1) a centralized cash pool assists in reducing the problem of mislocated funds and in

funds mobilization.

2) many of the skills necessary for effective cash management are the same regardless

of whether the firm has only domestic operations or if it operates internationally.

3) a multilateral netting system is beneficial in reducing the number of and the expense

associated with interaffiliate foreign exchange transactions.

4) shareholders of u.s. targets experience higher wealth gains when they are acquired by

foreign firms than when acquired by u.s. firms.

5) forfaiting meets islamic finance practices.

6) in a dealer market, the broker takes the trade through the dealer, who participates in

trades as a principal by buying and selling the security for his own account.

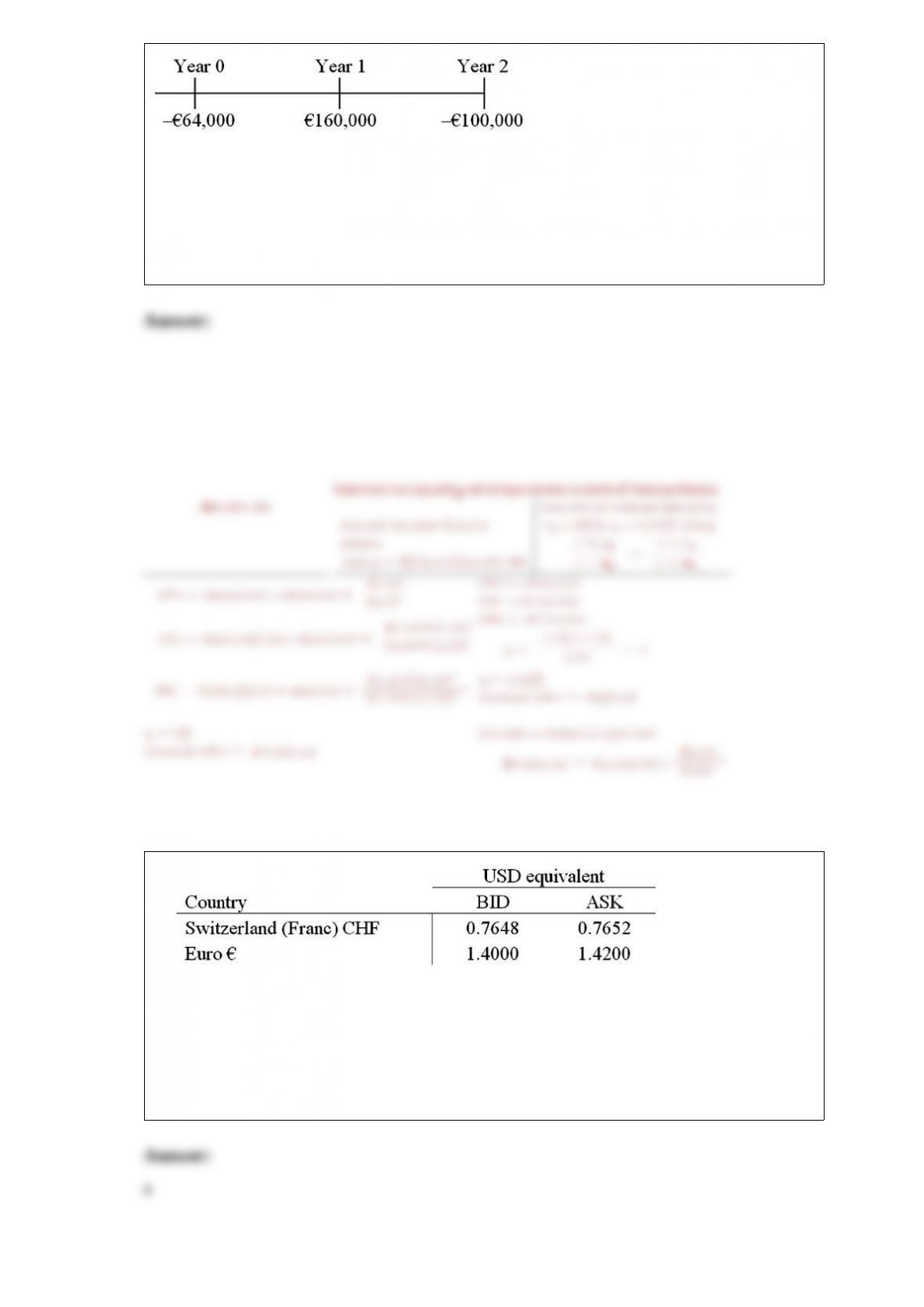

7) consider the following international investment opportunity. it involves a gold mine

that can be opened at a cost, then produces a positive cash flow, but then requires

environmental clean-up:

the current exchange rate is $1.60 = 1.00. the inflation rate in the u.s. is 6 percent and in

the euro zone 2 percent. the appropriate cost of capital to a u.s.-based firm for a

domestic project of this risk is 8 percent.

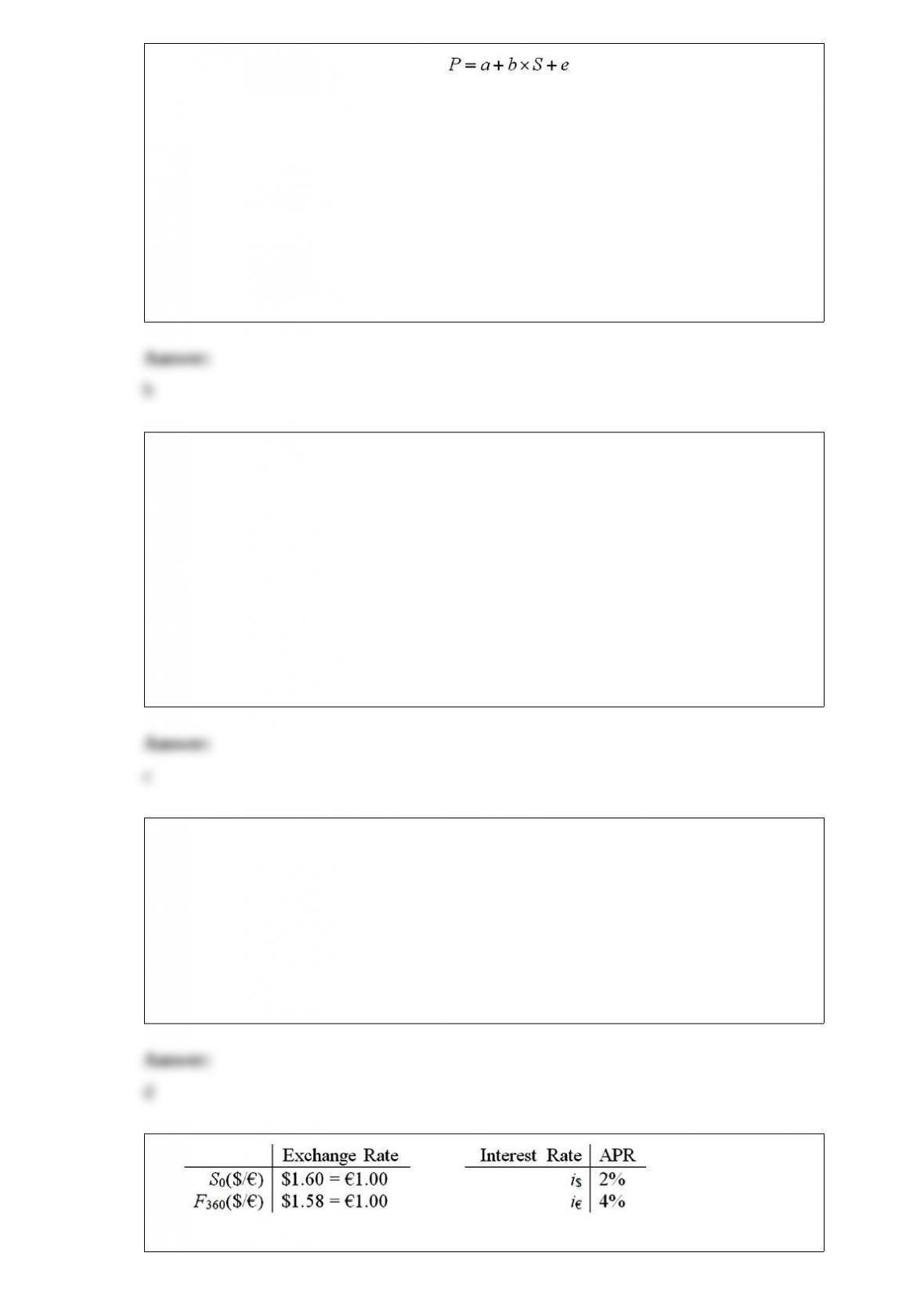

find the euro-zone cost of capital to compute is the dollar-denominated npv of this

project.

8)

find the no-arbitrage cross exchange rate. the dollar-euro exchange rate is quoted as

$1.60 = 1.00 and the dollar-pound exchange rate is quoted at $2.00 = £1.00.

a.1.25/£1.00

b.$1.25/£1.00

c.£1.25/1.00

d.0.80/£1.00

9) a subsidiary bank is

a.a locally incorporated bank that is wholly owned by a foreign parent

b.a locally incorporated bank that is majority owned by a foreign parent

c.a locally incorporated bank that is partially owned (but not controlled) by a foreign

parent

d.both a and b

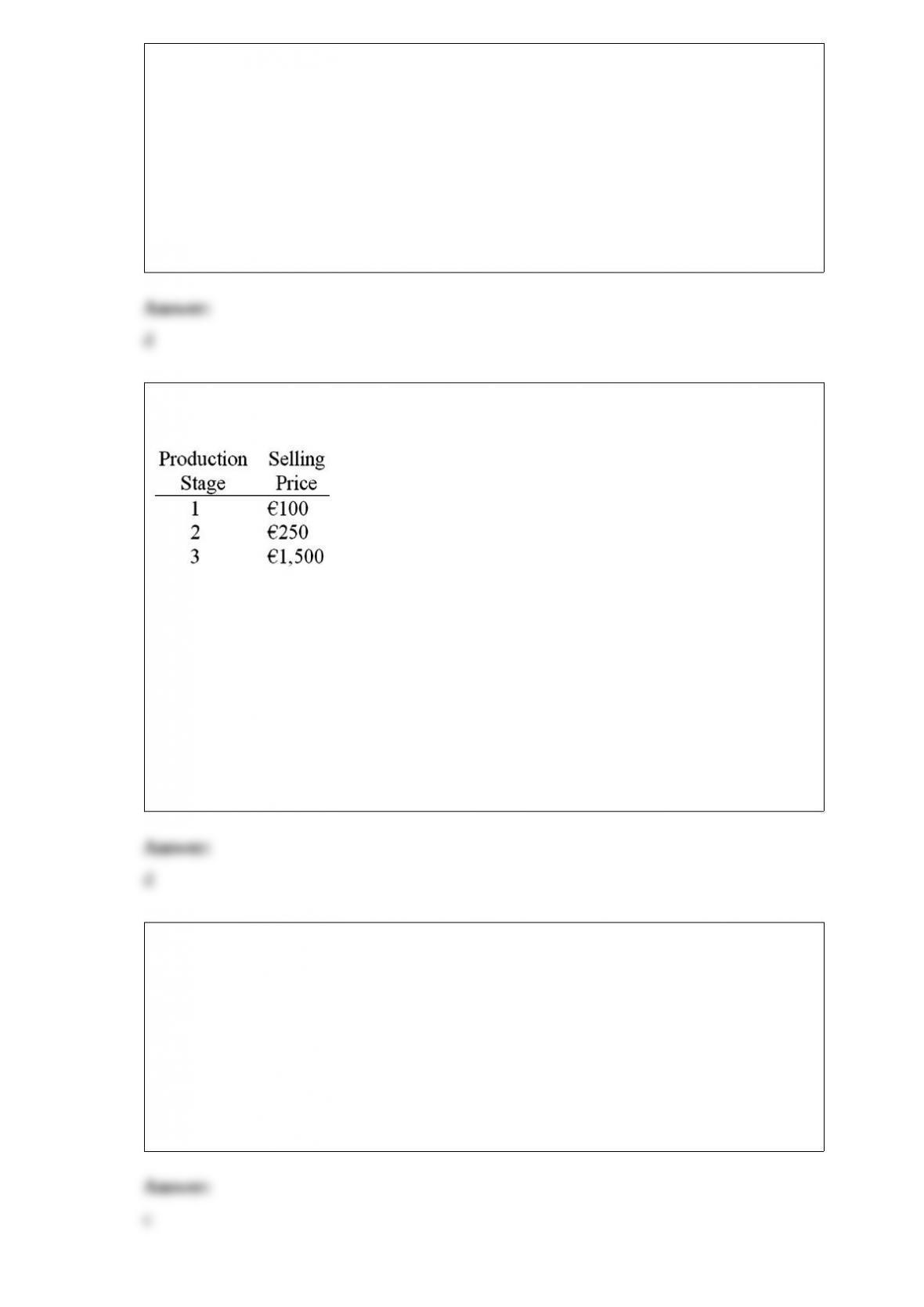

10) assume that a product has the following three stages of production:

if the value-added tax (vat) rate is 15%, what would be the vat over all stages of

production?

