1) covered interest arbitrage (cia) activities will result in

a.an unstable international financial markets

b.restoring equilibrium prices quickly

c.a disintermediation

d.no effect on the market

2) the goal of shareholder wealth maximization

a.is not appropriate for non-u.s. business firms

b.means that all business decisions and investments that a firm makes are done for the

purpose of making the owners of the firm better off financially

c.is a sub-objective the firm should attempt to achieve after the objective of customer

satisfaction is met

d.is in conflict with the privatization process taking place in third-world countries

3) as a general rule,

a.excess tax credits can be carried back two years

b.excess tax credits can be carried forward five years

c.excess tax credits must be used in the year recognized

d.both a and b

4) in the short run a currency depreciation can make a trade balance worse if

a.there is no domestic producer of an import

b.there is no domestic buyer for an import

c.there is no export market for a country’s output

5) the gold standard still has ardent supporters who believe that it provides

a.an effective hedge against price inflation

b.fixed exchange rates between all currencies

c.monetary policy autonomy

d.all of the above

6) which of the following is a translation method where the gain or loss due to

translation adjustment does not affect reported cash flows?

a.current/noncurrent method

b.current rate method

c.current/future method

d.short/long term method

7) in the interbank market, the standard size of a trade among large banks in the major

currencies is

a.for the u.s.-dollar equivalent of $10,000,000,000

b.for the u.s.-dollar equivalent of $10,000,000

c.for the u.s.-dollar equivalent of $100,000

d.for the u.s.-dollar equivalent of $1,000

8) a call option to buy £10,000 at a strike price of $1.80 = £1.00 is equivalent to

a.a put option to sell $18,000 at a strike price of $1.80 = £1.00

b.a call option on $18,000 at a strike price of $1.80 = £1.00

c.a put option on £10,000 at a strike price of $1.80 = £1.00

d.none of the above

9) in the bond market, there are brokers and market makers. which of the following are

true?

a.brokers accept buy or sell orders from market makers and then attempt to find a

matching party for the other side of the trade; they may also trade for their own account

b.brokers charge a small commission for their services to the market maker that

engaged them

c.brokers do not deal directly with retail clients

d.all of the above

10) suppose abc investment banker ltd., is quoting swap rates as follows: 7.50 – 7.85

annually against six-month dollar libor for dollars, and 11.00 – 11.30 percent annually

against six-month dollar libor for british pound sterling. abc would enter into a $/£

currency swap in which:

a.it would pay annual fixed-rate dollar payments of 7.5% in return for receiving annual

fixed-rate £ payments at 11.3%

b.it will receive annual fixed-rate dollar payments at 7.85% against paying annual

fixed-rate £ payments at 11%

c.a and b

d.none of the above

11) the volume of otc currency options trading is

a.much smaller than that of organized-exchange currency option trading

b.much larger than that of organized-exchange currency option trading

c.larger, because the exchanges are only repackaging otc options for their customers

d.none of the above

12) a complete contract between shareholders and managers

a.would specify exactly what the manager will do under each of all possible future

contingencies

b.would be an expensive contract to write and a very expensive contract to monitor

c.would eliminate any conflicts of interest (and managerial discretion)

