1) suppose the quote for a five-year swap with semiannual payments is 8.508.60

percent. the means

a.the swap bank will pay semiannual fixed-rate dollar payments of 8.60 percent against

receiving six-month dollar libor

b.the swap bank will receive semiannual fixed-rate dollar payments of 8.50 percent

against paying six-month dollar libor

c.if the swap bank is successful in getting counterparties to both legs of the swap at

these prices, he will have an annual profit of ten basis points

d.none of the above

2) a 1-year, 4 percent pound denominated bond sells at par. a comparable risk 1-year,

5.5 percent pound/dollar dual-currency bond pays $2,000 at maturity per £1,000 of face

value. it sells for £900. what is the implied direct $/£ exchange rate at maturity?

a.£0.4405/$1.00

b.$1.2048/£1.00

c.$2.2701/£1.00

d.$2.0000/£1.00

3) ‘samurai” bonds are

a.dollar-denominated foreign bonds originally sold to u.s. investors

b.yen-denominated foreign bonds originally sold in japan

c.pound sterling-denominated foreign bonds originally sold in the u.k

d.none of the above

4) the libor rate for euro

a.is euribor

b.is a government set rate

c.is the rate at which interbank deposits of euro are offered by one prime bank to

another in the euro zone

d.both a and c

5) unlike day orders, a good-til-cancelled (gtc) order is an order to buy or sell a security

at a specific or limit price that lasts until the order is completed or cancelled. which of

the following are true?

a.a gtc order will not be executed until the limit price has been reached, regardless of

how many days or weeks it might take

b.investors often use gtc orders to set a limit price that is far away from the current

market price

c.some brokerage firms may limit the time a gtc order can remain in effect and may

charge more for executing this type of order

d.all of the above are true

6) comparing “forward” and “futures” exchange contracts, we can say that

a.delivery of the underlying asset is seldom made in futures contracts

b.delivery of the underlying asset is usually made in forward contracts

c.delivery of the underlying asset is seldom made in either contractthey are typically

cash settled at maturity

d.both a and b

e.both a and c

7) the toronto stock exchange

a.is a fully automated

b.features electronic matching of public orders

c.has continuous order flow

d.all of the above

8) find the yield to maturity for this floating rate note: the reset date is today; coupons

are paid annually according to the formula (libor + percent); since issuance, there has

not been a change in the issuer’s credit rating. the bond has ten years to maturity and

libor = 3.5 percent.

a.3.5%

b.4%

c.3.75%

d.there is not enough information provided to make a determination

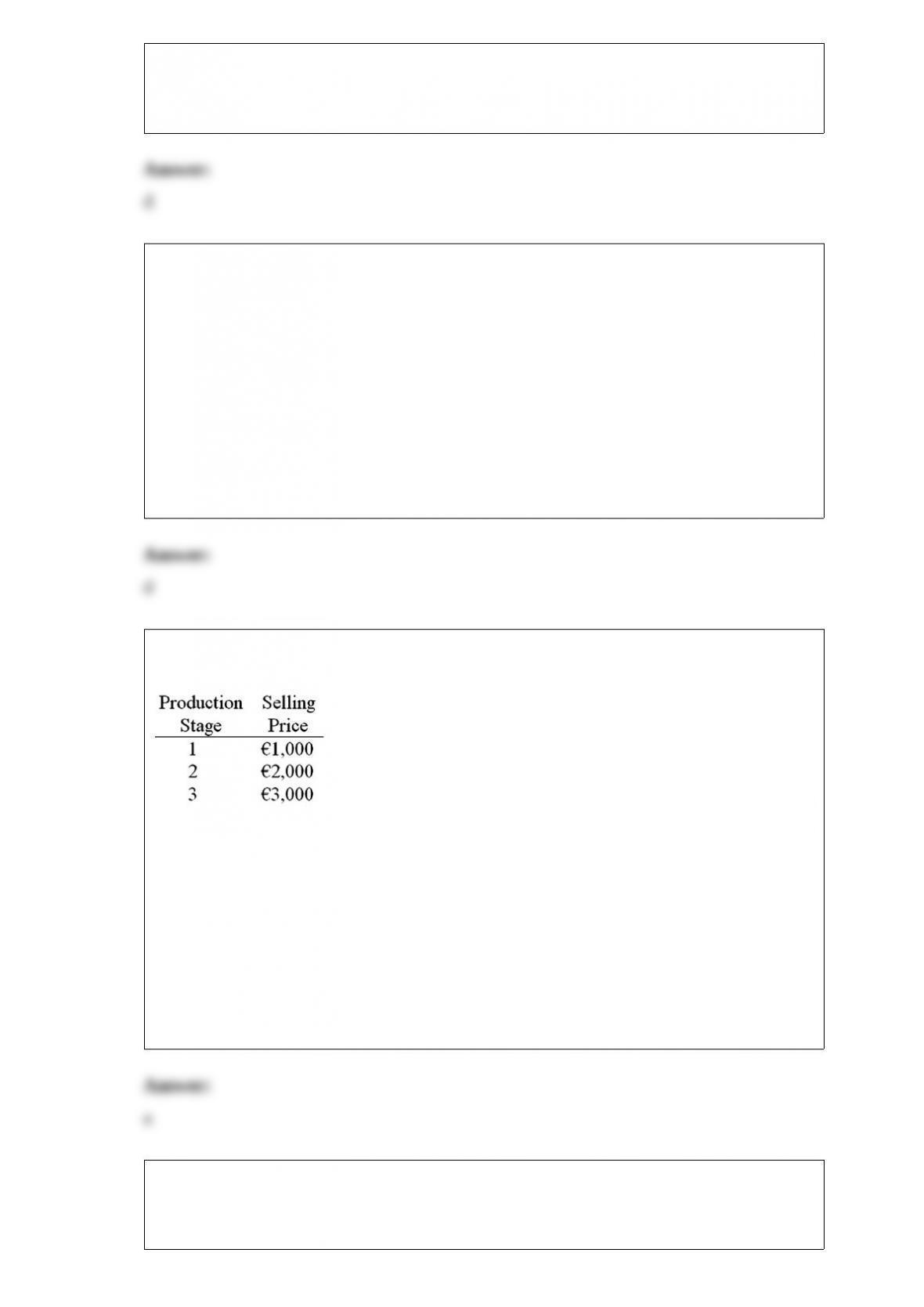

9) assume that a product has the following three stages of production:

if the value-added tax (vat) rate is 15%, what would be the vat over all stages of

production?

a.390

b.120

c.465

d.225

10) with regard to the financial structure of a foreign subsidiary

a.using local financing can reduce political risk

b.a mnc that finances a foreign investment with home-country equity faces greater risk

of expropriation than if it had financed the investment with at least some local debt or

equity

c.there may be advantages other than a reduction in political risk that encourage mncs

to finance foreign subsidiaries with local money

d.all of the above

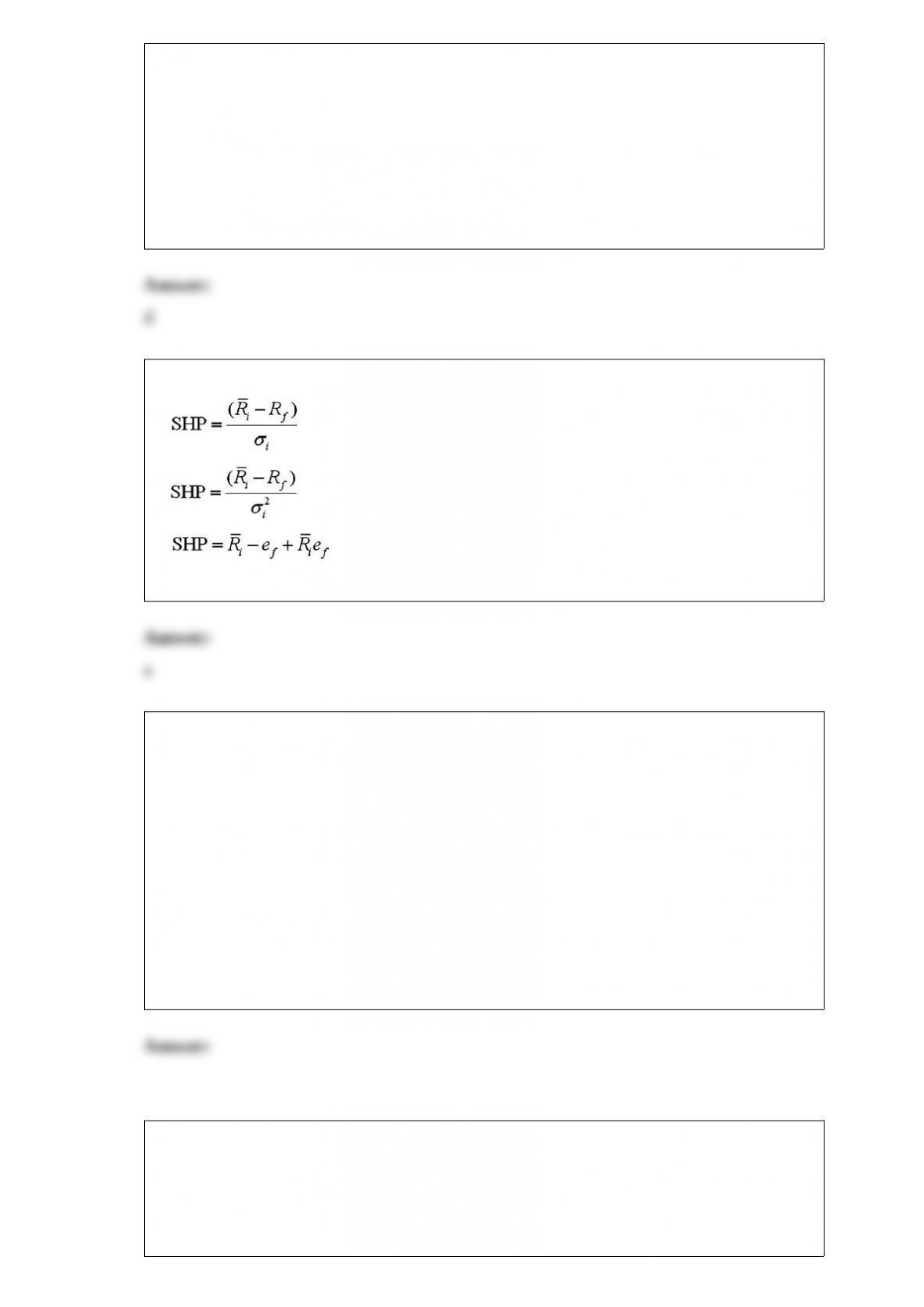

11) the ‘sharpe performance measure” (shp) is

a.

b.

c.

d.none of the above

12) xyz corporation enters into a 6-year interest rate swap with a swap bank in which it

agrees to pay the swap bank a fixed-rate of 9 percent annually on a notional amount of

sfr10,000,000 and receive libor – percent. as of the third reset date (i.e. mid-way

through the 6 year agreement), calculate the price of the swap, assuming that the

fixed-rate at which xyz can borrow has increased to 10%.

a.sfr248,685

b.sfr900,000

c.sfr2,700,000

d.sfr7,300,000

13) u.s. corporations

a.are allowed to issue bearer bonds to non-u.s. citizens

b.are not allowed to issue bearer bonds

c.are allowed to issue treasury bonds but not t-bills

d.none of the above

14) use the european option pricing formula to find the value of a six-month call option

on japanese yen. the strike price is $1 = ¥100. the volatility is 25 percent per annum; r$

= 5.5% and r¥ = 6%.

a.0.005395

b.0.005982

c.$0.006137/¥

d.none of the above

15) the same call from the last question (a 1-period call option on 10,000 with a strike

price of $12,500. could also be thought of as a 1-period at-the-money put option on

$12,500 with a strike price of 10,000.

as before, the spot exchange rate is 1.00 = $1.25. in the next period, the euro can

increase in dollar value to $2.00 or fall to $1.00. the interest rate in dollars is i$ =

27.50%; the interest rate in euro is i = 2%.

draw the binomial tree for this putoption.

