Studies of Siamese twin companies find __________, which __________ the EMH.

A. correct relative pricing; supports

B. correct relative pricing; does not support

C. incorrect relative pricing; supports

D. incorrect relative pricing; does not support

You purchased shares of a mutual fund at a price of $12 per share at the beginning of

the year and paid a front-end load of 4.75%. If the securities in which the fund invested

increased in value by 9% during the year, and the fund’s expense ratio was 1.5%, your

return if you sold the fund at the end of the year would be

A. 4.75%.

B. 3.54%.

C. 2.65%.

D. 2.39%.

The interest rate on a 1-year Canadian security is 7.8%. The current exchange rate is C$

= US $0.79. The 1-year forward rate is C$ = US $0.77. The return (denominated in U.S.

$) that a U.S. investor can earn by investing in the Canadian security is

A. 3.59%.

B. 4.00%.

C. 5.07%.

D. 8.46%.

E. None of the options

Early tests of the CAPM involved

A. establishing sample data.

B. estimating the security characteristic line.

C. estimating the security market line.

D. All of the options are correct.

E. None of the options are correct.

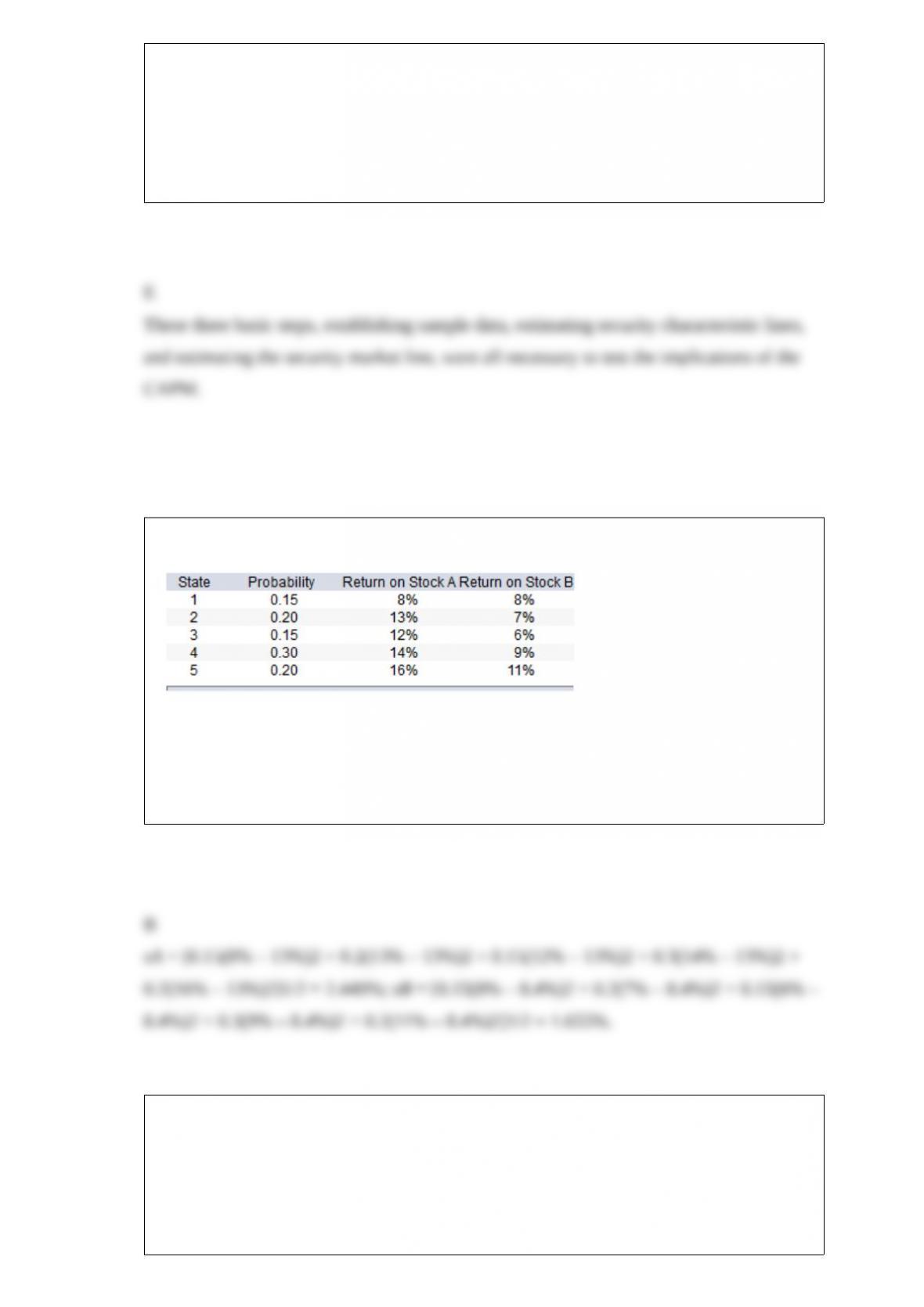

Consider the following probability distribution for stocks A and B:

The standard deviations of stocks A and B are _____ and _____, respectively.