d.all of the above

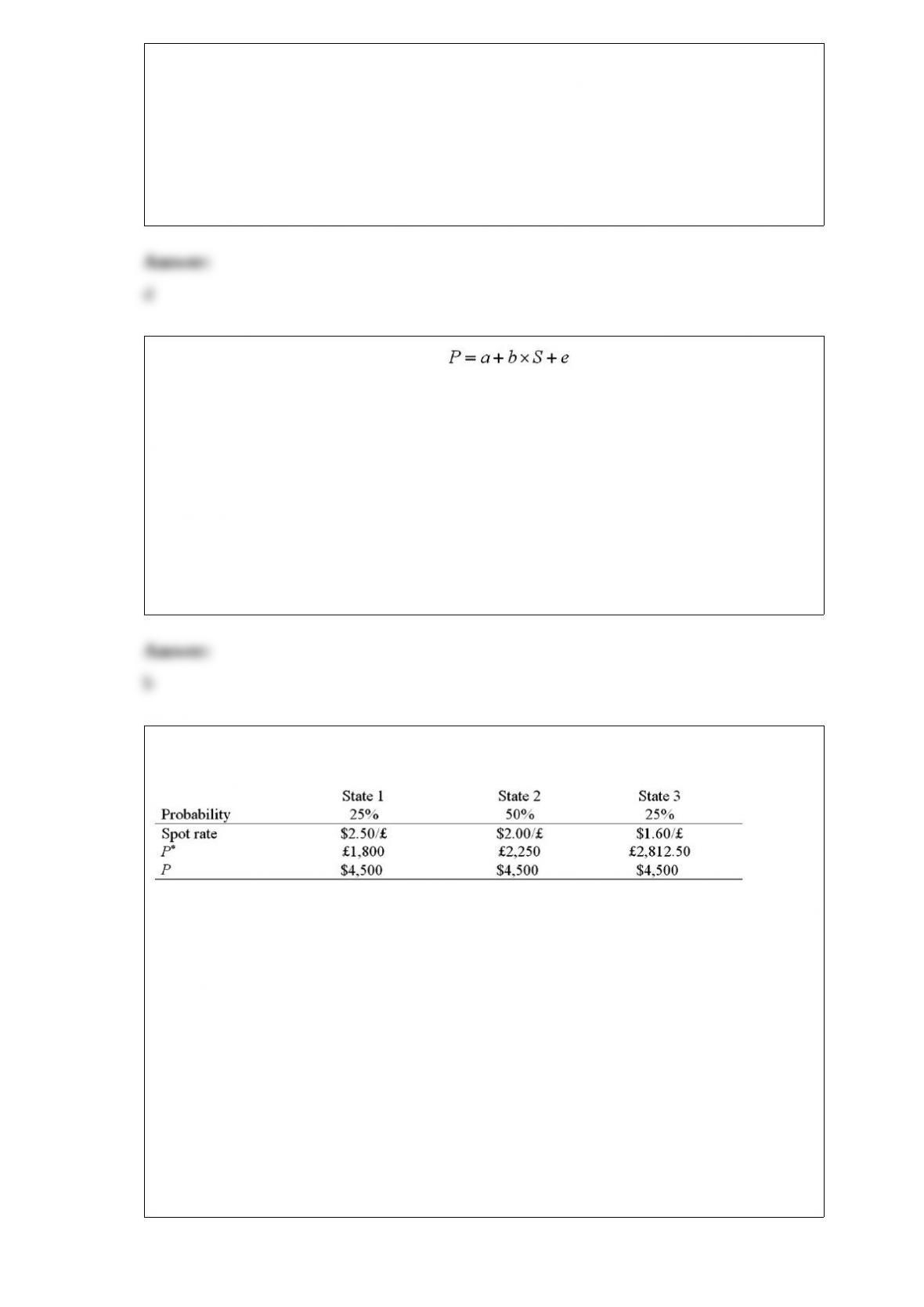

13) on the basis of regression equation we can decompose the

variability of the dollar value of the asset, var(p), into two separate components var(p) =

b2 var(s) + var(e).

the second term in the right-hand side of the equation, var(e) represents.

a.the part of the variability of the dollar value of the asset that is related to random

changes in the exchange rate

b.captures the residual part of the dollar value variability that is independent of

exchange rate movements

c.none of the above

14) a u.s. firm holds an asset in great britain and faces the following scenario:

where,

p* = pound sterling price of the asset held by the u.s. firm

p = dollar price of the same asset

which of the following would be an effective hedge?

