Which of the following statements is TRUE?A. An increase in interest rates will

benefit the FI since the increase in the market value of assets will be greater than the

increase in the market value of liabilities.

B. An increase in interest rates will harm the FI since the increase in the market value

of assets will be greater than the increase in the market value of liabilities.

C. An increase in interest rates will harm the FI since the decrease in the market value

of assets will be greater than the decrease in the market value of liabilities.

D. A decrease in interest rates will harm the FI since the increase in the market value of

assets will be greater than the increase in the market value of liabilities.

E. A decrease in interest rates will benefit the FI since the increase in the market value

of assets will be smaller than the increase in the market value of liabilities.

Answer:

Which of the following is TRUE concerning loans sold with recourse?A. Most loans

are sold with recourse.

B. The buyer cannot put the loan back to the selling FI.

C. The FI has no explicit liability if the loan eventually goes bad.

D. The FI that originated the loan retains a contingent credit risk liability.

E. The loan sale is technically removed from the balance sheet.

Answer:

Once a fixed-floating interest rate swap agreement has been negotiated under

no-arbitrage conditions, both parties to the swap agreement know with certainty the

exact amount of their respective cash flows.

Answer:

FIs typically provide secondary claims to household savers that have inferior liquidity

than primary securities of corporations such as equity and bonds.

Answer:

Which of the following is TRUE of secondary securities?A. They include equities,

bonds, and other debt claims.

B. They are backed by the real assets of corporations issuing them.

C. They are securities that back primary securities.

D. They are securities issued by FIs.

E. They must be placed in a separate account on order for primary securities to be

offered.

Answer:

The Fed now charges 20 basis points annually for daylight overdrafts.

Answer:

Negotiable certificates of deposits are differentiated from fixed time deposits by their

negotiability and active trading in the secondary markets.

Answer:

Macrohedging uses a derivative contract, such as a futures or forward contract, to hedge

a particular asset or liability risk.

Answer:

Commercial banks and finance companies have traditionally served the needs of the

residential real estate market.

Answer:

Loan loss ratio models are based on historical loan loss ratios of specific sectors relative

to the historic loan loss ratios of the FI’s entire loan portfolio.

Answer:

In an attempt to enhance the net social welfare benefits of the services provided by

financial intermediaries, safety and soundness regulation requires a DI to hold a

minimum level of cash reserves against deposits.

Answer:

It is impossible for money market mutual fund share prices to fall below $1.00.

Answer:

Due to a recent increase in demand for new insurance products, the number of life

insurance companies as been increasing in the United States.

Answer:

The purpose of the Foreign Bank Supervision Enhancement Act of 1991 was to extend

federal authority over foreign banking organizations in the U.S.

Answer:

Immunizing the balance sheet of an FI against interest rate risk requires that the

leverage adjusted duration gap (DA-kDL) should be set to zero.

Answer:

Although they are subject to reserve requirements, many DIs have begun to issue

medium-term notes because they are a stable source of funds.

Answer:

A positive net exposure position in FX implies an FI has purchased more foreign

currency than it has sold.

Answer:

Unlike GNMA, FNMA will securitize conventional mortgages issued by depository

institutions.

Answer:

Under Basel III, Tier I capital measures the market value of common equity plus the

amount of perpetual preferred stock plus minority equity interest held by the bank in

subsidiaries minus goodwill.

Answer:

Although financial markets deteriorated during the summer of 2009, by September of

that year the banking system had returned to normal operation.

Answer:

When interest rates increase, banks are more likely to be forced to increase

rate-sensitive liabilities to replace decreased balances in demand deposits and savings

accounts.

Answer:

Commercial banks, investment banks, and broker-dealers are the major forward market

participants.

Answer:

Mutual funds are prohibited from purchasing/participating in the FI loan sales market

by the SEC.

Answer:

Which of the following is TRUE?A. Investment bankers earn fees based on the success

of their placements when they underwrite using a best-efforts basis.