put the tree in this box zero points for trees without currency symbols

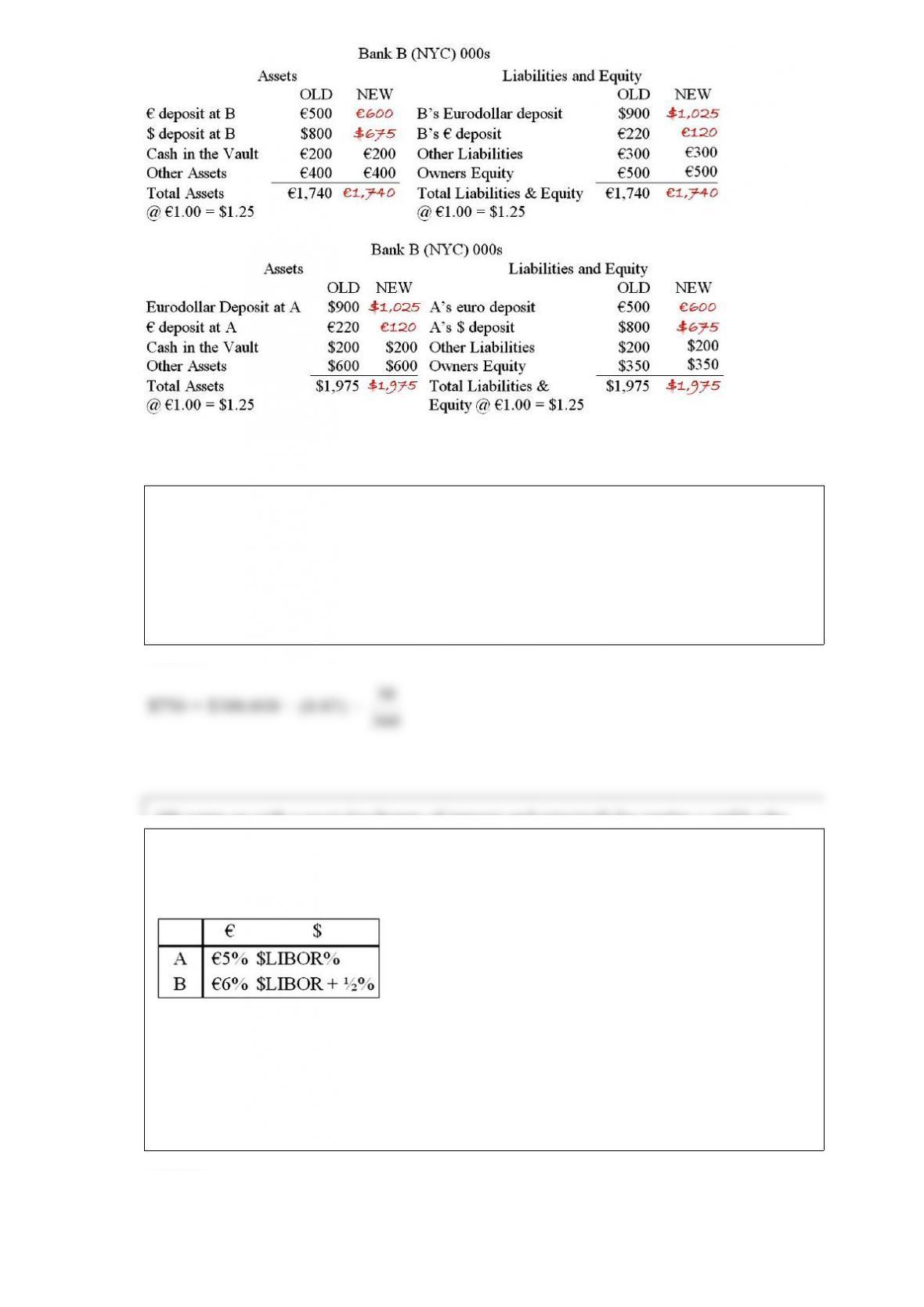

18) come up with a swap (exchange of interest and principal) for parties a and b who

have the following borrowing opportunities.

the current exchange rate is $1.60 = 1.00. company “a” is in milan, italy and wishes to

borrow $1,000,000 at a floating rate for 5 years and company “b” is a u.s. firm that

wants to borrow 625,000 for 5 years at a fixed rate of interest. you are a swap dealer.

quote a and b a swap that makes money for all parties and eliminates exchange rate risk

for both a and b.

19)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

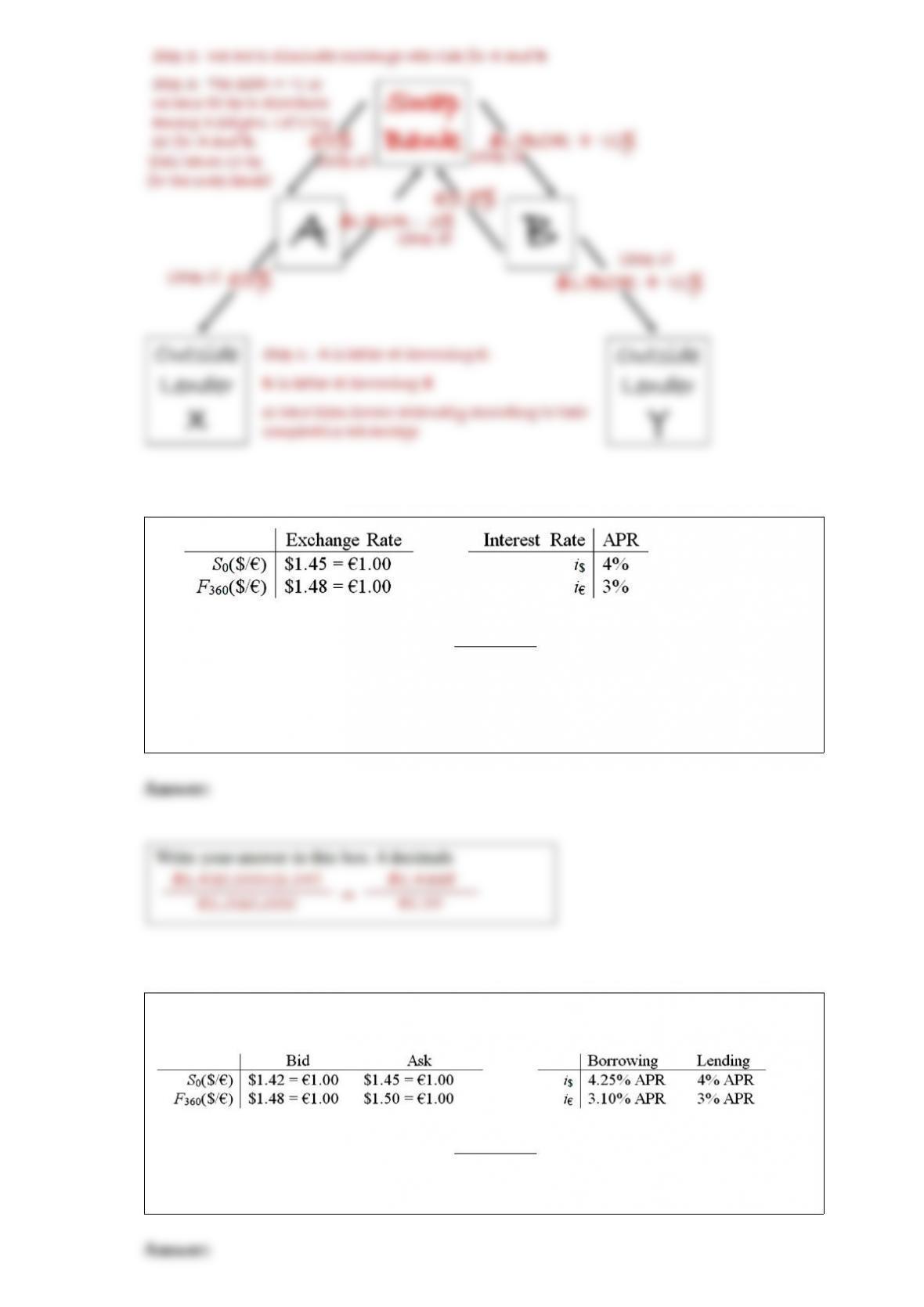

using your previous answers and a bit more work, find the 1-year forward ask exchange

rate in $ per that that satisfies irp from the perspective of a customer.

20) assume that you are a retail customer.

please note that your answers are worth zero points if they do not include currency

symbols ($, )

if you borrowed 1,000,000 for one year, how much money would you owe at maturity?

21) calculate the euro-based return an italian investor would have realized by investing

10,000 into a £50 british stock using 50% margin. one year after investment, the stock

pays a £1 dividend, and sells for £54 the exchange rate has changed from 1.25 per

pound to 1.30 per pound. the interest on the margin loan is 1% per year. the margin loan

was denominated in pounds.

22) the time from acceptance to maturity on a $1,000,000 banker’s acceptance is 90

days.

the importing bank’s acceptance commission is 3 percent and that the market rate for

90-day b/as is 5 percent.

determine the amount the exporter will receive if he holds the b/a until maturity.