1) on the basis of regression equation we can decompose the variability

of the dollar value of the asset, var(p), into two separate components var(p) = b2 var(s)

+ var(e).

the first term in the right-hand side of the equation, b2 var(s) represents.

a.the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate

b.captures the residual part of the dollar value variability that is independent of

exchange rate movements

c.none of the above

2) a recent survey of u.s. foreign exchange traders measured traders perceptions about

how fast news events that cause movements in exchange rates actually change the

exchange rate. the survey respondents claim that the bulk of the adjustment to economic

announcements regarding unemployment, trade deficits, inflation, gdp, and the federal

funds rate takes place within

a.ten seconds

b.one minute

c.five minutes

d.one hour

3) find the debt-to-equity ratio for a firm with a debt-to-total-value ratio of .

a.1

b.2

c.3

d.4

e.5

4) suppose that the one-year interest rate is 5.0 percent in the united states and 3.5

percent in germany, and that the spot exchange rate is $1.12/ and the one-year forward

exchange rate, is $1.16/. assume that an arbitrageur can borrow up to $1,000,000.

a.this is an example where interest rate parity holds

b.this is an example of an arbitrage opportunity; interest rate parity does not hold

c.this is an example of a purchasing power parity violation and an arbitrage opportunity

d.none of the above

5) a cfo should be least worried about

a.transaction exposure

b.translation exposure

c.economic exposure

d.none of the above

6) the payment amount under this fra is

a.$9,985

b.$10,111

c.$60,667

d.$120,000

7) bema gold is an exploration and production company that trades on the toronto stock

exchange. assume that when purchased by an international investor the stock’s price and

the exchange rate were cad5 and cad1.0/usd0.72 respectively. at selling time, one year

after the purchase date, they were cad6 and cad1.0/usd1.0. calculate the investor’s

annual percentage rate of return in terms of the u.s. dollars.

a.-13.60%

b.66.67%

c.38.89%

d.28.00%

8) you will get more diversification

a.across industries than across countries

b.across countries than across industries

c.across stocks and bonds than across countries

d.none of the above

9) generally speaking, any transaction that results in a receipt from foreigners

a.will be recorded as a debit, with a negative sign, in the u.s. balance of payments

b.will be recorded as a debit, with a positive sign, in the u.s. balance of payments

c.will be recorded as a credit, with a negative sign, in the u.s. balance of payments

d.will be recorded as a credit, with a positive sign, in the u.s. balance of payments

10) in what year were u.s. mncs mandated to implement fasb 52?

a.1952

b.1962

c.1972

d.1982

11) empirical tests of the black-scholes option pricing formula

a.shows that binomial option pricing is used widely in practice, especially by

international banks in trading otc options

b.works well for pricing american currency options that are at-the-money or

out-of-the-money

c.does not do well in pricing in-the-money calls and puts

d.both b and c

12) prior to the 1870s, both gold and silver were used as international means of

payment and the exchange rates among currencies were determined by either their gold

or silver contents. suppose that the dollar was pegged to gold at $30 per ounce, the

french franc is pegged to gold at 90 francs per ounce and to silver at 9 francs per ounce

of silver, and the german mark pegged to silver at 1 mark per ounce of silver. what

would the exchange rate between the u.s. dollar and german mark be under this system?

a.1 german mark = $2

b.1 german mark = $0.50

c.1 german mark = $3

d.1 german mark = $1

13) find the debt-to-value ratio for a firm with a debt-to-equity ratio of 2.

a.

b.

c.3/5

d.

e.5/7

14) suppose that the current exchange rate is 0.80 = $1.00. the direct quote, from the

u.s. perspective is

a.1.00 = $1.25

b.0.80 = $1.00

c.£1.00 = $1.80

d.none of the above

15) the bretton woods system ended in

a.1945

b.1973

c.1981

d.2001

16) when a currency trades at a discount in the forward market

a.the forward rate is less than the spot rate

b.the forward rate is more than the spot rate

c.the forward exchange rate is less than one dollar (e.g. 1.00 = $0.928)

