1) forward contracts are marked to market daily.

2) provision for loan losses, net charge-offs, and the percentage of nonperforming loans

all increased dramatically in 2007 .

3) the lower the level of interest rates, the greater a bond’s price sensitivity to interest

rate changes.

4) futures contracts are not subject to capital requirements for banks, but many forward

contracts are.

5) a borrower using a conventional mortgage will have to put up at least a 20% down

payment or purchase private mortgage insurance.

6) which one of the following statements about venture capitalists is not correct?

a.venture capitalists contribute to equity financing rather than make loans

b.venture capitalists are passive investors

c.most private venture capitalists are organized as limited partnerships

d.the federal government licenses some private firms to provide lower cost funds to

entrepreneurs

e.angel venture capitalists are wealthy individuals who fund business startups

7) the largest asset category of life insurers is _______________ and the largest liability

category is ___________.

a.bonds; separate account items

b.separate account items; current policy claims

c.bonds; policy reserves

d.policy reserves; mortgage loans

e.common stock; dividend reserve

8) a construction firm cannot obtain the necessary permits to begin building a shopping

mall until it can show it either has or will have the necessary funding to complete the

project. the firm may ask a bank for which of the following to allow it to obtain the

permits?

i. commercial letter of credit

ii. loan commitment

iii. credit line

iv. repurchase agreement

a.i or ii

b.ii or iii

c.ii or iv

d.iii or iv

e.i or iv

9) a macrohedge is a

a.hedge of a particular asset or liability

b.hedge of an entire balance sheet

c.hedge using options

d.hedge without basis risk

e.hedge using futures on macroeconomic variables

10) the fed allowed nonbank financial institutions to borrow money from the discount

window during the mortgage crisis and even allowed nonbanks to swap mortgages for

treasury securities. this was an attempt by the fed to reduce ________________ at

institutions.

