The optimal risky portfolio can be identified by finding:

I. The minimum-variance point on the efficient frontier

II. The maximum-return point on the efficient frontier and the minimum-variance point

on the efficient frontier

III. The tangency point of the capital market line and the efficient frontier

IV. The line with the steepest slope that connects the risk-free rate to the efficient

frontier

A. I and II only

B. II and III only

C. III and IV only

D. I and IV only

Assume that you have invested $500,000 to purchase shares in a hedge fund reporting

$800 million in assets, $100 million in liabilities, and 70 million shares outstanding.

Your initial lockout period is 3 years.

What is your annualized return over the 3-year holding period?

A. 14.45%

B. 15.18%

C. 16%

D. 17.73%

An investor buys $16,000 worth of a stock priced at $20 per share using 60% initial

margin. The broker charges 8% on the margin loan and requires a 35% maintenance

margin. The stock pays a $.50-per-share dividend in 1 year, and then the stock is sold at

$23 per share. What was the investor’s rate of return?

A. 17.5%

B. 19.67%

C. 23.83%

D. 25.75%

According to the put-call parity theorem, the payoffs associated with ownership of a

call option can be replicated by

__________________.

A. shorting the underlying stock, borrowing the present value of the exercise price, and

writing a put on the same underlying stock and with the same exercise price

B. buying the underlying stock, borrowing the present value of the exercise price, and

buying a put on the same underlying stock and with the same exercise price

C. buying the underlying stock, borrowing the present value of the exercise price, and

writing a put on the same underlying stock and with the same exercise price

D. shorting the underlying stock, lending the present value of the exercise price, and

buying a put on the same underlying stock and with the same exercise price

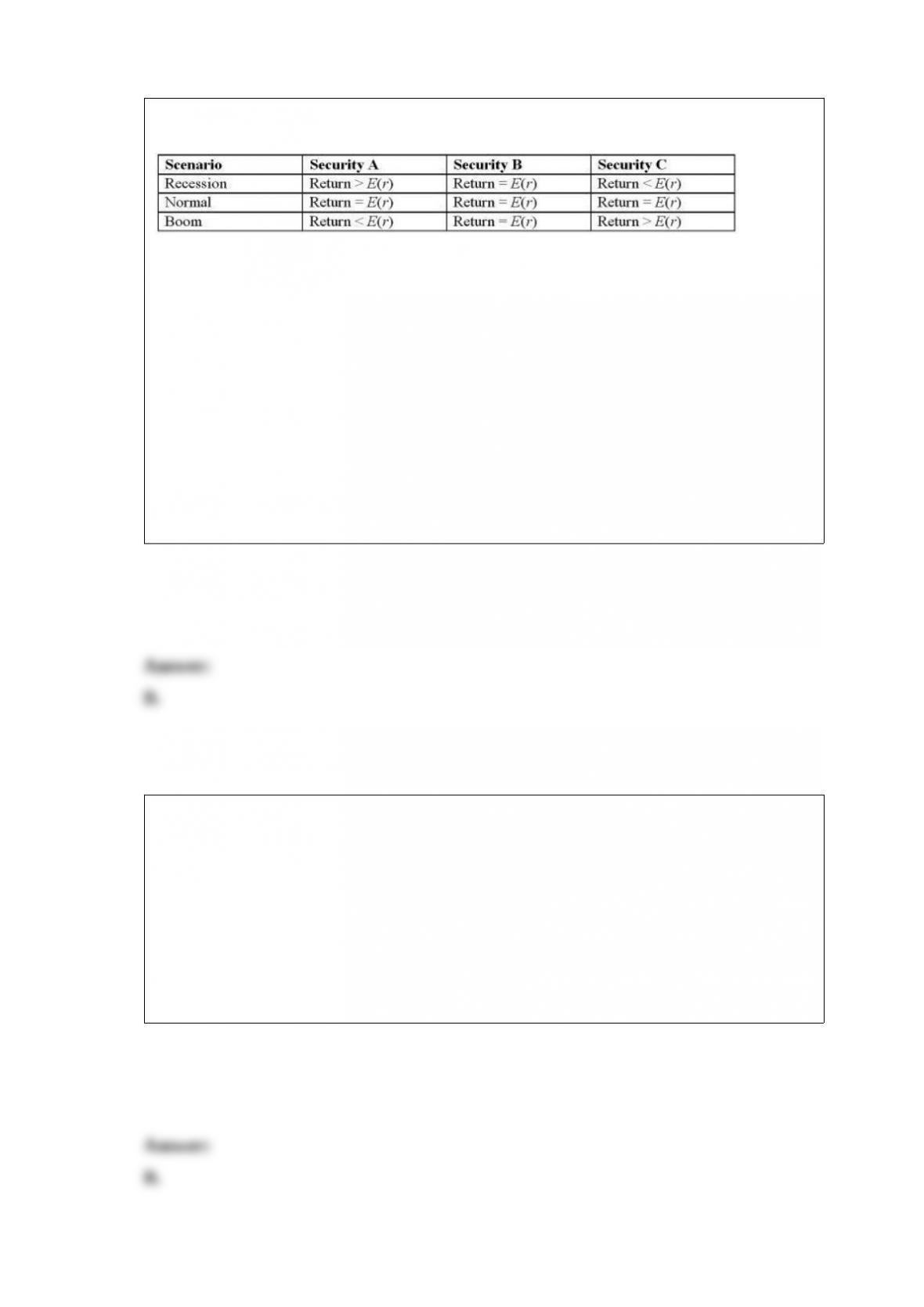

Based on the outcomes in the following table, choose which of the statements below is

(are) correct?

I. The covariance of security A and security B is zero.

II. The correlation coefficient between securities A and C is negative.

