The decline in the value of the dollar relative to the yen will have what impact on the

purchase of U.S. goods in Japan?

A. U.S. goods will increase in cost, and Japan will import more.

B. U.S. goods will increase in cost, and Japan will import less.

C. U.S. goods will decrease in cost, and Japan will import more.

D. U.S. goods will increase in cost, and Japan will export less.

__________ portfolio managers experience streaks of abnormal returns that are hard to

label as lucky outcomes, and _________ anomalies in realized returns have been

sufficiently persistent that portfolio managers could use them to beat a passive strategy

over prolonged periods.

A. No; no

B. No; some

C. Some; no

D. Some; some

Which of the following correlation coefficients will produce the least diversification

benefit?

A. -.6

B. -.3

C. 0

D. .8

In a simple CAPM world which of the following statements is (are) correct?

I. All investors will choose to hold the market portfolio, which includes all risky assets

in the world.

II. Investors’ complete portfolio will vary depending on their risk aversion.

III. The return per unit of risk will be identical for all individual assets.

IV. The market portfolio will be on the efficient frontier, and it will be the optimal risky

portfolio.

A. I, II, and III only

B. II, III, and IV only

C. I, III, and IV only

D. I, II, III, and IV

A mutual fund has $50 million in assets at the beginning of the year and 1 million

shares outstanding throughout the year. Throughout the year assets grow at 12%. The

fund imposes a 12b-1 fee on all shares equal to 1%. The fee is imposed on year-end

asset values. If there are no distributions, what is the end-of-year NAV for the fund?

A. $50

B. $55.44

C. $56.12

D. $54.55

You find that the annual Sharpe ratio for stock A returns is equal to 1.8. For a 3-year

holding period, the Sharpe ratio would equal _______.

A. 1.8

B. 2.48

C. 3.12

D. 5.49

An investor invests 70% of her wealth in a risky asset with an expected rate of return of

15% and a variance of 5%, and she puts 30% in a Treasury bill that pays 5%. Her

portfolio’s expected rate of return and standard deviation are __________ and

__________ respectively.

A. 10%; 6.7%

B. 12%; 22.4%

C. 12%; 15.7%

D. 10%; 35%

Market economists all predict a rise in interest rates. An astute bond manager wishing to

maximize her capital gain might employ which strategy?

A. Switch from low-duration to high-duration bonds.

B. Switch from high-duration to low-duration bonds.

C. Switch from high-grade to low-grade bonds.

D. Switch from low-coupon to high-coupon bonds.

One of the main problems with the arbitrage pricing theory is __________.

A. its use of several factors instead of a single market index to explain the risk-return

relationship

B. the introduction of nonsystematic risk as a key factor in the risk-return relationship

C. that the APT requires an even larger number of unrealistic assumptions than does the

CAPM

D. the model fails to identify the key macroeconomic variables in the risk-return

relationship

Suppose the 1-year risk-free rate of return in the United States is 5% and the 1-year

risk-free rate of return in Britain is 8%. The current exchange rate is $1 = ₤.50. A 1-year

future exchange rate of __________ would make a U.S. investor indifferent between

investing in the U.S. security and investing in the British security.

A. ₤.5150

B. ₤.5142

C. ₤.5123

D. ₤.4859

Suppose the 6-month risk-free rate of return in the United States is 5%. The current

exchange rate is 1 pound = US$2.05. The 6-month forward rate is 1 pound = US$2. The

minimum yield on a 6-month risk-free security in Britain that would induce a U.S.

investor to invest in the British security is

________.

A. 5.06%

B. 6.74%

C. 8.48%

D. 10.13%

A T-bill quote sheet has 90-day T-bill quotes with a 4.92 bid and a 4.86 ask. If the bill

has a $10,000 face value, an investor could buy this bill for

_____.

A. $10,000

B. $9,878.50

C. $9,877

D. $9,880.16

A measure of the riskiness of an asset held in isolation is ____________.

