1) consider bank that has entered into a five-year swap on a notational balance of

$10,000,000 with a corporate customer who has agreed to pay a fixed payment of 10

percent in exchange for libor. as of the fourth reset date, determine the price of the swap

from the bank’s point of view assuming that the fixed-rate side of the swap has

increased to 11 percent. libor is at 5 percent.

a.$909,090.91 gain

b.$90,090.09 loss

c.no loss or no gain since maturity has not arrived

d.$90,090.09 gain

2) ‘samurai” bonds are

a.dollar-denominated foreign bonds originally sold to u.s. investors

b.yen-denominated foreign bonds originally sold in japan

c.pound sterling-denominated foreign bonds originally sold in the u.k

d.none of the above

3) a mnc seeking to reduce transaction exposure with a strategy of leading and lagging

a.can probably employ the strategy more effectively with intra firm payables and

receivables than with customers or outside suppliers

b.can employ the strategy most easily with customers, regardless of market structure

c.can employ the strategy most easily with suppliers, regardless of market structure

d.none of the above

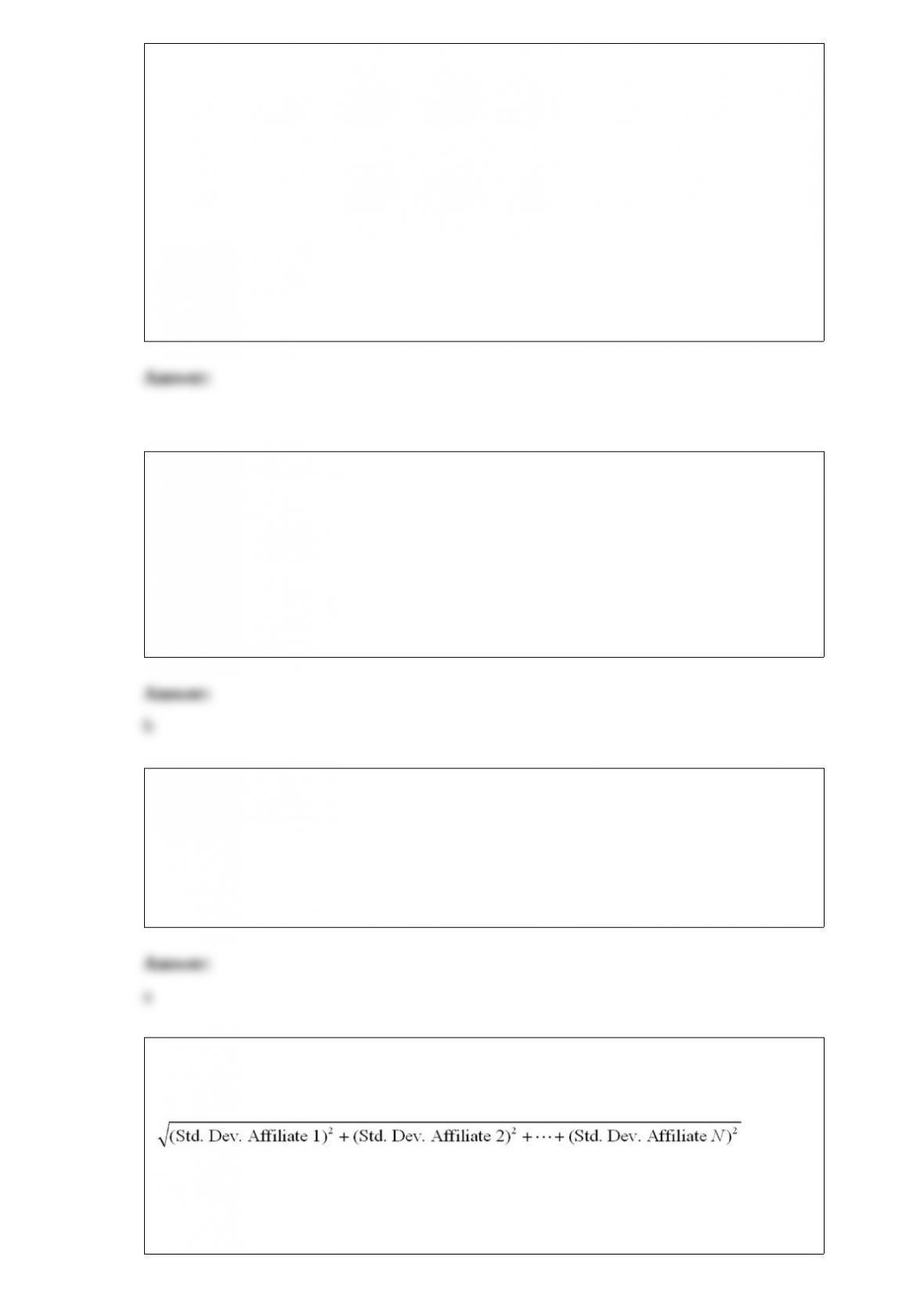

4) the formula for the standard deviation of cash held by the centralized depository for n