III. The correlation coefficient between securities B and C is positive.

A. I only

B. I and II only

C. II and III only

D. I, II, and III

The tax effect of a traditional retirement plan is to _____ taxes.

A. evade

B. postpone

C. erase

D. avoid

Suppose you have maxed out your allowable contributions to your tax-sheltered

retirement plans and you still want to shelter income. The best choice of investment for

you to minimize the tax bill is to invest in _________.

A. a bond portfolio

B. stocks with high dividend yields

C. a blended stock and bond portfolio containing zero-coupon bonds

D. stocks with low or zero dividend yields

A portfolio of stocks fluctuates when the Treasury yields change. Since this risk cannot

be eliminated through diversification, it is called

__________.

A. firm-specific risk

B. systematic risk

C. unique risk

D. none of the options

Which of the following statements is (are) true regarding time diversification?

I. The standard deviation of the average annual rate of return over several years will be

smaller than the 1-year standard deviation.

II. For a longer time horizon, uncertainty compounds over a greater number of years.

III. Time diversification does not reduce risk.

A. I only

B. II only

C. II and III only

D. I, II, and III

Mutual funds that hold both equities and fixed-income securities in relatively stable

proportions are called ____________________.

A. income funds

B. balanced funds

C. asset allocation funds

D. index funds

An important assumption underlying the use of technical analysis techniques is that

___________________.

A. security prices adjust rapidly to new information

B. security prices adjust gradually to new information

C. security dealers will provide enough liquidity to keep price changes relatively small

D. all investors have immediate and costless access to information

A firm has an ROE equal to the industry average, but its price-to-book ratio is below the

industry average. You know that the firm’s _________.

A. earnings yield is above the industry average

B. P/E ratio is above the industry average

C. dividend payout ratio is too high

D. interest burden must be below the industry average

Which of the following typically employ(s) significant amounts of leverage?