B. Investment bankers earn fees based on the success of their placement when they

underwrite using firm-commitment basis.

C. With best-efforts underwriting, investment bankers act as principals because they

purchase securities from the issuer and sell them at a higher price.

D. An investment banker is acting as an agent when conducting a firm-commitment

offering of securities.

E. Answers B and C only.

Answer:

Sometimes banks received criticism because domestic governments take special

political steps to reduce the probability that foreign borrowers will default or repudiate

their debt contracts, an occurrence that could cause financial harm to the domestic

banks.

Answer:

Recessionary phases in the business cycle typically cause greater hardship on

companies that borrow large amounts.

Answer:

Active trading of assets and liabilities creates market risk.

Answer:

Regulators tend to discourage, and even prohibit in some cases, FIs from writing

options because the upside potential is unlimited and the downside losses are

potentially limited.

Answer:

NOW accounts allow the explicit payment of interest.

Answer:

U.S. financial institutions have expanded abroad in recent years, although their foreign

counterparts have been prohibited from expanding into the U.S.

Answer:

The aggregate commitment funding risk can increase the cost of funds above normal

levels.

Answer:

As of 2010, the Department of Housing and Urban Development (HUD) no longer sells

loans that were used to purchase multifamily apartment properties.

Answer:

The standardization of many FI products is evidence of the inefficient

institutionalization by financial markets and the mechanisms through which these

products trade.

Answer:

The primary objective of the 1927 McFadden Act was to restrict interstate bank

branching.

Answer:

Sun Bank has issued a one-year $5 million loan commitment to a customer for an

up-front fee of 15 basis points and at a fixed rate of 12 percent. The back-end fee for the

unused portion of the commitment is 5 basis points. The bank requires a 10 percent

compensating balance in demand deposits. Reserve requirements on demand deposits

are 10 percent.

What is expected return on the loan to the bank if 50 percent of the loan is drawn? Do

not take future values of fee or interest income received. A. 13.45 percent.

B. 13.57 percent.

C. 13.60 percent.

D. 13.72 percent.

E. 13.90 percent.

Answer:

A person with a history of bad credit and an inconsistent record of payments on other

debt is most likely to find a short-term loan through a A. commercial bank.

B. personal credit institution.

C. savings bank.

D. sales finance institution.

E. payday lender.

Answer:

Banks often convert on-balance-sheet bankers acceptances into off-balance-sheet letters

of credit for the purpose of minimizing total assets and thus improving performance

ratios such as ROA.

Answer:

Which of the following is an outcome of an increase in the reserve requirement ratio?

A. DIs may hold fewer reserves against their transaction accounts.

B. DIs are able to lend out a greater percentage of their deposits.

C. Increased credit availability in the economy.

D. DIs are only able to lend a smaller percentage of their deposits than before.

E. A multiplier effect on the supply of DI deposits and thus the money supply.

Answer:

What is the FI’s leverage-adjusted duration gap? A. 0.91 years.

B. 0.83 years.

C. 0.73 years.

D. 0.50 years.

E. 0 years.

Answer:

The mean change in the value of a portfolio of trading assets has been estimated to be 0

with a standard deviation of 20 percent. Yield changes are assumed to be normally

distributed.

What is the maximum yield change expected if a 90 percent confidence (one-tailed)

limit is used? A. 3.30%.

B. 20.0%.

C. 33.0%.

D. 39.2%.

E. 46.6%.

Answer:

Which of the following is NOT a criticism of the Basel I risk-based capital ratio? A. All

commercial loans are given equal weight regardless of the credit risk of the borrower.

B. The ratio incorporates off-balance-sheet risk exposures.

C. Grouping assets into different risk categories may encourage balance sheet asset

allocation games.

D. The treatment does not include interest rate or foreign exchange risk.

E. The weights in the four risk categories imply a cardinal measurement of relevant

risk between each category.

Answer:

A bank’s net deposit drain A. is negative if deposits exceed withdrawals.