affiliates is

a.the formula assumes that interaffiliate cash flows have a correlation coefficient of -1

b.the formula assumes that interaffiliate cash flows have a correlation coefficient of +1

c.the formula assumes that interaffiliate cash flows have a correlation coefficient of 0

d.none of the above

5) consider a u.s.-based mnc with a wholly-owned german subsidiary. following a

depreciation of the dollar against the euro, which of the following describes the

conversion effect of the depreciation?

a.the cash flow in euro could be altered due a change in the firm’s competitive position

in the marketplace

b.a given operating cash flow in euro will be translated to a higher u.s. dollar cash flow

c.both a and b

d.none of the above

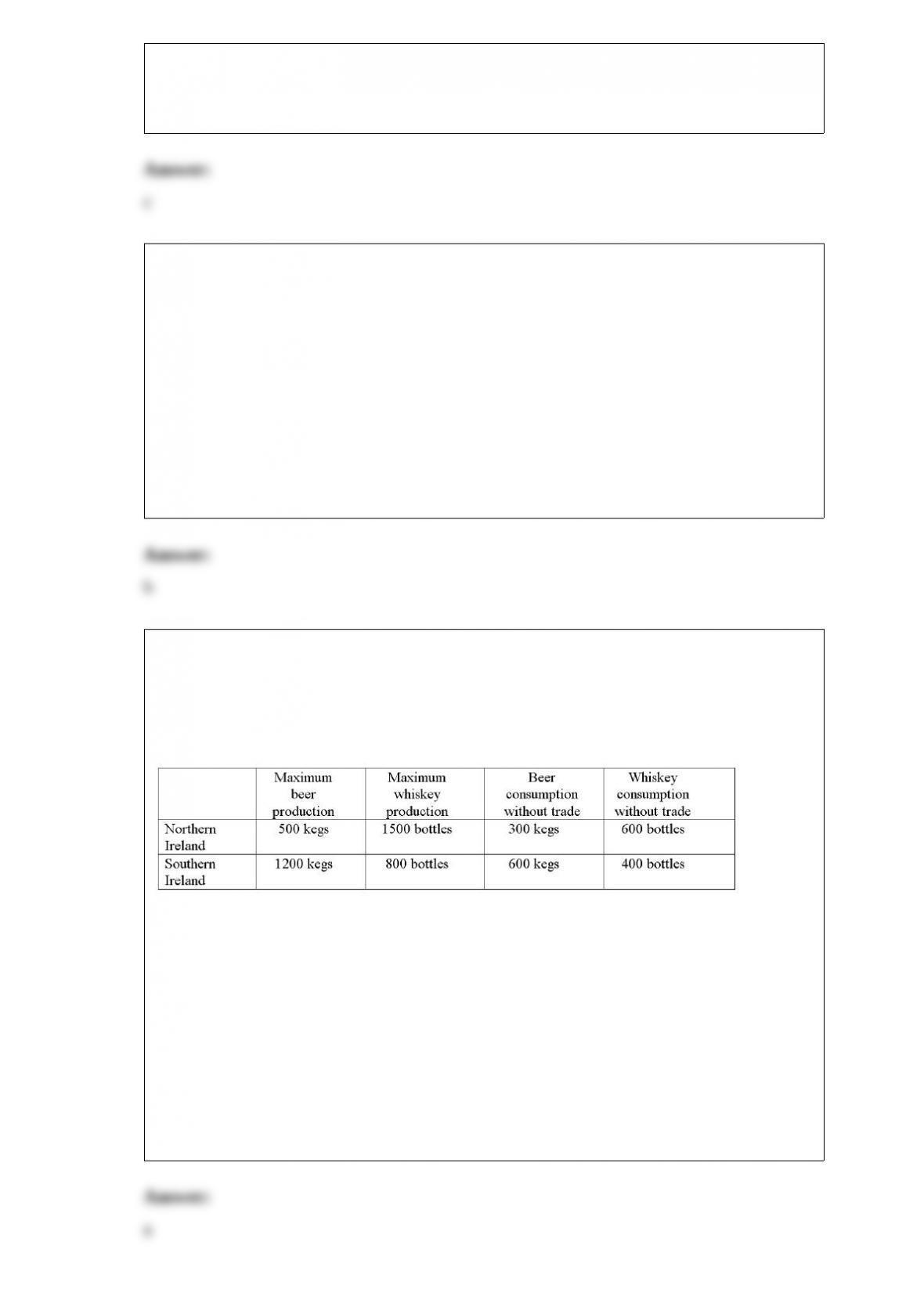

6) the first two columns give the maximum daily amounts of beer and whiskey that

southern ireland and northern ireland can produce when they completely specialize in

one or other product. the last two columns give each country’s consumption without

trade.