A. 1.56%; 1.99%

B. 2.45%; 1.66%

C. 3.22%; 2.01%

D. 1.54%; 1.11%

If the annual real rate of interest is 5%, and the expected inflation rate is 4%, the

nominal rate of interest would

be approximately

A. 1%.

B. 9%.

C. 20%.

D. 15%.

You want to purchase XON stock at $60 from your broker using as little of your own

money as possible. If initial margin is 50% and you have $3,000 to invest, how many

shares can you buy?

A. 100 shares

B. 200 shares

C. 50 shares

D. 500 shares

E. 25 shares

In words, the covariance considers the probability of each scenario happening and the

interaction between

A. securities’ returns relative to their variances.

B. securities’ returns relative to their mean returns.

C. securities’ returns relative to other securities’ returns.

D. the level of return a security has in that scenario and the overall portfolio return.

E. the variance of the security’s return in that scenario and the overall portfolio

variance.

The efficient frontier of risky assets is

A. the portion of the minimum-variance portfolio that lies above the global minimum

variance portfolio.

B. the portion of the minimum-variance portfolio that represents the highest standard

deviations.

C. the portion of the minimum-variance portfolio that includes the portfolios with the

lowest standard deviation.

D. the set of portfolios that have zero standard deviation.

The expected return-beta relationship

A. is the most familiar expression of the CAPM to practitioners.

B. refers to the way in which the covariance between the returns on a stock and returns

on the market measures

the contribution of the stock to the variance of the market portfolio, which is beta.

C. assumes that investors hold well-diversified portfolios.

D. All of the options are true.

E. None of the options are true.

Consider the Treynor-Black model. The alpha of an active portfolio is 2%. The

expected return on the market

index is 12%. The variance of the return on the market portfolio is 4%. The

nonsystematic variance of the active

portfolio is 2%. The risk-free rate of return is 3%. The beta of the active portfolio is

1.15. The optimal proportion

to invest in the active portfolio is

A. 48.7%.

B. 98.3%.

C.47.6%.

D. 100.0%.

______ can occur if _____.

A. Arbitrage; the law of one price is not violated

B. Arbitrage; the law of one price is violated

C. Low-risk economic profit; the law of one price is not violated

D. Low-risk economic profit; the law of one price is violated

E. Arbitrage and low-risk economic profit; the law of one price is violated

If the index model is valid, _________ would be helpful in determining the covariance

between assets K and L.

A. βk

B. βL

C. σM

D. all of the options

E. None of the options are correct.

Using the S&P 500 portfolio as a proxy of the market portfolio

A. is appropriate because U.S. securities represent more than 60% of world equities.

B. is appropriate because most U.S. investors are primarily interested in U.S. securities.

C. is appropriate because most U.S. and non-U.S. investors are primarily interested in

U.S. securities.

D. is inappropriate because U.S. securities make up less than 41% of world equities.

E. is inappropriate because the average U.S. investor has less than 20% of his or her

portfolio in non-U.S. equities.

Sehun (1986) finds that the practice of monitoring insider trade disclosures, and trading

on that information, would be

A. extremely profitable for long-term traders.

B. extremely profitable for short-term traders.

C. marginally profitable for long-term traders.

D. marginally profitable for short-term traders.

E. not sufficiently profitable to cover trading costs.

Consider a T-bill with a rate of return of 5% and the following risky securities:

Security A: E(r) = 0.15; Variance = 0.04

Security B: E(r) = 0.10; Variance = 0.0225

Security C: E(r) = 0.12; Variance = 0.01

Security D: E(r) = 0.13; Variance = 0.0625

From which set of portfolios, formed with the T-bill and any one of the four risky

securities, would a risk-averse

investor always choose his portfolio?

A. The set of portfolios formed with the T-bill and security A.

B. The set of portfolios formed with the T-bill and security B.

C. The set of portfolios formed with the T-bill and security C.

D. The set of portfolios formed with the T-bill and security D.

E. Cannot be determined.

Over the period 2011-2016, most correlations between the U.S. stock index and

stock-index portfolios of other countries were

A. negative.

B. positive but less than .9.

C. approximately zero.

D. .9 or above.

E. None of the options are correct.

Assume you purchased 200 shares of GE common stock on margin at $70 per share

from your broker. If the initial margin is 55%, how much did you borrow from the

broker?