B. is positive if deposits exceed withdrawals.

C. decreases during holiday and vacation periods.

D. in unaffected by holiday and vacation periods.

E. fluctuates unpredictably on any given day.

Answer:

Which of the following is NOT characteristic of the real estate portfolio for most

banks? A. Commercial real estate mortgages have been the fastest growing component

of real estate loans.

B. Adjustable rate mortgages have rates that are periodically adjusted to some index.

C. Borrowers prefer fixed-rate loans to ARMs during periods of high interest rates.

D. Residential mortgages are the largest component of the real estate loan portfolio.

E. The proportion of ARMs to fixed-rate mortgages can vary considerably over the rate

cycle.

Answer:

What are the possible ways that the bank can meet an expected net deposit drain of +4

percent using purchased liquidity management techniques?A. Utilize further the Fed

funds market.

B. Utilize repurchase agreements.

C. Liquidate all cash holdings.

D. All of the above.

E. Answers A and B only.

Answer:

What refers to the risk that the borrower is unable or unwilling to fulfill the terms

promised under the loan contract? A. Liquidity risk.

B. Interest rate risk.

C. Sovereign risk.

D. Default risk.

E. Solvency risk.

Answer:

As of 2011, approximately ________ of the industry total brokerage fee income was

generated by firms operating as subsidiaries of commercial bank holding companies.

A. $12.1 billion

B. $8.6 billion

C. $16.5 billion

D. $32.4 billion

E. $40.3 billion

Answer:

The future viability of the savings association industry in traditional mortgage lending

has been questioned because of A. securitization practices of other FIs.

B. the additional risk exposure of long-term mortgage lending.

C. intense competition from other FIs.

D. the liquidity risks associated with mortgage lending.

E. All of the above.

Answer:

Consider a situation where the duration of the fixed portion of a swap is greater than the

floating portion of a swap. Which of the following statements is most correct?A. The

fixed-rate payers gain when rates fall.

B. The market value of fixed-rate payments will decrease by more than the market

value of floating-rate payments when interest rates fall.

C. The market value of fixed-rate payments will decrease by more than the market

value of floating-rate payments when interest rates rise.

D. The floating-rate payers gain when rates rise.

E. The market value of the swap will increase with an increase in interest rates.

Answer:

The two policy categories offered by property-casualty insurers that are most likely to

be subject to rate regulation are A. auto insurance and worker’s compensation.

B. homeowner multiple peril and commercial multiple peril.

C. earthquake and flood.

D. surety bonds and financial guaranty.

E. product liability and farm owner multiple peril.

Answer:

The management of pools of assets by securities firms is considered to be the function

of A. market making.

B. investment banking.

C. trading.

D. investing.

E. cash management.

Answer:

The repricing model is based on an accounting world that reports asset and liability

values atA. their market value.

B. their book value.

C. their historic values or costs.

D. All of the above.

E. Answers B and C only.

Answer:

Credit scoring models include all of the following broad types of models EXCEPT A.

Linear discriminant models.

B. Linear probability models.

C. Term structure models.

D. Logit models.

E. None of the above.

Answer:

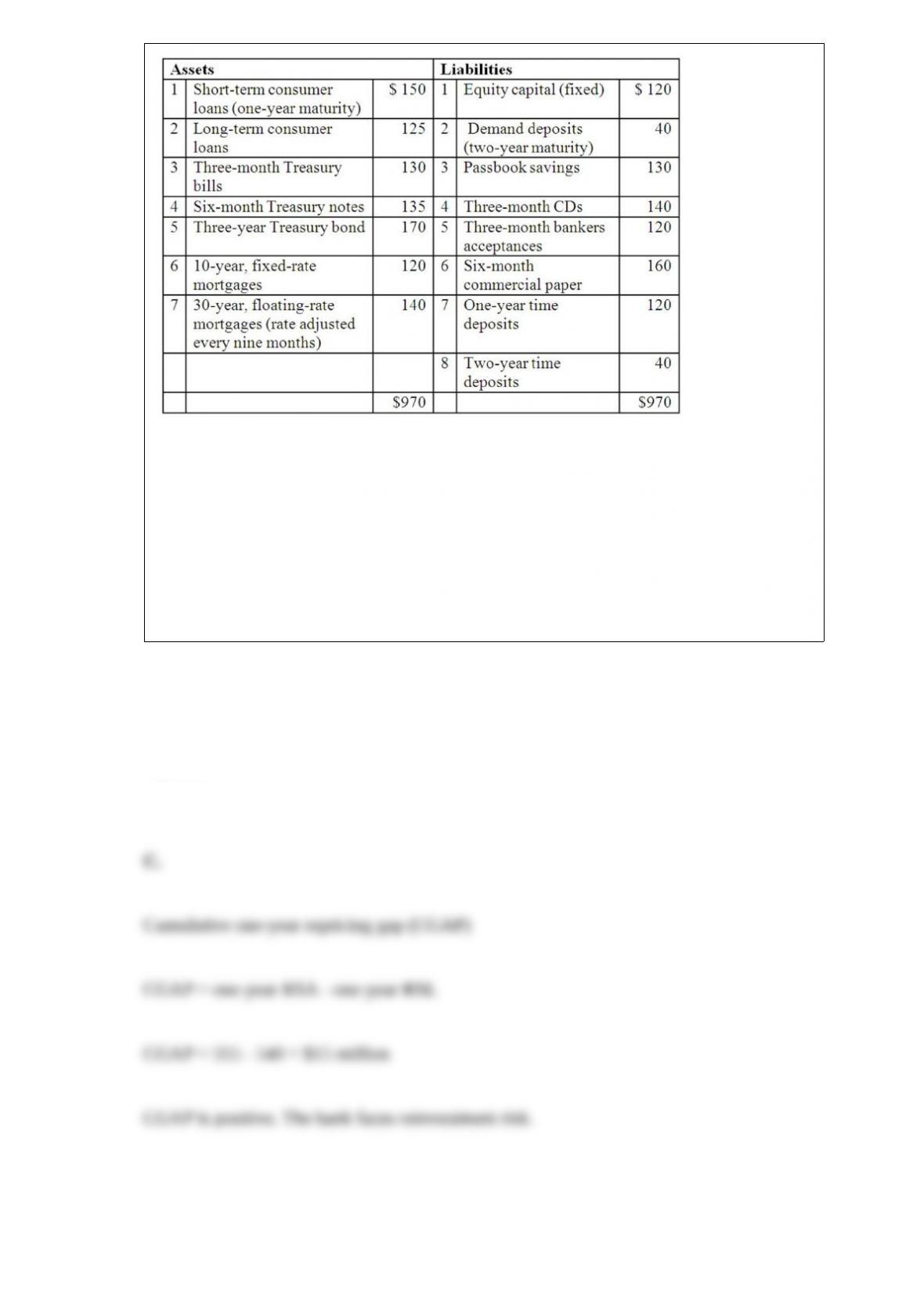

The balance sheet of XYZ Bank appears below. All figures in millions of US Dollars.

The cumulative

one-year repricing gap (CGAP) for the bank is A. $25 million.

B. $-140 million.

C. $15 million.

D. $-150 million.

E. $-15 million.

Answer:

Which practice is especially common in international funds as traders can exploit

differences in time zones? A. Directed brokerage.

B. Insider trading.

C. Late trading.

D. Market timing.

E. Spinning.

Answer:

In the Moody’s Analytics portfolio model, the expected loss on a loan is A. the product

of the estimated loss given default and risk-free rate on a security of equivalent

maturity.

B. annual all-in-spread minus the loss given default.

C. annual all-in-spread minus the expected default frequency.

D. the product of the expected default frequency and the estimated loss given default.

E. the volatility of the loan’s default rate around its expected value.

Answer:

A consumer lending function is performed by each of the following FIs EXCEPT A.

mutual funds.