a.operational risk

b.technological risk

c.liquidity risk

d.foreign exchange risk

e.diversifiable risk

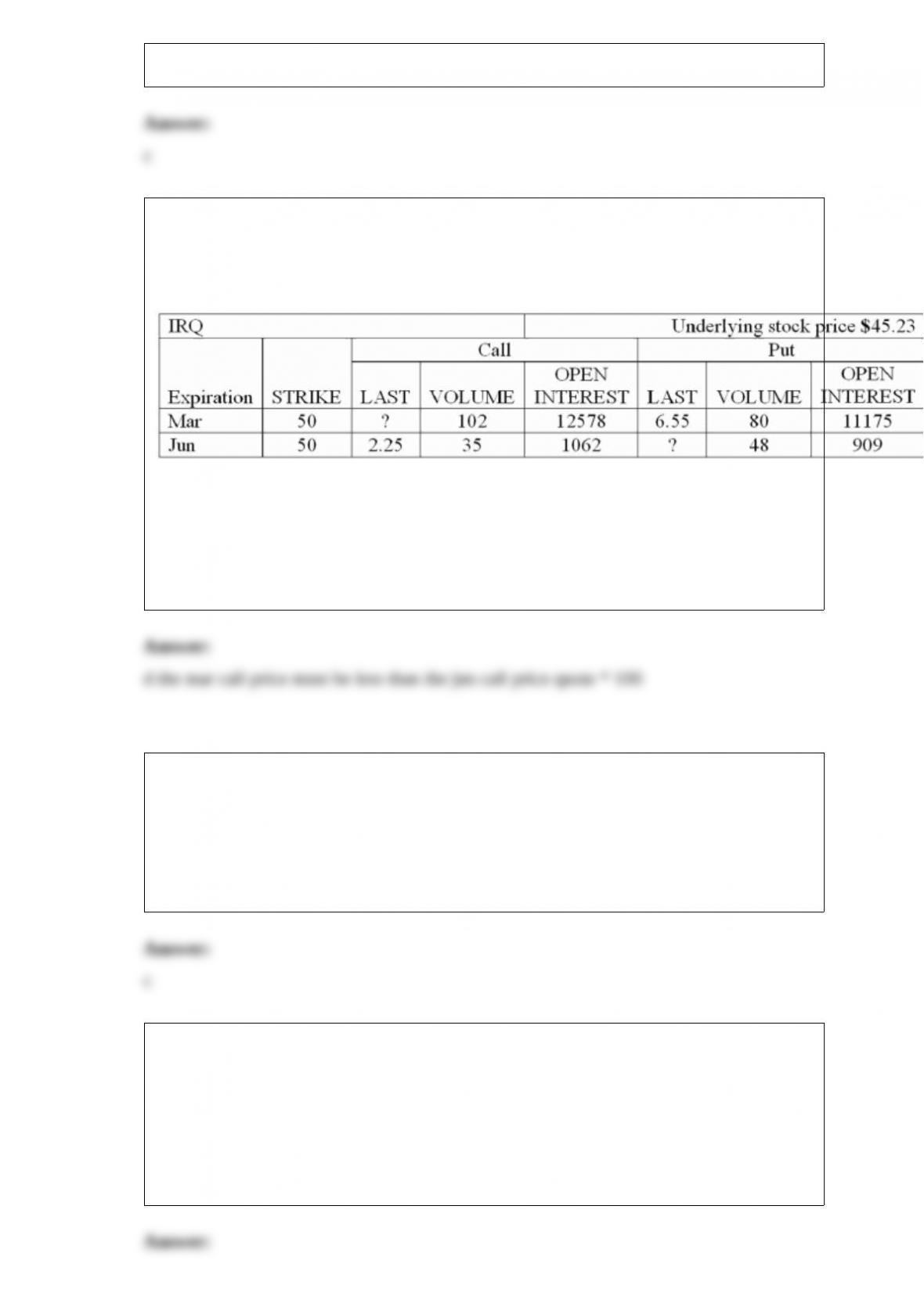

11) refer to the listed stock option price quote from february and assume it is now

january:

figure 10-1

based on the option quote, the mar call should cost

a.more than $477

b.more than $102

c.less than $665 but more than $477

d.less than $225

e.$0

12) requiring foreign banks to operate under the same rules as domestic banks is termed

a.favored status

b.iba clause

c.national treatment

d.nafta

e.post-patriotism requirement

13) basis risk occurs because it is generally impossible to

a.hedge unanticipated rate changes

b.exactly predict interest rate changes

c.exactly match the terms of the hedging instrument with the terms of the asset or

liability at risk

d.find negatively correlated asset prices

e.all of the above

14) a thrift makes long-term fixed-rate mortgages funded with short-term deposits and

then interest rates rise. which of the following is true?

a.profitability would decline

b.profitability would increase

c.the market value of equity increases

d.interest income would fall

e.both b and c would occur

15) in property and casualty insurance the combined ratio is equal to the

______________________ divided by total premiums written.

a.sum of the loss ratio plus loss adjustment expenses

b.sum of the loss ratio plus general expenses and broker’s commissions

c.operating ratio minus dividends paid to policyholders

d.nominal ratio plus real ratio

e.1 minus operating ratio

16) an investor starts with $1 million and converts it to 0.75 million pounds, which is

then invested for one year. in a year the investor has 0.7795 million pounds, which she

then converts to dollars at an exchange rate of 0.72 pounds per dollar. the u.s. dollar

annual rate of return earned was _____.

a.4.97%

b.5.27%

c.6.45%

d.7.69%

e.8.26%

17) duration is

a.the elasticity of a security’s value to small coupon changes

b.the weighted average time to maturity of the bond’s cash flows

c.the time until the investor recovers the price of the bond in today’s dollars

d.greater than maturity for deep discount bonds and less than maturity for premium

bonds

e.the second derivative of the bond price formula with respect to the ytm

18) a bank is using the raroc to evaluate large business loans. the benchmark rate of

return is 7.55%. the 1-year loan interest rate is 8.00% and the bank must pay 7.40% to

raise the funds. the cost to service the loan is 0.3%. if the loan defaults, 92% of the

money lent will be lost. based on historical default rates, the extreme worst-case loss

scenario is about 5%. should the bank make the loan? why or why not?