a.sell £2,278.13 forward at the 1-year forward rate, f1($/£), that prevails at time zero

b.buy £2,500 forward at the 1-year forward rate, f1($/£), that prevails at time zero

c.sell £25,000 forward at the 1-year forward rate, f1($/£), that prevails at time zero

d.none of the above

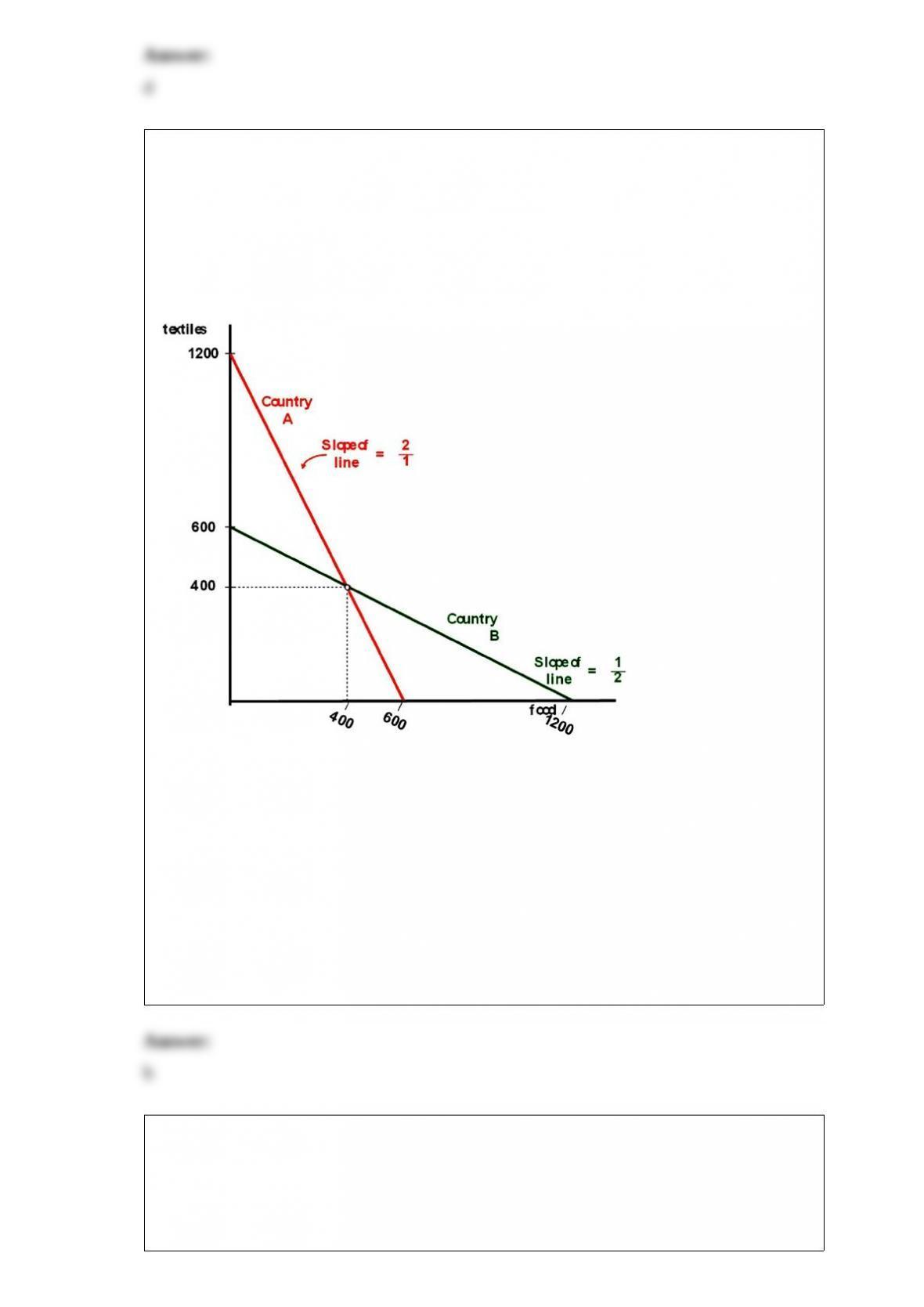

15) counties a and b currently consume 400 units of food and 400 units of textiles each

and currently do not trade with one another. the citizens of country a have to give up

one unit of food to gain two units of textiles, while the citizens of country b have to

give up one unit of textiles to gain two units of food. their production possibilities

curves are shown.

