1) nominal gdp measures a nation’s output in current year prices.

2) real gdp measures the change in the price level over time.

3) demand shocks may be positive or negative.

4) the ‘sticky price” model is the only one used by macroeconomists.

5) in the very short run, demand shocks will tend to change the level of output but have

little effect on prices.

6) china’s gdp per person in 2007 was a little more than one-tenth of u.s. gdp per person

in the same year.

7) the business cycle is primarily concerned with changes in the level of overall prices

over time.

8) a nation that realizes a 3 percent increase in its output per person is experiencing

modern economic growth.

9) higher unemployment rates are linked with higher crime rates and higher rates of

physical and mental illness.

10) if a farmer purchases 10 acres of farmland from a neighboring farmer, this would be

considered an economic investment.

11) economists believe that expectations have little impact on macroeconomic

outcomes.

12) output per person has grown steadily since the beginning of the roman empire.

13) according to a regression of gdp on market capitalization in 2010, virtually all

developed countries had _______ per capita gdp than (as) predicted by the regression.

a.higher

b.lower

c.the same

d.sometimes lower and sometimes higher

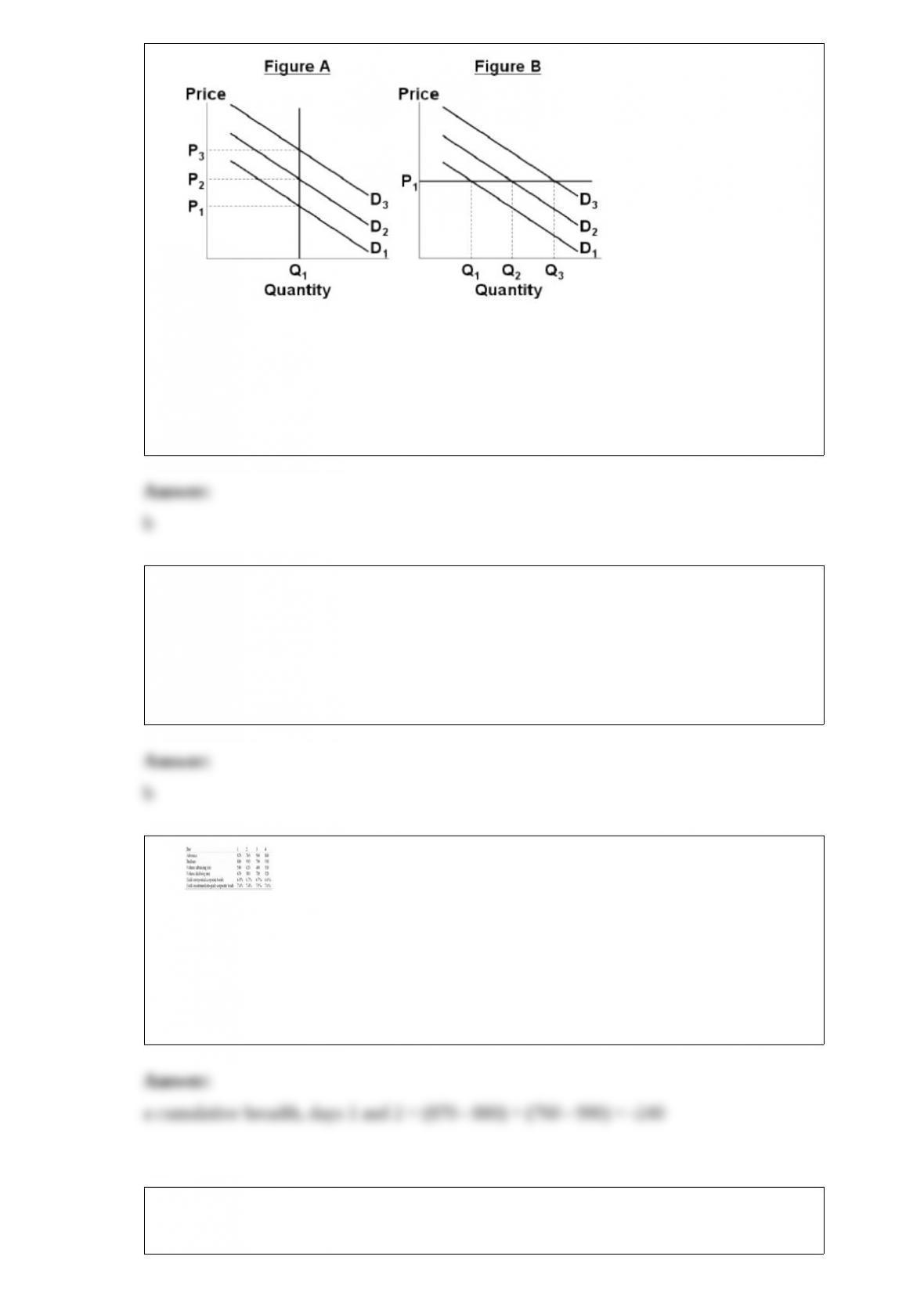

14)

refer to the above figures. which figure(s) represent a situation where firms are likely to

hold inventories to accommodate unexpected changes in demand?

a.a only.

b.b only.

c.both a and b.

d.neither a nor b.

15) decreasing the number of stocks in a portfolio from 50 to 10 would likely