A. $6,000

B. $4,000

C. $7,700

D. $7,000

E. $6,300

An analyst has determined that the intrinsic value of IBM stock is $80 per share using

the capitalized earnings model. If the typical P/E ratio in the computer industry is 22,

then it would be reasonable to assume the expected EPS of IBM in the coming year is

A. $3.64.

B. $4.44.

C. $14.40.

D. $22.50.

Del Guerico and Reuter (2014) report that the average underperformance of

actively-managed mutual funds is driven largely by

A. sector mutual funds.

B. index funds.

C. direct-sold funds.

D. broker-sold funds.

E. bank-sold mutual funds.

Consider a bond selling at par with modified duration of 12 years and convexity of 265.

A 1% decrease in yield would cause the price to increase by 12%, according to the

duration rule. What would be the percentage price change according to the

duration-with-convexity rule?

A. 21.2%

B. 25.4%

C. 17.0%

D. 13.3%

Mortgage-backed securities were created when ________ began buying mortgage loans

from originators and bundling them into large pools that could be traded like any other

financial asset.

A. GNMA

B. FNMA

C. FHLMC

D. FNMA and FHLMC

E. GNMA and FNMA

The interest rate charged by banks with excess reserves at a Federal Reserve Bank to

banks needing overnight loans to meet reserve requirements is called the

A. prime rate.

B. discount rate.

C. federal funds rate.

D. call money rate.

E. money market rate.

Which one of the following statements regarding open-end mutual funds is false?

A. The funds redeem shares at net asset value.

B. The funds offer investors professional management.

C. The funds offer investors a guaranteed rate of return.

D. The funds redeem shares at net asset value and offer investors professional

management.

Which one of the following par-value 12% coupon bonds experiences a price change of

$23 when the market yield changes by 50 basis points?

A. The bond with a duration of 6 years

B. The bond with a duration of 5 years

C. The bond with a duration of 2.7 years

D. The bond with a duration of 5.15 years

Which of the following two bonds is more price sensitive to changes in interest rates?

1) A par-value bond, D, with a 2 year to maturity and an 8% coupon rate.

2) A zero-coupon bond, E, with a 2 year to maturity and an 8% yield to maturity.

A. Bond D because of the higher yield to maturity

B. Bond E because of the longer duration

C. Bond D because of the longer time to maturity

D. Both have the same sensitivity because both have the same yield to maturity.

In 2016, the proportion of hybrid (bond and stock) mutual funds (based on total assets)

was

A. 21.7%.

B. 28.0%.

C. 54.1%.

D. 8.5%.

E. 22.6%.

A _________ portfolio is a well-diversified portfolio constructed to have a beta of 1 on

one of the factors and a beta of 0 on any other factor.

A. factor

B. market

C. index

D. factor and market

E. factor, market, and index

Assume that a security is fairly priced and has an expected rate of return of 0.17. The

market expected rate of

return is 0.11, and the risk-free rate is 0.04. The beta of the stock is

A. 1.25.

B. 1.86.

C. 1.

D. 0.95.

A mutual fund had year-end assets of $521,000,000 and liabilities of $63,000,000. If the

fund NAV was $26.12, how many shares must have been held in the fund?

A. 17,534,456

B. 16,488,372

C. 18,601,742

D. 17,542,515

Suppose two portfolios have the same average return and the same standard deviation

of returns, but Buckeye Fund has a higher beta than Gator Fund. According to the

Treynor measure, the performance of Buckeye Fund

A. is better than the performance of Gator Fund.

B. is the same as the performance of Gator Fund.

C. is poorer than the performance of Gator Fund.

D. cannot be measured as there are no data on the alpha of the portfolio.

E. None of the options are correct.

If a portfolio manager consistently obtains a high Sharpe measure, the manager’s

forecasting ability

A.is above average.

B. is average.

C. is below average.

D. does not exist.

E. cannot be determined based on the Sharpe measure.

Which of the following indices is(are) market-value weighted?

I) The New York Stock Exchange Composite Index

II) The Standard and Poor’s 500 Stock Index

III) The Dow Jones Industrial Average

A. I only

B. I and II only

C. I and III only

D. I, II, and III

E. II and III only

Financial futures contracts are actively traded on the following indices except

A. the All ordinary index.

B. the DAX 30 Index.

C. the CAC 40 Index.

D. the Toronto 35 Index.

E. All of the options are correct.

The beta of Exxon stock has been estimated as 1.6 using regression analysis on a

sample of historical returns. A commonly-used adjustment technique would provide an

adjusted beta of

A. 1.20.

B. 1.32.

C. 1.13.

D. 1.40.