1) capital export neutrality

a.is a goal based on worldwide economic efficiency

b.is an example of mercantilism

c.is based on host country economic efficiency

d.is based on mnc home country economic efficiency

2) the european stock exchange, comparable in volume to the nyse

a.is located in milan

b.is located in london

c.is located in frankfurt

d.none of the above

3) u.s. car makers were forced to build their own network of dealerships to enter the

japanese market.

a.this is an example of backward vertical integration

b.this is an example of forward vertical integration

c.this is an example of sideways vertical integration

d.none of the above

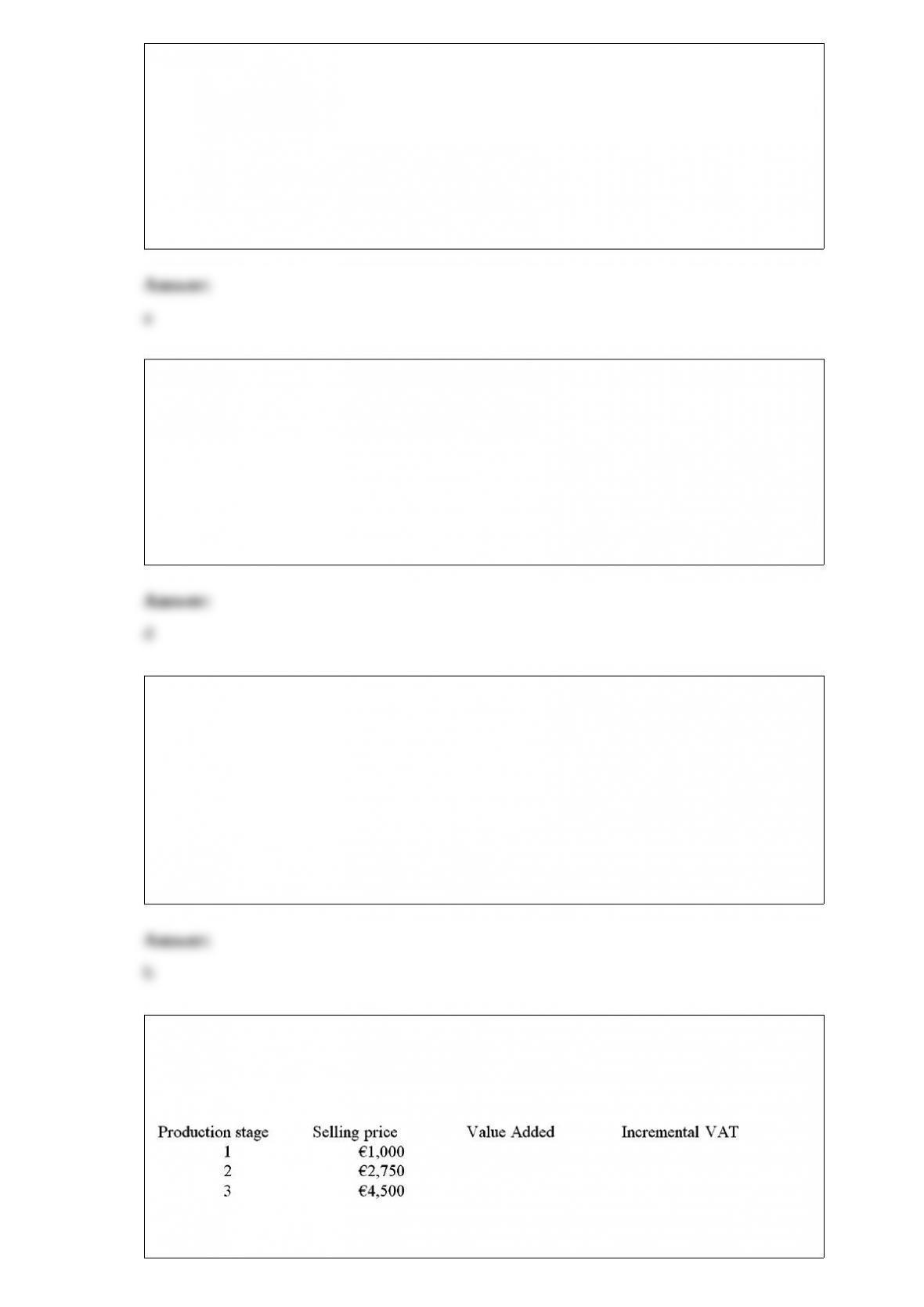

4) there are three production stages required before a bicycle produced by masi

bicicletia s.a. can be sold at retail for 4,500. the vat rate is 15%. find the total tax

liability due.

a.525

b.675

c.3,500

d.none of the above

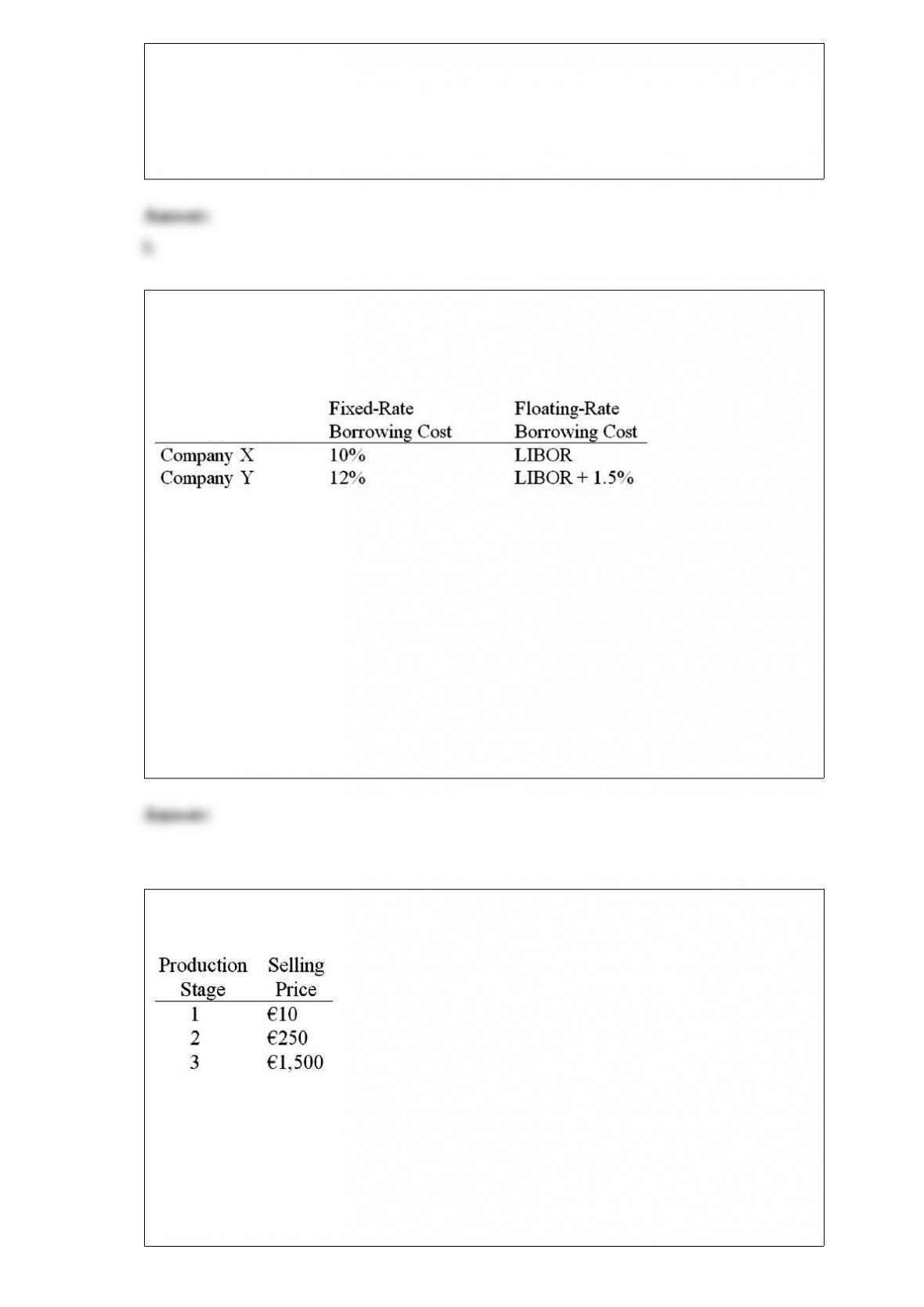

5) company x wants to borrow $10,000,000 floating for 5 years; company y wants to

borrow $10,000,000 fixed for 5 years. their external borrowing opportunities are shown

below:

a swap bank proposes the following interest only swap: x will pay the swap bank annual

payments on $10,000,000 with the coupon rate of libor – 0.15%; in exchange the swap

bank will pay to company x interest payments on $10,000,000 at a fixed rate of 9.90%.

what is the value of this swap to company x?

a.company x will lose money on the deal

b.company x will save 25 basis points per year on $10,000,000 = $25,000 per year

c.company x will only break even on the deal

d.company x will save 5 basis points per year on $10,000,000 = $5,000 per year

6) assume that a product has the following three stages of production:

if the value-added tax (vat) rate is 20%, what would be the vat over all stages of

production?

a.90

b.120

c.300

d.225

7) the rate charged by banks with excess funds is referred to as the interbank offered

rate; they will accept interbank deposits at the interbank bid rate.

a.the spread is generally 1/8 of 1 percent for most major eurocurrencies

b.the spread is generally referred to as “the ted spread”

c.the spread is generally referred to as the bid-ask commission

d.none of the above

8) under the gold standard, international imbalances of payment will be corrected

automatically under the

a.gresham exchange rate regime

b.european monetary system

c.price-specie-flow mechanism

d.bretton woods accord

9) suppose that the united states is on a bimetallic standard at $30 to one ounce of gold

and $2 for one ounce of silver. if new silver mines open and flood the market with

silver,

a.only the silver currency will circulate

b.only the gold currency will circulate

c.no change will take place since citizens could exchange their gold currency for silver

currency at any time

d.none of the above

10) american call and put premiums

a.should be at least as large as their intrinsic value

b.should be at no larger than their moneyness

c.should be exactly equal to their time value

d.should be no larger than their speculative value

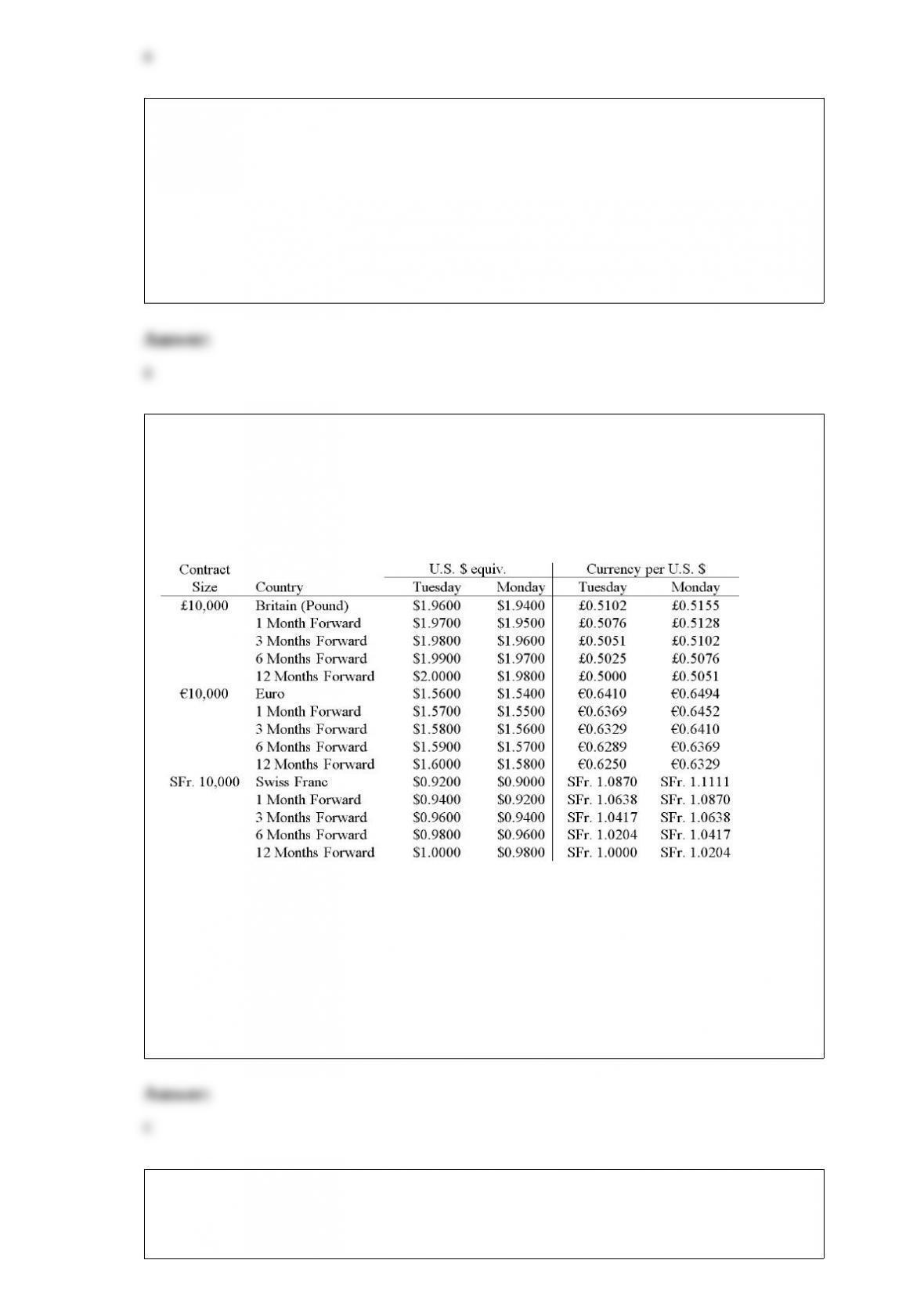

11) your firm is a swiss importer of bicycles. you have placed an order with an italian

firm for 1,000,000 worth of bicycles. payment (in euro) is due in 12 months. detail a

strategy using futures contracts that will hedge your exchange rate risk. have an

estimate of how many contracts of what type and maturity.

a.go short 100 12-month euro futures contracts; and short 160 12-month sfr. futures

contracts

b.go long 100 12-month futures contracts; and long 160 12-month sfr. futures contracts

c.go long 100 12-month euro futures contracts; and short 160 12-month swiss franc

futures contracts

d.go short 100 12-month euro futures contracts; and long 160 12-month swiss franc

futures contracts

e.none of the above

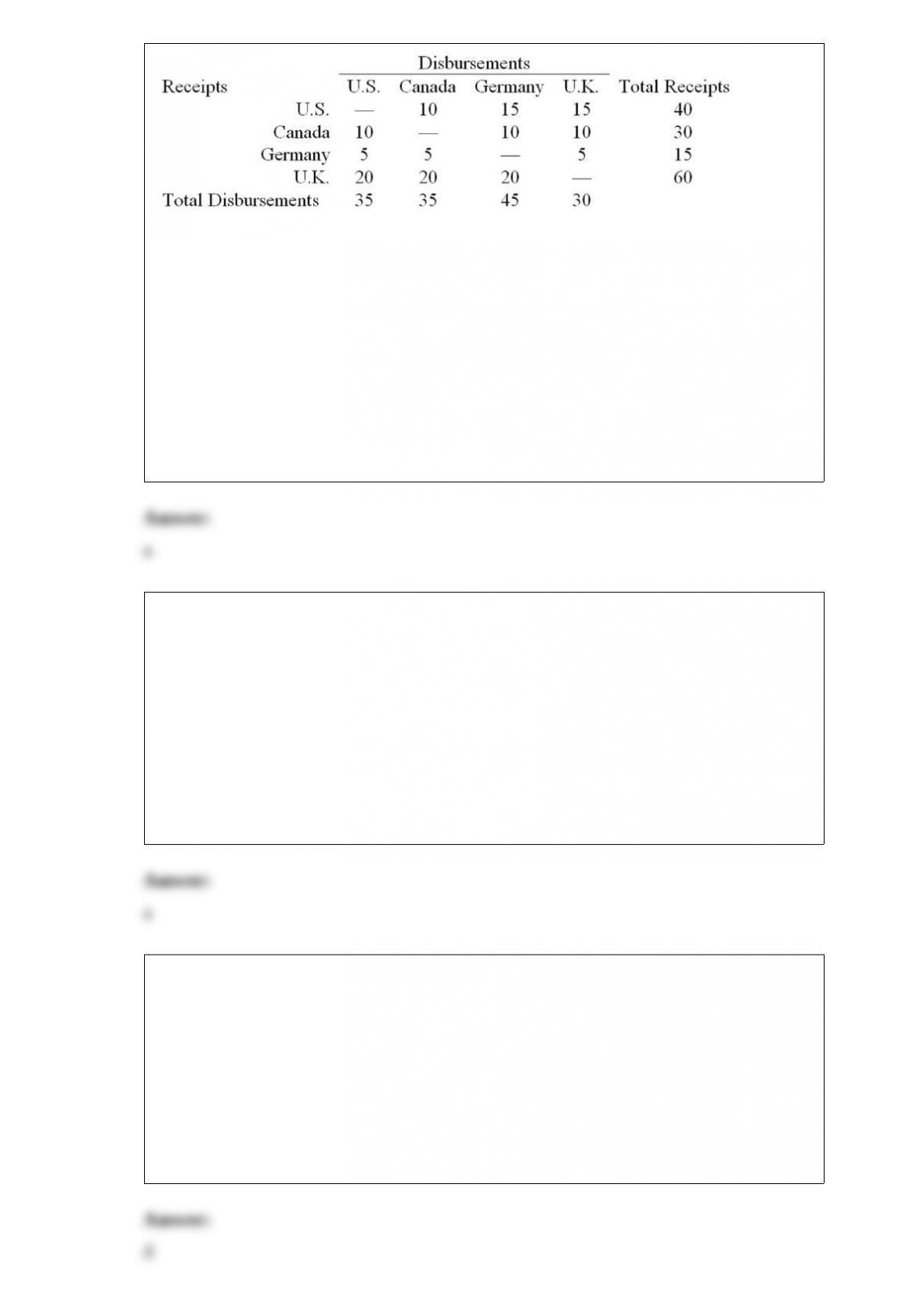

12) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

find the net cash flow in (out of) the u.s. affiliate.

a.$0 in or out

b.$5,000 out

c.$10,000 in

d.$15,000 out

e.none of the above

13) as of today, the spot exchange rate is 1.00 = $1.25 and the rates of inflation

expected to prevail for the next year in the u.s. is 2% and 3% in the euro zone. what is

the one-year forward rate that should prevail?

a.1.00 = $1.2379

b.1.00 = $1.2139

c.1.00 = $0.9903

d.$1.00 = 1.2623

14) the extent to which the value of the firm would be affected by expected changes in

the exchange rate is

a.transaction exposure

b.translation exposure

c.economic exposure

d.none of the above

15) eurobonds are usually

a.registered bonds

b.bearer bonds

c.floating-rate, callable and convertible

d.denominated in the currency of the country that they are sold in

16) suppose that the pound is pegged to gold at £20 per ounce and the dollar is pegged

to gold at $35 per ounce. this implies an exchange rate of $1.75 per pound. if the

current market exchange rate is $1.80 per pound, how would you take advantage of this

situation? hint: assume that you have $350 available for investment.

a.start with $350. buy 10 ounces of gold with dollars at $35 per ounce. convert the gold

to £200 at £20 per ounce. exchange the £200 for dollars at the current rate of $1.80 per

pound to get $360

b.start with $350. exchange the dollars for pounds at the current rate of $1.80 per

pound. buy gold with pounds at £20 per ounce. convert the gold to dollars at $35 per

ounce

c.a and b both work

d.none of the above

17) a “foreign bond” issue is

a.one denominated in a particular currency but sold to investors in national capital

markets other than the country that issued the denominating currency

b.one offered by a foreign borrower to investors in a national market and denominated

in that nation’s currency

c.for example, a german mnc issuing dollar-denominated bonds to u.s. investors

d.both b and c

18) suppose your firm issues a 100,000,000 one-year bond with a coupon rate of 8

percent per annum. the underwriting spread is 2 percent. your actual cost of this debt is

a.8 percent

b.10 percent

c.10.2 percent

d.none of the above

19) the time from acceptance to maturity on a $500,000 banker’s acceptance is 270

days.

the importing bank’s acceptance commission is 0.75 percent and that the market rate for

270-day b/as is 4 percent.

determine the amount the exporter will receive if he holds the b/a until maturity.

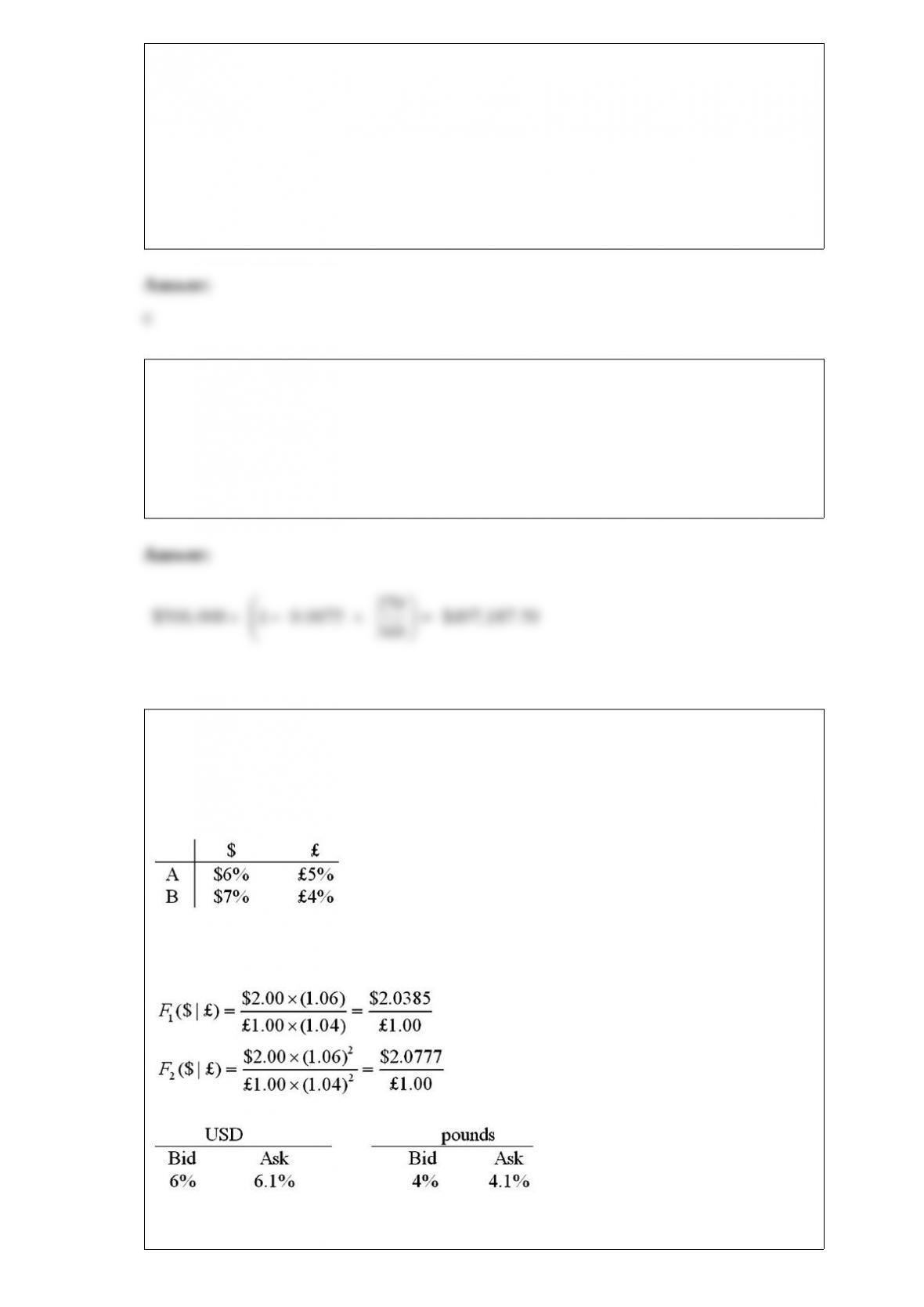

20) consider the situation of firm a and firm b. the current exchange rate is $2.00/£ firm

a is a u.s. mnc and wants to borrow £30 million for 2 years. firm b is a british mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown,

both firms have aaa credit ratings.

the irp 1-year and 2-year forward exchange rates are

explain how firm b could use the forward exchange markets to redenominate a 2-year

£30m 4% pound sterling loan into a 2-year usd-denominated loan.

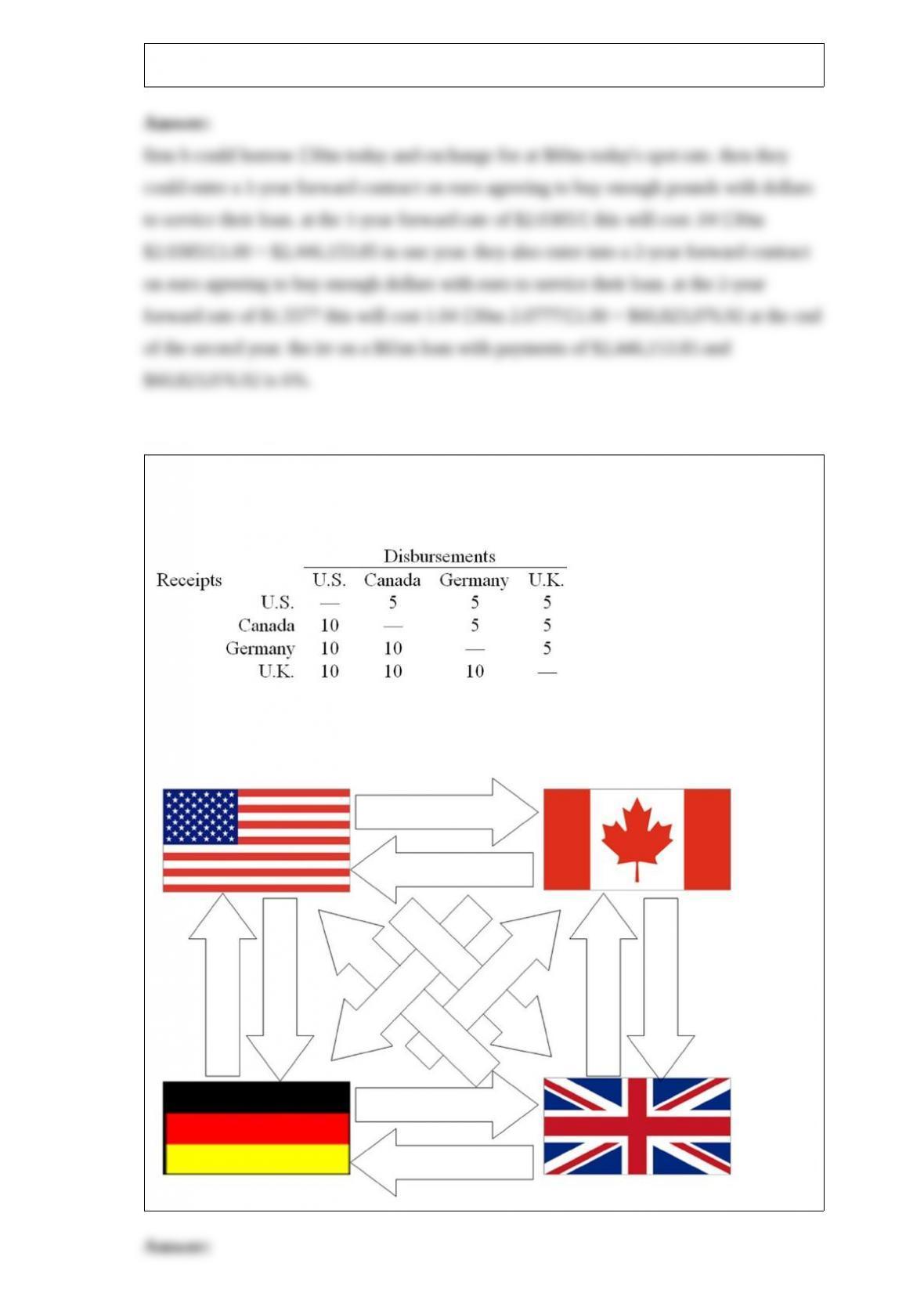

21) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

fill out the following figure with the initial situation shown in the table.

22) consider an option to buy 12,500 for £10,000. in the next period, the euro can

strengthen against the pound by 25% (i.e. each euro will buy 25% more pounds) or

weaken by 20%.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

use your results from the last three questions to verify your earlier result for the value of

the call.

23) assume that you are a retail customer.

please note that your answers are worth zero points if they do not include currency

symbols ($, )

there is (at least) one profitable arbitrage at these prices. what is it?

24)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

using your previous answers and a bit more work, find the 1-year forward exchange rate

in $ per that that satisfies irp from the perspective of a customer who borrowed 1m,

traded for dollars at the spot rate and invested at i$ = 4%.

25) consider an option to buy 12,500 for £10,000. in the next period, the euro can

strengthen against the pound by 25% (i.e. each euro will buy 25% more pounds) or

weaken by 20%.

big hint: don’t round, keep exchange rates out to at least 4 decimal places.

calculate the hedge ratio.

26) the time from acceptance to maturity on a $50,000 banker’s acceptance is 180 days.

the importing bank’s acceptance commission is 2.50 percent and that the market rate for

180-day b/as is 2 percent.

if the exporter’s opportunity cost of capital is 11 percent, should he discount the b/a or

hold it to maturity?

27) consider the situation of firm a and firm b. the current exchange rate is $2.00/£ firm

a is a u.s. mnc and wants to borrow £30 million for 2 years. firm b is a british mnc and

wants to borrow $60 million for 2 years. their borrowing opportunities are as shown,

both firms have aaa credit ratings.

explain how this opportunity affects which swap firm b will be willing to participate in.

28)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

if you borrowed $1,000,000 for one year, how much money would you owe at

maturity?