B. finance companies.

C. pension funds.

D. depository institutions.

E. insurance companies.

Answer:

In the derivatives markets, transactions costs are highest for A. options.

B. futures.

C. forwards.

D. swaps.

E. currencies.

Answer:

An underwriter is quoting the following rates for the issue of new securities on behalf

of a firm on a firm commitment basis: $64.00-64.25. 2,000,000 shares are being

offered. A. The maximum amount that can be earned by the underwriter (ignoring other

costs) $1,000,000.

B. The maximum amount that can be earned by the underwriter (ignoring other costs)

is $500,000.

C. The minimum amount that can be earned (ignoring other costs) by the underwriter is

$0.

D. The minimum amount that can be earned (ignoring other costs) by the underwriter is

-$500,000.

E. The minimum amount that can be earned (ignoring other costs) by the underwriter is

-$1,000,000.

Answer:

The earnings at risk for an FI is a function of A. the time necessary to liquidate assets.

B. the potential adverse move in yield.

C. the dollar market value of the position.

D. the price sensitivity of the position.

E. All of the above.

Answer:

If Bank C agrees to be purchased by Banks A and B, what proportion of assets of Bank

C should be taken by Banks A and B, respectively in order to have equal post-merger

assets?A. 52 percent and 48 percent.

B. 50 percent and 40 percent.

C. 56 percent and 44 percent.

D. 40 percent and 50 percent.

E. 45 percent and 55 percent.

Answer:

The expenses relating to increased technological improvements made by FIs during the

last several years has the most impact on which of the following? A. Interest expense.

B. Noninterest expense.

C. Net income.

D. Provision for loan losses.

E. Net securities gains or losses

Answer:

The number of funds and assets size of the mutual fund industry have grown

dramatically since 1970 because of the introduction of A. money market mutual funds

in 1972.

B. tax-exempt money market mutual funds in 1979.

C. special-purpose equity, bond, and derivative funds.

D. 401-k retirement plans sponsored by employers.

E. All of the above.

Answer:

What is the drawback of deposit insurance facility? A. Even when the DI is in trouble,

the deposit holder has no incentive to run.

B. DIs are more likely to increase the liquidity risk on their balance sheets.

C. Deposit holder’s place in line affects his or her ability to obtain their funds.

D. Deposit insurance does not deter contagious runs and panics.

E. Deposit holders are less likely to panic if there is a perceived bank solvency

problem.

Answer:

What is the expected shortfall (ES) of securities Alpha and Beta at the 99 percent

confidence level, respectively (in millions)? A. -$300 and -$3,300

B. -$3 and -$24.75

C. -$3 and -$25.50

D. -$300 and -$300

E. -$ and -$0.75.

Answer:

One method that may be employed by banks to lower required reserves is to A. transfer

deposits offshore on Friday and to transfer them back on Monday.

B. convert demand deposits into MMDA accounts on Friday and reverse the transfer

the following Monday.

C. rely more heavily on zero explicit interest-rate deposits.

D. delay posting deposits made on Friday until the following Monday.

E. do nothing, because reserve requirements cannot be avoided.

Answer:

What is the benefit of a regulatory guarantee or insurance program for liability holders

of FIs? A. It decreases the likelihood contagious runs.

B. It increases concerns about the asset quality of FI.

C. It increases concerns about solvency of an FI.

D. It provides incentives to liability holders to engage in runs.

E. It provides preference to those who are first in line to withdraw funds over those last

in line.

Answer:

What is the ratio of capital to risk-adjusted assets, if the bank has capital of $50

million?A. 5.00 percent.

B. 5.56 percent.

C. 6.94 percent.

D. 8.33 percent.

E. 6.25 percent.

Answer:

Answer:

Use the following two choices to identify whether each intermediary or entity is a net

buyer or net seller of credit derivative securities.

a. Net buyer (typically)

b. Net seller (typically)

Banks

Answer:

Answer:

Answer:

Answer: