1) Exhibit 22.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for Citigroup

A long straddle is an appropriate strategy if

a. An investor wishes to generate additional income.

b. An investor wished to insure against a decline in share values.

c. An investor expected share prices to be volatile.

d. An investor expected share prices to remain in a trading range.

e. An investor expected share prices to be volatile, but was inclined to be bullish.

2) Exhibit 20.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

December futures on the S&P 500 stock index trade at 250 times the index value of

1187.70. Your broker requires an initial margin of 10% percent on futures contracts.

The current value of the S&P 500 stock index is 1178.

How much must you deposit in a margin account if you wish to purchase one contract?

a. $267,232.5

b. $29,450

c. $29,692.50

d. $30,000

e. $265,050

3) Given Gitech’s beta of 1.55 and a risk free rate of 8 percent, what is the expected rate

of return assuming a 14 percent market return?

a. 12.4%

b. 14.3%

c. 17.3%

d. 20.4%

e. 29.7%

4) If interest rates increase due to inflation, but expected cash flows to a firm do not

change, then you would expect stock prices to

a. Rise.

b. Rise and then decline.

c. Remain unchanged.

d. Decline.

e. None of the above.

5) Consider a bond with a current yield of 8% and a price of $1,250. What is this bond’s

coupon?

a. 8.0%

b. 10.0%

c. 11.0%

d. 8.5%

e. 9.6%

6) Unlike the capital asset pricing model, the arbitrage pricing theory requires only the

following assumption(s):

a. A quadratric utility function.

b. Normally distributed returns.

c. The stochastic process generating asset returns can be represented by a factor model.

d. A mean-variance efficient market portfolio consisting of all risky assets.

e. All of the above

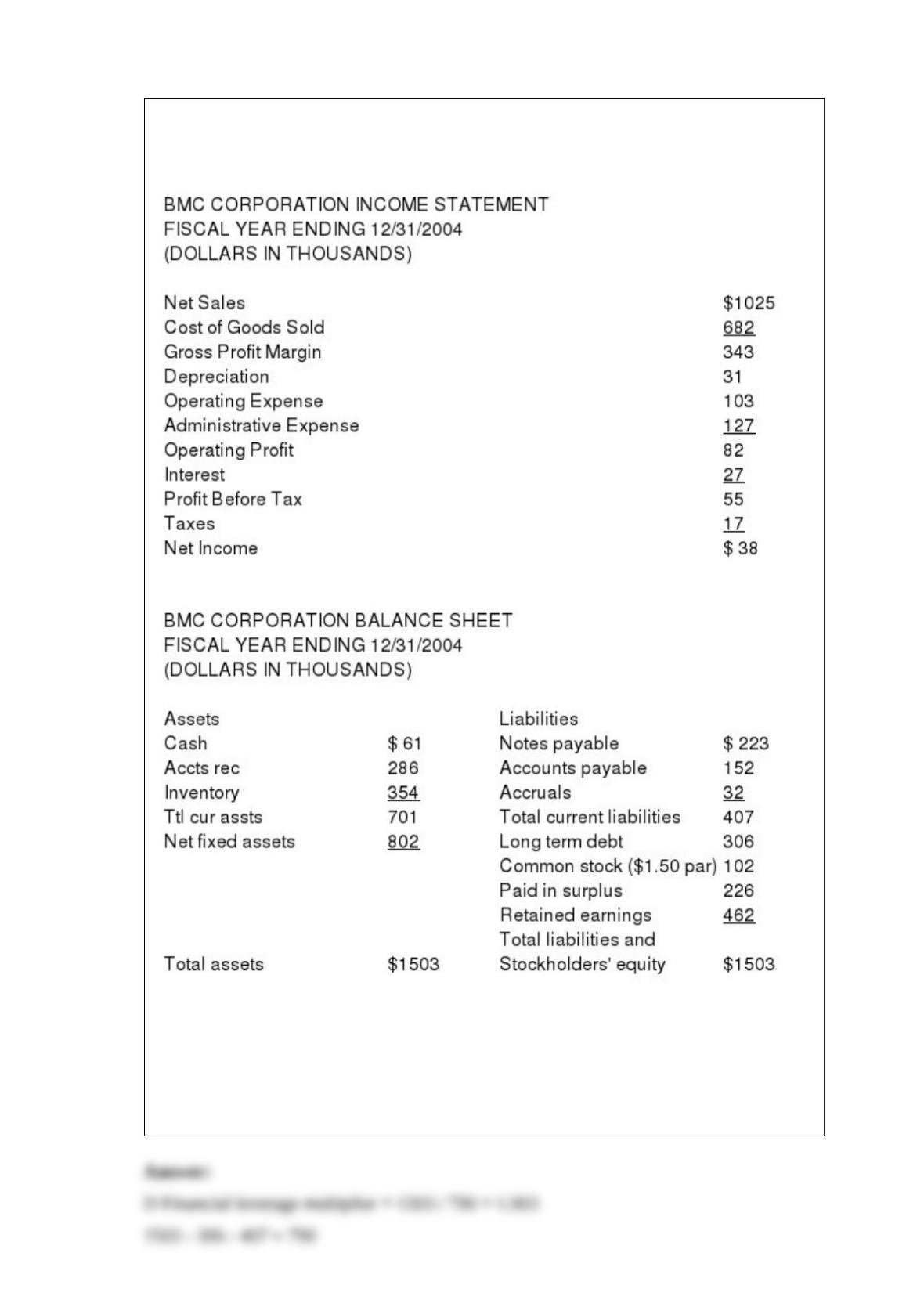

7) Exhibit 10.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

What was the financial leverage multiplier used in the BMC system?

a. 2.058

b. 2.289

c. 3.014

d. 1.903

e. 0.904

8) When the 50 day moving average crosses the 200 day moving average from ____ on

____ volume, this would be a ____ signal.

a. Above, low, bullish.

b. below, high, bearish.

c. below, low, bullish.

d. above, high, bullish.

e. below, high, bullish.

9) When individuals evaluate their portfolios they should evaluate

a. All the U.S. and non-U.S. stocks.

b. All marketable securities.

c. All marketable securities and other liquid assets.

d. All assets.

e. All assets and liabilities.

10) A(n) ____ contract is an arrangement whereby the coupon rate on a note moves in

the opposite direction of some variable rate index.

a. Inverse floating rate

b. Reverse floating rate

c. Backward floating rate

d. Opposing floating rate

e. Defensive floating rate

11) Calculate the expected return for D Industries which has a beta of 1.0 when the risk

free rate is 0.03 and you expect the market return to be 0.13.

a. 8.6%

b. 9.2%

c. 11.0%

d. 12.0%

e. 13.0%

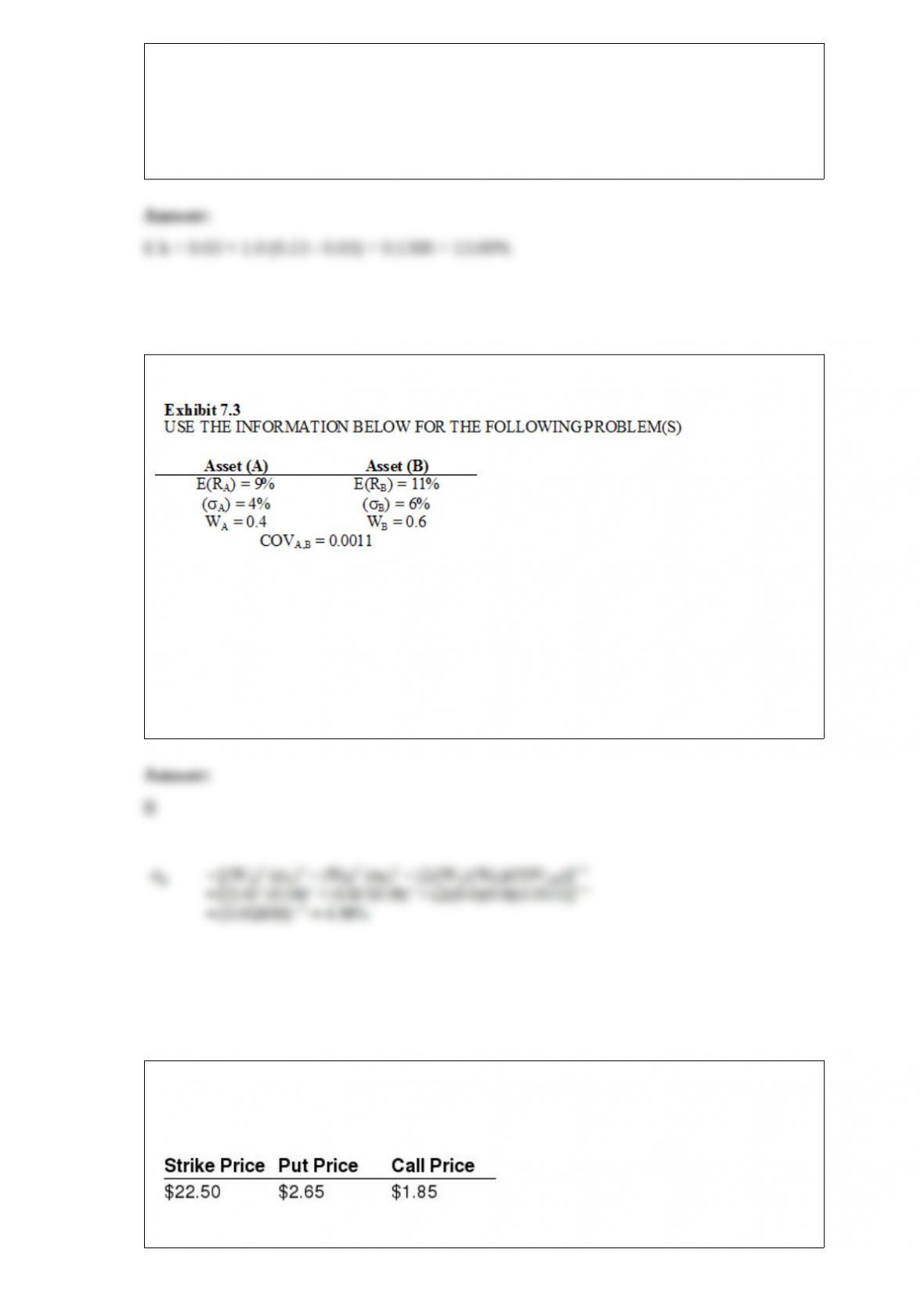

12)

Refer to Exhibit 7.3. What is the standard deviation of this portfolio?

a. 3.68%

b. 4.56%

c. 4.99%

d. 5.16%

e. 6.02%

13) Exhibit 22.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Consider the following information on put and call options for a common stock

Calculate the net value of a covered call position at an expiration stock price of $20.

a. $1.85

b. $4.45

c. $18.15

d. $21.85

e. $24.35

14) Growth stocks would have the following characteristics:

a. Low price/book, high price/earnings.

b. Low price/book, low price/earnings.

c. High EPS growth, high profitability.

d. Low EPS growth, high profitability.

e. None of the above.

15) For an investor with a time horizon of 15 years and moderate risk tolerance, an

appropriate asset allocation strategy would be

a.100% stocks

b.40% cash and 60% stocks

c.30% cash, 50% bonds, and 20% stocks

d.50% bonds, and 50% stocks

e.20% bonds, and 80% stocks

16) In a micro-economic (or characteristic) based risk factor model the following factor

would be one of many appropriate factors:

a. Confidence risk.

b. Maturity risk.

c. Expected inflation risk.

d. Call risk.

e. Return difference between small capitalization and large capitalization stocks.

17) During a recession,

a. Financial stocks rise on expectations of increases in loan demand, housing

constructions and security offerings.

b. Consumer durable stocks rise on expectations of rising consumer confidence and

personal income.

c. Capital goods stocks rise on expectation of increases in business capital spending.

d. Basic materials stocks rise on expectation of rising profit margins.

e. Consumer staple stocks rise on expectations that consumers will continue to spend on

necessities.

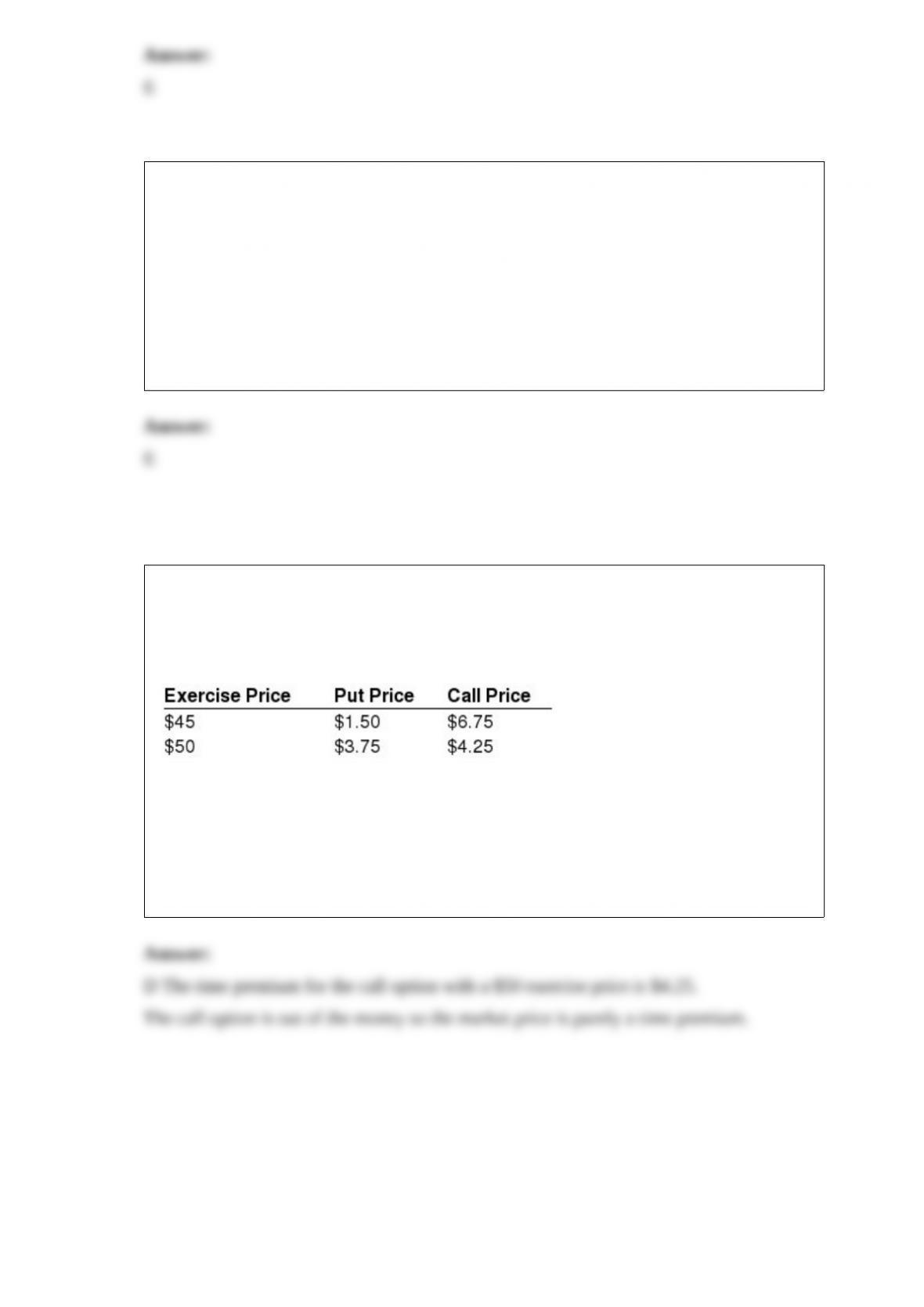

18) Exhibit 20.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The current stock price of Zanco Corporation is $50. Zanco Corporation has the

following put and call option prices with exercise prices at $45 and $50.

The time premium for the call option with a $50 exercise price is

a. $0.00

b. $1.50

c. $1.75

d. $4.25

e. $9.25