under the theory of comparative advantage, if free trade is allowed, the market clearing

price (or exchange rate if you will) between food and textiles will be

a.one unit of food for one unit of textiles

b.somewhere between one unit of food for two units of textiles and two units of food

for one unit of textiles

c.one unit of food for two units of textiles

d.two units of food for one unit of textiles

16) such products as mineral ore and cement that are heavy or bulky relative to their

economic values

a.may be suitable for exporting because high transportation costs will be overcome by

high profit margins in oligopolistic industries

b.have high “value-to-weight ratios” that protect profit margins

c.may not be suitable for exporting because high transportation costs will substantially

reduce profit margins

d.none of the above

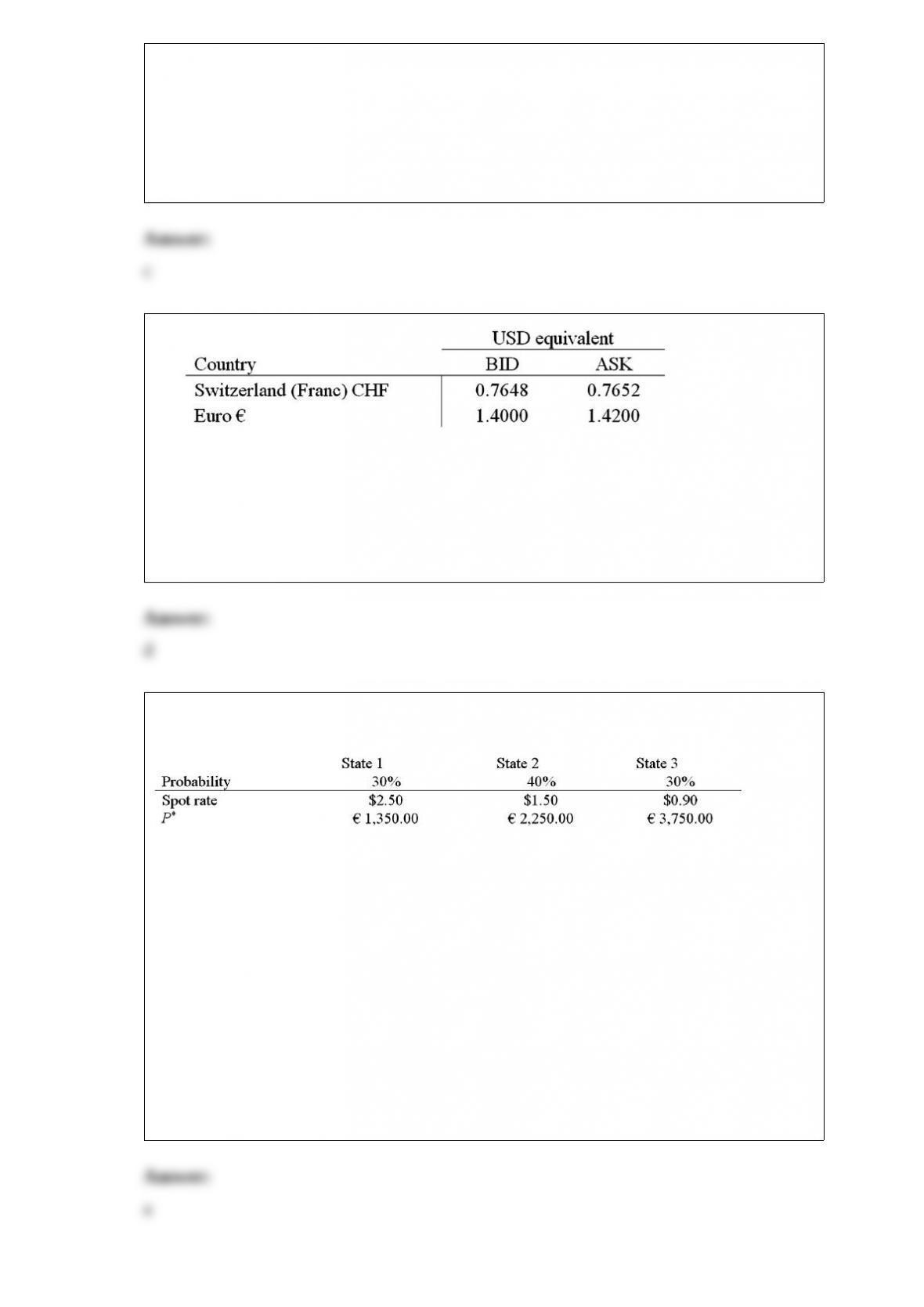

17)

what is the ask cross-exchange rate for swiss francs priced in euro?

hint: find the price that a currency dealer will take in euro to sell swiss francs.

a.0.5386/chf

b.0.5389/chf

c.0.5463/chf

d.0.5466/chf

18) a u.s. firm holds an asset in italy and faces the following scenario:

where

p* = euro price of the asset held by the u.s. firm

the cfo decides to hedge his exposure by selling forward the expected value of the euro