a.yes, because the raroc is 7.11%

b.no, because the raroc is 7.11%

c.yes, because the raroc is 6.52%

d.no, because the raroc is 6.52%

e.no, because the raroc is more than 7.55%

19) you can buy or sell the £ spot at $1.98 to the pound. you can buy or sell the pound

one-year forward at $2.01 to the pound. if u.s. annual interest rates are 5%, what must

be the approximate one-year british interest rate if interest rate parity holds?

a.4.00%

b.5.25%

c.2.75%

d.3.48%

e.5.65%

20) the process of packaging and/or selling mortgages which are then used to back

publicly traded debt securities is called

a.collateralization

b.securitization

c.market capitalization

d.stock diversification

e.mortgage globalization

21) the greater the _________________ ratio the more liquid is the institution, ceteris

paribus.

a.borrowed funds to total assets

b.core deposits to total assets

c.loans to deposits

d.unused commitments to lend to total assets

e.unused commitments to lend to liquid assets

22) a pass-through security is best characterized as

a.a multiclass mortgage-backed bond

b.a security with a pro rata claim to the underlying pool of assets

c.a bond backed by real estate

d.a part of a loan assignment

e.a part of a loan participation

23) figure 21-1

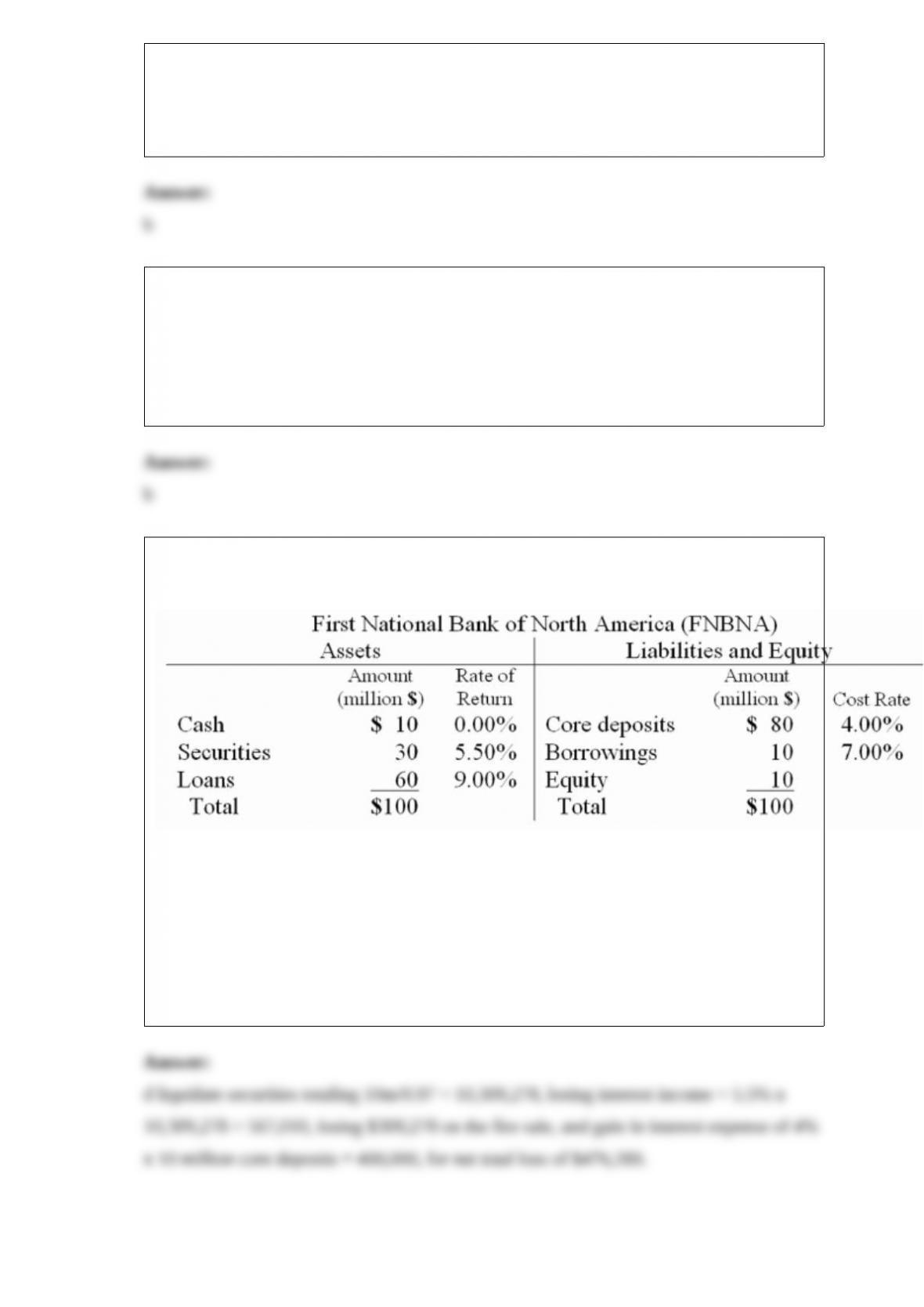

if fnbna is expecting a $10 million net deposit drain and the securities liquidity index is

0.97, by how much will pre-tax net income change if the drain is funded entirely

through securities sales?

