1) assume the following: the current spot rate s$/£ = 2.00 and the annual interest rates:

ius = 4% and iuk = 8%. according to covered interest parity, if an intern at a bank in u.k.

sets the 90-day forward: f90$/£ = 1.80, then:

a.the intern has correctly set the forward rate

b.both u.s. and u.k. investment returns are equal

c.the british investment return exceeds the u.s. investment return

d.the u.s. investment return exceed the british investment return

2) exchange rates are 150 yen per dollar, 0.8 euro per dollar, and 20 pesos per dollar. a

bottle of beer in new york costs 6 dollars, 1,200 yen in tokyo, 7 euro in munich, and

100 pesos in cancun. where is the most expensive beer?

a. tokyo

b. munich

c. new york

d. cancun

3) interest rates on ________ are higher at eurobanks than domestic banks.

a.loans

b.deposits

c.currency exchanges

d.none of the above

4) a pegged exchange rate is:

i.fixed to a currency or basket of currencies

ii.responds to indicators (such as inflation differentials)

iii.may require intervention to maintain the target pegged rate

a.i only

b.iii only

c.i and iii

d.i, ii, and iii

5) an advantage of netting of a multinational corporation and its subsidiaries is that it:

a.increases foreign exchange risk

b.decreases the total volume of inter-subsidiary fund flows

c.increases the total amount of currency conversion

d.decreases the number of employees

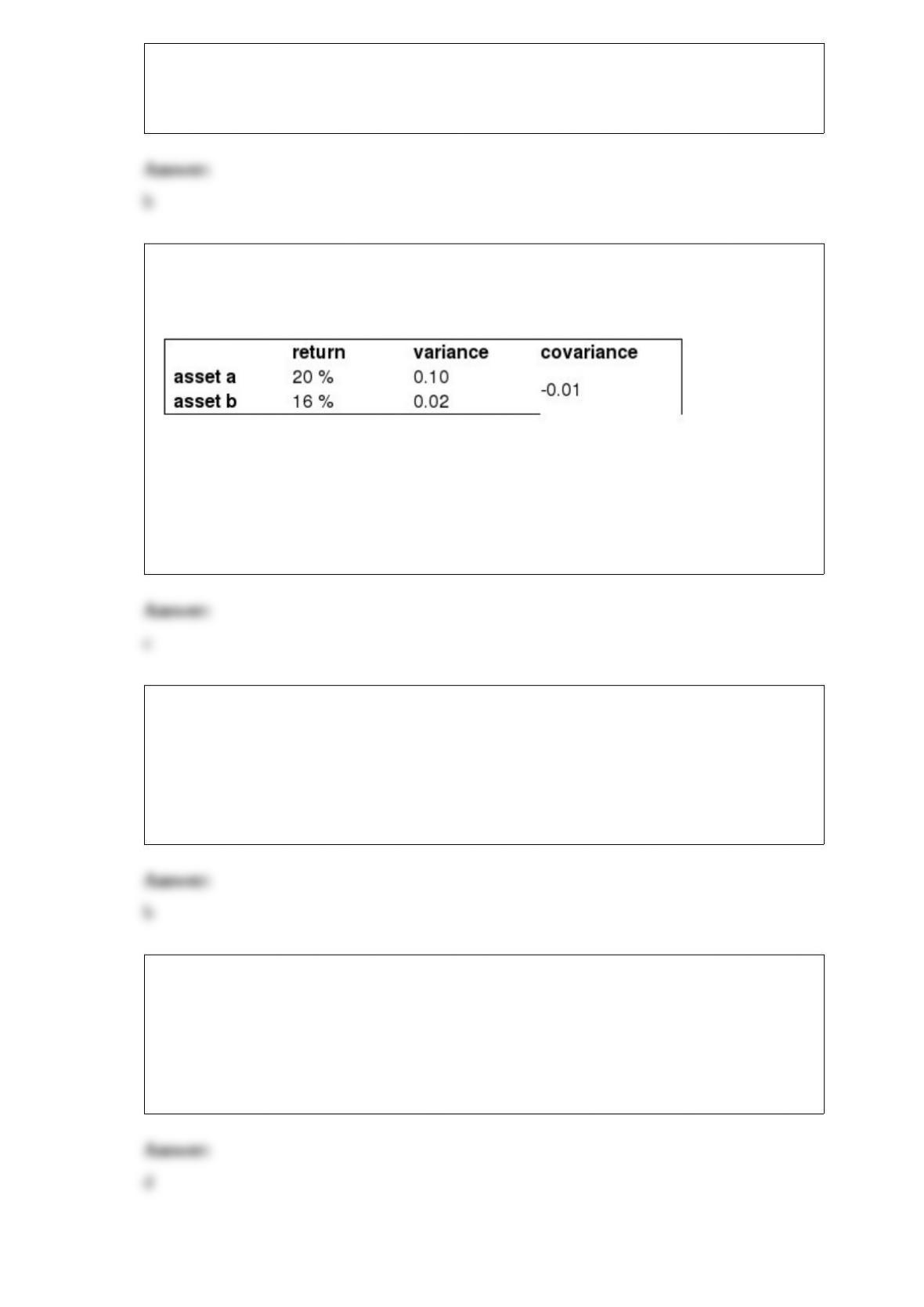

6) assume that you have a choice of two assets, a and b, and a portfolio of an equal

share of the two assets. assume also that the assets have the following statistics:

table 10-1:

see table 10-1. the negative covariance between asset a and asset b means that when

returns on asset a decrease then,

a.the variance of asset b tends to decreases

b.the returns on asset b tend to decrease

c.the returns on asset b tend to increase

d.the variance on asset a tends to decreases

7) security a and security b have a correlation coefficient of 1.0. if security as return is

expected to increase by 10 percent,

a.security bs return should also increase by 10 percent

b.security bs return should decrease by 10 percent

c.security bs return should be zero

d.security bs return is impossible to determine from the above information

8) a put option on japanese yen is written with a strike price of ¥95.00/$. which spot

exchange rate will maximize your profit if you choose to exercise the option?

a.¥85.00/$

b.¥90.00/$

c.¥100.00/$

d.¥115.00/$

9) figure 13-2

refer to figure 13.2. starting from an equilibrium point a, which of the following factors

would cause the is curve to shift to the left.

a.a tax cut

b.a decrease in money supply

c.an increase in money supply

d.a decrease in government spending

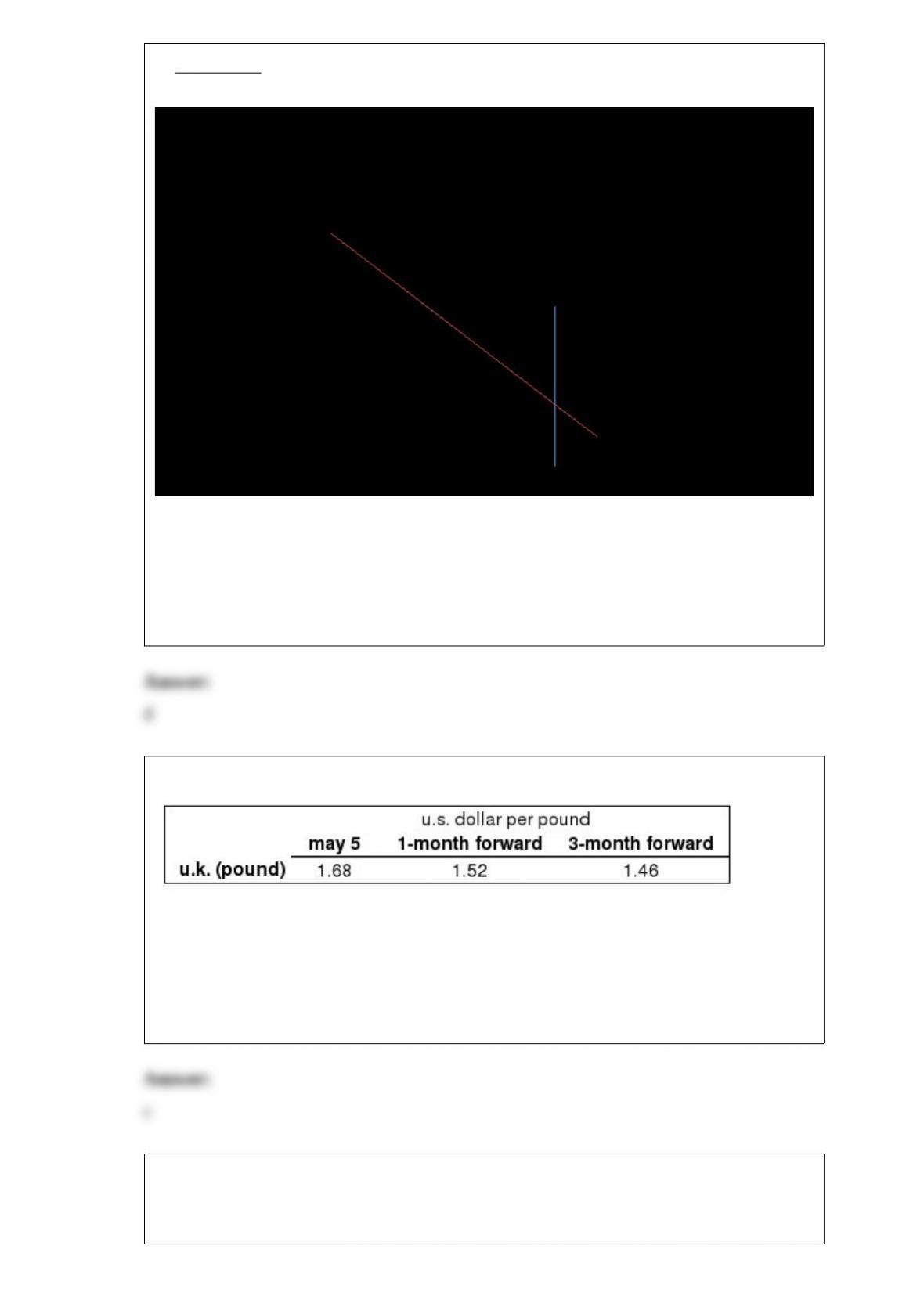

10) table 6-2: spot and forward exchange rates on may 5, 2012

refer to table 6-2. comparing the yens forward rates against the yens spot rate, over the

period of a forward contract, we would expect the yens spot rate to:

a.remain constant against the dollar

b.appreciate against the dollar

c.depreciate against the dollar

d.depreciate against the dollar in the first 30 days and then appreciate afterward