A. beta

B. standard deviation

C. covariance

D. alpha

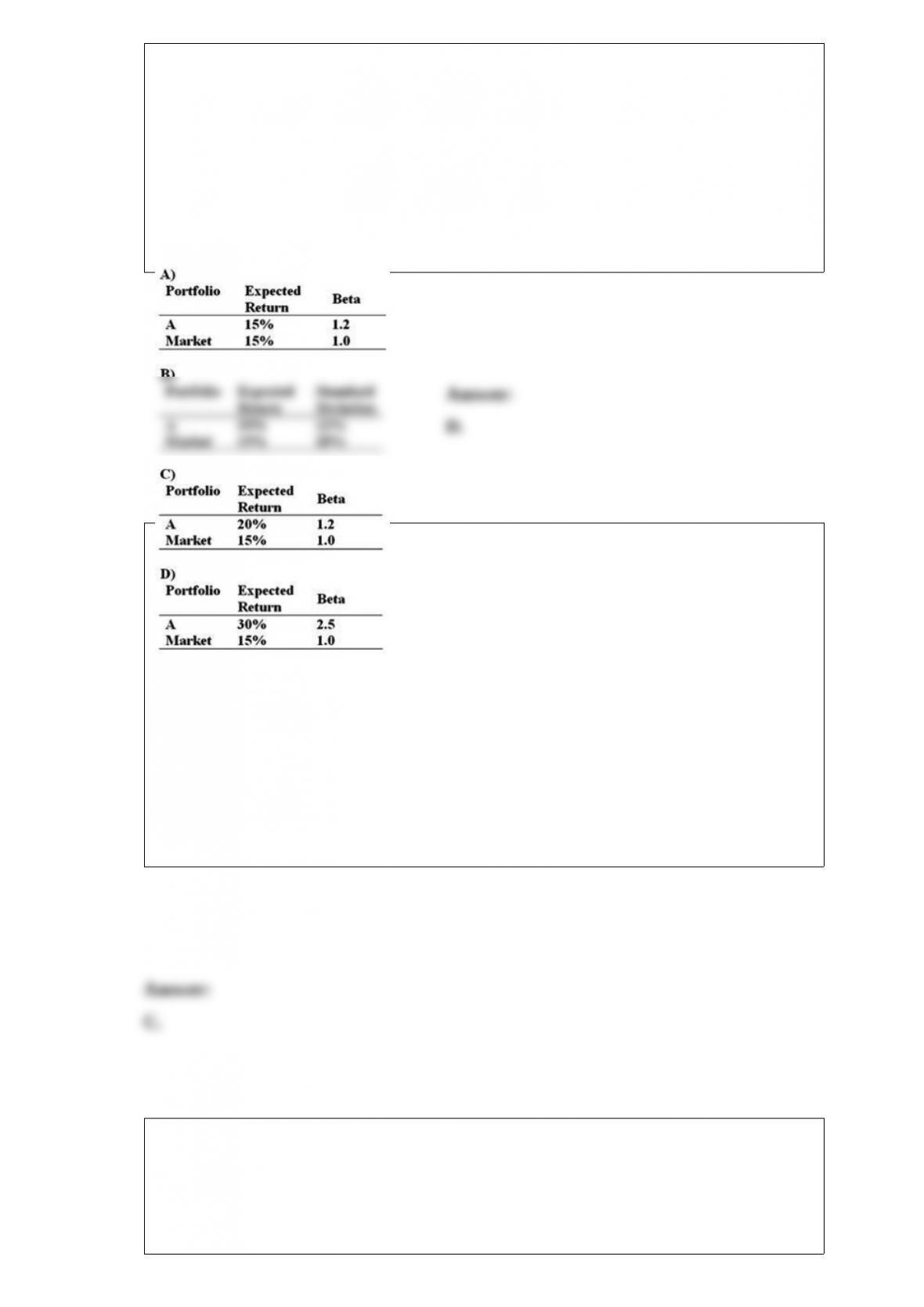

If the simple CAPM is valid and all portfolios are priced correctly, which of the

situations below is possible? Consider each situation independently, and assume the

risk-free rate is 5%.

A. Option A

B. Option B

C. Option C

D. Option D

Calculate the price of a European call option

using the Black Scholes model and the

following data: stock price = $56.80, exercise

price = $55, time to expiration = 15 days,

risk-free rate = 2.5%, standard deviation =

22%, dividend yield = 8%.

A. $1.49

B. $1.79

C. $2.04

D. $2.19

A family will retire in a few years. They have a high tax bracket and are concerned

about their after-tax rate of return. A meeting with their financial planner reveals that

they are primarily focused on safety of principal and will need a 6% to 8% average rate

of return on their portfolio. They desire a diversified portfolio, and liquidity is likely to

be a concern due to health reasons. Which of the following asset allocations seems to

best fit this family’s situation?