d.the exchange rate is less than it was yesterday

17) when using the current/noncurrent method, current assets are defined as

a.inventory that is currently salable

b.assets with a maturity of one year or less

c.assets with a maturity of 90 days or less

d.none of the above

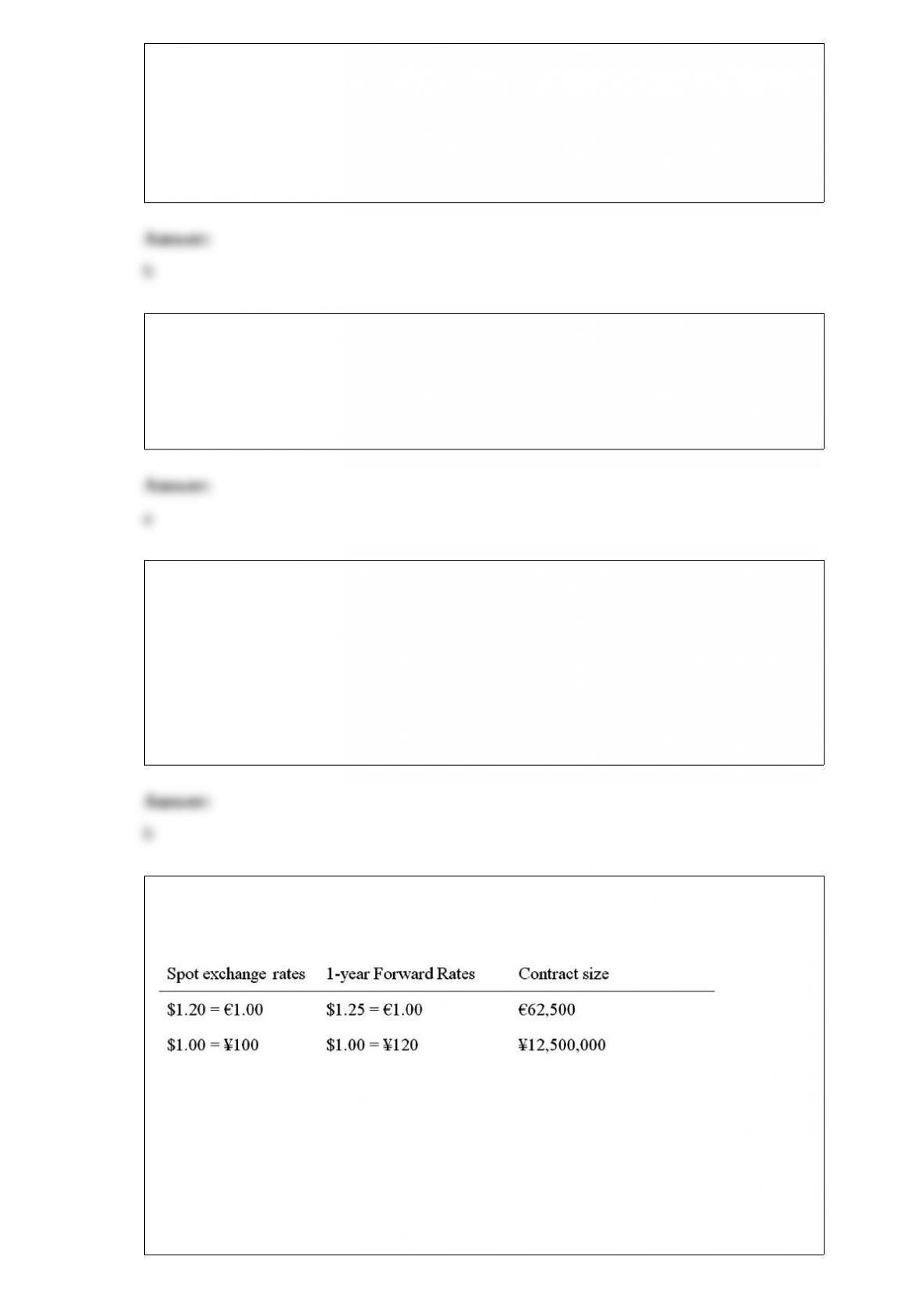

18) a japanese exporter has a 1,000,000 receivable due in one year. spot and forward

exchange rate data is given in the table:

the one-year risk free rates are i$ = 4.03%; i = 6.05%; and i¥ = 1%. detail a strategy

using forward contracts that will hedge exchange rate risk.

a.borrow 970,873.79 today; in one year you owe 1m, which will be financed with the

receivable. convert 970,873.79 to dollars at spot, receive $1,165,048.54. convert dollars

to yen at spot, receive ¥116,504,854

b.sell 1m forward using 16 contracts at the forward rate of $1.20 per 1. buy

¥150,000,000 forward using 11.52 contracts, at the forward rate of $1.00 = ¥120

c.sell 1m forward using 16 contracts at the forward rate of $1.25 per 1. buy

¥150,000,000 forward using 12 contracts, at the forward rate of $1.00 = ¥120

d.none of the above