________________.

a.increase the systematic risk of the portfolio

b.increase the unsystematic risk of the portfolio

c.increase the return of the portfolio

d.decrease the variation in returns the investor faces in any one year

16)

the cumulative breadth for the first 2 days is ___.

a.-240

b.-50

c.110

d.250

17) for a market timer, the _____________ will be higher when rm is higher.

a.portfolio’s alpha and beta

b.portfolio’s unsystematic risk

c.portfolio’s beta and slope of the characteristic line

d.security selection component of the portfolio

18) an investor buys $16,000 worth of a stock priced at $20 per share using 60% initial

margin. the broker charges 8% on the margin loan and requires a 35% maintenance

margin. the stock pays a $.50-per-share dividend in 1 year, and then the stock is sold at

$23 per share. what was the investor’s rate of return?

a.17.5%

b.19.67%

c.23.83%

d.25.75%

19) longer-term american-style options with maturities of up to 3 years are called

__________.

a.warrants

b.leaps

c.gics

d.cats

20) you believe that the spread between the september t-bond contract and the june

t-bond futures contract is too large and will soon correct. this market exhibits positive

cost of carry for all contracts. to take advantage of this, you should ______________.

a.buy the september contract and sell the june contract

b.sell the september contract and buy the june contract

c.sell the september contract and sell the june contract

d.buy the september contract and buy the june contract

21) if you want to know the portfolio standard deviation for a three-stock portfolio, you

will have to ______.

a.calculate two covariances and one trivariance

b.calculate only two covariances

c.calculate three covariances

d.average the variances of the individual stocks

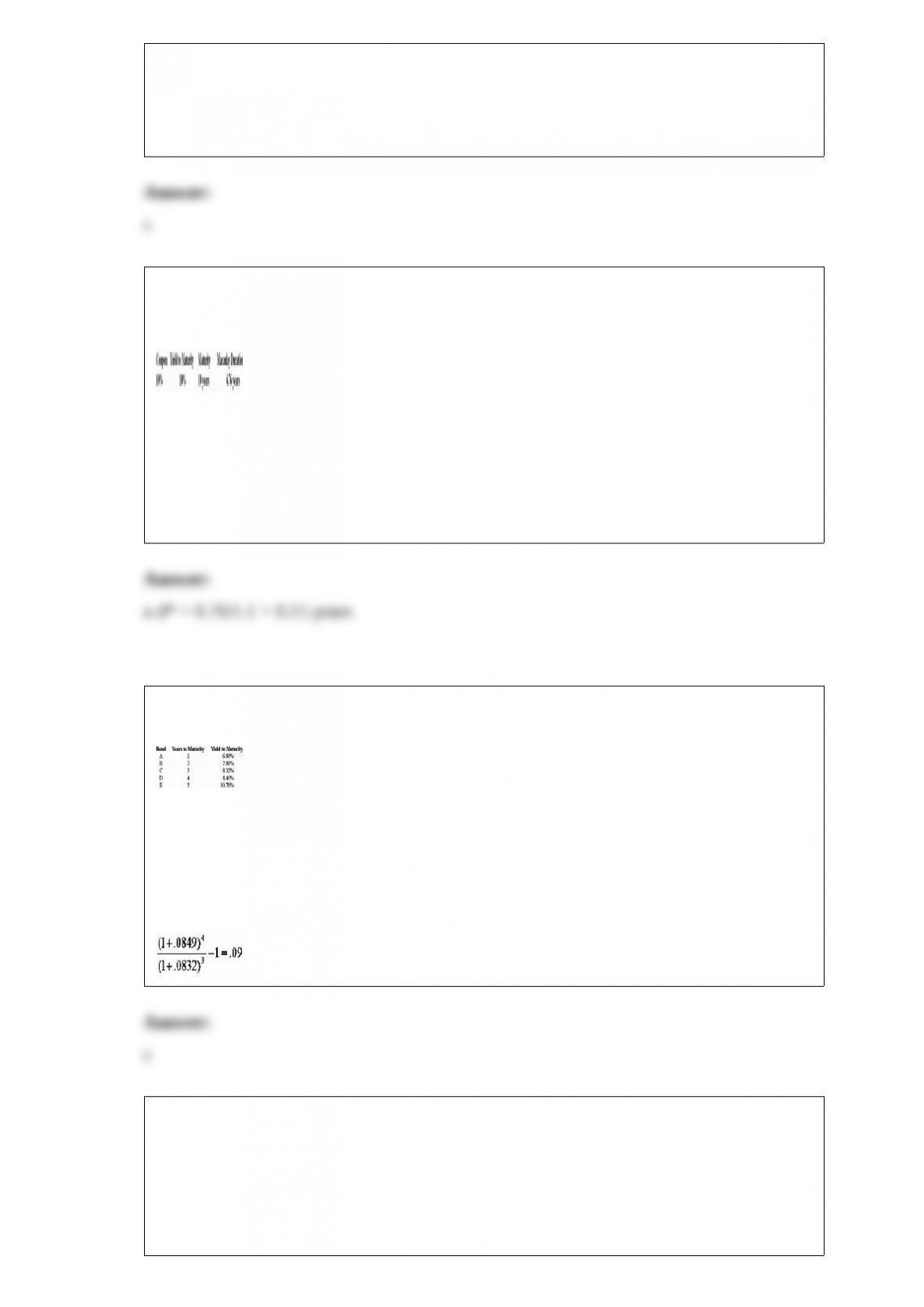

22) steel pier company has issued bonds that pay semiannually with the following

characteristics:

the modified duration for the steel pier bond is ______.

a.6.15 years

b.5.95 years

c.6.49 years

d.9.09 years

23) consider the following $1,000 par value zero-coupon bonds:

the expected 1-year interest rate 3 years from now should be _________.

a.7%

b.8%

c.9%

d.10%

24) a person in excellent health with a long life expectancy chooses a lifetime annuity.

this is an example of _________.

a.moral hazard

b.adverse selection

c.a texas hedge

d.actuarial error

25) in 2008 the largest corporate bankruptcy in u.s. history involved the investment

banking firm of ______.

a.goldman sachs

b.lehman brothers

c.morgan stanley

d.merrill lynch

26) (last word) many economists believe that the widespread use of computerized

inventory control systems:

a.has contributed to reduced severity in the business cycle.

b.will magnify recessions by triggering automatic reductions in output any time

inventories begin to accumulate.

c.has eliminated price stickiness.

d.will eventually prevent recessions from occurring.

27) a call option has an exercise price of $30 and a stock price of $34. if the call option

is trading for $5.25, what is the intrinsic value of the option?

a.$0

b.$1.25

c.$4

d.$5.25