11) in the uncovered interest rate parity, the forward rate is assumed to include a

________.

a.return differential

b.exposure risk

c.risk premium

d.future spot exchange rate

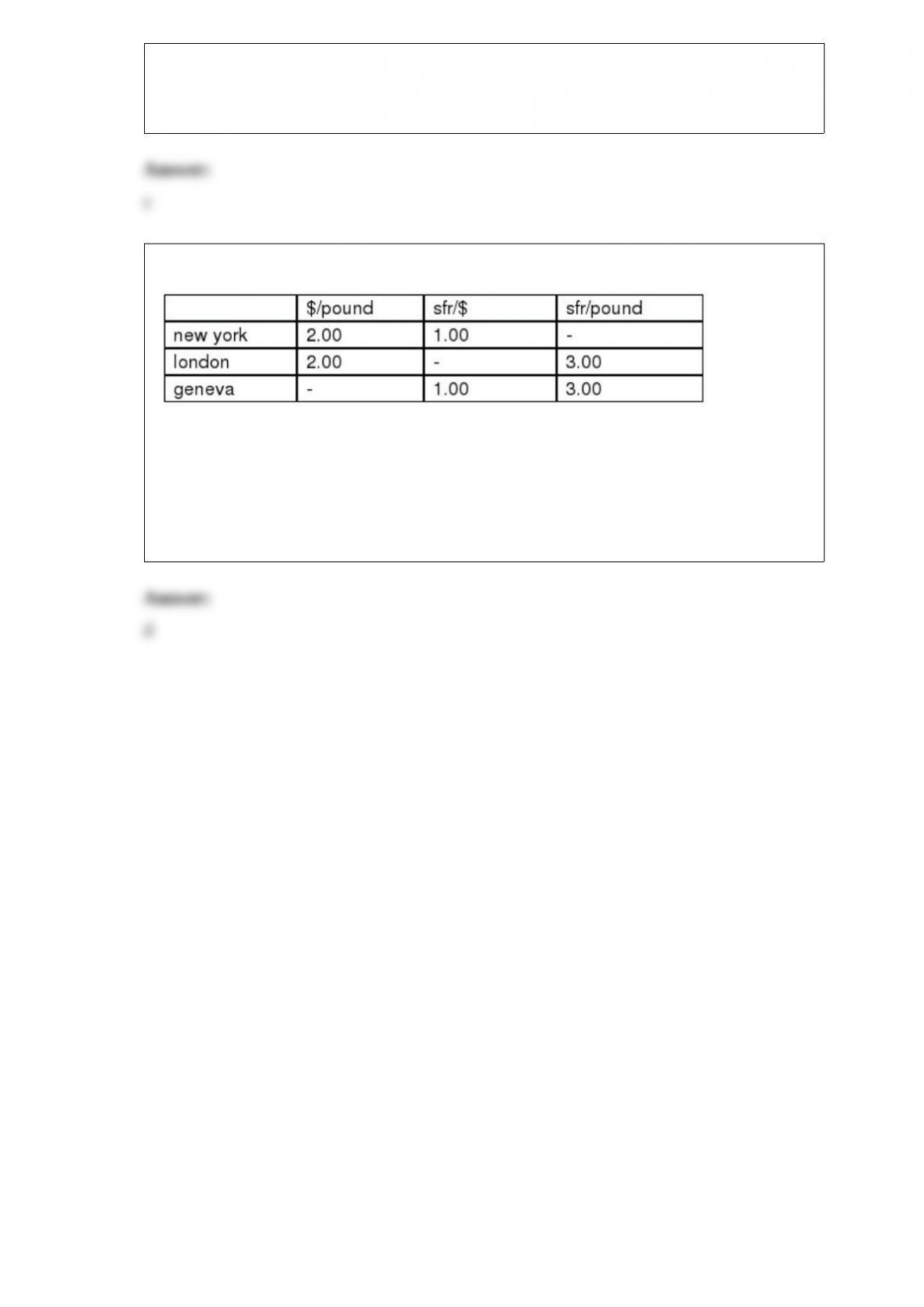

12) assume that the following exchange rates exist.

suppose that you are an arbitrageur that starts with $100 in new york. which of the

following paths is correct in order to make arbitrage profit?

a.buy pound in new york sell pound for sfr in new york sell sfr for dollar in new york

b.buy sfr in new york sell sfr for pound in new york sell pound for dollar in new york

c.buy sfr in new york sell sfr for pound in geneva sell pound for dollar in new york

d.buy pound in new york sell pound for sfr in london sell sfr for dollar in new york