A. 10% money market; 50% intermediate-term bonds; 40% blue chip stocks, many with

high dividend yields

B. 0% money market; 60% intermediate-term bonds; 40% stocks

C. 10% money market; 30% intermediate-term bonds; 60% high-dividend-paying

stocks

D. 5% money market; 35% intermediate-term bonds; 60% stocks, most with low

dividends

A big increase in government spending is an example of a _________.

A. positive demand shock

B. positive supply shock

C. negative demand shock

D. negative supply shock

Just 2 months after you put money into an investment, its price falls 25%. Assuming

that none of the investment fundamentals have changed, which of the following actions

would evidence the greatest risk tolerance?

A. You sell to avoid further worry and buy something else.

B. You do nothing and wait for the investment to come back.

C. You buy more, thinking that if it was a good investment before, now it’s not only

good but cheap too.

D. You sue your financial adviser.

A speculator will often prefer to buy a futures contract rather than the underlying asset

because:

I. Gains in futures contracts can be larger due to leverage.

II. Transaction costs in futures are typically lower than those in spot markets.

III. Futures markets are often more liquid than the markets of the underlying

commodities.

A. I and II only

B. II and III only

C. I and III only

D. I, II, and III

Rose Hill Trading Company is expected to have EPS in the upcoming year of $8. The

expected ROE is 18%. An appropriate required return on the stock is 14%. If the firm

has a plowback ratio of 70%, its dividend in the upcoming year should be _________.

A. $1.12

B. $1.44

C. $2.40

D. $5.60

Security selection refers to _________.

A. choosing specific securities within each asset class

B. deciding how much to invest in each asset class

C. deciding how much to invest in the market portfolio versus the riskless asset

D. deciding how much to hedge

A convertible bond is deep in the money. This means the bond price will closely track

the __________.

A. straight debt value of the bond

B. conversion value of the bond

C. straight debt value of the bond minus the conversion value

D. straight debt value of the bond plus the conversion value

The capital asset pricing model was developed by _________.

A. Kenneth French

B. Stephen Ross

C. William Sharpe

D. Eugene Fama

If an investor does not diversify his portfolio and instead puts all of his money in one

stock, the appropriate measure of security risk for that investor is the ________.

A. stock’s standard deviation

B. variance of the market

C. stock’s beta

D. covariance with the market index

An order to buy or sell a security at the current price is a ______________.

A. limit order

B. market order

C. stop-loss order

D. stop-buy order

A portfolio generates an annual return of 13%, a beta of .7, and a standard deviation of

17%. The market index return is 14% and has a standard deviation of 21%. What is the

Treynor measure of the portfolio if the risk-free rate is 5%?

A. .1143

B. .1233

C. .1354

D. .1477

The correct measure of timing ability is ____________ for a portfolio manager who

correctly forecasts 55% of bull markets and 55% of bear markets.

A. -5%

B. 5%

C. 10%

D. 95%

Lifecycle Motorcycle Company is expected to pay a dividend in year 1 of $2, a

dividend in year 2 of $3, and a dividend in year 3 of $4. After year 3, dividends are

expected to grow at the rate of 7% per year. An appropriate required return for the stock

is 12%. Using the multistage DDM, the stock should be worth __________ today.

A. $63.80

B. $65.13

C. $67.95

D. $85.60

Currently, the Dow Jones Industrial Average is computed by _________.

A. adding the prices of 30 large “blue-chip” stocks and dividing by 30

B. calculating the total market value of the 30 firms in the index and dividing by 30

C. measuring the current total market value of the 30 stocks in the index relative to the

total value on the previous day

D. adding the prices of 30 large “blue-chip” stocks and dividing by a divisor adjusted

for stock splits and large stock dividends

Stock prices are _____ measures of firm value.

A. backward-looking

B. forward-looking

C. coincident

D. lagging

The NYSE Hybrid Market allows _____.

A. individuals to send orders directly to a specialist

B. individuals to send orders directly to an electronic system

C. brokers to send orders directly to a specialist

D. brokers to send orders either to an electronic system or to a specialist

TIPS offer investors inflation protection by ______________ by the inflation rate each

year.

A. increasing only the coupon rate

B. increasing only the par value

C. increasing both the par value and the coupon payment

D. increasing the promised yield to maturity

The U.S. income tax code is generally _____.

A. regressive

B. progressive

C. flat

D. peaked

Sharon decides to put $5,000 into her retirement plan at the age of 25. She will continue

to invest the same amount for a total of 6 years and then stop contributing. Assume 10%

annual return.

How much money will Sharon have in her retirement plan after 6 years?

A. $30,000

B. $35,575

C. $38,578

D. $41,451