a.90

b.120

c.465

d.225

11) debt can reduce agency costs between shareholders and management, but

a.only if the firm is totally up to its eyeballs in debt

b.only to the extent that the firm can commit all of its free cash flow

c.excessive debt can create its own agency conflicts

d.debt is best used as a corporate governance mechanism by young companies with

limited cash reserves

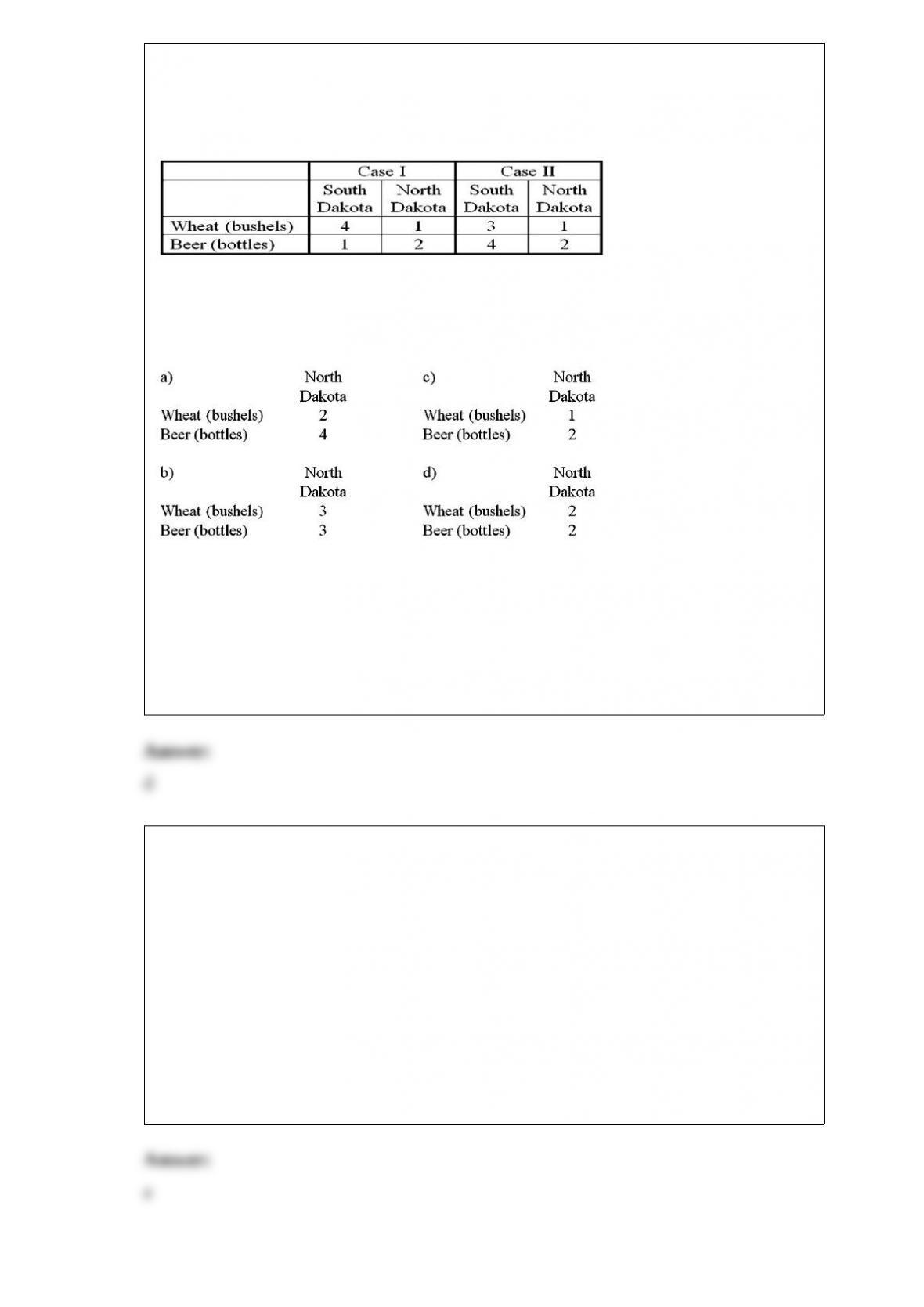

12) the table below shows the bushels of wheat and the bottles of beer that north and

south dakota can produce per day of labor under two different hypothetical situations

(cases i and ii).

for case ii, let the international price be 1 bottle = 1 bushel. derive north dakota’s

“trading possibilities curve.”

a.option a

b.option b

c.option c

d.option d

13) yesterday, you entered into a futures contract to buy 62,500 at $1.50/. your initial

margin was $3,750 (= 0.04 62,500 $1.50/ = 4 percent of the contract value in dollars).

your maintenance margin is $2,000 (meaning that your broker leaves you alone until

your account balance falls to $2,000). at what settle price (use 4 decimal places) do you

get a margin call?

a.$1.4720/

b.$1.5280/

c.$1.500/

d.none of the above

14) solnik (1984) examined the effect of exchange rate changes, interest rate

differentials, the level of the domestic interest rate, and changes in domestic inflation

expectations. he found that

a.international monetary variables had only weak influence on equity returns in

comparison to domestic variables

b.international monetary variables had a stronger influence on equity returns in

comparison to domestic variables

c.international monetary variables had no influence at all on equity returns

d.none of the above

15) adler and simon (1986) examined the exposure of a sample of foreign equity and

bond index returns to exchange rate changes. they found that

a.changes in exchange rates generally explained a smaller portion of the variability of

foreign bond indexes than foreign equity indexes

b.changes in exchange rates generally explained none of the variability of foreign bond

indexes but completely explained the variability in foreign equity indexes

c.changes in exchange rates generally explained a larger portion of the variability of

foreign equity indexes than foreign bond indexes

d.changes in exchange rates generally explained a larger portion of the variability of

foreign bond indexes than foreign equity indexes

16) suppose you observe a spot exchange rate of $1.50/. if interest rates are 5% apr in

the u.s. and 3% apr in the euro zone, what is the no-arbitrage 1-year forward rate?

a.1.5291/$

b.$1.5291/

c.1.4714/$

d.$1.4714/

17) on the basis of regression equation we can decompose the

variability of the dollar value of the asset, var(p), into two separate components.

a.cov(p,s) = b2 var(p) + var(s)

b.var(p) = b2 var(s) + var(e)

c.cov(p,s) = b2 cov(s,p) + cov(s,e)

d.var(p) = b2 var(s)

e.none of the above

18) suppose that the exchange rate is 1.25 = £1.00.

options (calls and puts) are available on the london exchange in units of 10,000 with

strike prices of £0.80 = 1.00.

options (calls and puts) are available on the frankfurt exchange in units of £10,000 with

strike prices of 1.25 = £1.00.

for an italian firm to hedge a £100,000 payable,

a.buy 10 call options on the pound with a strike in euro

b.buy 8 put options on the euro with a strike in pounds

c.both a and b will work

d.simultaneously use strategies a and b

e.none of the above

19) the public corporation has a key weakness:

a.the conflicts of interest between bondholders and shareholders

b.the conflicts of interest between managers and bondholders

c.the conflicts of interest between stakeholders and shareholders

d.the conflicts of interest between managers and shareholders

20)

please note that your answers are worth zero points if they do not include currency

symbols ($, )

if you had 1,000,000 and traded it for usd at the spot rate, how many usd will you get?

21) calculate the euro-based return an italian investor would have realized by investing

10,000 into a $50 american stock. one year after investment, the stock has no value

since the firm is bankrupt. meanwhile the exchange rate has changed from .625 per

dollar to .6875 per dollar, and he sold $16,000 forward at the forward rate of .65 per

dollar.

22) calculate the euro-based return an italian investor would have realized by investing

10,000 into a $50 american stock. one year after investment, the stock pays a $1

dividend, and sells for $54 the exchange rate has changed from .625 per dollar to .6875

per dollar, although he sold $16,000 forward at the forward rate of .65 per dollar.

23) in 1963, president john kennedy imposed the interest equalization tax (iet) on u.s.

purchases of foreign securities. the iet was designed to

a.decrease the cost of foreign borrowing in the u.s. bond market

b.increase the cost of foreign borrowing in the u.s. bond market

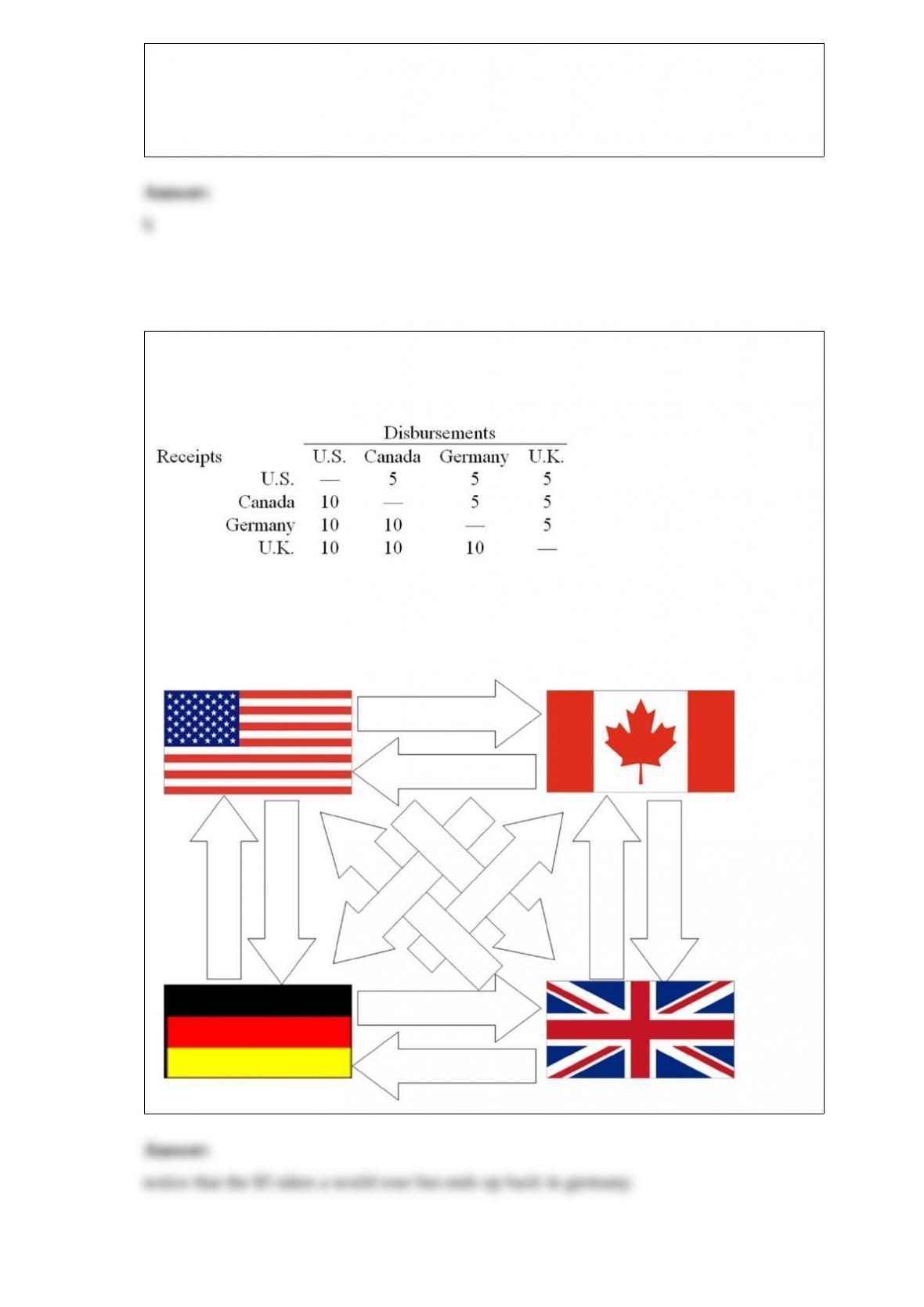

24) your firm’s interaffiliate cash receipts and disbursements matrix is shown below

($000):

using your results to the last question, use multilateral netting to simplify.