denominated cash flow at f1($/£) = $1.50/. as a result

a.the firm’s exposure to the exchange rate is made worse

b.he has a nearly perfect hedge

c.he has a perfect hedge

d.none of the above

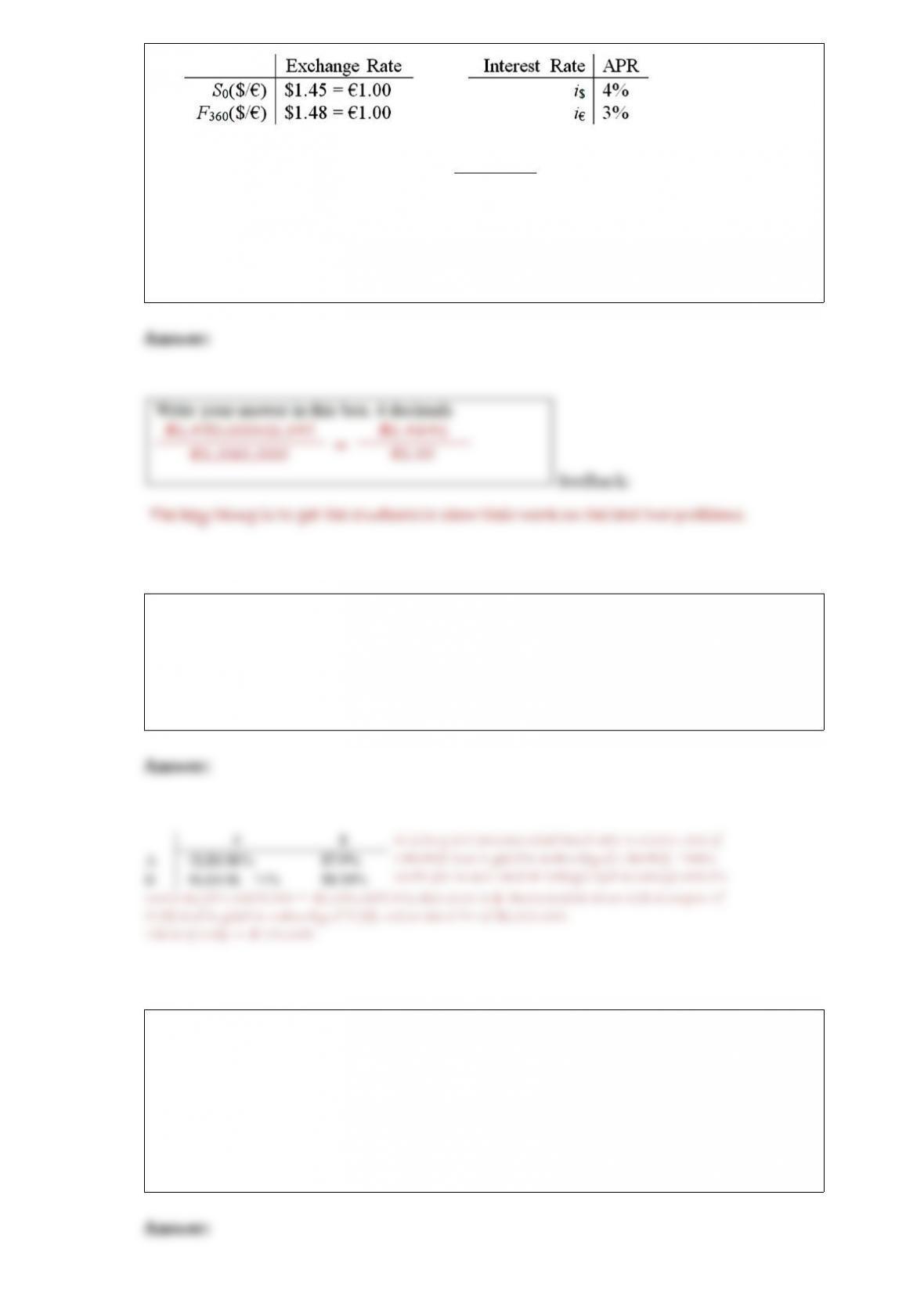

19)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

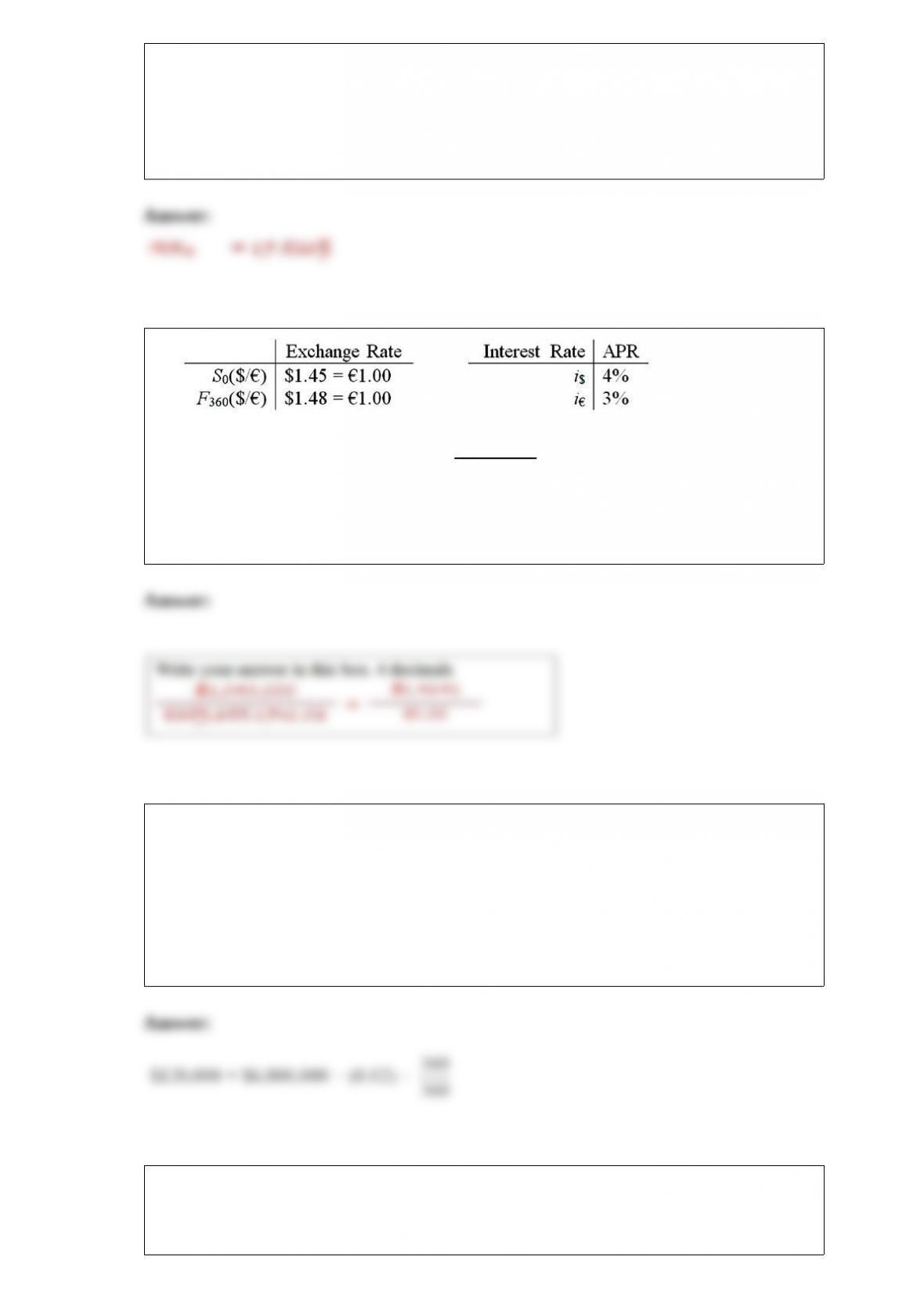

using your previous answers and a bit more work, find the 1-year forward exchange rate

in $ per that that satisfies irp from the perspective of a customer who borrowed 1m,

traded for dollars at the spot rate and invested at i$ = 4%.

20) suppose that the swap that you proposed in question 2 is now 4 years old (i.e. there

is exactly one year to go on the swap). if the spot exchange rate prevailing in year 4 is

$1.8778 = 1 and the 1-year forward exchange rate prevailing in year 4 is $1.95 = 1,

what is the value of the swap to the party paying dollars? if the swap were initiated

today the correct rates would be as shown:

21) the time from acceptance to maturity on a $6,000,000 banker’s acceptance is 360

days.

the importing bank’s acceptance commission is 2 percent and that the market rate for

360-day b/as is 3 percent.

determine the amount the exporter will receive if he discounts the b/a with the