a.-$306,122

b.-$150,000

c.-$375,339

d.-$476,289

e.-$474,490

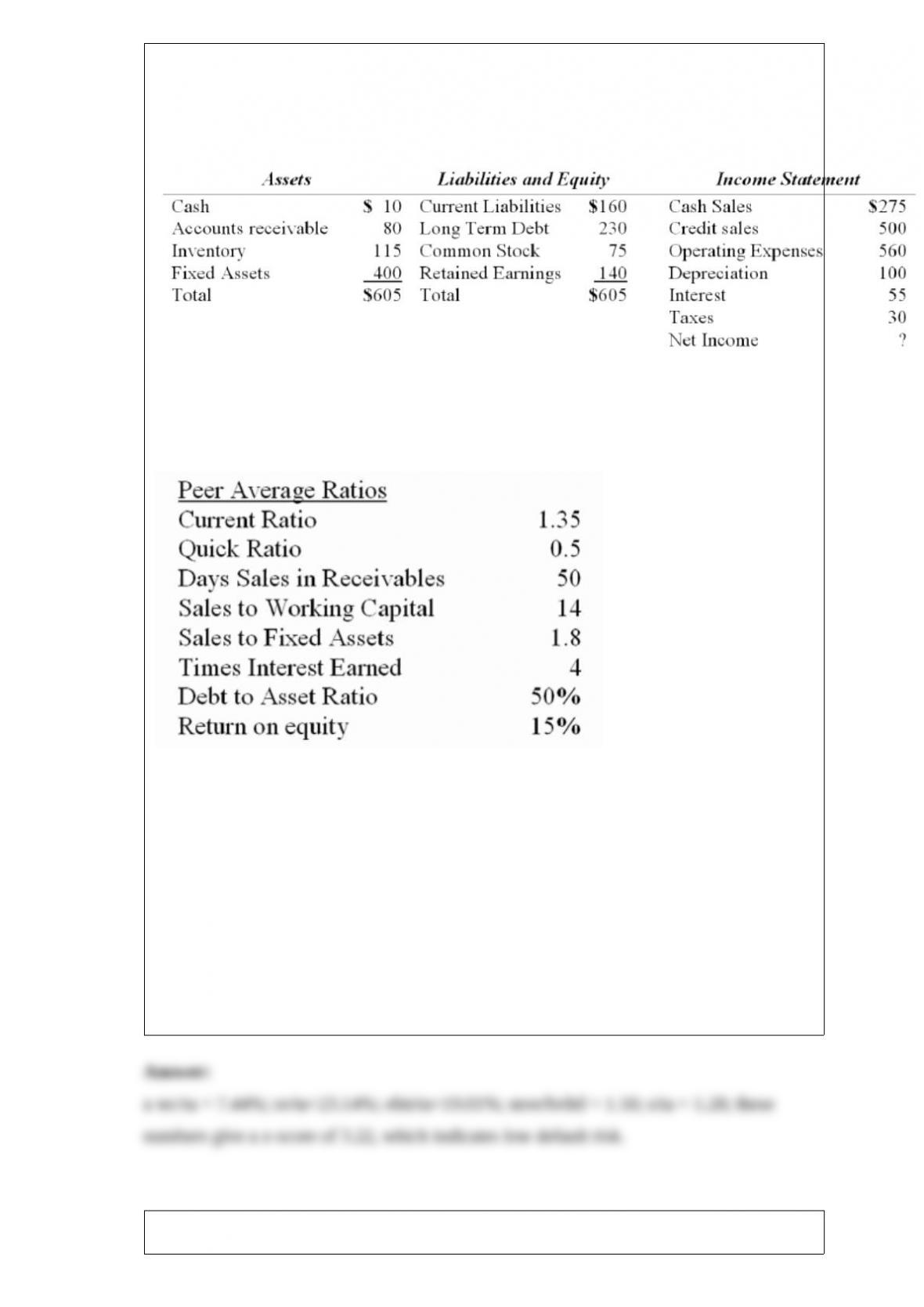

24) figure 20-2

balance sheet big valley enterprises

interest is big valley’s only fixed cash charge.