if the international price of beer is one keg of beer = 1 bottle of whiskey, how much

whiskey will northern ireland consume? each country completely specializes and 500

kegs of beer are traded for 500 bottles of whiskey.

a.1,000 bottles

b.1,200 bottles

c.500 bottles

d.600 bottles

7) in the wholesale money market, denominations

a.are at least $10,000, but sizes of $100,000 or larger are more typical

b.are at least $100,000, but sizes of $500,000 or larger are more typical

c.are at least $500,000, but sizes of $1,000,000 or larger are more typical

d.none of the above

8) in modern times, it is not a country per se but rather a controller of capital and

know-how that gives the country in which it is domiciled a comparative advantage over

another country. these controllers of capital and technology are

a.the state

b.the multinational corporations (mncs)

c.portfolio managers of international mutual funds

d.none of the above

9) with a bearer bond,

a.possession is evidence of ownership

b.the issuer keeps records indicating only who the current owner of a bond is

c.the owner’s name is on the bond

d.the owner’s name is assigned to the bond serial number, but not indicated on the bond

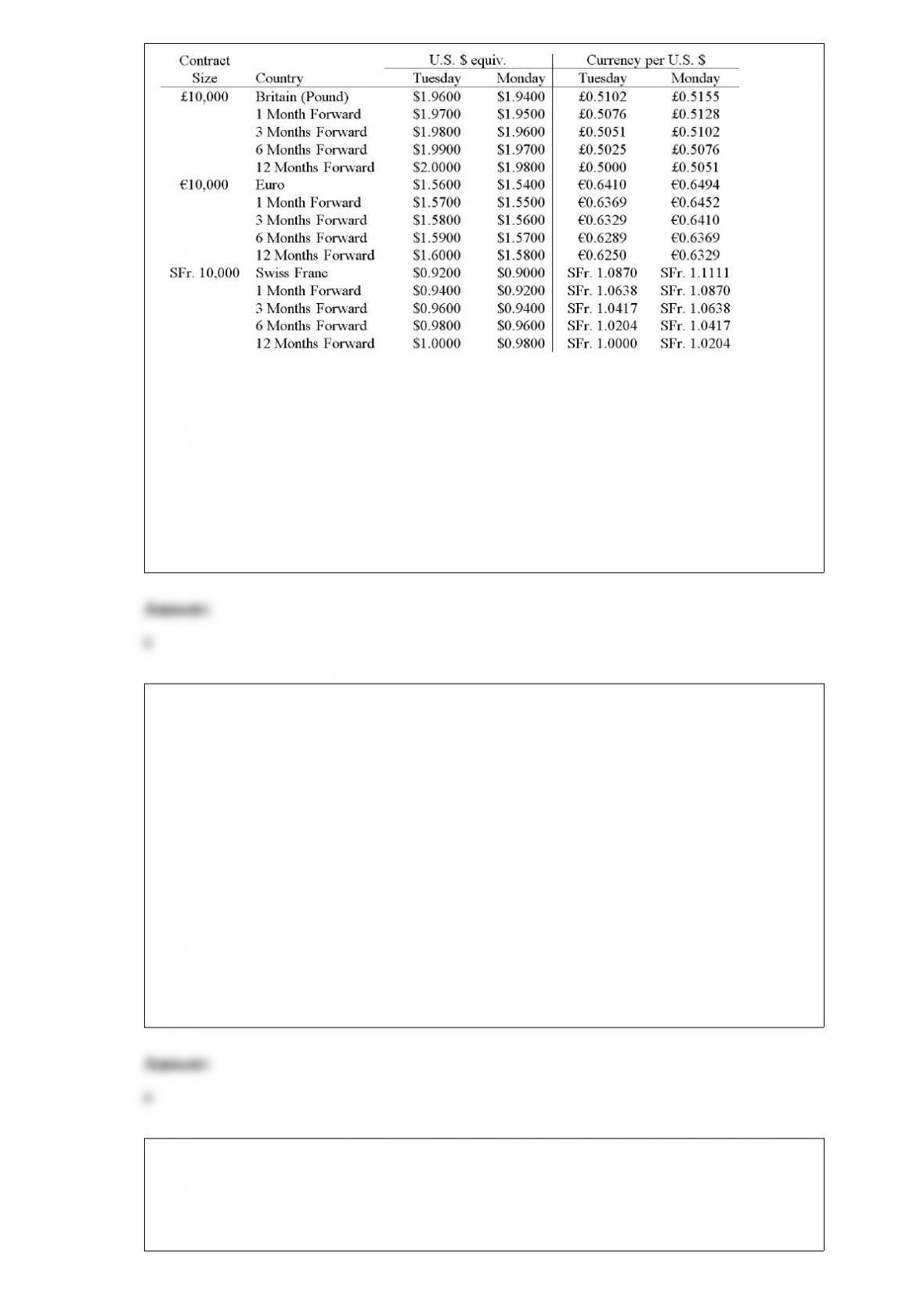

10) your firm is a u.k.-based exporter of bicycles. you have sold an order to a swiss firm

for sfr. 1,000,000 worth of bicycles. payment from the swiss firm (in swiss francs) is

due in 12 months. detail a strategy using futures contracts that will hedge your

exchange rate risk. have an estimate of how many contracts of what type and maturity.

a.go short 100 12-month swiss franc futures contracts; and long 50 12-month pound

futures contracts

b.go long 100 12-month swiss franc futures contracts; and short 50 12-month pound

futures contracts

c.go short 100 12-month swiss franc futures contracts; and short 50 12-month pound

futures contracts

d.go long 100 12-month swiss franc futures contracts; and long 50 12-month pound

futures contracts

e.none of the above

11) which of the following is a true statement?

a.while researchers found it difficult to reject the random walk hypothesis for exchange

rates on empirical grounds, there is no theoretical reason why exchange rates should

follow a pure random walk

b.while researchers found it easy to reject the random walk hypothesis for exchange

rates on empirical grounds, there are strong theoretical reasons why exchange rates

should follow a pure random walk

c.while researchers found it difficult to reject the random walk hypothesis for exchange