importer’s bank.

22) the stock market of country a has an expected return of 5%, and a standard

deviation of expected return of 8%. the stock market of country b has an expected

return of 15% and a standard deviation of expected return of 10%.

find the global minimum variance portfolio.

23) the time from acceptance to maturity on a $2,000,000 banker’s acceptance is 90

days.

the importing bank’s acceptance commission is 1.25 percent and that the market rate for

90-day b/as is 6 percent.

determine the amount the exporter will receive if he discounts the b/a with the

importer’s bank.

24) your firm is based in southern ireland (and thereby operates in euro, not pounds)

and is considering an investment in the united states.

the project involves selling widgets: you project a sales volume of 50,000 widgets per

year, sales price of $20 per widget with a contribution margin of $15 per widget.

the project will last for 5 years, require an investment of $1,000,000 at time zero (which

will be depreciated straight-line to $10,000 over the 5 years). salvage value for the

equipment is projected to be $10,000. the project will operate in rented quarters:

$300,000 rent is due at the start of each year.

the corporate tax rate is 12% in ireland and 40% in the u.s.

for simplicity, assume that taxes are paid like sales taxes: immediately.

the spot exchange rate is $1.50 = 1.00. the cost of capital to the irish firm for a domestic

project of this risk is 8%. the u.s. risk-free rate is 3%; the irish risk-free rate is 2%.

what is the dollar-denominated irr?

25)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

using your previous answers and a bit more work, find the 1-year forward bid exchange

rate in $ per that satisfies irp from the perspective of a customer.

26) the time from acceptance to maturity on a $6,000,000 banker’s acceptance is 360

days.

the importing bank’s acceptance commission is 2 percent and that the market rate for

360-day b/as is 3 percent.

calculate the amount the banker will receive if the exporter discounts the b/a with the

importer’s bank.

27) the stock market of country a has an expected return of 8%, and standard deviation

of expected return of 5%. the stock market of country b has an expected return of 16%

and standard deviation of expected return of 10%.

assume that the correlation of expected return between a and b is negative 1. calculate

the standard deviation of expected return of the portfolio in the last question.