big valley’s market value of equity to book value of debt ratio = 1.5

altman’s z-score model is z = 1.2×1 + 1.4×2 + 3.3×3 + 0.6×4 + 1.0×5

x1 = working capital/total assets

x2 = retained earnings/total assets

x3 = ebit/total assets

x4 = market value equity/book value long-term debt

x5 = sales/total assets

using the altman’s z model, big valley’s z-score is

a.3.22

b.2.88

c.2.65

d.2.11

e.1.85

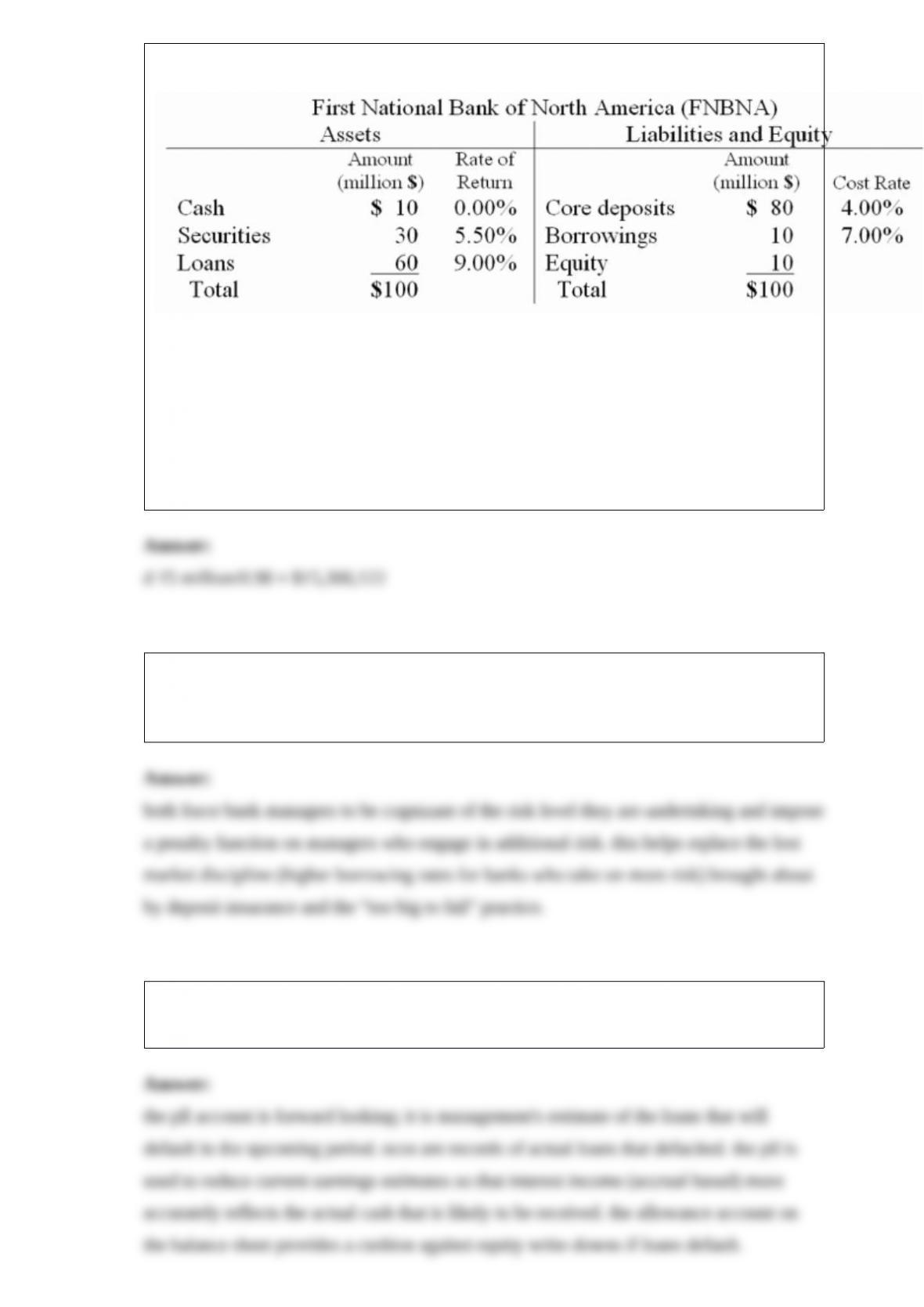

25) figure 21-1

if fnbna is expecting a $15 million net deposit drain and the securities liquidity index is

0.98, how many securities would have to be liquidated if the bank used only its

securities to fund the expected deposit drain?

a.$15,000,000

b.$16,444,331

c.$15,600,000

d.$15,306,122

e.$16,772,345

26) how do risk-based deposit insurance premiums and risk-based capital requirements

help reduce the moral hazard problem of deposit insurance? (hint: moral hazard means

that because of deposit insurance, banks may take on excessive amounts of risk.)

27) what is the difference between net charge-offs (sometimes called write-offs) and the

provision for loan loss? what is the purpose of the provision for loan loss account?

28) what do bond rating agencies look at in setting a bond’s rating?

29) suppose that oil prices hit an all-time high of $200 a barrel, driving u.s. inflation up

to 7% per year. at the same time, weak u.s. growth and increasing foreign competition

has generated unacceptably high levels of unemployment in the united states. you are

the chair of the federal reserve. what do you suggest?

30) the roa for financial institutions such as banks is typically quite low as compared to

non-financial firms. why? with such a low roa, how can banks attract stockholders?

