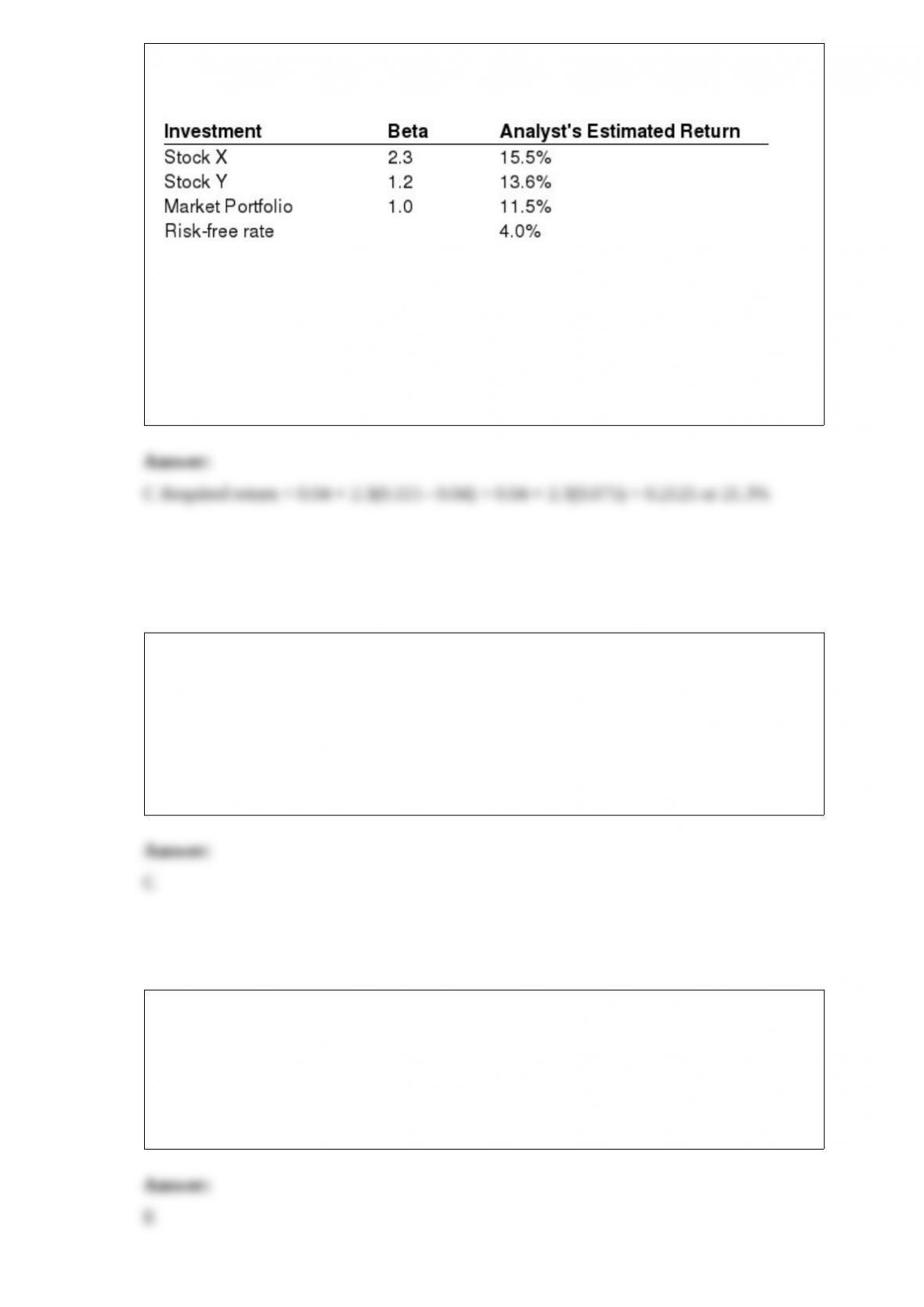

1) Exhibit 14.11

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

What is the required rate of return for Stock X based on the capital asset pricing model

(CAPM)?

a. 15.5%

b. 17.3%

c. 21.3%

d. 26.5%

e. 30.5%

2) The short interest ratio is the ratio between the number of shares sold short and not

covered, and the

a. Average number of stocks reaching new highs.

b. Average daily number of stocks that increased in value.

c. Average daily volume of trading on the exchange.

d. Average monthly volume of trading on the exchange.

e. Average number of shares outstanding in those stocks.

3) Options can be used to

a. Modify an equity portfolio’s systematic risk.

b. Modify an equity portfolio’s unsystematic risk.

c. Manage currency exposures in international equity portfolios.

d. Change a portfolio’s exposure to a particular asset

e. All of the above

4) Exhibit 11.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The National Motor Company’s last dividend was $1.25 and the directors expect to

maintain the historic 4 percent annual rate of growth. You plan to purchase the stock

today because you feel that the growth rate will increase to 7 percent for the next three

years and the stock will then reach $25.00 per share.