rates on empirical grounds, there are compelling theoretical reasons why exchange rates

should follow a pure random walk

d.none of the above

12) as of today, the spot exchange rate is 1.00 = $1.50 and the rates of inflation

expected to prevail for the next year in the u.s. is 2% and 3% in the euro zone. what is

the one-year forward rate that should prevail?

a.1.00 = $1.5147

b.1.00 = $1.4854

c.1.00 = $0.6602

d.$1.00 = 0.6602

13) which country is not using the euro?

a.greece

b.italy

c.sweden

d.portugal

14) the term “forfaiting”

a.means relinquishing, waiving, yielding, and penalty

b.is a type of medium-term trade financing used to finance the sale of capital goods

c.involves the sale of promissory notes signed by the importer in favor of the exporter,

who might sell the notes at a discount from face value

d.both b and c

15) the current spot exchange rate is $1.55/ and the three-month forward rate is $1.50/.

based on your analysis of the exchange rate, you are confident that the spot exchange

rate will be $1.62/ in three months. assume that you would like to buy or sell 1,000,000.

what actions do you need to take to speculate in the forward market? what is the

expected dollar profit from speculation?

a.sell 1,000,000 forward for $1.50/

b.buy 1,000,000 forward for $1.50/

c.wait three months, if your forecast is correct buy 1,000,000 at $1.52/

d.buy 1,000,000 today at $1.55/; wait three months, if your forecast is correct sell

1,000,000 at $1.62/

16) consider fixed-for-fixed currency swap. firm a is a u.s.-based multinational. firm b

is a u.k.-based multinational. firm a wants to finance a £2 million expansion in great

britain. firm b wants to finance a $4 million expansion in the u.s. the spot exchange rate

is £1.00 = $2.00. firm a can borrow dollars at $10% and pounds sterling at 12%. firm b

can borrow dollars at 9% and pounds sterling at 11%. which of the following swaps is

mutually beneficial to each party and meets their financing needs? neither party should

face exchange rate risk.

a.there is no mutually beneficial swap that has neither party facing exchange rate risk

b.firm a should borrow $4 million in dollars, pay 11% in pounds to firm b, who in turn

borrows 2 million pounds and pays 8% in dollars to a

c.firm a should borrow $2 million in dollars, pay 11% in pounds to firm b, who in turn

borrows 4 million pounds and pays 8% in dollars to a

d.firm a should borrow $4 million in dollars, pay 11% in pounds to firm b, who in turn

borrows 2 million pounds and pays 10% in dollars to a