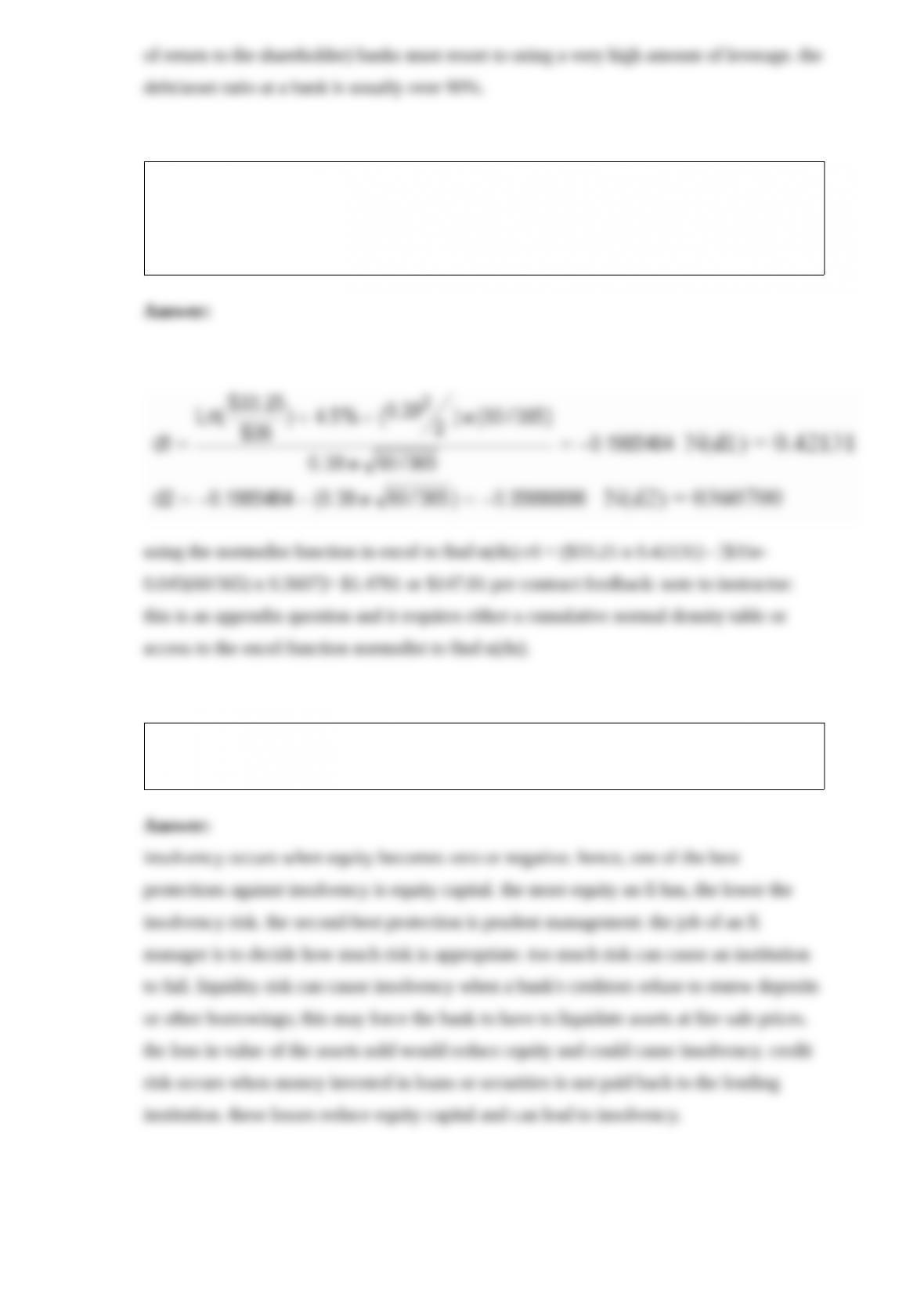

31) a stock is priced at $33.25. the stock has 35 call options that expire in 60 days. the

underlying stock price volatility is 39% per year and the annual risk-free rate is 4.5%.

according to the black-scholes option pricing model, what is the most you should be

willing to pay for this call option?

32) what is insolvency risk? how can liquidity risk and credit risk cause insolvency?

what are the two best protections against insolvency at an fi?