,000.

C. reduces the number of inputs needed from more than 125,000 to about 10,000.

D. reduces the number of inputs needed from more than 5 million to about 10,000.

E. increases the number of inputs needed from about 150 to more than 1,500.

Investment manager Peter Lynch refers to firms that are in bankruptcy or soon might be

as

A. slow growers.

B. stalwarts.

C. cyclicals.

D. asset plays.

E.-turnarounds.

Assume that stock market returns do not resemble a single-index structure. An

investment fund analyzes 40 stocks in order to construct a mean-variance efficient

portfolio constrained by 40 investments. They will need to calculate _____________

expected returns and ___________ variances of returns.

A. 100; 100

B. 40; 40

C. 4950; 100

D. 4950; 4950

E. None of the options are correct.

Of the following types of ETFs, an investor who wishes to invest in a diversified

portfolio that tracks the Wilshire 5000 should choose

A. SPY.

B. DIA.

C. QQQ.

D. IWM.

E. VTI.

When Country A’s currency strengthens against Country B’s, citizens of Country A will

A. pay less to buy Country B’s products.

B. pay more to buy Country B’s products.

C. pay more to buy domestically-produced products.

D. not be affected by the change in their currency’s value

If the economy is shrinking, firms with high operating leverage will experience

A.-larger decreases in profits than firms with low operating leverage.

B. similar decreases in profits as firms with low operating leverage.

C. smaller decreases in profits than firms with low operating leverage.

D. no change in profits.

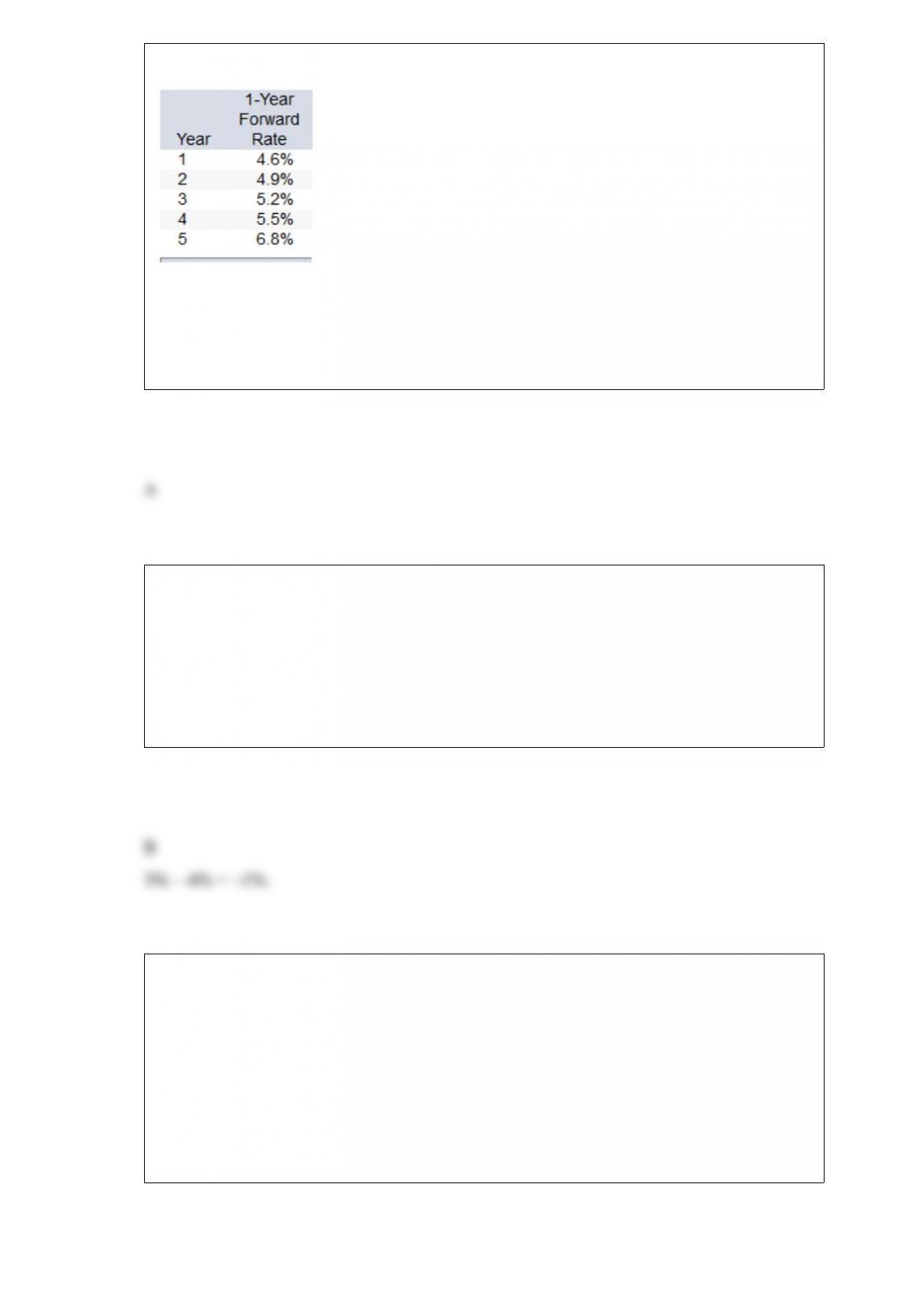

What is the yield to maturity of a 1-year bond?

A. 4.6%

B. 4.9%

C. 5.2%

D. 5.5%

E. 5.8%

A year ago, you invested $10,000 in a savings account that pays an annual interest rate

of 3%. What is your

approximate annual real rate of return if the rate of inflation was 4% over the year?

A. 1%

B. –1%

C. 7%

D. 3%

One year ago, you purchased a newly-issued TIPS bond that has a 4% coupon rate, five

years to maturity, and a par value of $1,000. The average inflation rate over the year

was 3.6%. What is the amount of the coupon payment you will receive, and what is the

current face value of the bond?

A. $40.00, $1,000

B. $41.44, $1,036

C. $40.00, $1,036

D. $36.00, $1,040

E. $76.00, $1,000

The index model was first suggested by

A. Graham.

B. Markowitz.

C. Miller.

D. Sharpe.

The secondary market consists of

A. transactions on the AMEX.

B. transactions in the OTC market.

C. transactions through the investment banker.

D. transactions on the AMEX and in the OTC market.

E. transactions on the AMEX, through the investment banker, and in the OTC market.

An example of ________ is that a person may reject an investment when it is posed in

terms of risk surrounding potential gains, but may accept the same investment if it is

posed in terms of risk surrounding potential losses.

A. framing

B. regret avoidance

C. overconfidence

D. conservatism