I. Hedge funds

II. Equity mutual funds

III. Money market funds

IV. Income mutual funds

A. I only

B. I and II only

C. III and IV only

D. I, II, and III only

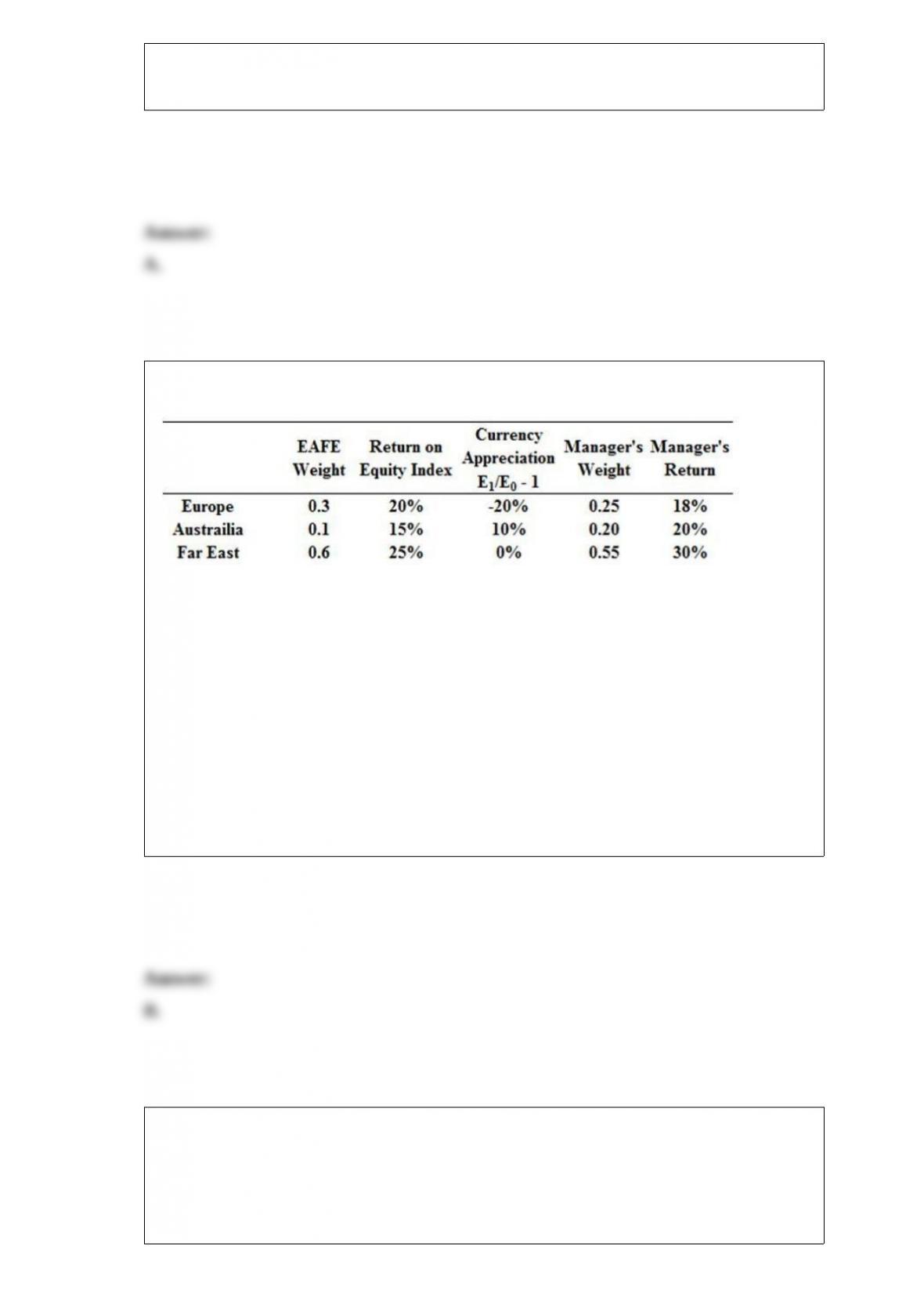

All exchange rates are expressed as units of foreign currency that can be purchased with

one U.S. dollar. Answer the following about decomposing the manager’s performance.

What is the difference in return of the manager’s portfolio due to stock selection?

A. 1.15%

B. 3.25%

C. 5.45%

D. 6.13%

Which one of the following is equal to the ratio of common shareholders’ equity to

common shares outstanding?

A. book value per share

B. liquidation value per share

C. market value per share

D. Tobin’s q

Which of the following describes the rate at which your ability to purchase grows while

you hold an interest-earning investment?

A. the nominal exchange rate

B. the nominal interest rate

C. the real exchange rate

D. the real interest rate

A firm has a stock price of $54.75 per share. The firm’s earnings are $75 million, and

the firm has 20 million shares outstanding. The firm has an ROE of 15% and a

plowback of 65%. What is the firm’s PEG ratio?

A. 1.5

B. 1.25

C. 1.1

D. 1

Which of the following indexes are market value-weighted?