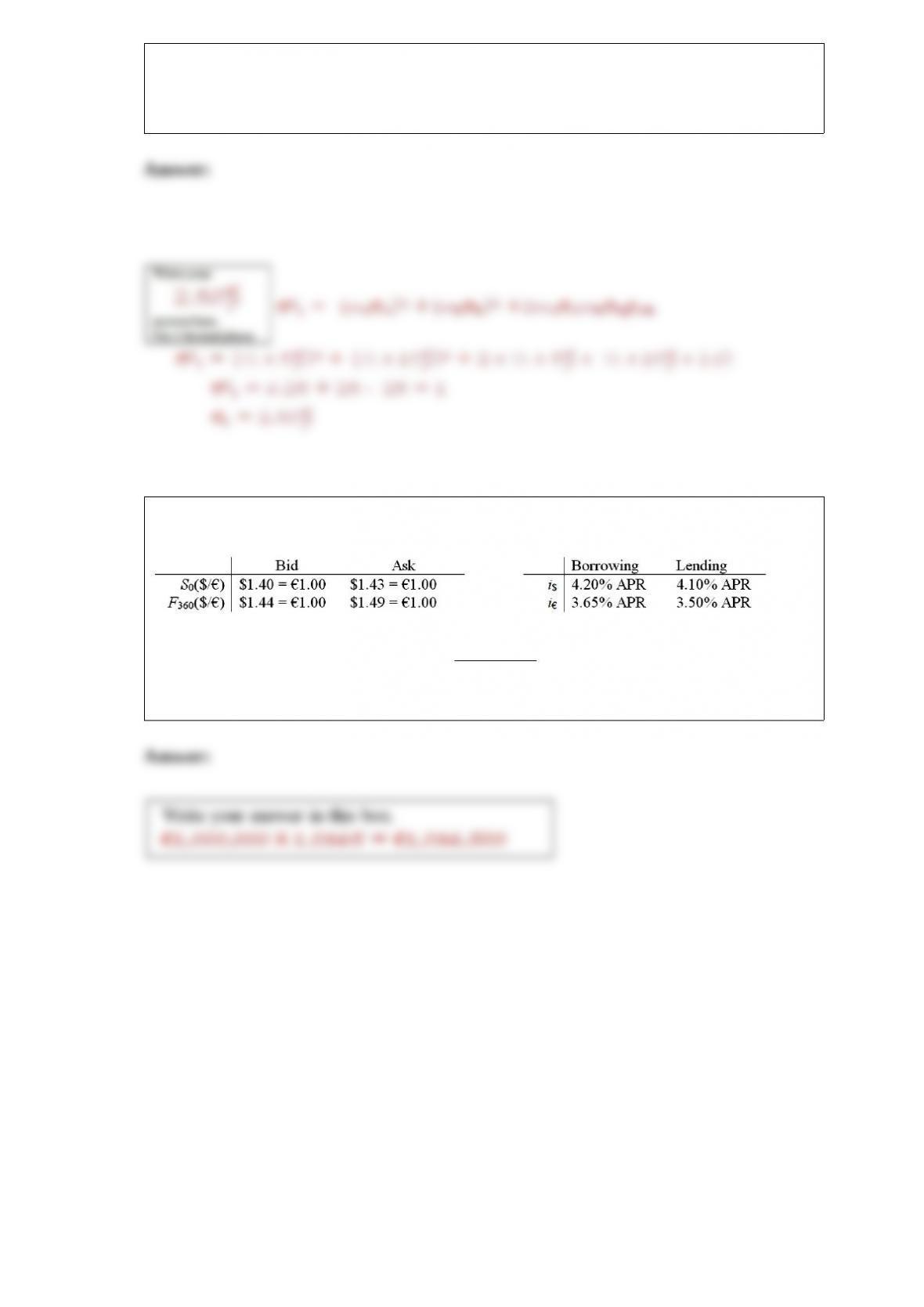

28) assume that you are a retail customer.

please note that your answers are worth zero points if they do not include currency

symbols ($, )

if you borrowed 1,000,000 for one year, how much money would you owe at maturity?