How much should you be willing to pay for the stock if you require a 16 percent return?

a. $17.34

b. $18.90

c. $19.09

d. $19.21

e. None of the above

5) An investor wishes to construct a portfolio consisting of a 70% allocation to a stock

index and a 30% allocation to a risk free asset. The return on the risk-free asset is 4.5%

and the expected return on the stock index is 12%. The standard deviation of returns on

the stock index is 6%. Calculate the expected standard deviation of the portfolio.

a. 4.20%

b. 25.20%

c. 3.29%

d. 10.80%

e. 5.02%

6) In the Grinblatt-Titman (GT) performance measure,

a. Portfolio performance is measured by assessing the quality of services provided by

money managers by looking at adjustments made to the content of their portfolios.

b. Portfolio performance is measured by examining both unsystematic and systematic

risk.

c. Portfolio performance is measured by comparing the returns of each stock in the

portfolio to the return of a benchmark portfolio. With the same aggregate investment

characteristics as the security in question.

d. Portfolio performance is measured on the basis of return per unit of risk.

e. Portfolio performance is measured on the basis of historic average differential return

per unit of historic variability of differential return.

7) A firm has a current price of $40 a share, an expected growth rate of 11 percent and

expected dividend per share (D1) of $2. Given its risk you have a required rate of return

for it of 12 percent. Assuming that you expect the stock price to increase to $42 during

the investment period, your expected rate of return and decision would be:

a. 10% – do not buy

b. 12% – do not buy

c. 14% – buy

d. 16% – buy

e. 18% – buy

8) The Ryan Treasury Index is an example of a

a.Bond market indicator series.

b.Stock market indicator series.

c.Composite security market series.

d.World market series.

e.Commodity market series.

9) The position of a bondholder that is long a callable bond is equal to being

a. Long a noncallable bond + long a call option on the bond.

b. Long a noncallable bond + short a call option on the bond.

c. Short a noncallable bond + long a call option on the bond.

d. Short a noncallable bond + short a call option on the bond.

e. None of the above.

10) A portfolio manager uses two different proxies for the market portfolio, the S&P

500 index and the

a. The size effect

b. The market effect

c. Measurement error

d. Benchmark error

e. Manager’s performance error

11) The entity that acts as the guarantor of each CBOE-traded contract is the

a. Federal government

b. Securities and exchange commission

c. CBOE

d. Options clearing corporation

e. Federal reserve bank

12) If the yield to maturity for a par value TIPS bond with 8 years to maturity is 3%,

and the yield to maturity of a U.S Treasury note with 8 years is 4.25%, this implies that

a. The expected annual rate of inflation over the next 8 years is -1.25%.

b. The expected annual rate of inflation over the next 8 years is 1.25%.

c. The expected annual rate of inflation over the next 8 years is -2.25%

d. The expected annual rate of inflation over the next 8 years is 2.25%

e. None of the above.

13) Secondary markets are important because

a.The prevailing market price of securities is determined in the secondary market

b.It has an impact on price stability

c.It has an impact on price continuity

d.All of the above

e.None of the above

14) Derivative securities can be used

a. By investors in the same way as the underlying security

b. To modify the risk and expected return characteristics of existing investment

portfolios

c. To duplicate cash flow patterns for arbitrage opportunities

d. All of the above

e. None of the above

15) A narrowing of the T-bill-Eurodollar and ____ signal, because ____.

a. Bearish, it signals falling investor confidence

b. Bullish, it signal rising investor confidence

c. Bearish, it signals a flight to quality

d. Bullish, it signals a flight to quality

e. b and d

16) When a bond issue is secured by a legal claim on equipment it is known as a(n)

a. Junior bond.

b. Income bond.

c. Bearer bond.

d. Trust certificate.

e. Perpetuity.

17) Exhibit 22.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

A stock currently trades for $130 per share. Options on the stock are available with a

strike price of $125. The options expire in 10 days. The risk free rate is 3% over this

time period, and the expected volatility is 0.35.

Calculate the price of the put option.

a. $1.086

b. $0.862

c. $6.234

d. $0.623

e. $2.317

18) A statistic that measures how two variables tend to move together is the

a.Coefficient of variation

b.Correlation coefficient

c.Standard deviation

d.Mean

e.Variance

19) In a two stock portfolio, if the correlation coefficient between two stocks were to

decrease over time, everything else remaining constant, the portfolio’s risk would

a. Decrease.

b. Remain constant.

c. Increase.

d. Fluctuate positively and negatively.

e. Be a negative value.

20) The fundamental determinants of interest rates are the real risk free rate, inflation,

and the risk premium.

21) According to the segmented market hypothesis, yields for a particular maturity

segment depend on supply and demand within the maturity segment.

22) The typical proxy for the market portfolio is the S&P 500 Index because it is

diversified and price weighted.

23) Style identification allows an investor to select investment managers that allow his

overall portfolio to be properly diversified.

24) A market where prices adjust rapidly to new information is considered to be

internally efficient.

25) Forward contracts are traded over-the-counter and are generally not standardized.

26) Credit analysis and core-plus management are examples of active bond portfolio

management.

27) The cost-of-carry model is useful for pricing future contracts.

28) A value weighted index automatically adjusts for stock splits.

29) Super DOT is an electronic order-routing system through which member firms can

transmit market and limit orders directly to the posts where the securities are traded.