I. The NYSE Composite

II. The S&P 500

III.The Wilshire 5000

A. I and II only

B. II and III only

C. I and III only

D. I, II, and III

The Treynor-Black model assumes that security markets are _________.

A. completely efficient

B. nearly efficient

C. very inefficient

D. random walks

If an individual confers legal title to property to another person or institution to manage

the property on their behalf, the individual has created ___________.

A. a personal trust

B. a charitable trust

C. an endowment fund

D. a mutual fund

You buy a bond with a $1,000 par value today for a price of $85. The bond has 6 years

to maturity and makes annual coupon payments of $5 per year. You hold the bond to

maturity, but you do not reinvest any of your coupons. What was your effective EAR

over the holding period?

A. 10.4%

B. 9.5%

C. .45%

D. 8.8%

Futures markets are regulated by the __________.

A. CFA Institute

B. CFTC

C. CIA

D. SEC

Treasury bills are paying a 4% rate of return. A risk-averse investor with a risk aversion

of A = 3 should invest entirely in a risky portfolio with a standard deviation of 24%

only if the risky portfolio’s expected return is at least ______.

A. 8.67%

B. 9.84%

C. 21.28%

D. 14.68%

Consider the multifactor APT with two factors. Portfolio A has a beta of .5 on factor 1

and a beta of 1.25 on factor 2. The risk premiums on the factor 1 and 2 portfolios are

1% and 7%, respectively. The risk-free rate of return is 7%. The expected return on

portfolio A is __________ if no arbitrage opportunities exist.

A. 13.5%

B. 15%

C. 16.25%

D. 23%

Generally speaking, as a firm progresses through the industry life cycle, you would

expect the PVGO to ________ as a percentage of share price.

A. increase

B. decrease

C. stay the same

D. No typical pattern can be expected.

The writer of a put option _______________.

A. agrees to sell shares at a set price if the option holder desires

B. agrees to buy shares at a set price if the option holder desires

C. has the right to buy shares at a set price

D. has the right to sell shares at a set price

An investor in a T-bill earns interest by _________.

A. receiving interest payments every 90 days

B. receiving dividend payments every 30 days

C. converting the T-bill at maturity into a higher-valued T-note

D. buying the bill at a discount from the face value to be received at maturity

The major difference between IFRS and GAAP is that U.S. standards are ___________

and IFRS standards are _________.

A. strictly enforced; weakly enforced

B. rules-based; principles-based

C. evolutionary; devolutionary

D. based on government standards; based on corporate practice

A moving average of stock prices _________________.

A. always lies above the most recent price

B. always lies below the most recent price

C. is less volatile than the actual prices

D. is more volatile than the actual prices

From 1971 to 2013 the average return on the Wilshire 5000 Index was _________ the

return of the average mutual fund.

A. identical to

B. .9% higher than

C. .9% lower than

D. 1.3% higher than

Probably the biggest problem with evaluating the portfolio performance of actively

managed funds is the assumption that __________________________.

A. the markets are efficient

B. portfolio risk is constant over time

C. diversification pays off

D. security selection is more valuable than asset allocation

Cache Creek Manufacturing Company is expected to pay a dividend of $3.36 in the

upcoming year. Dividends are expected to grow at 8% per year. The risk-free rate of

return is 4%, and the expected return on the market portfolio is 14%. Investors use the

CAPM to compute the market capitalization rate and use the constant-growth DDM to

determine the value of the stock. The stock’s current price is $84. Using the

constant-growth DDM, the market capitalization rate is _________.

A. 9%

B. 12%

C. 14%

D. 18%

You own a $15 million bond portfolio with a modified duration of 11 years. Interest

rates are expected to increase by 5 basis points, or

.05%. What is the price value of a basis point?

A. $10,400

B. $14,300

C. $16,500

D. $21,300

When the returns of an option and stock are perfectly correlated as in a two-state

binomial option model, the hedge ratio must be equal to the ratio of ____________.

A. the range of the option outcomes to the range of the stock outcomes

B. the range of the stock outcomes to the range of the option outcomes

C. the standard deviation of the option returns to the standard deviation of the stock

returns

D. the standard deviation of the stock returns to the standard deviation of the option

returns